Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.90 Billion |

| Market Size (2026) | USD 5.04 Billion |

| Market Size (2031) | USD 5.77 Billion |

| Growth Rate (2026 - 2031) | 2.76% CAGR |

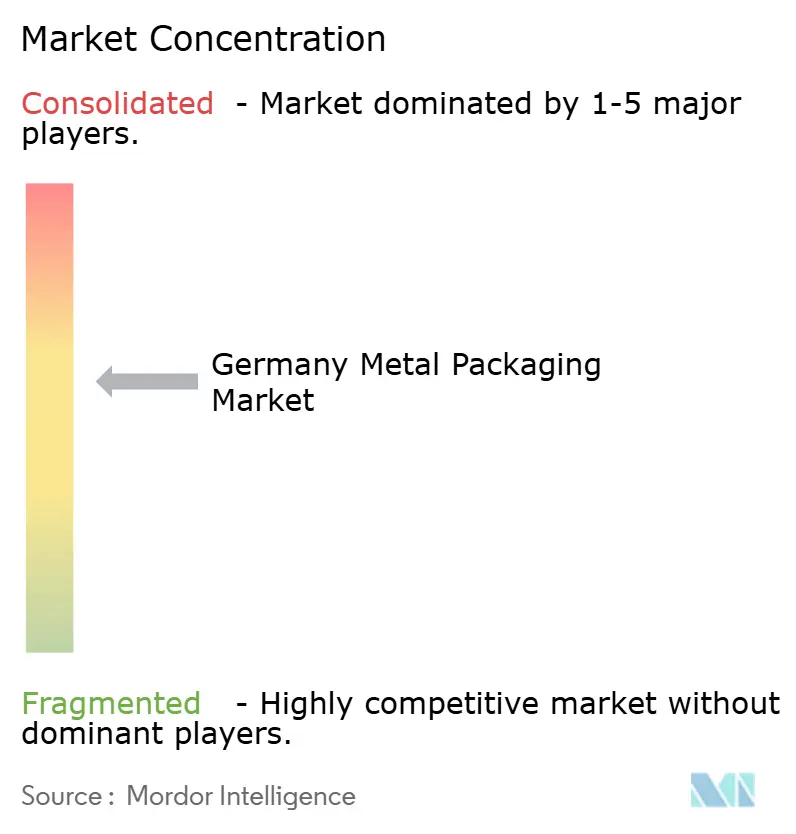

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Metal Packaging Market Analysis by Mordor Intelligence

The Germany metal packaging market size was valued at USD 4.90 billion in 2025 and estimated to grow from USD 5.04 billion in 2026 to reach USD 5.77 billion by 2031, at a CAGR of 2.76% during the forecast period (2026-2031). The growth pace underscores a mature yet resilient environment shaped by circular-economy legislation, Industry 4.0 modernization, and consumer affinity for infinitely recyclable materials. Advances in automated can-forming lines, rising demand from ready-to-drink beverages, and OEM shifts toward monomaterial containers are supporting new volume, whereas base-metal cost swings and high-barrier plastics temper expansion. Crucially, Aluminum’s 64.14% share and steel’s 3.72% CAGR illustrate a dual reality: entrenched dominance and emergent substitution, respectively. Germany’s position as Europe’s largest packaging production hub further entrenches domestic output while providing export leverage into the wider EU.

Key Report Takeaways

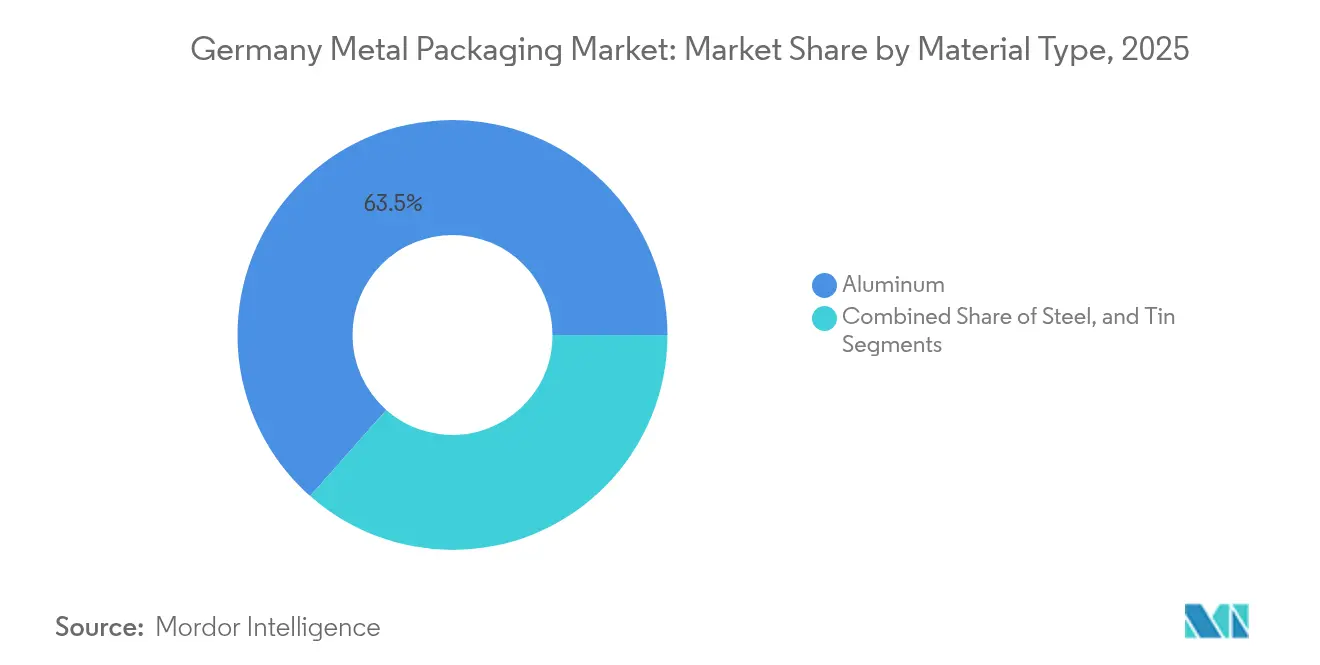

- By material type, Aluminum captured 63.48% of Germany metal packaging market share in 2025; steel is projected to advance at a 3.55% CAGR through 2031.

- By product type, cans held 42.25% of the Germany metal packaging market size in 2025, whereas bulk containers are forecast to grow at a 3.95% CAGR to 2031.

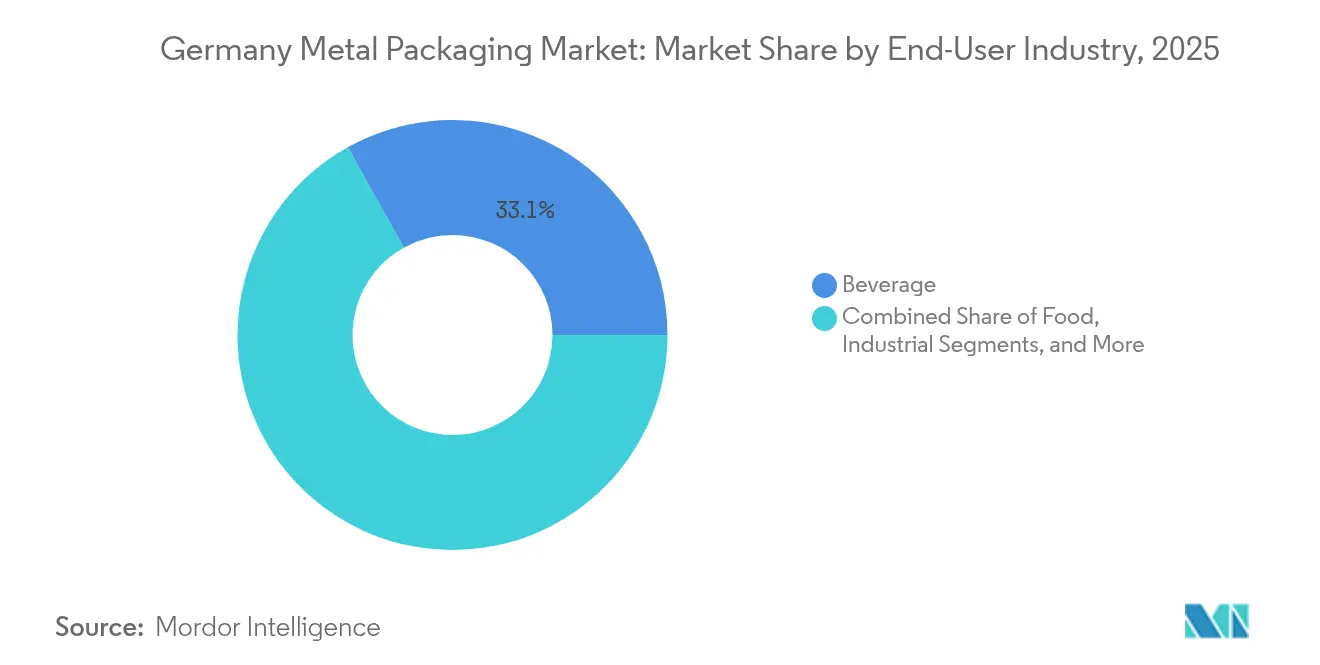

- By end-user industry, beverages led with a 33.10% share of the Germany metal packaging market size in 2025; industrial applications are set to expand at a 3.75% CAGR between 2026 and 2031.

- By coating type, epoxy phenolic dominated with a 39.05% Germany metal packaging market share in 2025, and BPA-free alternatives are rising at a 3.32% CAGR to 2031.

- Ardagh Metal Packaging, Ball Corporation, and Crown Holdings collectively retained over 54.60% share in 2025, reinforcing a moderately consolidated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Metal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability targets of German FMCG brands | +0.8% | Germany, spillover to EU | Medium term (2–4 years) |

| Shift toward lightweight recyclable packaging | +0.6% | Global, early gains in Germany, Netherlands, Austria | Long term (≥ 4 years) |

| Growth of ready-to-drink beverage segment | +0.7% | Germany core, DACH expansion | Short term (≤ 2 years) |

| Expansion of Germany’s craft-beer exports | +0.4% | National, export focus on EU and North America | Medium term (2–4 years) |

| Automation in metal-can production lines | +0.5% | Germany, France, Netherlands | Long term (≥ 4 years) |

| OEM preference for monomaterial packaging | +0.3% | Germany automotive and industrial | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Sustainability Targets of German FMCG Brands

German food and beverage multinationals have pledged to achieve 100% recyclability rates by 2027, prompting a decisive shift toward metal packaging due to its 83% recycling rate and closed-loop potential.[1]Bundesvereinigung der Deutschen Ernährungsindustrie, “Nachhaltigkeitstrends in der Ernährungsindustrie,” bve-online.de Brand owners are replacing composite laminates with Aluminum or steel containers that meet VerpackG eco-modulation fees and simplify end-of-life sorting. Beverage fillers are particularly aggressive, switching premium ready-to-drink SKUs into brightly printed Aluminum cans that underscore infinite recyclability. Retailers reward this shift by granting shelf-space premiums, while deposit-return gains help reclaim scrap for smelters, closing material loops, and offsetting reliance on virgin metal.

Automation in Metal Can Production Lines

Industry 4.0 retrofits across German facilities have demonstrated scrap declines of 25% and energy savings of nearly 10 kWh per ton when digital twins synchronize coil feed, cupping, and necking stations.[2]CORDIS, “Transitioning to smart automation benefits the metal industry and the environment,” cordis.europa.eu Sensors embedded in presses capture high-frequency vibration patterns, feeding AI models that identify die misalignment before it generates waste. Predictive maintenance intervals lengthen machine uptime, and cloud-based SPC dashboards let operators fine-tune sheet-thickness tolerances within ±3 µm. The Manufacturing-X framework promotes secure, standardized data exchange among OEMs, varnish suppliers, and fillers, reducing batch-release delays and enabling lot-level traceability.

Growth of Ready-to-Drink Beverage Segment

German consumers are increasingly preferring single-serve energy drinks, hard seltzers, and cold-brew coffees, which is lifting the appeal of the can format due to its lightweight transport and 360° printable real estate. Surveyed beverage processors plan to allocate 38% of new CAPEX toward Aluminum-can filling lines between 2025 and 2027, citing product integrity and brand storytelling as core motivators. Functional-ingredient drift-like herbal infusions-benefits from metal’s superior O₂ and UV barriers, extending shelf life without refrigeration. As convenience stores and forecourt retailers widen RTD portfolios, order volumes for slim 250 mL and sleek 330 mL cans rise, pressuring suppliers to augment color-separation capabilities for short runs.

Expansion of Germany’s Craft-Beer Exports

Canned craft ales shipped abroad grew 12% YoY in 2024 despite Aluminum-tariff gyrations. Exporters favor 440 mL formats to stand out on boutique beer shelves, leveraging the strength of cans to survive trans-Atlantic distribution. Lightweight ends shave logistics costs, allowing smaller breweries to reach U.S. markets without compromising on sterile filtration. Nonetheless, currency swings and LME spot prices produce budgeting headaches, spurring cooperatives that bulk-purchase can-sheet stock and hedge via futures contracts, stabilizing input expenditures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of base metals | –0.9% | Global, acute on German costs | Short term (≤ 2 years) |

| Rising adoption of high-barrier plastics | –0.6% | Germany and EU, food-safety driven | Medium term (2–4 years) |

| Regulatory scrutiny of BPA-based coatings | –0.4% | EU-wide, German compliance lead | Long term (≥ 4 years) |

| High CAPEX for advanced coating equipment | –0.3% | German manufacturing centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Base Metals

London Metal Exchange Aluminum premiums spiked 27% in early 2025 following geopolitical disruptions, directly increasing the cost per thousand units of can sheet. Large converters hedge by locking 12-month contracts, yet SMEs lack credit headroom, leading to squeezed margins and deferred machine upgrades. Volatility complicates quoted pricing to brand clients, some of whom experiment with hybrid packaging or down-gauging options, reducing overall can demand. Recycled-content substitution offers partial relief but is capped by collection yield and melt-loss limits, keeping price pressure elevated.

Rising Adoption of High-Barrier Plastics

Polyethylene terephthalate bottles with plasma-polymer coatings now achieve O₂ transmission rates rivaling those of three-piece steel cans, prompting dairy and baby-food fillers to pilot plastic alternatives. Weight reduction leads to transportation savings, and integrated in-mold handles enhance consumer convenience. While EU single-use rules impose recycled-content mandates, resin suppliers pledge to include 30% PCR by 2028, narrowing the sustainability edge of metal. Consequently, non-carbonated beverages and sensitive sauces represent battleground categories where metal producers must bolster value propositions beyond recyclability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Dominance Amid Steel’s Emerging Growth

Aluminum commanded 63.48% of Germany metal packaging market share in 2025, buoyed by its lightweight profile, corrosion resistance, and closed-loop recyclability advantages. This supremacy translates into favorable freight economics and reduced scope-3 emissions, positioning Aluminum exporters competitively under Germany’s Carbon Border Adjustment Mechanism. Steel, however, is pacing at a 3.55% CAGR, signaling demand from industrial bulk-container users who weigh cost per volume over grams per unit. Major mills have introduced chrome-free tinplate that meets upcoming REACH mandates, lowering compliance overhead for fillers.

Steel’s ascent benefits Germany’s dense network of electric-arc furnaces supplied by scrap streams exhibiting >85% recovery rates. Producers tout life-cycle cost parity with Aluminum when can-body thickness drops below 0.18 mm, especially for hot-fill food applications. Furthermore, steel’s magnetic properties simplify automated sorting in municipal plants, reinforcing collection economics. Although Aluminum retains halo effects in premium beverage marketing, steel’s robust mechanical strength secures its foothold in aerosols and chemical drums, diversifying revenue resilience for the Germany metal packaging market.

By Product Type: Cans Lead Market While Bulk Containers Drive Growth

Cans retained 42.25% of Germany metal packaging market size in 2025, propelled by beverage, food, and personal-care SKUs that value hermetic sealing and billboard branding real estate. Sleek-can variants for energy drinks multiply SKUs, demanding fast-changeover decorators capable of <5 min downtime to push order profitability. Bulk containers, notably 500 L and 1,000 L IBC liners, are forecast to log a 3.95% CAGR, reflecting chemical and pharma sector reliance on contamination-free transport of high-value liquids. Ringmetall SE’s liner acquisitions aim to exploit this pocket of momentum, mirroring the Germany metal packaging market’s tilt toward specialized, higher-margin niches.

Growing e-commerce palletization calls for stackable metal drum designs with anti-slip bead geometry, reducing transit damage and insurance claims. Meanwhile, aerosol can volumes stabilize amidst regulatory scrutiny of propellants, but brand owners counter with compressed formats that achieve equal spray duration using 20% less metal, alleviating material cost exposure. Decorative tins for seasonal confectionery leverage lithographic advances to deliver photo-realistic prints, extending gifting appeal and showcasing German design craftsmanship.

By End-User Industry: Beverage Sector Leadership with Industrial Applications Accelerating

Beverages accounted for 33.10% of Germany metal packaging market share in 2025, as deposit-return schemes (+25 ct per unit) deliver closed-loop feedstock and reassure brand ESG metrics. Carbonated soft drinks migrate to slim cans that reduce aluminum mass by 20%, while nitrogen-dosed cold brews utilize can rigidity to create cascading foam visuals. Industrial buyers are set to climb at a 3.75% CAGR through 2031, guided by Germany’s export-oriented machinery and specialty-chemicals output. ISO-container compatible drums with UN-rated latching rings provide hazardous-goods compliance, and traceability QR codes printed under varnish feed into Manufacturing-X ledgers.

Food processors maintain steady demand for tin-plate packaging for ready meals targeting on-the-go consumers, yet face pressure to cut salt and acid preservatives, nudging interest toward retortable Aluminum trays. Pharmaceuticals and OTC supplements pivot to child-resistant closures with integrated desiccants, elevating value-added closure formats within the Germany metal packaging market.

By Coating Type: Epoxy Phenolic Leads While BPA-Free Alternatives Gain Momentum

Epoxy phenolic coatings held 39.05% of Germany metal packaging market share in 2025, appreciated for broad chemical compatibility and cost-effective line speeds. However, BPA-free coatings, logging a 3.32% CAGR, are rapidly shifting from niche to mainstream as multinational fillers set 2026 cut-off dates. Acrylic hybrids blended with silicone elastomers now withstand 8 bar internal pressures, enabling use in high-gravity lagers without flavor scalping. Polyester varnishes demonstrate sub-2 ppm migration in retort tests, satisfying impending German BfR thresholds.

Transition dynamics involve dual-running lines: legacy epoxy for export markets lacking BPA limits and new chemistry reserved for EU-bound goods. Equipment suppliers bundle turnkey retrofits, including IR curing modules and inline styrene sniffers, compressing qualification timelines. This dual-track strategy safeguards revenue continuity during regulatory evolution and underpins a resilient, technology-forward Germany metal packaging market.

Geography Analysis

Germany anchors the broader DACH packaging ecosystem, accounting for over half of Central European can-sheet consumption in 2025. North Rhine-Westphalia hosts vertically integrated clusters where smelting, rolling, printing, and filling converge within a 100 km radius, minimizing scope-3 logistics emissions and supporting same-day coil deliveries. Bavaria’s mechanical-engineering base fosters R&D collaborations between can-line OEMs and technical universities, accelerating inline camera-inspection algorithms that ripple across the Germany metal packaging market.

The country’s deposit-return infrastructure recovers 97% of beverage cans, supplying domestic remelters with high-grade scrap and lowering imports of primary Aluminum billets. This closed-loop synergy shields local converters from raw-material turbulence and keeps the Germany metal packaging industry cost-competitive. Conversely, eastern regions such as Saxony contend with legacy plant modernization needs and higher electricity tariffs, nudging capacity toward western hubs. Cross-border flows into Austria and Switzerland remain fluid, although Swiss incineration practices limit scrap repatriation, challenging full circularity ambitions.

Germany’s regulatory vanguard-manifest in VerpackG modulations-exerts soft power across neighboring markets. Producers exporting into Germany must redesign packaging toward recyclability thresholds, effectively harmonizing design-for-recycling principles throughout the EU single market. While this creates compliance complexity, it standardizes orders for pan-European brand portfolios, benefitting suppliers able to certify can lines to German scrutiny. Future PPWR alignment will likely tighten post-fill traceability directives, reinforcing data-sharing frameworks seeded by the Manufacturing-X consortium.

Competitive Landscape

The Germany metal packaging market hosts a moderately consolidated cohort led by Ardagh Metal Packaging, Ball Corporation, and Crown Holdings, whose collective share surpasses 55%. These leaders utilize multi-plant networks and shared R&D centers located around Bonn and Braunschweig to launch can-body profiles with an average body wall thickness of 0.200 mm, while retaining drop-test integrity. Capital intensity remains a hurdle for mid-tier players; thus, Ringmetall SE’s serial acquisitions of Peak Packaging Poland, Hutek Oy, and Evopack stakes represent targeted plays to corner industrial liner niches and eco bag-in-box innovation, aligning with sustainability megatrends.[4]Ayondo, “Ringmetall expands into Scandinavian market for bag-in-box systems via acquisition,” ayondo.com

Strategic alliances typify the current era. KHS Group and Ferrum Group acquired H.F. Meyer Maschinenbau to leverage its expertise in depalletizing, rinsing, and seaming, enabling the development of turnkey high-speed beverage lines. Co-development contracts with ink-chemistry specialists aim to reduce VOC emissions and meet Germany’s stringent TA-Luft provisions, adding another layer of differentiation. Meanwhile, Ball Corporation channels EU grants into lightweighting R&D, isolating novel alloy recipes that reduce per-can mass while maintaining buckle resistance, a key lever for carbon footprint cuts integrated within brand LCA dashboards.

Digitalization emerges as the competitive fault line. Plants deploying AI-assisted vision systems can double first-pass yield compared with legacy eight-camera arrays, enhancing line efficiencies above 92%. Data sovereignty remains paramount; therefore, German operators adopt edge-computing modules that retain proprietary process signatures within factory walls, assuaging IP theft anxieties. As extended-producer-responsibility fees escalate, converters offering verified recycled-content certificates and blockchain-anchored traceability strengthen customer lock-in and justify premium contract renewals.

Germany Metal Packaging Industry Leaders

Ardagh Metal Packaging S.A.

Ball Corporation

Crown Holdings Inc.

Silgan Holdings Inc.

HUBER Packaging Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ringmetall SE acquired a 25.1% stake in Evopack, the creator of the “Boxli 1000” bag-in-box system, which features 90% recyclable content and claims a 70% reduction in CO₂ emissions compared to rigid drums.

- January 2025: Ringmetall SE acquired Hutek Oy to enter Scandinavian bag-in-box markets serving dairy and beverage dispensing clientele.

- March 2025: The Federal Ministry for Economic Affairs and Climate Action expanded the Manufacturing-X initiative to encompass metal packaging, advancing standardized data interfaces across the supply chain.

- February 2025: Ball Corporation announced investments to upscale lightweight-can alloy R&D and recycled-content melting at European facilities supplying German beverage fillers.

Germany Metal Packaging Market Report Scope

The market size is computed in real terms and reflects the value(In USD Million)of consumption of metal packaging products among the examined end-users in Germany. The market is segmented by Material Type (Aluminum, Steel), Product Type (Cans, Bulk Containers, Shipping Barrels and Drums, Caps and Closures, Others), and End-user Type (Beverage, Food, Paints, Chemicals, Industrial, Other). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Material Type

| Aluminium |

| Steel |

| Tin |

By Product Type

| Cans | Food Cans |

| Beverage Cans | |

| Aerosol Cans | |

| Decorative Cans | |

| Bulk Containers | |

| Drums and Barrels | |

| Caps and Closures | |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Paints, Coatings and Chemicals |

| Pharmaceuticals and Healthcare |

| Industrial |

| Other End-user Industries |

By Coating Type

| Epoxy Phenolic |

| Acrylic |

| Polyester |

| BPA-Free Alternatives |

| Other Coating Types |

| By Material Type | Aluminium | |

| Steel | ||

| Tin | ||

| By Product Type | Cans | Food Cans |

| Beverage Cans | ||

| Aerosol Cans | ||

| Decorative Cans | ||

| Bulk Containers | ||

| Drums and Barrels | ||

| Caps and Closures | ||

| Other Product Types | ||

| By End-User Industry | Food | |

| Beverage | ||

| Paints, Coatings and Chemicals | ||

| Pharmaceuticals and Healthcare | ||

| Industrial | ||

| Other End-user Industries | ||

| By Coating Type | Epoxy Phenolic | |

| Acrylic | ||

| Polyester | ||

| BPA-Free Alternatives | ||

| Other Coating Types | ||

Key Questions Answered in the Report

What is the forecast size of the Germany metal packaging market in 2031?

The market is projected to reach USD 5.77 billion by 2031, growing at a 2.76% CAGR.

Which material leads in German metal packaging?

Aluminium holds 63.48% share, driven by its recyclability and lightweight profile.

Which segment is growing fastest by product type?

Bulk containers, especially IBC inner liners, are advancing at a 3.95% CAGR.

How are German regulations influencing packaging choices?

VerpackG eco-modulation fees and PPWR alignment incentivize highly recyclable metal formats.

Why are BPA-free coatings gaining traction?

Stricter EFSA limits drive brand owners to transition toward acrylic and polyester alternatives.

Who are the leading companies in the market?

Ardagh Metal Packaging, Ball Corporation, and Crown Holdings collectively lead, leveraging automation and sustainability investments.

Page last updated on: