Qatar Fruit And Vegetable Market Analysis by Mordor Intelligence

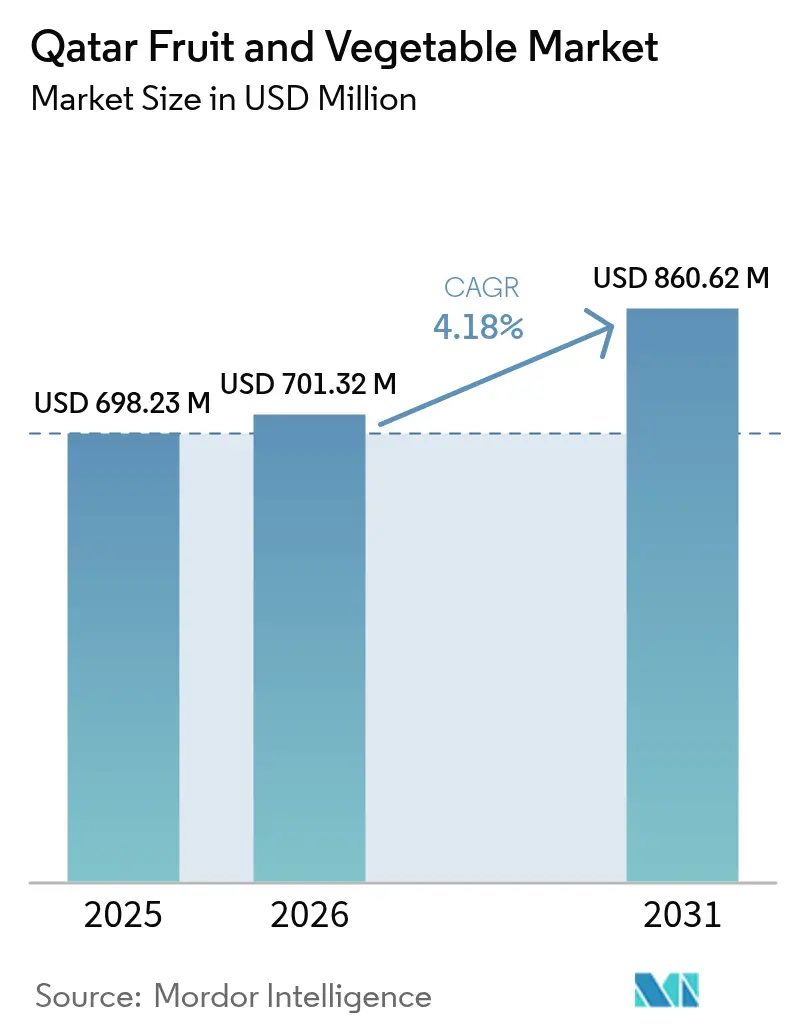

The Qatar fruit and vegetable market size is projected to expand from USD 698.23 million in 2025 and USD 701.32 million in 2026 to USD 860.62 million by 2031, registering a 4.18% CAGR over 2026-2031. Intensive investment in controlled-environment agriculture and diplomatic blockade has shifted production toward cooled and non-cooled greenhouses, reducing import exposure during the hot season. Government procurement through Mahaseel, energy price reforms that reward efficiency, and rapid technology adoption by firms such as Agrico and Pure Harvest Smart Farms are reshaping cost structures and competitive behavior. Demand is buoyed by rising health awareness among expatriates and locals, who are responding to the Ministry of Public Health's dietary campaigns to increase fresh produce intake by 20% by 2030. Meanwhile, groundwater depletion and volatile electricity tariffs remain structural headwinds that encourage investments in hydroponics, solar cooling, and water-reuse systems.

Key Report Takeaways

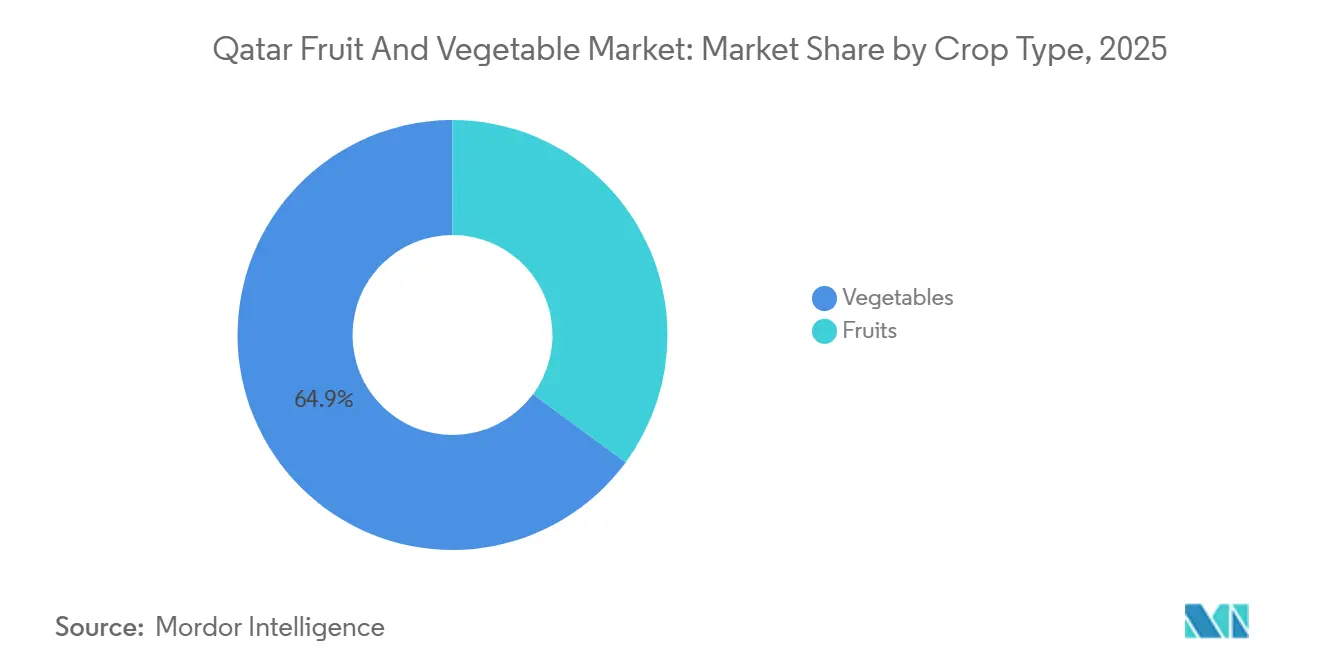

- By crop type, vegetables led with a 64.9% of the Qatar fruit and vegetable market share in 2025, while fruits are set to post the fastest 5.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Fruit And Vegetable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding protected cultivation acreage | +0.9% | Al Shahaniya, Umm Salal, and Al Khor | Medium term (2-4 years) |

| Government food-security funds for desert agriculture | +0.6% | National, 441 farms funded in 2024 to 2025 | Short term (≤ 2 years) |

| Agri-voltaic projects monetizing dual land use | +0.3% | Pilot sites in Al Khor and Qatar University | Long term (≥ 4 years) |

| Increasing per-capita fruit and vegetable intake targets | +0.5% | National dietary programs | Medium term (2-4 years) |

| Surplus desalination brine valorized for fertigation | +0.3% | Experimental coastal farms | Long term (≥ 4 years) |

| Proven yield gains from hydroponics and vertical farms | +0.7% | Agrico, Pure Harvest, and Qatar University | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Protected Cultivation Acreage

Protected cultivation in Qatar is expanding rapidly to improve food security, with a focus on greenhouses and net houses to address the challenges posed by harsh climatic conditions. The Ministry of Municipality distributed 3,476 greenhouse structures covering 666 hectares by 2024, targeting 110 hectares of high-tech facilities[1]Source: Ministry of Municipality Qatar, “Agricultural Development and Food Security Initiatives,” mm.gov.qa. The growth clusters around service centers in Al Shahaniya, Umm Salal, and Al Khor now support 150 farms, providing inputs and technical support. Protected facilities safeguard heat-sensitive crops such as lettuce and cucumbers when summer temperatures rise above 45 degrees Celsius, resulting in a 98% increase in total vegetable output over five years. The Ministry of Municipality (MoM) has launched a 2024 project to develop 'protected farms' and implement climate-smart agriculture. This initiative aims to transform open farm areas into closed farms, reducing evaporation, minimizing water loss, and addressing soil-related challenges. Export-oriented farms such as Al Sulaiteen are pairing new acreage with GLOBALG.A.P. compliance to unlock European demand.

Government Food-Security Funds for Desert Agriculture

A flexible voucher program launched in September 2025 lets growers buy seeds, fertilizers, and drip lines from approved dealers instead of accepting mismatched in-kind inputs, improving yield response for tomatoes, cucumbers, eggplants, zucchini, and sweet peppers, which together account for more than 70% of domestic vegetable sales. Mahaseel’s Daman pre-contracting scheme fixes purchase prices before planting, de-risking field decisions for 199 participating farms. Vegetable yards in Sheehaniya, Al Mazrouah, Al Wakrah, Al Khor-Al Thakhira, and Al Shamal offer produce roughly 30% below hypermarket prices, stabilizing household budgets. Complementary tariffs and anti-dumping rules introduced in 2024 further insulate growers from low-cost seasonal imports, anchoring the domestic floor price.

Agri-Voltaic Projects Monetizing Dual Land Use

Solar panels mounted above crop rows are being trialed at Qatar University and commercial farms to offset electricity costs that have ballooned 100-fold following the tariff reform. Research published in 2024 confirmed that lettuce yields under semi-transparent photovoltaic panels match open-field yields while slashing net energy demand by 40%. Although commercial-scale systems remain few, Agrico has signaled its intent to pursue solar integration across 250,000 square meters of greenhouses, and forthcoming Ministry rules are projected to streamline grid connection. Over the long term, crops such as strawberries and leafy greens, which require continuous cooling, stand to gain the most from on-farm electricity generation that mitigates tariff volatility.

Increasing Per-Capita Fruit and Vegetable Intake Targets

Qatar is making significant progress toward enhancing its national food security, aiming to achieve 55% vegetable self-sufficiency by 2030 under the National Food Security Strategy 2024-2030. This strategy emphasizes a 50% increase in local production, promoting consumption through health awareness campaigns, and building on the 39% vegetable self-sufficiency achieved by 2023. Current interventions include school meals, public campaigns, and clearer labeling at retailers such as Lulu Hypermarket and Carrefour that now highlight farm origin and carbon footprint. Rising wellness consciousness among the expatriate majority is fueling demand for pesticide-free and organic produce, prompting Agrico and Paramount Agricole to pursue organic certification. The ministry aims to increase fresh intake by 2030, thereby expanding the addressable demand for fruits and vegetables and supporting capacity additions in hydroponics and vertical farms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking groundwater reserves in arid regions | −0.6% | Southern and western agricultural zones | Long term (≥ 4 years) |

| Volatile energy prices inflating controlled-environment costs | −0.5% | All greenhouse and vertical farm operators | Short term (≤ 2 years) |

| High salinity drift clogging drip lines | −0.3% | Farms reliant on untreated wells | Medium term (2-4 years) |

| Bio-security risks from expanding seed-import channels | −0.2% | Air and sea entry points | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shrinking Groundwater Reserves in Arid Regions

Qatar experiences severe water stress due to heavily depleted, non-renewable, and brackish groundwater reserves, worsened by over-extraction for agricultural purposes and minimal rainfall. The water table is declining at approximately 1 meter per year, and extraction levels exceed the safe yield by up to 5 times. This has led to significant degradation of the country's limited, predominantly karstic aquifers, including seawater intrusion. The Ministry targets a 70% extraction cut by 2030, hinging on treated sewage effluent, which accounted for only 31% of irrigation in 2019. Scaling reuse to 72% could satisfy more than 90% of crop water demand, but pipeline coverage and on-farm storage lag investment needs. Farms outside effluent networks pay for reverse-osmosis desalination, raising break-even prices and discouraging acreage expansion.

Bio-Security Risks from Expanding Seed-Import Channels

The shift away from neighboring suppliers has led to an increase in seed consignments through Hamad International Airport and Hamad Port. This change reflects efforts to diversify supply chains and reduce dependency on regional sources. Phytosanitary protocols are being strengthened, and customs officers intercepted forty-seven contaminated seed lots in 2024, highlighting ongoing challenges in ensuring seed quality. The Ministry is preparing stricter pre-shipment testing regulations, which may increase lead times and working capital requirements for growers relying on imported genetics for high-value greenhouse crops. These measures aim to enhance biosecurity and safeguard agricultural productivity. However, implementing these stricter protocols may also require additional investments in testing infrastructure and training for customs officials to ensure effective enforcement and minimize disruptions to the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Vegetables Dominate Value While Fruits Lead Growth

Vegetables accounted for 64.9% of the Qatar fruit and vegetable market share in 2025, as Mahaseel pre-contracts reinforce planting confidence and cooled greenhouses extend the production calendar[2]Source: The Peninsula Qatar, “Mahaseel Marketing and Local Vegetable Production,” thepeninsulaqatar.com. According to the Food and Agriculture Organization, tomatoes alone reached 27,321.7 metric tons in 2024, and cucumbers and gharkins followed at 14,410.1 metric tons, both sourced mainly from Al Shahaniya and Umm Salal. Hydroponic leafy green suppliers such as Agrico are compressing cycles to 30 days, capturing premium shelf space in 44 hypermarkets where Mahaseel merchandises local produce within 24 hours of harvest. Potatoes and onions remain largely imported because their long seasons and high field requirements collide with summer heat and scarce water.

Fruits are advancing at a 5.0% CAGR, the fastest among segments, as retailers expand assortments beyond citrus to grapes, berries, and melons that arrive by air from Egypt, Turkey, South Africa, and the United States. Date palm output reached 35,317.6 metric tons in 2024, and the ministry distributed 880 metric tons of offshoots to expand groves. Pilot citrus blocks under shade nets are being tested for local adaptation, while Eden Farm’s mushroom unit targets hotel and airline buyers seeking novelty items. Easier-peel mandarins see demand spikes of up to 40% during Ramadan, illustrating how cultural events shape import scheduling.

Geography Analysis

Qatar's fruit and vegetable market is transitioning from significant import dependence to localized, technology-driven production, with vegetables dominating the market. This shift is propelled by food security objectives, leading to the expansion of hydroponic and greenhouse farming in northern regions, particularly for crops such as tomatoes, cucumbers, and leafy greens. Doha and its suburbs host 99.4% of the population in 2024, enabling same-day delivery from farms in Al Shahaniya, Umm Salal, and Al Khor to retail hubs, which cuts spoilage to below 10% in 2024 compared with 25% in 2010. Five government-operated yards serve as nodal points, feeding forty-four Mahaseel outlets, and integrate collection, grading, and auction activities to shorten the farm-to-shelf interval.

European Union fruit and nut exports to Qatar fell by 19% in 2023 as the country pivoted toward Egypt, Turkey, and South Africa, lowering freight costs and currency risk[3]Source: European Commission, “European Union Agricultural Exports to Qatar,” agriculture.ec.europa.eu. In contrast, shipments from the United States increased by 201% over the decade leading to 2024, driven by the premium positioning of apples and grapes targeting high-income expatriates. The strong demand for high-quality produce among Qatar's affluent expatriate population has bolstered the United States' market share, highlighting the appeal of premium products in this segment.

Qatar’s desert agriculture experiments attract attention from the Gulf Cooperation Council and North African nations facing similar climates. Pure Harvest’s USD 180.5 million raise in 2022 and Agrico for Agricultural Development W.L.L.’s hydroponic demonstration center with Yara International ASA provide templates for technology roll-out elsewhere. The Ministry’s partnership framework, embedded in the 2024 to 2030 plan, encourages foreign joint ventures that bring know-how in solar cooling and nutrient recycling, accelerating regional diffusion.

Competitive Landscape

The market remains moderately fragmented, with more than 950 productive farms alongside vertically integrated players that control greenhouses, logistics, and shelf space. Mahaseel purchased 24,000 metric tons of vegetables worth QAR 68 million (USD 18.7 million) in 2024 and stocked forty-four hypermarket corners, establishing a price floor that narrows private importer margins. Lulu Hypermarket and Carrefour compete on breadth and convenience, while Mahaseel drives volume.

Technology is the key differentiator. Agrico for Agricultural Development W.L.L. operates 250,000 square meters of greenhouses, supplying 1,400 customers, and opened an indoor farm hub on Green Island in May 2025 to showcase vertical farming to students. Baladna Food Industries Q.P.S.C. leveraged its dairy distribution network to launch twenty-five fruit beverage stock-keeping units in the first half of 2025 and partnered with Veolia to recycle 22,000 liters of water daily, halving freshwater use. Al Sulaiteen Agricultural and Industrial Complex Q.S.C. holds GLOBALG.A.P. certification and started selective vegetable exports to Europe.

Emerging disruptors include Paramount Agricole, which secured organic mushroom certification and sells high-margin oyster and shiitake lines, and Global Farm for Agricultural Supplies, which builds turnkey greenhouses while producing cucumbers and peppers. Local input suppliers such as Al Noor Plastic Factory and Mitras Trading Company now provide greenhouse films and custom fertilizers, deepening value-chain localization.

Recent Industry Developments

- February 2026: LuLu Hypermarket Qatar organized the "Taste of Sri Lanka" festival to celebrate Sri Lanka's 78th Independence Day. Customers could purchase authentic Sri Lankan groceries, fresh fruits such as bananas, and vegetables at discounted prices. These products were sourced directly through LuLu Group's export distribution center in Colombo, ensuring both freshness and quality.

- November 2025: The Ministry of Municipality has launched the second Aswaq Winter Festival in collaboration with Hassad Food Company. The event showcases a variety of local products, including dates, seasonal organic fruits and vegetables, and traditional Qatari foods. It also features stalls for family-run businesses and a dedicated section supporting families of Gaza residents receiving treatment in Qatar, highlighting the festival's social focus.

- May 2025: Qatar-based startup VFarms has successfully grown iceberg lettuce heads weighing over 600 grams, nearly four times the standard weight achieved globally in vertical farms. This accomplishment was achieved despite challenging growing conditions, including external temperatures exceeding 50°C and extreme humidity.

Qatar Fruit And Vegetable Market Report Scope

Fruits and vegetables are high in vitamins, minerals, and phytochemicals. The Qatar Fruit and Vegetable Market Report is Segmented by Crop Type (Fruits and Vegetables). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, and More. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Crop Type

| Vegetables | Potatoes | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Onions | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Tomatoes | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Carrots | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Cabbage and Brassicas | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Pumpkins and Squash | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Chillies and Peppers | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Fruits | Citrus (Oranges, Lemons and Limes) | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Apples and Pears | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Grapes | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Peaches and Nectarines | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Watermelons | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Cantaloupes and Other Melons | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Tangerines, Mandarins, and Clementines | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| By Crop Type | Vegetables | Potatoes | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |||

| Key Supplying Markets | |||||

| Export Market Analysis | Export Value and Volume | ||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Onions | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Tomatoes | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Carrots | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Cabbage and Brassicas | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Pumpkins and Squash | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Chillies and Peppers | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Fruits | Citrus (Oranges, Lemons and Limes) | Production Analysis | Production Volume | ||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Apples and Pears | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Grapes | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Peaches and Nectarines | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Watermelons | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Cantaloupes and Other Melons | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Tangerines, Mandarins, and Clementines | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

Key Questions Answered in the Report

How large will Qatar fruit and vegetable demand be by 2031?

The Qatar fruit and vegetable market size is forecast to reach USD 860.62 million by 2031, expanding at a 4.18% compound annual rate from 2026.

Which product category currently dominates grocery sales?

Vegetables lead, holding 64.9% of Qatar fruit and vegetable market share in 2025, with tomatoes and cucumbers forming the bulk of volumes.

What segment is expanding the quickest?

Fruits post the fastest growth, advancing at a 5.0% CAGR as import diversification and pilot orchards boost availability.

Why are hydroponic systems gaining popularity among Qatari growers?

Hydroponics cut water usage by up to ninety percent, mitigate saline groundwater risks, and deliver consistent yields inside climate-controlled facilities.

How is the government supporting growers against import competition?

Mahaseel pre-contracts, tariff protections during peak harvest, and QAR 1.1 billion (USD 302 million) earmarked for greenhouses under the 2024-2030 plan provide price certainty and capital access.

What drives retailer interest in local produce?

Same-day delivery from nearby farms reduces spoilage and carbon footprint, while consumer demand for traceable and pesticide-free food commands premium shelf placement.

Page last updated on: