Generative AI-powered Social Engineering and Deepfake Detection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

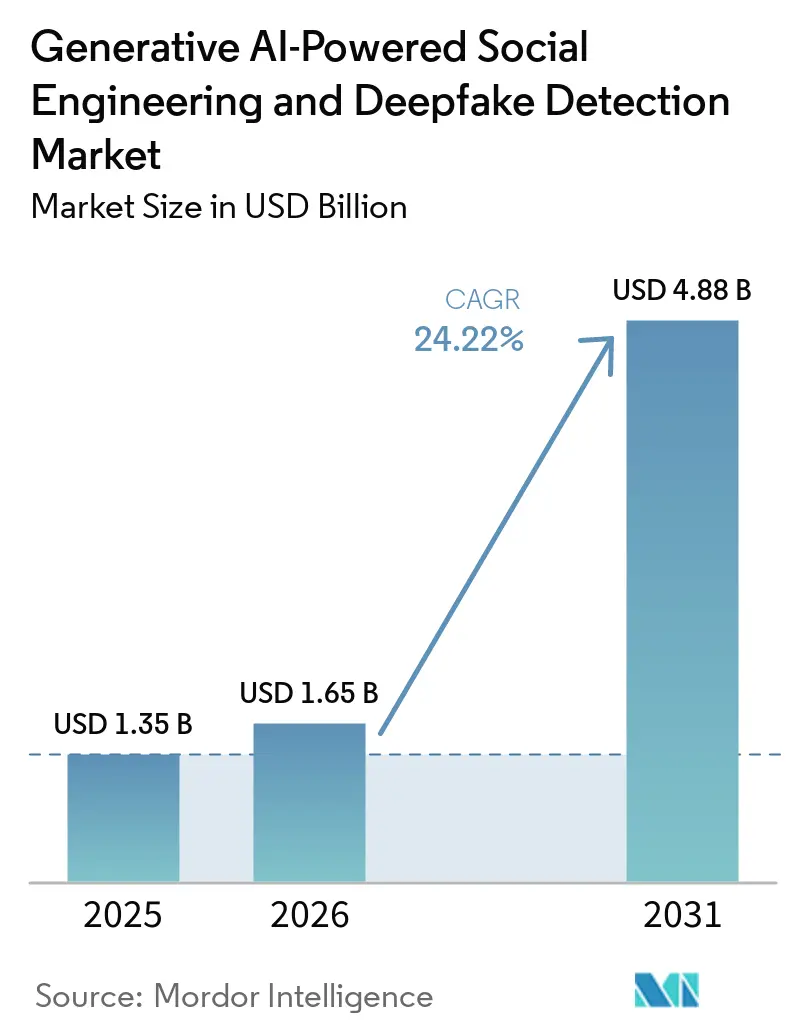

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 4.88 Billion |

| Growth Rate (2026 - 2031) | 24.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Generative AI-powered Social Engineering and Deepfake Detection Market Analysis by Mordor Intelligence

The Generative AI-powered Social Engineering and Deepfake Detection Market size is expected to increase from USD 1.35 billion in 2025 to USD 1.65 billion in 2026 and reach USD 4.88 billion by 2031, growing at a CAGR of 24.22% over 2026-2031. The Generative AI-powered Social Engineering and Deepfake Detection Market is expanding as AI-generated fraud has moved from isolated misuse to organized, repeatable attacks across identity verification, customer onboarding, and contact center workflows. Enterprises are now treating voice, face, document, and behavioral checks as a single set of controls because attackers increasingly combine them within the same fraud attempt. The Generative AI-powered Social Engineering and Deepfake Detection Market is also benefiting from stronger buying interest in continuously updated platforms that can support compliance reviews, remote approvals, and large transaction volumes without long deployment cycles. Competition is shifting toward vendors that can refresh models quickly, support real-time analysis, and maintain larger synthetic media libraries for adversarial training. The Generative AI-powered Social Engineering and Deepfake Detection Market is creating clear opportunities in healthcare, remote meeting verification, and smaller enterprises, where API-led tools and consumption pricing are making adoption easier.

Key Report Takeaways

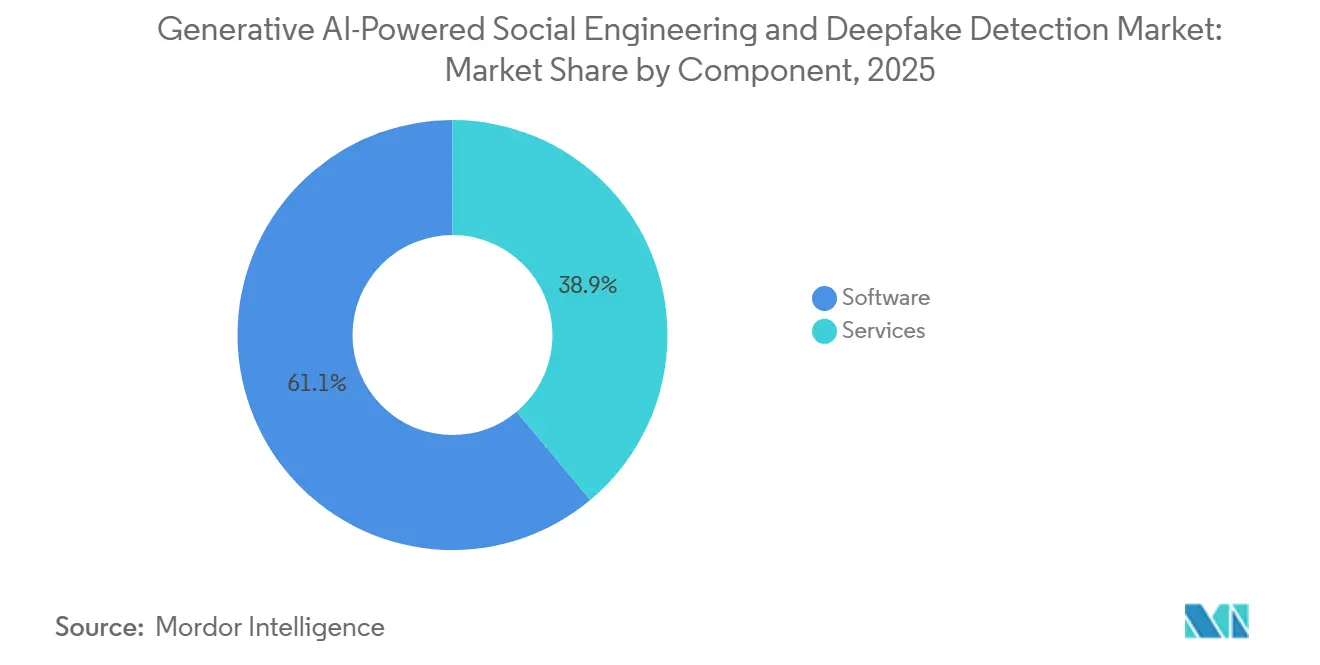

- By component, software held a 61.02% share in the Generative AI-powered Social Engineering and Deepfake Detection Market in 2025, while services are projected to expand at a 25.41% CAGR through 2031.

- By detection modality, video detection accounted for a 29.18% share in 2025, while audio detection is projected to grow at a 25.52% CAGR through 2031.

- By deployment, cloud accounted for 54.11% of the Generative AI-powered Social Engineering and Deepfake Detection Market in 2025, while hybrid deployment is projected to grow at a 25.63% CAGR through 2031.

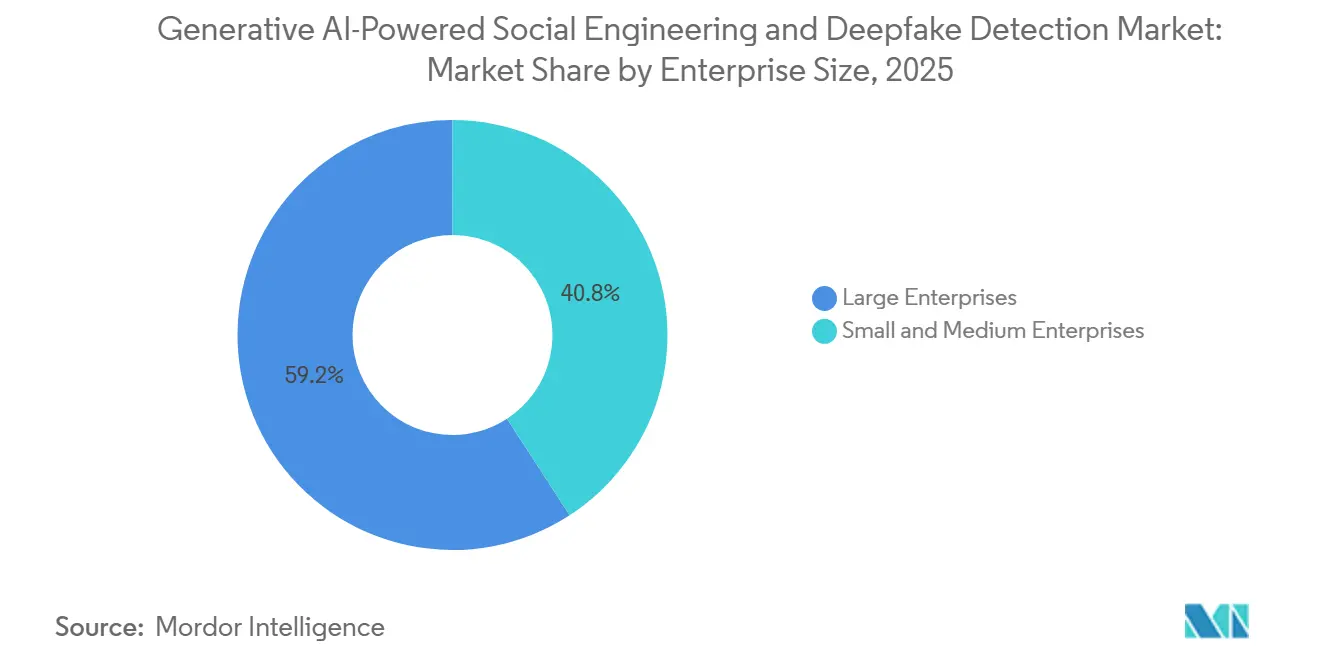

- By enterprise size, large enterprises held a 59.17% share in 2025, while small and medium enterprises are projected to expand at a 25.74% CAGR through 2031.

- By end-user industry, BFSI captured a 16.19% share in 2025, while healthcare and life sciences are projected to grow at a 25.85% CAGR through 2031.

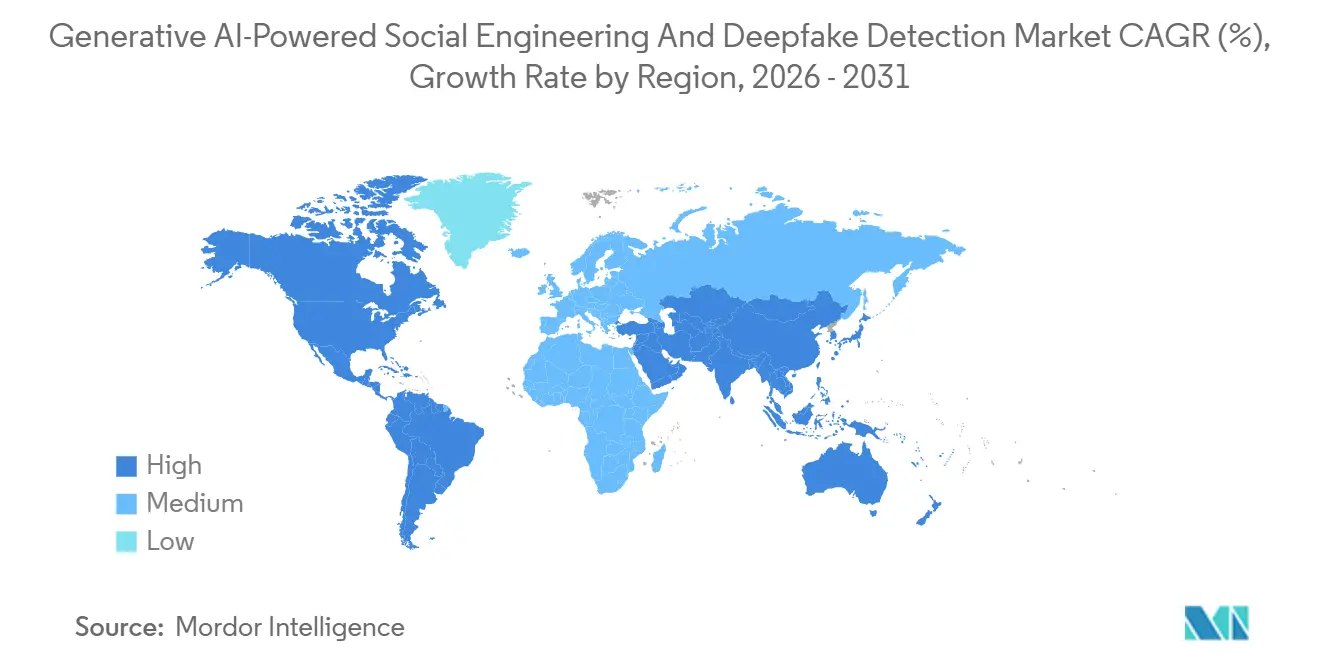

- By geography, North America led with a 32.13% share in 2025, while Asia-Pacific is projected to record the highest CAGR at 25.96% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Generative AI-powered Social Engineering and Deepfake Detection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Deepfake-Enabled Fraud in Digital Identity Workflows | +6.5% | Global, with concentration in North America, Europe, and Asia-Pacific financial centers | Short term (≤ 2 years) |

| Agentic AI and Voice Cloning Increasing Social Engineering Attack Surface | +5.5% | Global, particularly high in North America and Western Europe | Short term (≤ 2 years) |

| Enterprise Shift Toward Multimodal Fraud Detection | +4.0% | North America and Europe, with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Real-Time Verification Demand in Remote and Hybrid Workflows | +3.5% | Global, with emphasis on North America, Western Europe, and urban Asia-Pacific centers | Short term (≤ 2 years) |

| High-Value Use Of Synthetic Media Detection n BFSI and Government | +3.0% | North America, Europe, and Middle East | Medium term (2-4 years) |

| Expansion of API-Led Trust and Safety Integrations | +2.0% | Global, especially North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Deepfake-Enabled Fraud in Digital Identity Workflows

The Generative AI-powered Social Engineering and Deepfake Detection Market is being pushed most directly by the industrialization of identity fraud across digital verification systems. AU10TIX reviewed more than 9 million identity verification transactions in Q1 2026 and found 3 active fraud rings running coordinated campaigns, with 1 campaign peaking at 1.3 million fraud events in a single day. The same report showed AI-generated selfie attacks rising 54.5% quarter over quarter in Q1 2026, while 67.6% of identity verification sessions still lacked deepfake detection. The Federal Reserve stated in April 2025 that deepfake attacks had increased twentyfold over the prior 3 years and urged banks to strengthen facial, voice, and behavioral identity checks. This pattern is widening the role of the Generative AI-powered Social Engineering and Deepfake Detection Market from a fraud tool into a required control for regulated digital identity workflows.[1]Michael S. Barr, “Cybersecurity In The Banking System,” Federal Reserve Board, federalreserve.gov

Agentic AI and Voice Cloning Increasing Social Engineering Attack Surface

The Generative AI-powered Social Engineering and Deepfake Detection Market is also rising because agentic AI can now sustain longer voice and video interactions that feel believable enough to bypass older verification habits. Pindrop stated in February 2026 that more than half of healthcare contact center fraud attempts now include AI-generated elements, which shows that the threat is no longer limited to consumer scams or isolated spoofing. The company also reported a 1,210% surge in AI-driven fraud attempts in 2025, reinforcing why telephony and contact center defenses are rising enterprise spending lists. Voice cloning tools can now generate convincing synthetic speech from as little as 3 seconds of source audio, weakening older methods that relied on familiarity with a caller’s voice or simple callback procedures. As a result, the Generative AI-powered Social Engineering and Deepfake Detection Market is seeing stronger demand for real-time audio analysis that can operate during the call rather than after the loss is already recorded.

Enterprise Shift Toward Multimodal Fraud Detection

The Generative AI-powered Social Engineering and Deepfake Detection Market is benefiting from the shift away from single-channel defenses toward platform-based detection. GetReal Security reported in 2026 that 41% of surveyed IT and cybersecurity leaders said their organizations had hired and onboarded a fraudulent candidate, while 88% said they encountered deepfake or impersonation attacks at least occasionally. A 2025 study in Frontiers in Artificial Intelligence found that cloned-voice detection methods based on MFCC features did not generalize well across different cloning algorithms, supporting the case against isolated modality models.[2]Detection Of Cloned Voices In Realistic Forensic Voice Comparison Scenarios,” Frontiers In Artificial Intelligence, frontiersin.org Resemble AI said its DETECT-3B Omni model reached 98% detection accuracy across more than 38 languages and covered audio, video, images, and text, reflecting the kind of vendor capability enterprise buyers are beginning to expect. That shift is widening the role of the Generative AI-powered Social Engineering and Deepfake Detection Market beyond point products and into integrated trust, safety, and identity platforms.

Real-Time Verification Demand in Remote and Hybrid Workflows

The Generative AI-powered Social Engineering and Deepfake Detection Market is also benefiting from the spread of remote hiring, digital onboarding, and video-based approvals that rely on live verification rather than in-person checks. iProov said in 2025 that it had surpassed 1 million daily identity verification transactions, which shows how large the volume of exposed remote identity events has become.[3]iProov, “iProov Announces iProov Verified Meetings To Tackle Deepfake Risks In Video Calls,” iProov, iproov.com The company launched iProov Verified Meetings in May 2026 to authenticate video call participants in real time via a Red-Amber-Green interface, directly addressing fraud risk in remote meetings. A 2026 study in Frontiers in Bioengineering and Biotechnology found that multi-modal coherence analysis outperformed single-modality detection in telemedicine environments where compression and obfuscation are common. This is pushing the Generative AI-powered Social Engineering and Deepfake Detection Market toward faster inference, tighter workflow integration, and stronger support for live risk scoring.[4]iProov, “iProov Scales To Over 1 Million Daily Transactions As Deepfakes Redefine The Enterprise Attack Surface,” iProov, iproov.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| False Positive Sensitivity In High-Stakes Verification Flows | -1.8% | Global, particularly in North America and Europe where compliance stakes are highest | Short term (≤ 2 years) |

| Data Access Constraints For Model Training And Benchmarking | -1.5% | Global, with particular severity in regions with strict data localization laws, including Europe and Asia-Pacific | Medium term (2-4 years) |

| Fragmented Adversarial Attack Patterns Across Languages And Modalities | -1.2% | Asia-Pacific and Middle East and Africa, with spill-over to South America | Long term (≥ 4 years) |

| Budget Friction For Continuous Model Refresh And Human Review | -0.8% | Global, with higher impact on small and medium enterprises in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

False Positive Sensitivity in High-Stakes Verification Flows

The Generative AI-powered Social Engineering and Deepfake Detection Market still faces a hard adoption limit when legitimate users are flagged during sensitive verification events. iProov announced in February 2026 that its Dynamic Liveness solution achieved CEN/TS 18099 Level 2 High and Ingenium Level 4 certification, while maintaining a Bona Fide Presentation Classification Error Rate of 1.3%, a notable achievement that demonstrates deepfake resilience without a significant increase in false positives. That performance level is still difficult for much of the Generative AI-powered Social Engineering and Deepfake Detection Market to match consistently in real operating conditions. In contact centers, public telephone quality, mobile compression, and background noise narrow the practical accuracy gap between leading and average vendors, often forcing additional review steps. The result is slower deployment in healthcare, government, and financial workflows, where a wrongful denial can create operational, legal, and customer service costs.

Data Access Constraints for Model Training and Benchmarking

The difficulty of gathering comprehensive data also constrains the Generative AI-powered Social Engineering and Deepfake Detection Market, as well as the availability of up-to-date training data across languages, attack methods, and content types. The 2025 Frontiers in Artificial Intelligence study showed that cloned-voice detection methods can break down when tested against cloning algorithms not present in the training data. A 2025 Springer Nature study also found that audio deepfake performance drops when models encounter synthesis techniques outside their training set, a structural problem in a field where new-generation methods continue to emerge. The MedForge research accepted to ACL 2026 introduced a 90,000-sample benchmark for realistic medical image edits, demonstrating progress in healthcare-specific training data but also underscoring the continued incompleteness of comparable datasets in other use cases. This gives vendors in the Generative AI-powered Social Engineering and Deepfake Detection Market an advantage, enabling them to build proprietary synthetic libraries internally and refresh them faster than their peers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors The Defense Stack While Services Scale Faster

Software held a 61.02% share of the market in 2025, which shows that buyers still prefer platforms they can run continuously rather than isolated project work. The software layer in the Generative AI-powered Social Engineering and Deepfake Detection Market covers deepfake detection and authentication tools, biometric liveness checks, social engineering detection, and risk analytics that support the full identity attack chain. Enterprises favor software because detection logic must be updated often, and that makes recurring platform relationships more practical than one-time implementations. Reality Defender launched a public API and a free tier in July 2025, with 50 free detections per month, reflecting how software vendors are opening access to developer teams and large security buyers.

Services are projected to grow at a 25.41% CAGR through 2031, making them the fastest-growing component of the Generative AI-powered Social Engineering and Deepfake Detection Market. This growth reflects the need for continuous model retraining, managed detection, red-team operations, deployment support, and ongoing tuning as attack methods change. The 2025 Springer Nature research on audio deepfake detection supports this pattern, showing that performance degrades when models encounter unfamiliar synthesis methods. Service-heavy operating models are becoming increasingly important because many enterprises want help with response rules, human review paths, and ongoing testing, rather than just buying raw detection software.

By Detection Modality: Video Leads While Audio Records The Fastest Gain

Video detection accounted for 29.18% of the market in 2025, reflecting the weight of face-related fraud risk across onboarding, KYC, and live meeting environments. The Generative AI-powered Social Engineering and Deepfake Detection Market still places video first because face deepfakes can affect customer account opening, employee screening, and executive impersonation inside the same enterprise. Image detection supports adjacent use cases such as manipulated identity documents, while text and document detection are becoming more relevant as generated phishing content and fabricated records become easier to produce. iProov’s 2026 Threat Intelligence Report said that image-to-video tools are making it easier to create realistic synthetic identities from limited source material, which supports continued investment in video-focused defenses.

Audio detection is projected to grow at a 25.52% CAGR through 2031, making it the fastest-growing modality in the Generative AI-powered Social Engineering and Deepfake Detection Market. Pindrop said its platform can detect synthetic and bot-generated speech with up to 99.2% accuracy using 2 seconds of inbound audio in real time, which shows why category leaders are gaining attention in call-heavy workflows. Audio is scaling faster because voice remains a trusted channel in banking, insurance, healthcare, and account recovery, even though cloning tools have become easier to use and harder for humans to recognize. The gap between how quickly video defenses matured and how recently audio defenses started to scale suggests that fresh investment in voice-layer protection will remain strong across the forecast period.

By Deployment: Cloud Leads While Hybrid Becomes The Practical Choice

Cloud deployment accounted for 54.11% of the market in 2025, reflecting its advantages of faster rollout, lower upfront costs, and simpler model update cycles. The Generative AI-powered Social Engineering and Deepfake Detection Market relies heavily on cloud delivery because many customers require API access, rapid integration, and shared infrastructure to absorb traffic spikes. Cloud is especially well-suited to technology platforms, retail environments, and digital financial services workflows where the surrounding architecture is already cloud native. At the same time, on-premises deployment remains relevant in government, intelligence, and tightly regulated financial settings where sensitive biometric and identity data cannot move easily outside controlled environments.

Hybrid deployment is projected to expand at a 25.63% CAGR through 2031, which makes it the fastest-growing architecture in the Generative AI-powered Social Engineering and Deepfake Detection Market. This model is gaining ground because it allows light screening and response decisions close to the source while sending only selected events for deeper cloud analysis. Hybrid setups are a practical fit for contact centers and video verification flows where low latency matters, but data-handling rules still limit how far raw media can travel. As a result, the Generative AI-powered Social Engineering and Deepfake Detection Market is increasingly favoring deployment choices that balance response speed, privacy controls, and operational flexibility rather than pushing one architecture across every use case.

By Enterprise Size: Large Enterprises Hold Revenue While Small And Medium Enterprises Expand Faster

Large enterprises held 59.17% of the Generative AI-powered Social Engineering and Deepfake Detection Market share in 2025, which reflects their greater fraud exposure and stronger capacity to fund continuous monitoring. These organizations run more complex identity workflows, handle larger transaction volumes, and face greater compliance demands across financial services, government, healthcare, and large platform operations. Procurement patterns are shifting from multiple narrow tools toward broader multimodal platforms that support unified audit trails, enterprise integrations, and consistent policy controls. Jumio launched Liveness Premium in June 2025 and said early-release deployments showed a 30% increase in detecting sophisticated injection attacks and deepfakes, which meet the needs of larger organizations looking for stronger, certified protection.

Small and medium enterprises are projected to grow at a 25.74% CAGR through 2031, making them the fastest-scaling size tier in the Generative AI-powered Social Engineering and Deepfake Detection Market. Growth in this segment is being supported by API-native products and consumption pricing that remove much of the upfront cost and staffing burden that once limited adoption. Resemble AI raised USD 13 million in December 2025 to scale its multilingual DETECT-3B Omni platform and broaden distribution through identity ecosystem partners, which supports easier access for smaller buyers. GetReal Security’s finding that 41% of surveyed organizations had hired and onboarded a fraudulent candidate is especially important for smaller firms, as many lack dedicated fraud teams and need automation to close that gap.

By End-User Industry: BFSI Leads While Healthcare And Life Sciences Grow Faster

BFSI held a 16.19% share of the market in 2025, making it the largest end-user group in the Generative AI-powered Social Engineering and Deepfake Detection Market. Banks, insurers, and payment providers face a high concentration of identity abuse, account takeover attempts, and social engineering attacks that can move funds quickly if verification fails. Feedzai reported in 2025 that 90% of financial institutions are actively combating emerging fraud with AI-powered tools, while 44% of financial professionals said deepfakes were used in fraudulent schemes and 56% cited AI-powered social engineering as a major related threat. Government, IT and telecom, retail and e-commerce, and manufacturing each add demand through their own exposure to impersonation, procurement fraud, account abuse, and credential-based deception.

Healthcare and life sciences are projected to grow at a 25.85% CAGR through 2031, making them the fastest-expanding end-user segment in the Generative AI-powered Social Engineering and Deepfake Detection Market. Pindrop said in February 2026 that more than half of healthcare contact center fraud attempts now involve AI-generated elements, which shows why provider, payer, and benefits workflows are drawing more attention. The MedForge research accepted to ACL 2026 introduced MedForge-90K for realistic medical image manipulation detection, which points to the rapid specialization of deepfake defense tools for clinical environments. This part of the Generative AI-powered Social Engineering and Deepfake Detection Market is gaining speed because fraud risk now extends beyond voice impersonation into synthetic records, manipulated images, and altered clinical documentation.

Geography Analysis

North America held a 32.13% share of the market in 2025, maintaining its lead in the Generative AI-powered Social Engineering and Deepfake Detection Market. The region benefits from a dense base of financial institutions, public agencies, and technology platforms that run high-assurance identity workflows every day. The Federal Reserve warned in April 2025 that deepfake attacks had increased 20-fold over the previous 3 years, reinforcing the need for stronger biometric and behavioral verification in banking. The SEC said in March 2025 that 25.9% of executives reported their organizations had experienced 1 or more deepfake incidents, which added further pressure on financial and corporate controls.

Europe is the second-largest regional market for generative AI-powered social engineering and deepfake detection, with Germany, the United Kingdom, and France as the main centers of enterprise demand. Regional adoption is being shaped by strong compliance expectations and by the need to protect digital identity, financial approvals, and corporate communications from manipulated media. Enterprises across the region are showing rising interest in auditable detection tools that can support disclosure, review, and evidentiary needs when suspicious content appears in regulated workflows. Data handling caution around biometric and identity media is also encouraging deployment choices that keep tighter control over sensitive inputs.

Asia-Pacific is projected to grow at a 25.96% CAGR through 2031, making it the fastest-growing region in the Generative AI-powered Social Engineering and Deepfake Detection Market. Growth is supported by the rapid expansion of digital payments, high transaction volumes, and a rising need to protect onboarding and verification systems from synthetic identity abuse. China’s synthetic content labeling rules took effect on September 1, 2025, and require platform-level content labeling and provenance controls, thereby increasing the operational need for detection infrastructure at scale. South America remains an earlier-stage opportunity, with Brazil standing out as digital banking and government identity programs broaden the number of exposed workflows. The Middle East and Africa are led by the United Arab Emirates and Saudi Arabia, where digital government programs and financial modernization are raising interest in deepfake defense tools. South Africa and Nigeria contribute to regional demand because mobile and digital banking channels create a larger base of customer interactions exposed to fraud.

Competitive Landscape

The Generative AI-powered Social Engineering and Deepfake Detection Market remained moderately fragmented in 2026, with more than 59 identified third-party providers worldwide. This structure means the market lacks a single dominant incumbent, and competition is shaped more by technical differentiation than by sheer scale. Vendors are separating themselves through breadth of modality support, inference speed, workflow integration, and the depth of their proprietary synthetic media libraries used to train detection systems. The Generative AI-powered Social Engineering and Deepfake Detection Market is also rewarding vendors that can provide independent validation rather than relying solely on self-reported performance. iProov’s February 2026 certification to CEN/TS 18099 Level 2 High and Ingenium Level 4 illustrates how third-party testing is becoming an important sales advantage in government and regulated financial accounts.

Strategy in the Generative AI-powered Social Engineering and Deepfake Detection Market is clustering around API-first distribution, deeper vertical specialization, and tighter integration with existing security and identity stacks. Reality Defender’s July 2025 public API and free tier launch showed how vendors are trying to widen developer adoption while still maintaining enterprise pathways for larger deployments. Pindrop’s February 2026 healthcare expansion took a different path, with real-time synthetic voice and video detection deployed in HIPAA-regulated environments where fraud consequences are high and workflow trust matters. Resemble AI’s December 2025 funding round added another strategic signal, as it was aimed at accelerating the deployment of a multilingual, multimodal detection model through broader ecosystem relationships.

The Generative AI-powered Social Engineering and Deepfake Detection Market still has wide room to penetrate routine identity workflows. AU10TIX said deepfake detection was absent in 67.6% of identity verification sessions in Q1 2026, suggesting a large unmet adoption base even as fraud activity becomes more organized. A large opportunity remains in multilingual and non-English detection, where data scarcity and rapidly changing attack styles still create accuracy gaps across many vendors. Companies that can generate, test, and refresh synthetic media internally are likely to defend against performance better as new attack methods emerge. Even so, the Generative AI-powered Social Engineering and Deepfake Detection Market remains far from concentrated, as buyers continue to evaluate vendors based on workflow fit, operational speed, and evidence quality rather than brand size alone.

Generative AI-powered Social Engineering and Deepfake Detection Industry Leaders

Microsoft Corporation

Reality Defender, Inc.

Sensity AI

Pindrop Security, Inc.

iProov Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Truepic and Cotality announced a strategic integration enabling authenticated virtual property inspections for mortgage lenders through Cotality's Mercury Network and Collateral Management System platforms, announced June 23, 2026, targeting home equity evaluations, disaster documentation, construction and renovation draws, and default servicing, expanding Truepic's visual risk intelligence platform into real estate finance workflows.

- May 2026: AU10TIX's Q1 2026 Global Identity Fraud Benchmark Report, released May 27, 2026, documented that AI-generated fraud surpassed physical document forgery for the first time on record, with AI-generated selfie attacks rising 54.5% quarter-over-quarter and a single coordinated fraud campaign peaking at 1.3 million fraud events in 1 day, underscoring that fraud operations now function as industrialized, multi-platform infrastructure.

- May 2026: iProov launched iProov Verified Meetings on May 19, 2026, enabling real-time deepfake detection for video conference participants as part of its Workforce Solutions Suite, with a Red-Amber-Green status interface that allows hosts to verify participant authenticity without alerting potential attackers or disrupting call flow, targeting remote hiring, financial approvals, and account recovery workflows.

- April 2026: iProov released its 2026 Threat Intelligence Report on April 8, 2026, documenting how generative AI is enabling threat actors to scale synthetic identity attacks using widely accessible image-to-video generation tools, with deepfakes increasingly used beyond identity verification and into everyday corporate video workflows.

Global Generative AI-powered Social Engineering and Deepfake Detection Market Report Scope

The Generative AI-powered Social Engineering and Deepfake Detection Market comprises solutions and services that leverage artificial intelligence to identify, prevent, and mitigate risks posed by deepfakes, synthetic media, and AI-driven social engineering attacks. These platforms encompass video, audio, image, and text-based detection technologies, biometric liveness verification, threat intelligence, and risk analytics to safeguard organizations against identity fraud, misinformation, and manipulation. Driven by the rapid rise of generative AI tools, increasing incidents of deepfake-enabled fraud, and regulatory demands for digital trust and security, industries such as BFSI, healthcare, IT, manufacturing, retail, and government are adopting these solutions to protect sensitive data, ensure compliance, and maintain operational resilience. The primary objective of this market is to deliver proactive, intelligence-driven defenses that enhance trust, mitigate reputational and financial risks, and secure digital ecosystems against evolving AI-powered threats.

The Generative AI-powered Social Engineering and Deepfake Detection Market report is segmented by Component (Software [Deepfake Detection and Authentication Software, Biometric Liveness Detection Software, Social Engineering Detection and Prevention Software, Threat Intelligence and Risk Analytics Software], and Services), Detection Modality (Video, Audio, Image, Text and Document), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Deepfake Detection and Authentication Software |

| Biometric Liveness Detection Software | |

| Social Engineering Detection and Prevention Software | |

| Threat Intelligence and Risk Analytics Software | |

| Services |

| Video |

| Audio |

| Image |

| Text and Document |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | Deepfake Detection and Authentication Software | |

| Biometric Liveness Detection Software | |||

| Social Engineering Detection and Prevention Software | |||

| Threat Intelligence and Risk Analytics Software | |||

| Services | |||

| By Detection Modality | Video | ||

| Audio | |||

| Image | |||

| Text and Document | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the Generative AI-powered Social Engineering and Deepfake Detection Market?

The market stands at USD 1.65 billion in 2026 and is forecast to reach USD 4.88 billion by 2031 at a 24.22% CAGR.

Which region leads spending on deepfake and social engineering detection solutions?

North America leads with a 32.13% share in 2025 because of its concentration of financial institutions, government agencies, and technology platforms with high-assurance identity workflows.

Which content type is growing fastest in detection demand?

Audio detection is growing fastest at a 25.52% CAGR through 2031 as voice cloning becomes easier to deploy and harder to catch with human judgment alone.

Why does BFSI remain the largest end-user segment?

BFSI held a 16.19% share in 2025 because financial institutions face persistent identity fraud, payment risk, and regulatory pressure around customer verification.

Why are healthcare and life sciences becoming a major growth area?

Healthcare and life sciences are projected to grow at a 25.85% CAGR through 2031 because AI-generated fraud is moving into contact centers, records, images, and other sensitive care and payment workflows.

What kind of vendors are gaining the strongest competitive position?

Vendors with multimodal coverage, fast real-time analysis, strong workflow integration, and independently validated performance are gaining more attention in regulated and high-risk deployments.

Page last updated on: