Energy & Power

30th JulyUnlocking Market Potential for Solid-State Transformers

3 Min Read

The United States Hybrid Electric Vehicle Battery Market Report is Segmented by Battery Chemistry (Lithium-Ion, Nickel-Metal Hydride, Lead-Acid, and Emerging Solid-State/Sodium-ion), Degree of Hybridization (Mild Hybrid, Full Hybrid, Plug-In Hybrid, and Range-Extender Hybrid), Voltage Class (Up To 60V, 60 To 200V, 200 To 400V, and Above 400V), and Vehicle Class (Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and More).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

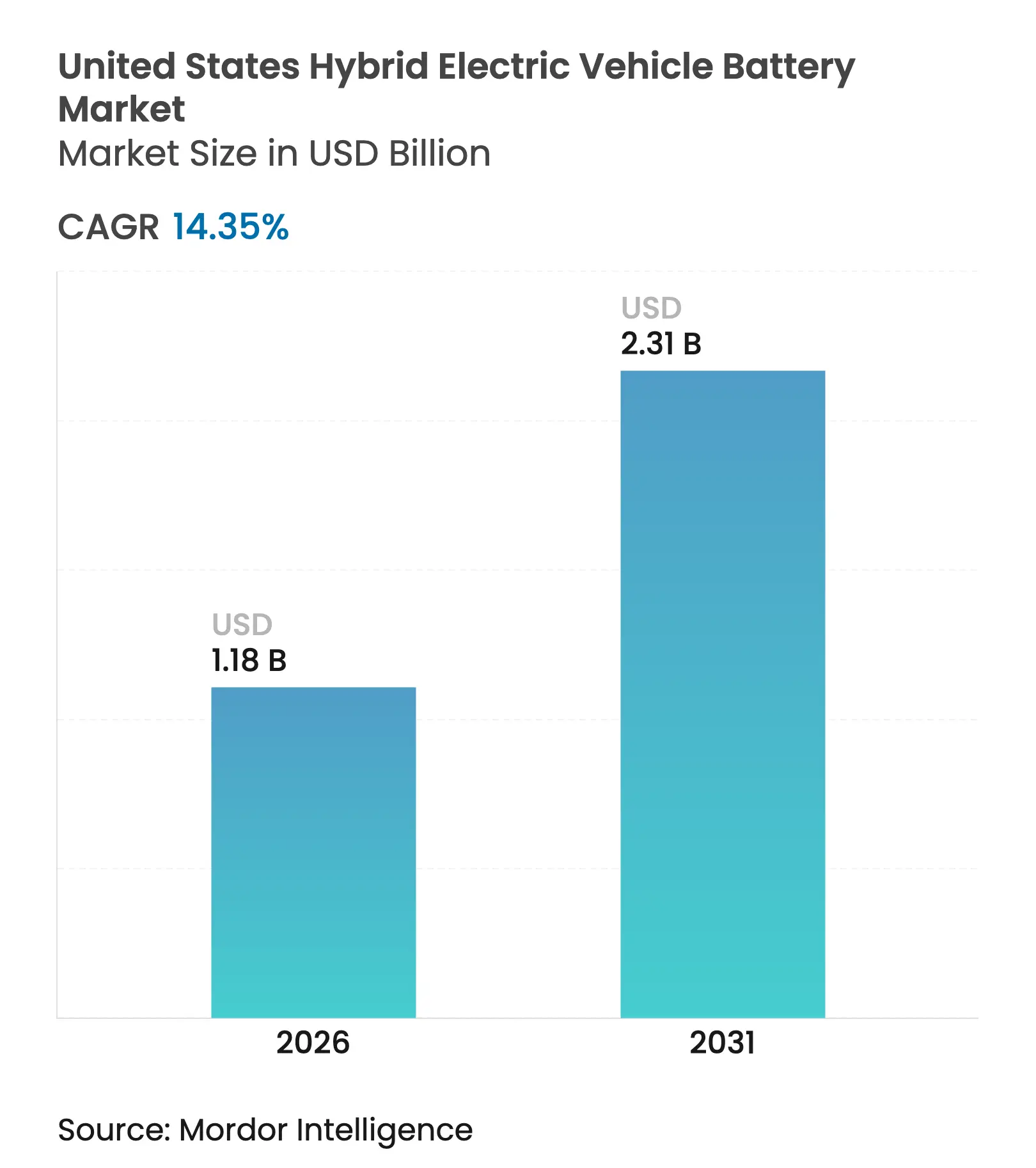

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 14.35 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Automakers are leaning on hybrid programs to hedge against slower-than-expected battery-electric uptake, while the Inflation Reduction Act’s production credit compresses supply chains, lifts domestic output margins, and improves pricing visibility.[1]U.S. Department of Energy, “Inflation Reduction Act of 2022—Advanced Manufacturing Production Credit,” energy.gov Concurrently, lithium-ion pack costs are approaching the USD 100 per-kilowatt-hour threshold, raising the economic case for hybrids even in the absence of subsidies.[2]BloombergNEF, “Battery Pack Prices Fall to USD 115/kWh, Approaching Cost Parity,” bloomberg.com Second-life applications and vehicle-to-grid revenue streams are beginning to elevate residual values, lowering the total cost of ownership for fleets and retail buyers alike. Regulatory tailwinds, including California’s Advanced Clean Cars II targets and nationwide FMVSS 305a safety protocols, further underpin the demand outlook.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

IRA-driven domestic battery manufacturing incentives IRA-driven domestic battery manufacturing incentives | 4.2% | United States, with concentration in Southeast manufacturing corridor (Tennessee, Georgia, Kentucky) | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:4.2% | Geographic Relevance :United States, with concentration in Southeast manufacturing corridor (Tennessee, Georgia, Kentucky) | Impact Timeline :Medium term (2-4 years) |

Surging hybrid sales amid EV-only slowdown Surging hybrid sales amid EV-only slowdown | 3.8% | United States, particularly California, Colorado, and Northeast states with ZEV mandates | Short term (≤ 2 years) | |||

Rapid sub-USD 100/kWh Li-ion pack cost decline Rapid sub-USD 100/kWh Li-ion pack cost decline | 3.1% | United States, benefiting OEMs with domestic assembly and localized supply chains | Medium term (2-4 years) | |||

Second-life & V2G revenue pools raise residual value Second-life & V2G revenue pools raise residual value | 1.9% | United States, early adoption in California, Texas, and PJM Interconnection grid territories | Long term (≥ 4 years) | |||

FMVSS 305a safety rule pushing advanced chemistries FMVSS 305a safety rule pushing advanced chemistries | 1.5% | United States (federal mandate) | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

IRA-Driven Domestic Battery Manufacturing Incentives

Section 45X offers USD 35 per kilowatt-hour for battery cells and USD 10 per kilowatt-hour for modules produced domestically, improving gross margins by double digits for vertically integrated players. The credit is accelerating gigafactory build-outs across Tennessee, Georgia, and Kentucky, where LG Energy Solution and General Motors plan 50 gigawatt-hours of annual capacity by 2026. Content-origin thresholds that rise to 50% by 2029 are pushing Asian suppliers to localize cathode and anode lines, creating openings for mid-tier firms such as Microvast, supported by a USD 200 million Department of Energy loan. A 2033 phase-out places a premium on early investment, prompting long-term offtake agreements between cell makers and automakers. These factors jointly lift the near-term growth profile of the United States hybrid electric vehicle battery market.[3]U.S. Department of Energy, “Inflation Reduction Act of 2022—Advanced Manufacturing Production Credit,” energy.gov

Surging Hybrid Sales Amid EV-Only Slowdown

Hybrid registrations grew 38% year over year in 2024 to about 1.4 million units, while battery-electric growth cooled to 7%. Limited public fast-charger density outside urban centers keeps range anxiety elevated, guiding cost-sensitive buyers toward hybrids. Ford redirected 40% of its electrification budget to hybrid and plug-in programs through 2027, reversing a prior BEV-first stance. California regulations allow long-range plug-in hybrids to satisfy Zero-Emission Vehicle targets, anchoring demand for higher-capacity packs. The shift supports a broader revenue base for pack suppliers in the United States hybrid electric vehicle battery market.

Rapid Sub-USD 100/kWh Li-Ion Pack Cost Decline

Pack prices slipped to USD 115 per kilowatt-hour in 2024 and continue to edge toward USD 100 as material deflation and plant scale economies accrue. Lithium iron phosphate designs, such as BYD’s Blade, reached USD 95 per kilowatt-hour at the cell level for high-volume orders. Dry-electrode coating cuts energy use nearly 30% in production, trimming capital outlays by one-fifth. These developments allow OEMs to price hybrid variants within USD 3,000 of combustion equivalents, reinforcing the United States hybrid electric vehicle battery market trajectory.

Second-Life & V2G Revenue Pools Raise Residual Value

Vehicle-to-grid pilots in California and Texas show annual grid-services revenue of USD 300-500 per vehicle, offsetting ownership costs. Duke Energy’s North Carolina project aggregated retired hybrid packs into a 2 MWh array at USD 180 per kilowatt-hour, half the cost of new builds. Updated SAE J2929 protocols streamline state-of-health certification, enhancing secondary-market liquidity. These monetization pathways strengthen lifecycle economics for buyers, fostering greater uptake within the United States hybrid electric vehicle battery market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Critical-mineral supply tightness Critical-mineral supply tightness | -2.8% | United States, dependent on imports from Australia, Chile, Argentina, and China | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-2.8% | Geographic Relevance :United States, dependent on imports from Australia, Chile, Argentina, and China | Impact Timeline :Medium term (2-4 years) |

Political uncertainty over federal tax credits Political uncertainty over federal tax credits | -1.7% | United States (federal policy) | Short term (≤ 2 years) | |||

Limited US battery-recycling capacity Limited US battery-recycling capacity | -1.2% | United States, with nascent infrastructure in Nevada, Ohio, and Georgia | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Critical-Mineral Supply Tightness

Lithium hydroxide averaged USD 45,000 per metric ton in late 2024, triple 2020 levels, and domestic output covers less than 2% of demand.[4]U.S. Geological Survey, “Mineral Commodity Summaries 2024—Lithium,” usgs.gov High-nickel cathodes face additional pressure from Indonesian export restrictions, while cobalt sourcing remains concentrated in the Democratic Republic of Congo. Permitting delays at Thacker Pass and Rhyolite Ridge push first production into the late 2020s. Automakers are pivoting toward lithium iron phosphate to mitigate exposure, but lower energy density can raise pack mass and erode efficiency. These dynamics temper the growth outlook for the United States' hybrid electric vehicle battery market.

Political Uncertainty Over Federal Tax Credits

Congressional proposals in 2024 sought to trim the USD 7,500 plug-in hybrid credit or apply price caps, clouding product-planning visibility. Fewer than 40% of eligible models met escalating domestic-content thresholds in 2024, down sharply from 2023. Any curtailment would immediately flow through lease pricing, cooling demand in a price-sensitive segment. Automakers must either absorb the gap or delay launches, injecting cyclical volatility into the United States hybrid electric vehicle battery market.

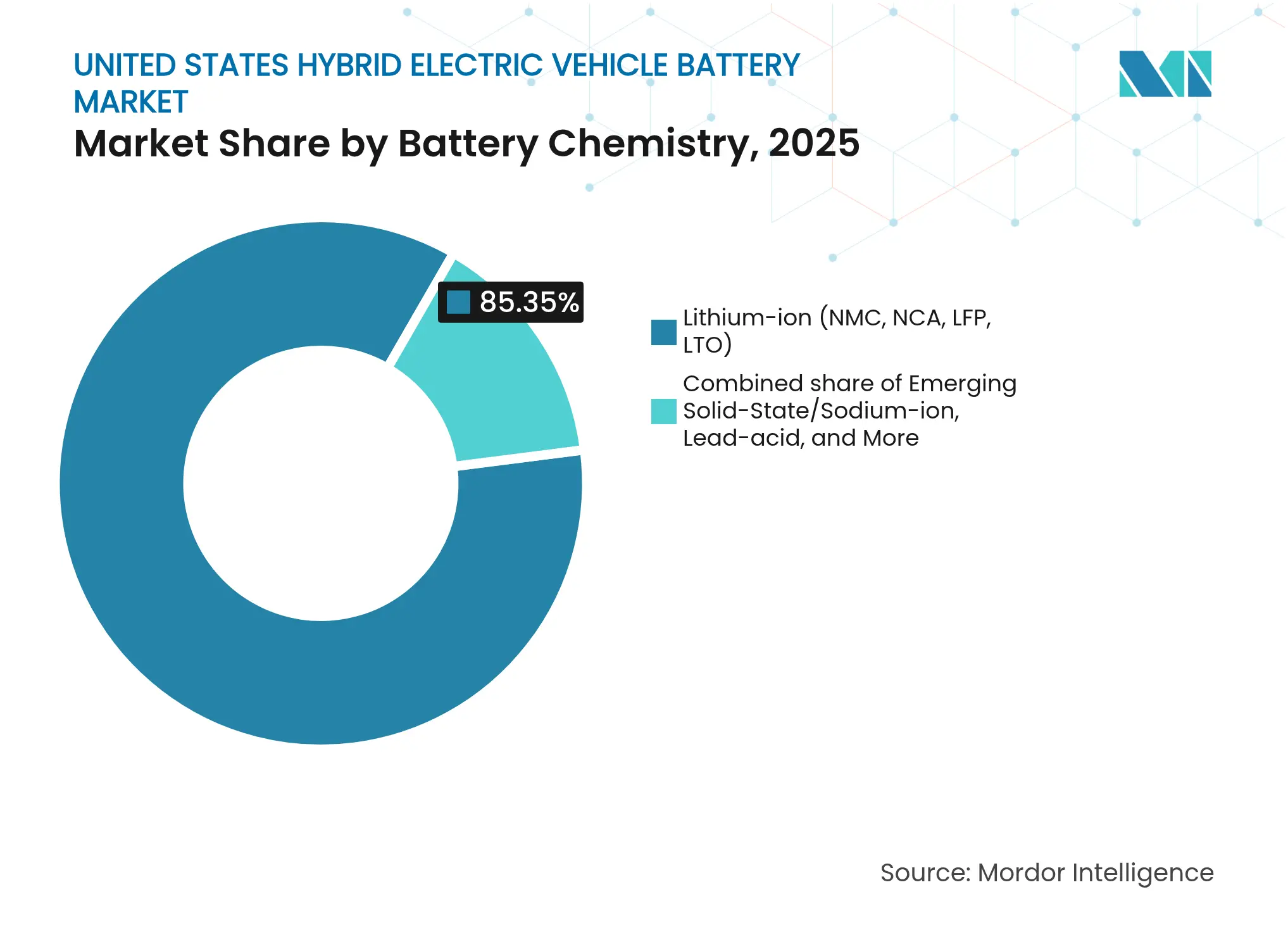

By Battery Chemistry: Lithium-Ion Maintains Lead Amid Chemistry Diversification

The United States hybrid electric vehicle battery market size for lithium-ion solutions equaled 85.35% of the 2025 value, reflecting superior energy density and a maturing cost curve. Nickel-manganese-cobalt variants dominate plug-in architectures that need 220-260 Wh/kg, while lithium iron phosphate appeals to mild hybrids prioritizing safety and cobalt-free sourcing. Nickel-metal hydride’s role contracts as OEMs transition to higher-capacity lithium-ion designs, yet it survives in selected Toyota platforms because of proven durability. Lead-acid continues in 12-volt auxiliaries, but limited depth-of-discharge restricts its traction potential.

Emerging chemistries increase the addressable base of the United States hybrid electric vehicle battery market. Solid-state prototypes from Solid Power reached 390 Wh/kg in 2024 laboratory trials and target pilot output by 2026. Sodium-ion’s cost advantage and broader temperature band make it a candidate for 48-volt packs in harsh climates. EPA-proposed labeling rules on mineral content encourage chemistry diversification, de-risking upstream supply chains.

Note: Segment shares of all individual segments available upon report purchase

By Degree of Hybridization: Cost-Focused Mild Systems Drive Volume

Mild hybrids operating at 48 volts captured 46.05% of 2025 revenue in the United States hybrid electric vehicle battery market and are forecast to grow 16.25% CAGR through 2031. A belt starter-generator paired with a 0.5-1.5 kWh pack enables regenerative braking, engine stop-start, and torque assist, delivering 10-15% fuel savings at sub-USD 1,500 incremental cost. ISO 6469-3 compliance eases integration because high-voltage interlocks are unnecessary.

Full hybrids remain pivotal for meeting fleet fuel-economy targets, while plug-in hybrids occupy a premium niche where federal and state incentives lessen sticker shock. Range-extender formats are fading as OEMs streamline portfolios toward either larger packs or lower-cost mild solutions. Together, these mixes underpin resilient growth for the United States hybrid electric vehicle battery market.

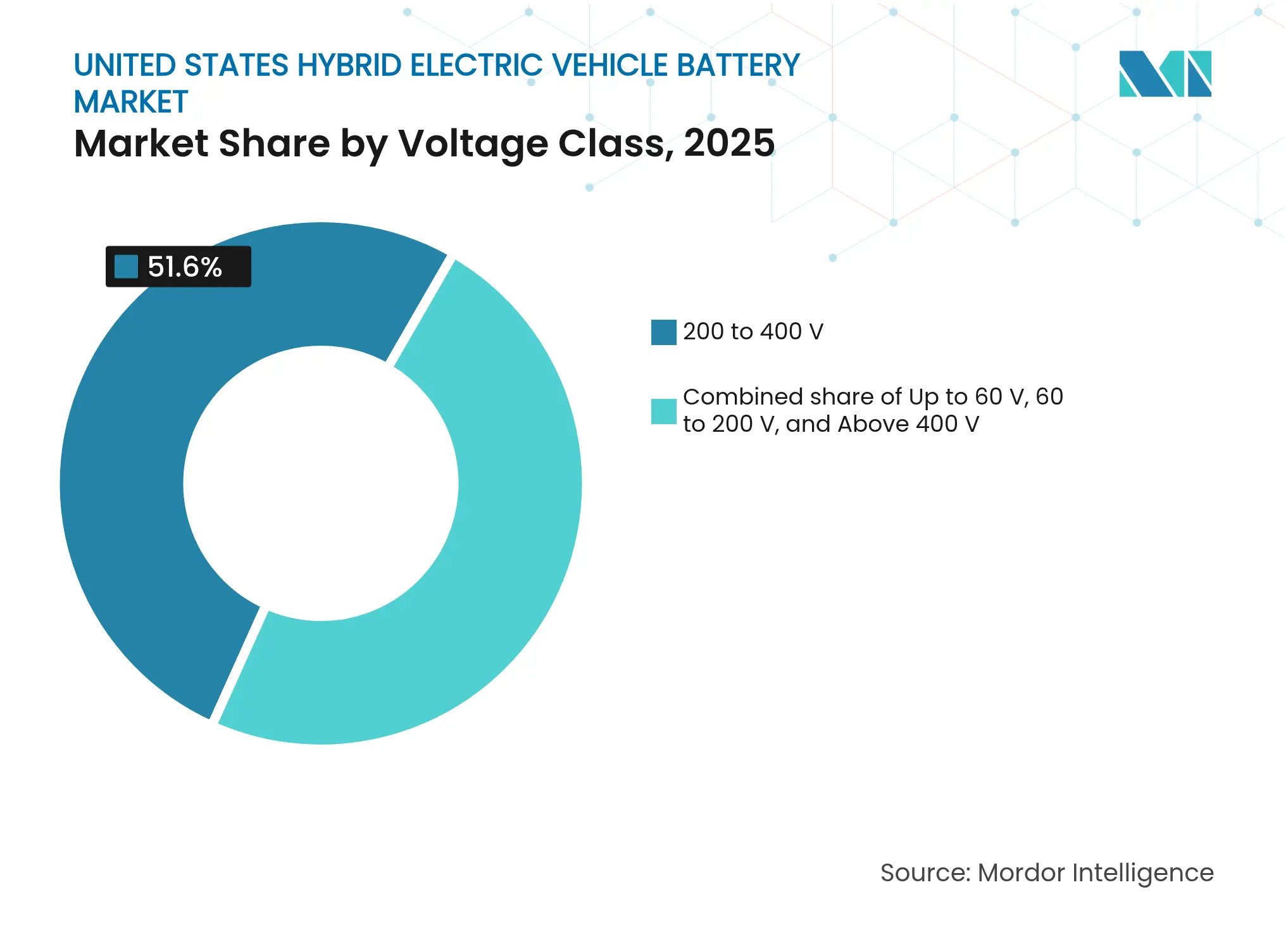

By Voltage Class: Legacy Mid-Voltage Designs Hold Sway, 800 V Gains Momentum

Battery systems between 200 and 400 volts held a 51.60% share in 2025, reflecting entrenched Toyota and Honda architectures that minimize copper mass and thermal-management complexity. Sub-60-volt packs, crucial for mild hybrids, represent a sizeable secondary block that attracts cost-sensitive buyers.

Architectures above 400 volts expand rapidly, posting a 18.55% forecast CAGR as premium plug-in hybrids adopt 800-volt platforms for 150 kW DC fast charging. Silicon-carbide inverters lift efficiency by two percentage points, offsetting higher semiconductor costs and further diversifying the United States hybrid electric vehicle battery market.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Class: Passenger Cars Anchor Demand, Commercial Fleets Accelerate

Passenger cars retained 56.85% of 2025 consumption and are projected to grow 17.15% CAGR to 2031 in the United States hybrid electric vehicle battery market. Consumer attraction centers on crossovers such as the RAV4 Prime that pair 40-mile electric range with conventional refueling convenience. Shared architectures, including Ford’s CD6, distribute R&D costs across multiple nameplates.

Commercial vehicles, from last-mile vans to medium-duty trucks, form the next growth wedge as fleet operators seek fuel savings without depot charging upgrades. Off-highway machinery and small two- or three-wheel vehicles remain a nascent slice but signal future diversification. Collectively, these segments enhance the resilience of the United States hybrid electric vehicle battery market.

A southeastern corridor spanning Tennessee, Georgia, Kentucky, and South Carolina is emerging as the manufacturing heartland for the United States' hybrid electric vehicle battery market. Planned capacity exceeds 100 GWh by 2028, driven by LG Energy Solution, SK On, and Envision AESC, each leveraging state incentives and proximity to assembly plants. California, although light on cell production, anchors demand through Advanced Clean Cars II mandates and robust vehicle-to-grid pilots that demonstrate monetizable grid services.

The Midwest concentrates pack-integration and battery-management expertise around Detroit, where A123 Systems and Romeo Power maintain technical centers that support OEM validation cycles. Texas attracts recycling and second-life startups because low-cost renewable power lowers hydrometallurgical operating costs. Charging infrastructure disparities shape regional mix: rural areas favor full or mild hybrids, while cities with dense Level 2 networks prefer plug-in models. The federal NEVI program targets corridor coverage by 2027 and could swing demand toward bigger packs.

Regulatory frameworks remain fragmented; for instance, the absence of a nationwide vehicle-to-grid interconnection standard complicates multi-state fleet deployments. Yet the aggregate outcome is a geographically balanced growth profile for the United States hybrid electric vehicle battery market.

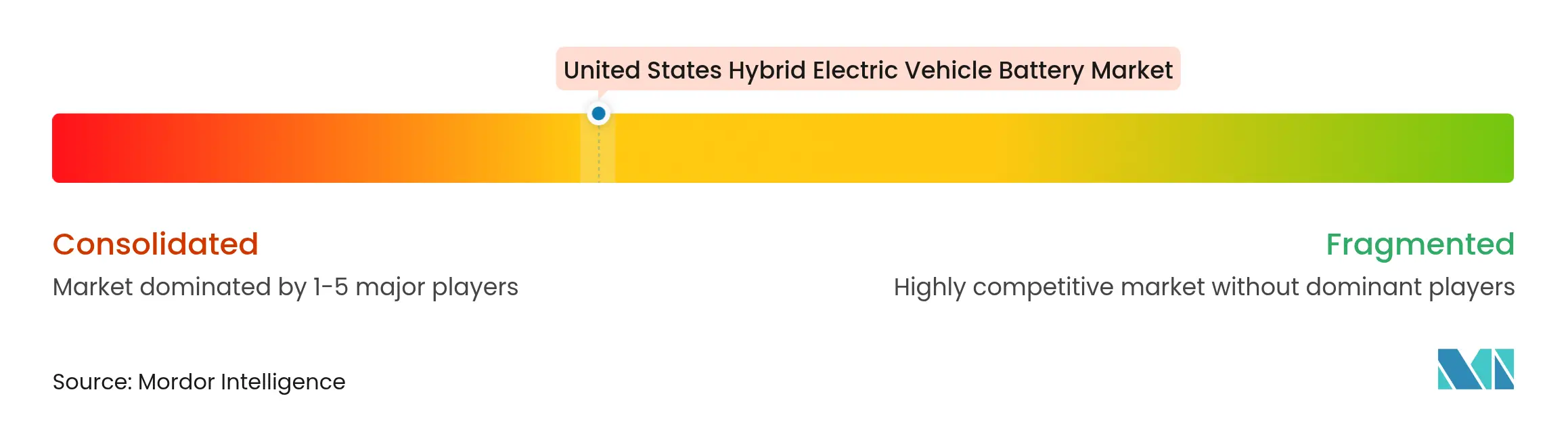

Market Concentration

The United States hybrid electric vehicle battery market is moderately concentrated. The five largest suppliers, Panasonic Energy, LG Energy Solution, Samsung SDI, CATL, and Prime Planet Energy & Solutions, held 60-65% combined share in 2024. Asian incumbents leverage fully integrated supply chains and long-standing OEM ties. Joint ventures such as Ultium Cells lock in capacity and technology roadmaps, while BYD and Gotion aim to undercut pricing in lithium iron phosphate packs destined for commercial fleets.

Technology competition intensifies around solid-state breakthroughs. Solid Power and QuantumScape attract OEM investment stakes, whereas incumbents file patents on silicon-anode designs in record volume, up 40% in 2024. Entry barriers rise as FMVSS 305a and SAE J2464 abuse-testing compliance can exceed USD 2 million per cell design. This fosters an environment where scale, certification capacity, and intellectual-property breadth dictate competitive advantage inside the United States hybrid electric vehicle battery market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

A Hybrid Electric Vehicle (HEV) battery is a rechargeable energy storage system that powers the electric motor of a hybrid vehicle. HEVs combine a conventional internal combustion engine (ICE) with an electric propulsion system. The battery in an HEV is crucial for capturing and storing energy, particularly during regenerative braking, and for providing additional power during acceleration.

The United States' hybrid electric vehicle battery market is segmented by battery chemistry, degree of hybridization, voltage class, and vehicle class. By battery chemistry, the market is segmented into Lithium-Ion Battery, Lead-Acid Battery, Sodium-Ion Battery, and Others. The market is segmented by degree of hybridization into Mild Hybrid (48 V MHEV), Full Hybrid (HEV), Plug-in Hybrid (PHEV), and Range-Extender Hybrid. By voltage class, the market is divided into Up to 60 V, 60 to 200 V, 200 to 400 V, and Above 400 V. By vehicle class, the market is segmented into Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and Off-Highway and Specialty. The report offers market size forecasts in revenue (USD) for all the above segments.

Unlocking Market Potential for Solid-State Transformers

3 Min Read

Feasibility Analysis for FBO Services in East Africa

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.