Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

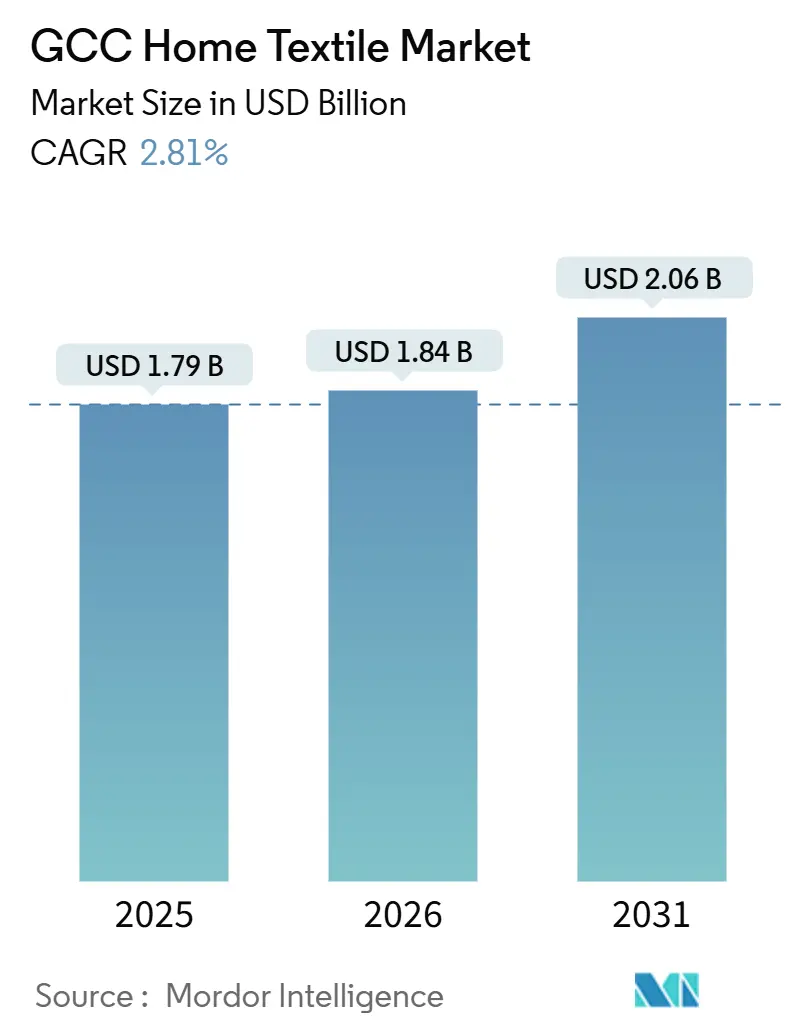

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.06 Billion |

| Growth Rate (2026 - 2031) | 2.81% CAGR |

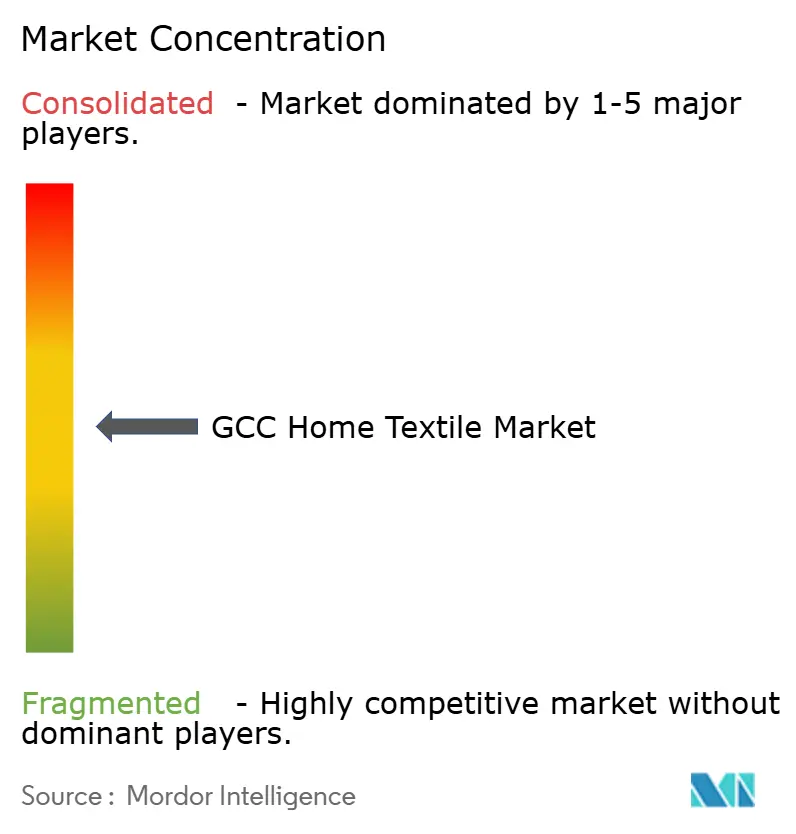

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Home Textile Market Analysis by Mordor Intelligence

The GCC home textile market size is expected to increase from USD 1.79 billion in 2025 to USD 1.84 billion in 2026 and reach USD 2.06 billion by 2031, growing at a CAGR of 2.81% over 2026-2031. Growth in the GCC home textile market continues to be anchored by institutional procurement cycles in hospitality and healthcare, while residential demand is shaped by new home handovers and the first-time purchase of complete textile sets. Compliance requirements and sustainability screening are now embedded into tenders, which favor certified, vertically integrated suppliers able to guarantee batch-level traceability and fast replenishment. Premiumization trends in luxury hospitality, including higher thread counts and antimicrobial finishes, support price realization in the upper tier despite cost volatility in inputs and logistics. Re-export and logistics ecosystems centered in the UAE sustain faster delivery into Saudi Arabia and the wider Gulf, improving availability for quick-turn assortments even during high season. Saudi housing programs and a rising homeownership base underpin the recurring baseline for bedding, toweling, and window treatments, while hotel development pipelines and branded residences lift commercial volumes in the GCC home textile market.

Key Report Takeaways

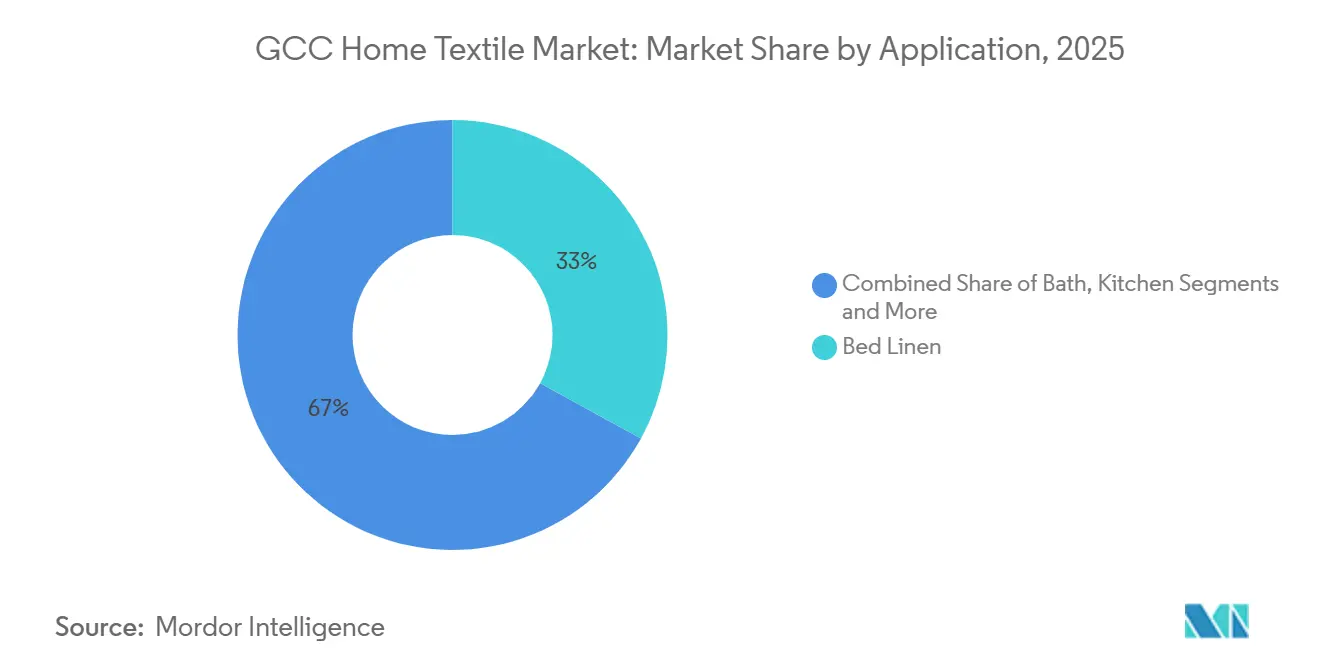

- By product type, bed linen led with 33% of the GCC home textile market share in 2025, while carpets and rugs are projected to expand at a 3.72% CAGR through 2031.

- By material, cotton held 68.42% of the GCC home textile market share in 2025, whereas alternative fibers are forecast to grow at a 5.64% CAGR through 2031.

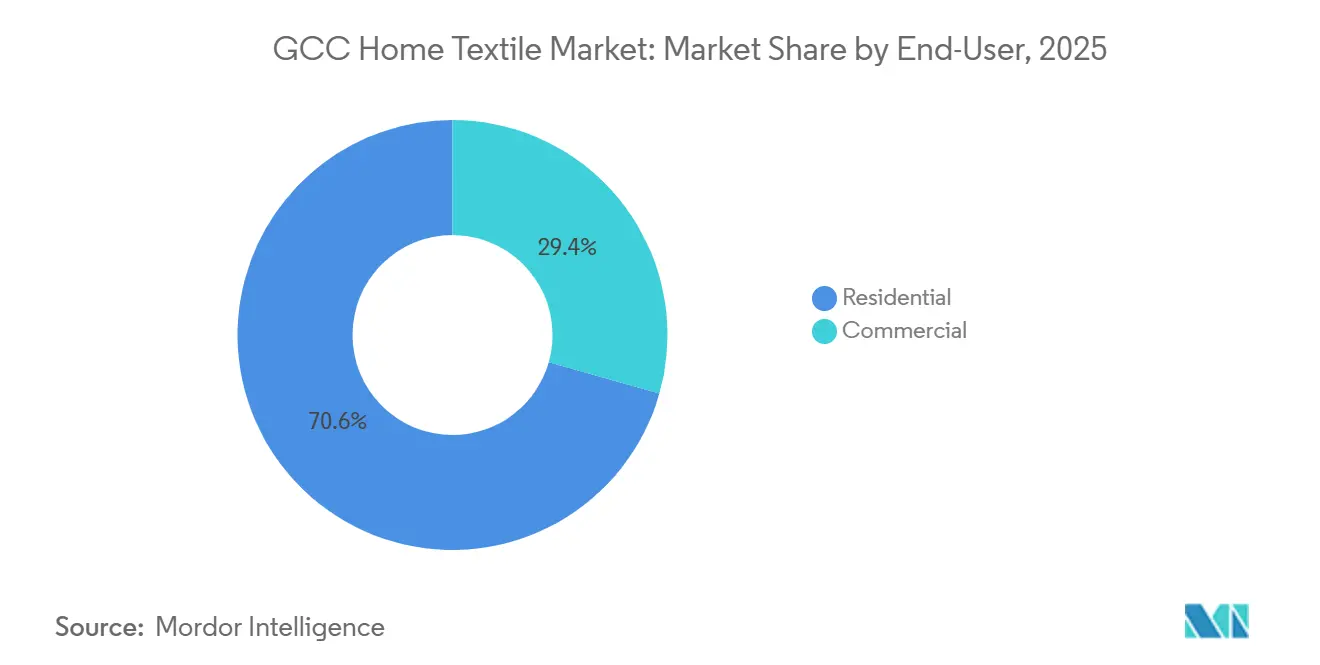

- By end user, residential accounted for 70.61% of the GCC home textile market share in 2025, while commercial is advancing at a 4.53% CAGR through 2031.

- By distribution channel, offline commanded 66.74% of the GCC home textile market share in 2025, whereas online is set to expand at a 6.51% CAGR through 2031.

- By geography, Saudi Arabia held 42% of the GCC home textile market share in 2025, while the UAE is projected to record the fastest 4.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hotel room pipeline in KSA and UAE lifts B2B linen demand | +0.8% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Housing programs and rising homeownership in Saudi Arabia boost residential textile purchases | +0.7% | Saudi Arabia, with spillover to Bahrain and Kuwait | Medium term (2-4 years) |

| Government economic diversification initiatives | +0.4% | GCC-wide with early gains in Riyadh, Dubai, Doha | Long term (≥ 4 years) |

| Premiumization in luxury hospitality, including FR and antimicrobial specifications | +0.5% | Saudi Arabia and UAE luxury clusters | Short term (≤ 2 years) |

| SASO and GSO textile compliance tightening raises certified sourcing | +0.3% | Saudi Arabia and GCC-wide adoption | Medium term (2-4 years) |

| UAE re-export hubs compress lead times for assortments | +0.2% | UAE with cross-border reach into Oman and Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hotel Room Pipeline in KSA and UAE Lifts B2B Linen Demand

Commercial procurement remains the center of gravity for the GCC home textile market, led by hotel openings and expansions that translate into large, repeat orders for sheets, duvet covers, and towels. Chain-led signing momentum in 2025 carried into 2026, with Marriott highlighting Saudi Arabia and the UAE among its highest growth Middle East markets and reporting more than 230 organic signings across EMEA in 2025, which supports multi-year linen frameworks for new and converted properties[1]Marriott International, “Marriott International Announces Robust Growth Momentum Across Europe, Middle East, Africa in 2025,” Marriott International, marriott.pressarea.com . Procurement teams specify par stocks that typically range to six full sets per key for high-occupancy hotels, which multiplies base room counts into sizeable textile tenders that renew on 18 to 24 month cycles in premium segments. Branded residences and mixed-use luxury developments also add institutional volume, as villa and apartment operators standardize bedroom, bath, and window treatments at handover to protect brand standards. Large owners and operators favor suppliers that can demonstrate end-to-end traceability and consistent testing documentation, which further consolidates spend among vertically integrated firms that can service multi-country pipelines. As operators scale, purchase orders often pool across clusters to capture volume discounts, which strengthens demand visibility for certified suppliers in the GCC home textile market.

Housing Programs and Rising Homeownership in Saudi Arabia Boost Residential Textile Purchases.

Saudi Arabia’s housing initiative and mortgage programs have lifted the owner-occupier share, which in turn stimulated initial household purchases of complete textile sets after unit handover. The Housing Program’s 2024 report confirmed progress on delivery of more than 122,000 housing solutions for Saudi families, reinforcing a steady pipeline of new households entering the market for bedding, toweling, kitchen textiles, and curtains[2]Saudi Press Agency, “Housing Program Annual Report 2024: Home Ownership Rate Reaches 65.4%, Surpassing 2025 Target,” Saudi Press Agency, spa.gov.sa. First-time buyers typically make consolidated purchases within weeks of key collection, which compresses demand into the same quarter and benefits distributors able to maintain inventory breadth closest to new communities. As more master-planned neighborhoods go live across major cities, developers and retailers coordinate curated packages that simplify selection and standardize quality, which supports higher attach rates for mid-tier and premium lines. The procurement model for these neighborhoods often embeds a short-list of approved vendors, which channels volume to suppliers with reliable documentation and post-sale support. These housing dynamics anchor a broad base of residential demand that complements institutional cycles in the GCC home textile market.

Government Economic Diversification Initiatives

Economic diversification agendas continue to prioritize tourism, entertainment, and mixed-use real estate, which sustains institutional buying of hospitality-grade bed and bath linens. Global brands are expanding their presence in Saudi Arabia and the UAE as part of this shift, with Marriott reporting a strong pipeline and record branded residential signings across EMEA in 2025, activity that carries direct implications for textile procurement in the region. Master developments that combine hotels, serviced apartments, and retail further blur the line between retail and institutional assortments, as operators enforce uniform textile standards across properties. Public and quasi-public clients are now including sustainability and safety conformity in their RFPs, which elevates the value of certifying labels and supplier testing capabilities. The transition from ad hoc purchasing to framework agreements with clear service levels and ESG requirements provides more predictable demand for compliant vendors. This policy-driven momentum continues to reinforce commercial volume within the GCC home textile market.

Premiumization in Luxury Hospitality, Including FR and Antimicrobial Specifications

Elevated specifications in four- and five-star properties are lifting average selling prices through higher thread counts, premium cottons, and antimicrobial finishes. Hotel groups and large operators now increasingly request percale weaves at T-300 and higher, with mercerization and tight shrinkage tolerances to hold up under industrial laundering, which aligns with procurement guides issued by specialized textile manufacturers serving global brands[3]Gencer Textile, “The Procurement Guide: Sourcing Premium Percale Bedding for US Hotel Brands,” Gencer Textile, gencertextile.com. Antimicrobial elements, including silver-ion treated fabrics validated to ISO efficacy standards for hygiene-sensitive environments, are showing up in large portions of healthcare and high-touch hospitality orders across the Gulf, which keeps replacement cycles within target while supporting guest comfort and odor control. Fire safety is non-negotiable in public spaces, with FR-compliant curtains and upholstery tested to standards such as NFPA 701 and BS 5852 Crib 5, where brand policies demand these benchmarks, which require consistent batch testing and records for audits. Luxury portfolios on the Arabian Peninsula have anchored these higher standards and are expanding their footprints, which sustains a thicker layer of premium demand in the GCC home textile market. Suppliers that invest in FR compliance, antimicrobial validation, and color fastness controls are best positioned to capture the premiumization gains tied to luxury development clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cotton and freight costs pressure pricing and margins | -0.6% | GCC-wide with acute pressure in Saudi Arabia and the UAE | Short term (≤ 2 years) |

| Fragmented retail landscape and private labels intensify price competition | -0.4% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Water scarcity limits local dyeing and finishing scalability | -0.3% | Saudi Arabia and the UAE | Long term (≥ 4 years) |

| Giga-project execution risks delay hospitality-driven orders | -0.2% | GCC-wide with concentration in Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Cotton and Freight Costs Pressure Pricing and Margins

Input and transport cost swings remain a key headwind for the GCC home textile market, since mills and distributors must manage quarterly variability in raw cotton and global shipping. Industry association updates for early 2026 point to choppy cotton pricing conditions around contract rollovers, which complicates fixed-price commitments with institutional clients that resist mid-cycle surcharges[4]National Cotton Ginners Association, “Weekly Cotton Market Update: Feb 28, 2026,” National Cotton Ginners Association, cottongins.org. Shipping costs stabilized from prior peaks but remain elevated compared with pre-pandemic baselines, while route disruptions across key lanes have lifted insurance and added days-in-transit on certain corridors, which challenge JIT replenishment for time-sensitive orders. Exporters documented the impact of rerouting and higher logistics expenses in 2024, with one leading South Asian mill reporting significant increases in selling costs tied to shipping detours and related premiums, which compressed margins at the supplier level. GCC importers often absorb part of these surges to preserve shelf prices for cost-sensitive residential shoppers, which reduces unit economics in promotional periods. Institutional buyers also negotiate volume flexibility into contracts, which can magnify the effect of adverse cost movements on supplier EBITDA. The combination of cotton volatility and freight variability forces more cautious buying and shorter tender tenures in the GCC home textile market.

Fragmented Retail Landscape and Private Labels Intensify Price Competition.

The residential channel remains fragmented with strong private-label penetration, which raises price competition and compresses branded margins in the GCC home textile market. Retailers and marketplaces increasingly leverage direct sourcing from mills to widen the price gap versus branded equivalents, which shifts volume toward house labels at mid-tier price points. Some brands are countering this trend by investing in direct-to-consumer channels that bypass traditional wholesale markups, which improves price realization and shortens feedback loops on product performance. Institutional procurement has mirrored this discipline by shortening contract terms and tightening approved-vendor lists, which puts smaller distributors at risk if they cannot match pricing or service-level metrics in head-to-head bids. Differentiation through certifications, fabric innovation, and durability promises gives premium brands a footing in the upper tiers, but trading down during promotional cycles still moves share to private labels. The result is a market where value propositions must be clear, tested, and repeatable to sustain long-term positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Accelerated carpet demand complements bed-linen stability

Bed linen held 33% of revenue in 2025, reflecting its significant role in both residential and institutional procurement, while carpets and rugs are projected to lead product growth at a 3.72% CAGR through 2031 within the GCC home textile market size. The profile of bed linen purchases in hospitality is stabilizing at higher specifications, including T-300 percale and antimicrobial finishes for hygiene-focused environments, which lifts unit values even as replacement cycles extend in premium tiers. Hotels and serviced apartments also continue to anchor large tender volumes, where six-set par stock norms per room translate into bulk orders that repeat on 18 to 24 month cycles, supporting steady baseline demand in the GCC home textile market. Residential bed linen shoppers add seasonality around Eid and year-end periods, which benefits retailers and marketplaces that synchronize assortments and promotions with local holidays. Bath linen remains a durable mid-tier category in institutional settings, where frequent laundering and durability expectations guide specifications like GSM and pile structure, which helps suppliers segment the offer by price and performance. In the value segment, private-label bath and kitchen textiles sourced from large South Asian mills reinforce price leadership, while premium assortments play in higher thread counts, long-staple cottons, and design-led weaves.

Carpets and rugs benefit from interior fit-out cycles in villas and apartments as handovers surge, as well as periodic refreshes in hospitality lobbies and corridors aligned with renovation schedules in the GCC home textile market. Residential buyers often allocate a defined budget to area rugs when furnishing new-build properties, which supports steady unit movement even in soft retail months. Hospitality properties seek stain resistance and color fastness validated by lab reports, which advantages mills with in-house testing and reliable batch consistency. Kitchen linen and upholstery textiles are niche subcategories where house labels win share based on unit price and basic quality controls, while specialty stores differentiate with tactile experience and customization. Suppliers that sustain end-to-end traceability and maintain compliance-ready documentation meet the rising bar for institutional bids that now embed ESG and safety screens. Across product categories, certified inputs and reliable finishes have become table stakes for winning the most valuable business in the GCC home textile market.

By Material: Organic and alternative fibers disrupt cotton’s incumbent share.

Cotton retained a 68.42% share in 2025, supported by long-standing supply chains and material familiarity, yet alternative fibers are set to grow faster at a 5.64% CAGR (2026-2031), reflecting premiumization and eco-led choices within the GCC home textile market size. Sustainable sourcing and traceability are increasingly non-negotiable, with leading manufacturers reporting high shares of sustainably sourced cotton and building toward full targets by 2030, supported by blockchain-enabled fiber-to-shelf tracking. Linen blends attract luxury residential buyers seeking breathability in air-conditioned climates, while wool and silk remain limited to decorative uses and luxury suites where tactile feel and visual finish command premiums. Bamboo and other cellulosic fibers appeal to eco-conscious consumers willing to pay for certified towels and sheets, which gives retailers a storytelling angle and a margin buffer in curated ranges. In utility bedding, synthetic fills dominate pillows and quilts due to hypoallergenic properties and cost-of-care advantages, which align with large bed-in-a-bag programs run by global brands expanding their capacity through acquisitions in adjacent categories. Regulatory and testing initiatives, including increased focus on microplastic shedding standards aligned with ISO frameworks, are pushing suppliers to segregate material streams and maintain stronger labeling controls for GCC-bound shipments.

Cotton price volatility and freight variability continue to shape material choices and product structure for the GCC home textile market. Buyers hedge risk by maintaining mixed portfolios that include organic cotton, recycled polyester, and bamboo in select lines, which allows a quick response to input cost shifts without disrupting brand standards. Institutional buyers emphasize durability and wash performance over composition per se, which sustains demand for blended fabrics that survive high-temperature cycles while retaining feel. Retailers use material stories to differentiate tiered ranges, pairing certifications with visual merchandising to move consumers up the price ladder. Suppliers that can guarantee both compliance and consistent fabric hand in cotton-rich lines defend core volume while testing eco-forward options in new collections. This balance enables the GCC home textile industry to adapt to both price swings and rising sustainability expectations.

By End-User: Commercial segment captures giga-project tailwinds.

The residential segment held 70.61% of revenue in 2025, yet commercial buyers are projected to grow faster at 4.53% CAGR (2026-2031) as hotel, healthcare, and government programs aggregate volumes into large framework agreements in the GCC home textile market. Chains and owner-operators prioritize suppliers that can certify FR and antimicrobial performance where required, and that maintain multiple par stocks across portfolios to accommodate high occupancy and fast turnarounds. International operators are scaling their Middle East presence, reinforcing predictable institutional demand for premium linens matched to brand standards across properties and branded residences. The procurement model often centralizes at regional hubs, which concentrate orders across multiple hotels and residences into fewer bids with higher quality gates. Healthcare facility expansions and seasonal capacity surges also necessitate medical-grade bedding designed to withstand frequent laundering at high temperatures, which pushes buyers toward specialized specifications and documented test performance. As a result, certified suppliers with scale and documentation capabilities expand their share across non-residential channels in the GCC home textile market.

Residential demand remains a stable bedrock driven by new home handovers and periodic refresh cycles for bedding, towels, and curtains. Housing program momentum from 2024 supported an influx of first-time buyers entering furnishing cycles, which drives concentrated purchase windows soon after key collection. Retailers and marketplaces respond by aligning assortment timing with handover clusters and holiday seasons, which keeps shelves balanced between value private labels and premium branded lines. Specialty stores differentiate through tactile service, customization, and curated international collections, while omnichannel retailers stress convenience and delivery reliability. A rising share of consumers research materials, thread counts, and certifications online before purchase, which rewards brands that publish detailed product content. In this context, the GCC home textile industry blends institutional growth with steady household cycles to keep overall demand resilient.

By Distribution Channel: Digital penetration reshapes retail footprints

Offline channels accounted for 66.74% of sales in 2025, reflecting the continued strength of hypermarkets, home centers, and specialty stores, while online channels are projected to grow at 6.51% CAGR (2026-2031) with direct-to-consumer and marketplace models scaling across the GCC home textile market. Hypermarkets and home centers leverage private labels that are sourced directly from mills to sustain value leadership, which keeps pressure on branded price points in mid-tier ranges. Specialty stores continue to convert higher-income shoppers by offering expert guidance, sensory experience, and made-to-order options like monogrammed towels and custom-length curtains. In parallel, brands that invest in D2C infrastructure can sidestep wholesale markups and use localized content to educate shoppers on fabric performance and certifications, an approach documented by leading exporters that scaled licensed brands and utility bedding portfolios in recent years. The best omnichannel players align inventory and promotion calendars across physical and digital storefronts to capture handover-driven and holiday-driven spikes. As compliance requirements rise, both offline and online channels increasingly feature certification badges and testing claims at the point of sale, which aids shopper confidence and reduces returns in the GCC home textile market.

E-commerce also supports niche categories and premium lines that can educate and convert through rich media and verified reviews. Marketplaces amplify reach but compress margins, so brands balance marketplace exposure with owned-channel depth that better reflects the full assortment and tells sustainability stories. Logistics partners tied into regional hubs help meet fast-ship expectations for curated sets and replenishment items, especially in urban centers. Offline remains indispensable for institutional buyers and project-based sales, where physical sample validation is standard, which preserves showroom and B2B wholesale relevance. Payment and invoice terms also differ by channel, with institutional buyers favoring longer payment horizons that digital platforms do not always match, which influences working capital planning for suppliers. The GCC home textile market thus converges toward a hybrid model where offline strength and online acceleration operate side by side.

Geography Analysis

Saudi Arabia’s scale anchors 2025 value, while the UAE leads on growth through 2031, resulting in a two-speed pattern between a volume-driven market and a premium-intensive one within the GCC home textile market. Saudi housing programs and mortgage expansion lifted homeownership and produced a high number of new handovers in 2024, which delivered concentrated waves of household purchases for bedding, towels, curtains, and carpets. Residential buyers typically complete textile purchases within weeks of key collection, which creates quarterly spikes rather than a uniform monthly pattern across the year. Institutional procurement in Saudi Arabia benefits from international operators adding new properties and branded residences, which multiplies the need for FR-compliant curtains and premium linens at consistent brand standards. SABER-based enforcement in Saudi Arabia remains strict on labeling and conformance, which narrows panels to vendors that can issue shipment-level certificates promptly and handle testing updates connected to emerging standards. Local wet-processing is challenged by water and treatment costs, so import streams focus on pre-finished products with embedded sustainability and safety assurances.

The UAE’s fastest growth through the forecast period 2026-2031 reflects a persistent tilt toward luxury travel, branded residences, and premium retail, which drives a higher specification mix for textiles. Global chains are scaling in the Emirates, which supports multi-year linen programs tied to new hotel and residence openings and conversions. Dubai’s position as a logistics and re-export hub allows suppliers to hold bonded inventory close to end markets, reducing stockout risk during holiday seasons and major events. Online channel growth in the UAE amplifies assortment breadth and enables D2C penetration by global brands that ship quickly into the region, while specialty stores preserve share among higher-income shoppers. Retailers and institutional buyers enforce visible certification and testing credentials at the point of sale and within tenders, which has raised the bar for smaller importers without in-house testing or established lab partners. These dynamics produce a resilient premium segment in the GCC home textile market centered on the Emirates.

Qatar, Kuwait, Bahrain, and Oman together contribute steady, if smaller, shares with distinct demand drivers. Qatar’s post-tournament hospitality and mixed-use landscape continues to draw premium textile requirements as international operators align brand standards across properties. Kuwait and Bahrain’s higher incomes drive premium bedding and towel purchases in retail, aided by a growing comfort with online ordering and quick delivery. Oman grows with boutique hospitality developments and family tourism, where value and durability matter in product selection. In all four markets, cross-border re-export flows and compliant shipment documentation support reliable delivery schedules for both retailers and institutional buyers. Suppliers that combine certified inputs, documented batch performance, and regional warehousing remain best positioned to capture share. These geographic patterns extend the growth runway across the GCC home textile market through 2031.

Competitive Landscape

The GCC home textile market remains moderately fragmented, with leading global exporters and regional specialists competing across retail and institutional channels. Vertically integrated manufacturers that combine yarn, weaving, finishing, and cut-and-sew operations, along with in-house testing labs, enjoy an advantage in compliance, speed, and cost-to-serve. Sustainability commitments and traceability platforms differentiate upper-tier players that are winning longer framework agreements, particularly in hospitality and healthcare. For example, one large global manufacturer reports a high share of sustainably sourced cotton and a roadmap to achieve full sustainable sourcing by 2030, facilitated by a blockchain-enabled tracking system that verifies farm-to-shelf provenance and supports premium positioning with international buyers. Another global exporter broadened its portfolio through acquisitions in utility bedding and scaled licensed brands, which diversified revenue beyond core bed linen and positioned the company to capture pillow, quilt, and protector demand in global channels that also reach GCC buyers. Together, these strategic moves support greater resilience through category breadth, compliance readiness, and improved speed-to-market.

Institutional clients in the Gulf are concentrating supplier panels on vendors that can deliver to multiple countries and maintain quality consistency across large, multi-property portfolios. Hospitality operators increasingly specify antimicrobial and FR performance with batch-level test reports, which entrenches the position of manufacturers with accredited labs and fast certification issuance. Healthcare buyers prioritize medical-grade bedding that withstands high-temperature laundering while preserving comfort and durability, which raises the importance of specialized finishing and documented efficacy in treated fabrics. On the retail side, private labels sourced through direct mill relationships compress margins for branded lines at entry and mid-tier price points, while D2C channels provide an offset for brands that can own customer relationships and storytelling. Across channels, certification visibility and verifiable sustainability claims are now critical to shelf placement and tender eligibility in the GCC home textile market.

Local processing constraints for dyeing and finishing favor exporters with advanced water-recycling systems and renewable energy integration at source, which strengthens their competitiveness when tendering to GCC buyers. Documented impacts of logistics disruptions and water-related costs at large mills have reinforced the logic of concentrating finishing in source countries, then staging compliant finished goods at regional hubs for quick delivery. Suppliers that add RFID and other tracking capabilities to their institutional programs provide hotel operators with improved inventory control and loss prevention, which reduces the total cost of ownership. These capabilities, combined with robust compliance and sustainability practices, define the competitive edge at the top of the vendor pool. As a result, differentiation in the GCC home textile market now rests on price, speed, documentation, and ESG leadership, with top-tier players widening their lead over smaller importers lacking multi-country logistics and lab-backed quality assurance.

GCC Home Textile Industry Leaders

WestPoint Home

Trident Limited

Zorlu Tekstil

Al Abdullatif Industrial Investment Co.

Standard Carpets Ind. LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Marriott International reported robust growth across EMEA, identifying Saudi Arabia and the United Arab Emirates as top markets for signings in 2025. In 2025, the company achieved over 230 organic signings, equating to more than 31,000 rooms, and added 170 properties with 24,000 rooms, resulting in 7.8% net room growth. The pipeline now includes over 600 properties, totaling 113,000 rooms.

- January 2026: Marriott International and Al Qimmah Hospitality signed agreements for five new Marriott-branded hotels in Saudi Arabia. These projects, located in Jeddah, Makkah, and Madinah, will add over 2,700 rooms. Key projects include JW Marriott Jeddah The Apartments with 356 units, Four Points by Sheraton Shesha Makkah with 1,030 rooms, and Element Madinah Sultana Road featuring 136 studios and apartments. This development marks Marriott reaching 100 hotels, both operational and in the pipeline, across Saudi Arabia.

GCC Home Textile Market Report Scope

Home textile is a subfield of technical textiles, which includes the use of textiles for domestic purposes. Home textile is nothing but an interior environment, which refers to the interior spaces and their furniture. Home textile is mainly used for their functional and aesthetic properties, which give us mood and mental relaxation.

The GCC home textile market is segmented by application, material, end-user, distribution channel, and geography. By application, the market is segmented into bed linen, bath linen, kitchen linen, upholstery, and others (carpets & area rugs). By material, the market is segmented into cotton, linen, synthetic fibres, and other materials (wool, hemp, silk, jute, bamboo). By end-user, the market is segmented into residential and commercial sectors. By distribution channel, the market is segmented into offline and online channels. The offline segment is further divided into mass merchandisers (hypermarkets/supermarkets), home centers, specialty stores, and other offline channels. By geography, the market is segmented into Saudi Arabia, the UAE, Qatar, Kuwait, Oman, and Bahrain. The report offers market size in value terms in USD for all the above-mentioned segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets & Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline |

| Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers |

| Specialty Stores |

| Other Offline Channels |

| Online |

By Region

| Saudi Arabia |

| UAE |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Application | Bed Linen |

| Bath Linen | |

| Kitchen Linen | |

| Upholstery | |

| Others (Carpets & Area Rugs) | |

| By Material | Cotton |

| Linen | |

| Synthetic Fibres | |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | |

| By End-User | Residential |

| Commercial | |

| By Distribution Channel | Offline |

| Mass Merchandisers (Hypermarkets/Supermarkets) | |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online | |

| By Region | Saudi Arabia |

| UAE | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the growth outlook for the GCC home textile market through 2031?

The GCC home textile market is projected to reach USD 2.06 billion by 2031, growing at a 2.81% CAGR over 2026-2031, with institutional demand and premiumization supporting the trajectory.

Which product categories are set to grow the fastest in the GCC home textile market?

Carpets and rugs are projected to post the fastest growth at a 3.72% CAGR through 2031, while bed linen remains the largest product category by value due to institutional procurement cycles.

How are regulations shaping supplier selection in the GCC home textile market?

SABER and GSO-aligned requirements for labeling, safety, and shipment-level certification are tightening, which concentrates share among certified, vertically integrated suppliers with in-house testing and traceability.

Which end-user segment is expected to lead growth in the GCC home textile market?

Commercial end-users, including hotels and healthcare facilities, are expected to grow faster than residential at a 4.53% CAGR, driven by chain expansions and standardization of premium specifications.

What is driving premiumization in the GCC home textile market?

Luxury hospitality’s requirements for higher thread counts, FR compliance, and antimicrobial finishes are lifting average selling prices and expanding demand for certified, high-performance textiles.

How is online retail changing the GCC home textile market?

Online channels are growing at a 6.51% CAGR (2026-2031) as D2C brands and marketplaces expand reach, while omnichannel retailers integrate private labels and premium lines with faster shipping through regional hubs.

Page last updated on: