Germany Domestic Courier, Express And Parcel (CEP) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

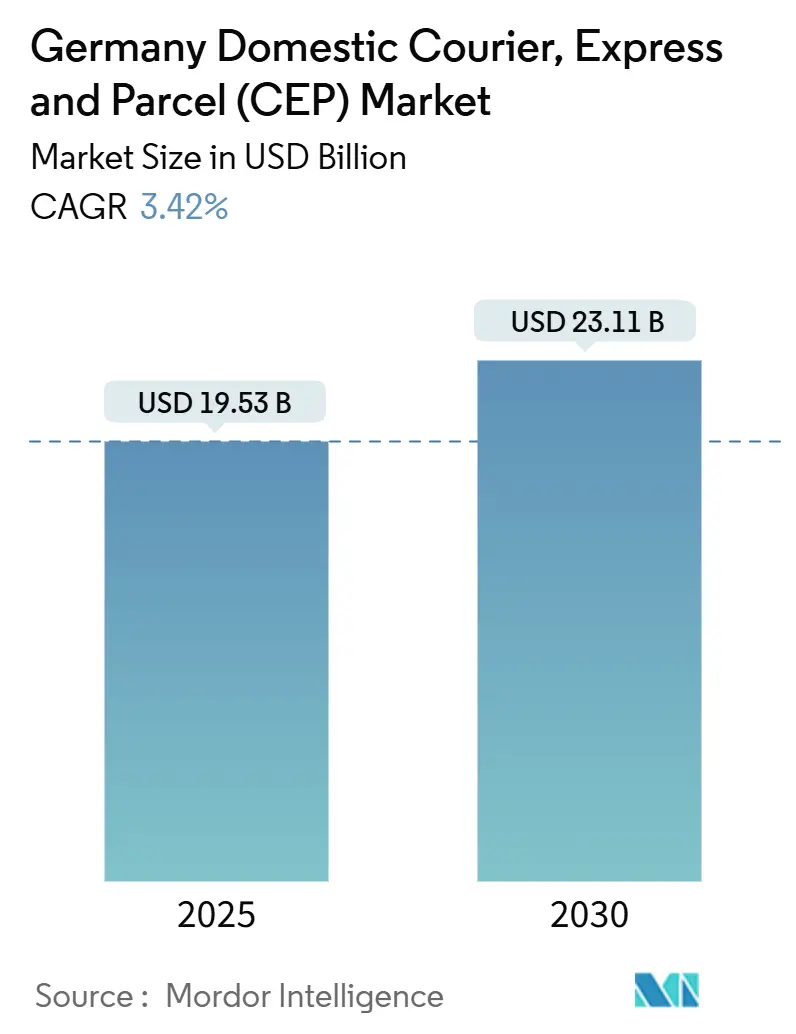

| Market Size (2025) | USD 19.53 Billion |

| Market Size (2030) | USD 23.11 Billion |

| Growth Rate (2025 - 2030) | 3.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Domestic Courier, Express And Parcel (CEP) Market Analysis by Mordor Intelligence

The Germany Domestic Courier, Express And Parcel Market size is estimated at USD 19.53 billion in 2025, and is expected to reach USD 23.11 billion by 2030, at a CAGR of 3.42% during the forecast period (2025-2030).

The Germany domestic courier, express and parcel market is maturing after its pandemic-era surge, so volume growth now hinges on premium time-definite services, denser pickup-drop-off ecosystems and technology-led cost controls. E-commerce still anchors demand, yet its slowing shipment expansion pushes carriers toward higher-margin same-day and scheduled tiers. Investment in parcel lockers, autonomous route planning and electric vans shields margins against rising driver wages and low-emission mandates. The Germany domestic courier, express and parcel market also benefits from near-shoring by manufacturers, which converts small-batch components into medium-weight parcels, and from growing healthcare cold-chain flows that command premiums well above standard B2C rates

Key Report Takeaways

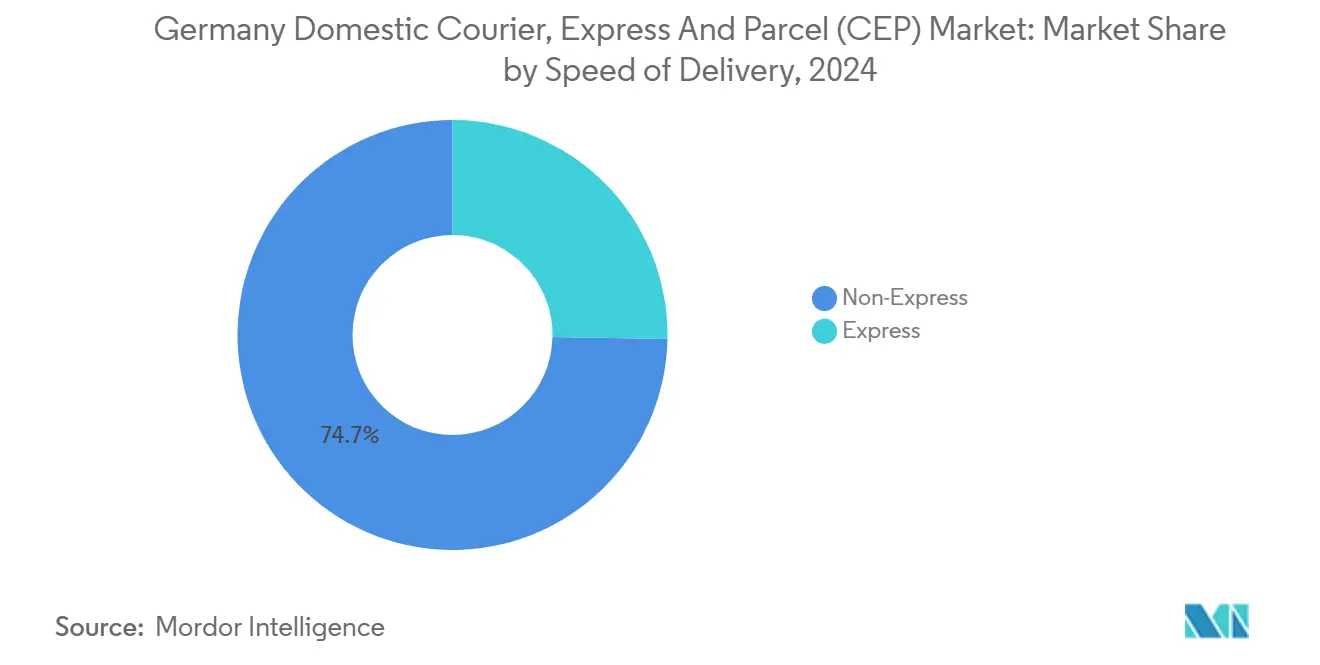

By speed of delivery, non-express services captured 74.70% of the Germany domestic courier, express and parcel market share in 2024, while express is set to advance at a 4.10% CAGR through 2030.

By shipment weight, light parcels held 48.33% of the Germany domestic courier, express and parcel market size in 2024 and medium-weight parcels are forecast to expand at a 3.94% CAGR to 2030.

By end-user industry, e-commerce led with 39.06% revenue share in 2024; healthcare is the fastest growing segment at a 5.0%–plus CAGR through 2030.

By business model, the B2C segment held 46.80% of the Germany domestic courier, express and parcel market in 2024, whereas C2C is projected to grow at 5.12% per year to 2030.

By mode of transport, road carried 38.20% of 2024 volumes, yet air freight is advancing at a 3.80% CAGR as express demand rises.

Germany Domestic Courier, Express And Parcel (CEP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid e-commerce expansion | +0.9% | National, high density in Berlin, Hamburg, Munich | Medium term (2-4 years) |

| High internet & smartphone penetration | +0.5% | National | Long term (≥ 4 years) |

| Same-day delivery premiumization | +0.7% | National, early adoption in Frankfurt, Cologne, Stuttgart | Short term (≤ 2 years) |

| Urban micro-fulfillment networks | +0.6% | National, clusters in Rhine-Ruhr, Berlin, Munich | Medium term (2-4 years) |

| Near-shoring of German manufacturing | +0.4% | Baden-Württemberg, Bavaria, North Rhine-Westphalia | Long term (≥ 4 years) |

| Closed-loop packaging mandates | +0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid E-Commerce Expansion

German online retail is growing due to sustaining parcel flow even as growth moderates from pandemic highs. Quick-commerce players such as Flink and Gorillas run 10-minute delivery windows that generate multiple daily parcel cycles per micro-hub. Amazon’s EUR 10 billion logistics program extends same-day coverage to 90% of residents, resetting service benchmarks. Otto Group’s 70+ automated city warehouses shorten fulfillment radii to under 5 kilometers, lifting delivery density. As a result, the Germany domestic courier, express and parcel market pivots from pure volume to blended revenue per stop, favoring carriers that integrate premium tiers seamlessly.

High Internet and Smartphone Penetration

Internet availability above 95% and smartphone adoption around 85% create a consumer base that demands real-time visibility. DHL’s MyWays lets receivers reroute parcels mid-journey, trimming failed deliveries by double digits. DPD’s Predict one-hour windows lift first-attempt success past 92%. C2C platforms integrate label APIs so sellers print at home, propelling shipment self-service growth. Data from route and address preferences feeds machine-learning models that reduce empty miles, enhancing the Germany domestic courier, express and parcel market operating margin.

Same-Day Delivery Premiumization

Carriers price same-day parcels EUR 5–15 above standard, winning 15–20% extra revenue per piece. DHL now serves 50 cities with sub-12-hour guarantees for automotive and diagnostic shipments. Amazon’s LastMileTram in Frankfurt uses tram cargo cabins to bypass traffic and hit four-hour windows. Profitability, however, relies on dense urban stops of at least 15 per hour, which limits reach to metro zones. Dynamic surge pricing aligns capacity with demand spikes, preserving yield inside the Germany domestic courier, express and parcel market.

Urban Micro-Fulfillment Networks

Automated mini-warehouses of 5,000–10,000 sq m bring 10,000+ SKUs within two-hour radii. Otto Group sites process 10,000-15,000 daily orders, cutting trunk-haul kilometers and boosting last-mile density. Flaschenpost’s beverage hubs double stop counts per kilometer, showing model scalability. Rising city rents and labor costs require two-plus orders a month for profitability, which pushes carriers to weave MFC pickups into existing courier runs, improving truck utilization across the Germany domestic courier, express and parcel market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver shortage & labor costs | -0.6% | National, acute in Rhine-Ruhr, Hamburg, Berlin | Short term (≤ 2 years) |

| City-centre emissions restrictions | -0.4% | Berlin, Munich, Stuttgart, Cologne | Medium term (2-4 years) |

| Rail-first modal shift policies | -0.2% | National | Long term (≥ 4 years) |

| Cyber-security & data-breach liability | -0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortage and Labor Costs

Vacancies in German transport exceed 5%, double the national average. Wage deals in 2024 lifted salaries 6–8%, squeezing mid-tier operators that lack price power. DHL and DPD deploy e-cargo bikes and ground robots, but pedestrian-zone limits cap productivity to 30% over foot couriers. Turnover above 25% raises training costs, while court rulings increase the risk that gig couriers are deemed employees, adding social-security liabilities. Rural routes, already costly, become harder to staff, restraining the Germany domestic courier, express and parcel market expansion.

City-Centre Emissions Restrictions

More than 60 cities enforce low-emission zones; Berlin will require zero-emission vans inside the S-Bahn ring by 2028[1]Berlin Senate, “Low-Emission Zone Regulations,” berlin.de. DHL’s plan to field 20,000 electric vans demands EUR 10 billion and 1,000 chargers with E.ON[2]DHL Group, “Post & Parcel Germany Strategy,” dhl.com. Range limits shave productive hours, and hydrogen vans lack fueling sites—under 100 open stations nationally—with fuel 40% costlier than diesel. Early adopters bear depreciation risk, yet laggards lose urban access, creating compliance drag on the Germany domestic courier, express and parcel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Speed of Delivery: Express Poised to Outpace Standard

Non-express services retained 74.70% of the Germany domestic courier, express and parcel market share in 2024. Express bookings, however, are projected to log a 4.10% CAGR, supported by automotive just-in-time replenishment and healthcare biologics. The Germany domestic courier, express and parcel market size for express tiers translates to higher yields, because B2B shippers rarely return parcels and accept surcharges for four-hour windows. DHL’s 50-city same-day footprint and UPS’s refrigerated fleet after its Frigo-Trans and BPL buy position both to capture premium flows.

Margin dynamics favor express, which delivers roughly 25% better EBIT per parcel than standard. Still, non-express volumes underpin network utilization, helping carriers dilute fixed costs in sorting, IT and locker infrastructure. Amazon’s next-day offering, priced near standard rates, blurs the boundary and forces rivals to raise speed without eroding yield. As a result, the Germany domestic courier, express and parcel market blends multi-tier menus—economy, standard, next-day and same-day—so shippers self-select by urgency, stabilizing revenue per stop.

By Shipment Weight: Medium Parcels Gain on Near-Shoring

Light parcels led with 48.33% share in 2024 thanks to apparel and electronics B2C flows. Yet medium-weight consignments between 5 kg and 20 kg will climb fastest at 3.94% to 2030 as component suppliers ship small batches from near-shore factories. The Germany domestic courier, express and parcel market size for medium parcels expands when manufacturers transition from containerized freight to parcel networks for flexibility[3]Hermes Germany, “Iłowa Facility Opening,” hermesworld.com.

Light parcels face fee compression as free-shipping thresholds rise, but medium weights offer superior unit economics. Hermes reinforced belts in its Iłowa super-hub to handle 30-kg items destined for German assembly lines. Heavy parcels above 20 kg remain a niche as shippers turn to LTL carriers. Consequently, operators that diversify toward medium-weight industrial parts enjoy 5–7 percentage-point EBITDA lifts inside the Germany domestic courier, express and parcel market.

By End User Industry: Healthcare Cold-Chain Accelerates

E-commerce still generated 39.06% of revenue in 2024, but its 3.72% growth reflects market saturation. Pharmaceutical and diagnostic shipments require 2–8 °C control and GDP compliance, enabling double-digit price premiums. UPS’s newly acquired 15 cold-stores expand coverage for clinics and trial sites. The Germany domestic courier, express and parcel market size devoted to healthcare balloons as biologics and specialty drugs proliferate.

Manufacturing stays resilient through spare-parts flows, though some bulk moves shift to pallet networks. BFSI paper shipments shrink with e-signatures, but resale platforms push C2C fashion parcels higher. Thus vertical specialization around healthcare and industrial spare parts offers richer margins, shaping investment priorities across the Germany domestic courier, express and parcel market.

By Business Model: C2C Delivers Fastest Growth

B2C kept 46.80% share in 2024, yet C2C is advancing 5.12% annually on the back of Vinted, eBay Kleinanzeigen and Momox APIs that auto-generate shipping labels. Low-value items need low fees, so carriers extend parcel-shop networks to compress pickup costs. DPD and GLS plan 20,000+ shared outlets and 2,000 open lockers by 2026.

By Mode of Transport: Air Freight Climbs on Premium Demand

Road trucks handled 38.20% of parcels in 2024, but airport hubs upgrade to capture growing express flows. Frankfurt’s CargoHub aims for 3 million tonnes by 2040 through new terminals and rail links. FedEx’s EUR 125 million Kabelsketal site in Leipzig raises sortation by 30% and shortens Europe-wide transit times. The Germany domestic courier, express and parcel market size for air segments therefore expands even as rail pilots target CO₂ cuts.

Rail gains subsidies yet struggles with 24-hour delays from multiple handoffs, limiting share. Carriers may deploy hybrid truck-rail-air chains to balance cost, speed and carbon goals, but each mode demands distinct assets and know-how, stretching capital budgets throughout the Germany domestic courier, express and parcel market.

Geography Analysis

Metropolitan regions—Rhine-Ruhr, Berlin, Hamburg, Munich and Frankfurt—generated more than 60% of parcel volumes in 2024 despite housing 35% of residents. Locker density exceeds one unit per 500 households in these areas, driving 24/7 collection and lowering failed-delivery costs. Expansion of the OneStopBox open locker grid, adding 100 units in 2024 and targeting 2,000 more by 2025, prioritizes stations, malls and campuses that guarantee 50+ daily interactions.

Rural stops, typically eight to ten per hour, double the cost per parcel versus urban routes. Carriers test cluster delivery windows and parcel-shop aggregation to restore economics, yet consumer adoption remains under 30%. Amazon’s promise of sub-24-hour coverage for 90% of households raises nationwide expectations, stretching the Germany domestic courier, express and parcel market cost curve.

Eastern states such as Brandenburg, Saxony and Thuringia log 6–8% annual parcel growth, outpacing the 3–4% gains in mature western zones. Hermes leverages its Polish hub only 80 km from the border to exploit labor and subsidy advantages, then injects sorted flows into German last-mile loops. Future network redesigns will mix cross-border super-hubs with dense domestic micro-centers, optimizing the Germany domestic courier, express and parcel market for both cost and service.

Competitive Landscape

The top three operators—DHL, DPD, and Hermes hold a significant share in shipments, giving the German domestic courier, express, and parcel market a moderate concentration. DHL’s integrated mail-parcel platform plus 14,200 lockers secure over 40% share, backed by a EUR 10 billion spend on electrification and AI routing. DPD and GLS counter with a locker-shop alliance that spreads infrastructure costs and widens consumer access.

Strategic white space lies in high-compliance verticals. UPS’s 200-vehicle refrigerated fleet and 15 GDP hubs address rising drug volumes, while FedEx modernizes Leipzig to cut intra-EU transit times. Startups attack C2C micro-niches with gig couriers and robot pilots, though employment-law uncertainty clouds scalability. Investment races center on locker density, electric fleets and data platforms, each demanding capital and scale, thereby reinforcing incumbents’ grip on the Germany domestic courier, express and parcel market.

Recent Industry Developments

- October 2024: Hermes inaugurated a 118,000 sq m cross-border hub in Iłowa, Poland, to process 110 million parcels annually and serve German-Polish lanes.

- October 2024: DPD and GLS formed a nationwide locker and parcel-shop partnership targeting 20,000 outlets by 2026.

- September 2024: UPS bought Frigo-Trans and BPL, adding 200+ temperature-controlled vehicles and 15 cold-stores to its European network.

- March 2024: UPS expanded its Frankfurt Airport hub, adding 5,000 sq m and boosting daily capacity 20%.

Germany Domestic Courier, Express And Parcel (CEP) Market Report Scope

| Express |

| Non-Express |

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

| E-commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| Road |

| Air |

| Others |

| By Speed of Delivery | Express |

| Non-Express | |

| By Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| By End User Industry | E-commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| By Mode of Transport | Road |

| Air | |

| Others |

Key Questions Answered in the Report

How large is the Germany domestic courier, express and parcel market in 2025?

The Germany domestic courier, express and parcel market size is USD 19.53 billion in 2025 and is forecast to reach USD 23.11 billion by 2030.

What is the expected growth rate for Germany’s domestic parcel volumes to 2030?

Overall revenue is projected to rise at a 3.42% CAGR, with express services outpacing non-express at 4.10% annually.

Which delivery speed segment is expanding fastest in Germany?

Express and same-day tiers are the quickest-growing segments, supported by automotive and healthcare shippers that pay premiums for time-definite guarantees.

Why are medium-weight parcels gaining share in Germany?

Near-shoring of manufacturing moves small-batch components across short distances, increasing 5–20 kg shipments at a 3.94% CAGR.

How are carriers tackling urban emission rules in Germany?

Major operators are investing in electric vans, hydrogen pilots and dense locker networks to comply with low-emission-zone deadlines while protecting margins.

Which region inside Germany shows the strongest parcel growth?

Eastern states such as Brandenburg and Saxony are expanding 6–8% yearly, supported by cross-border hubs that leverage lower Polish labor costs.

Page last updated on: