Market Overview

| Study Period | 2020 - 2031 |

|---|---|

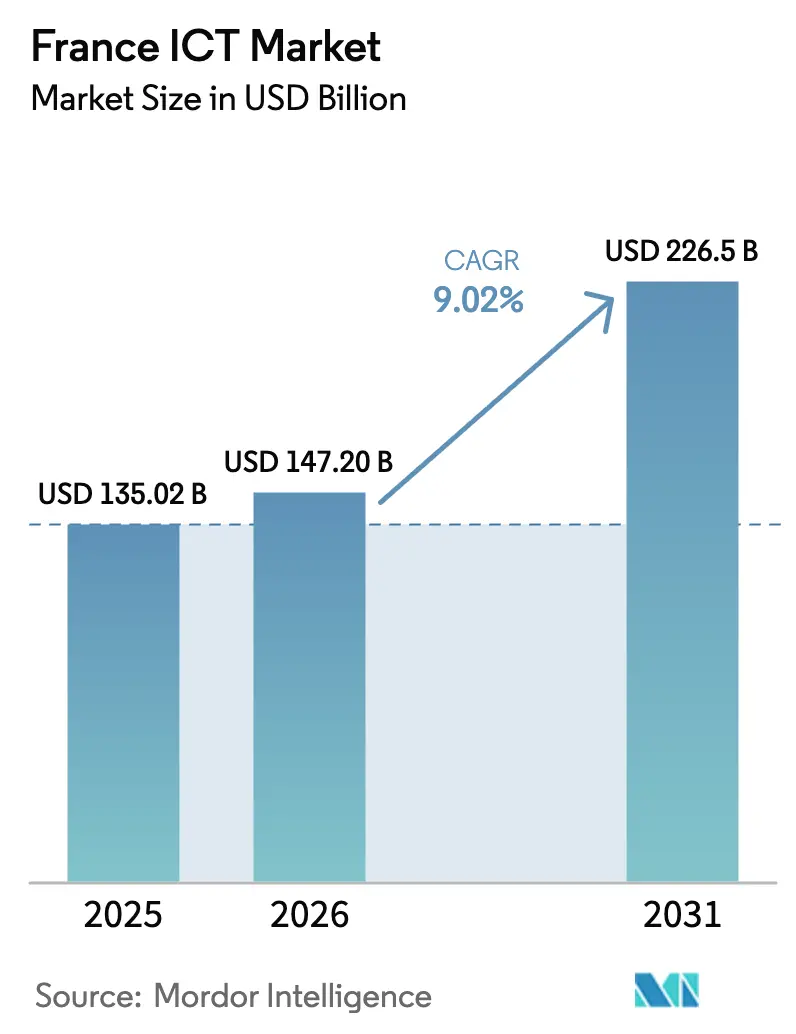

| Base Year Market Size (2025) | USD 135.02 Billion |

| Market Size (2026) | USD 147.2 Billion |

| Market Size (2031) | USD 226.5 Billion |

| Growth Rate (2026 - 2031) | 9.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France ICT Market Analysis by Mordor Intelligence

The France ICT market size was valued at USD 135.02 billion in 2025 and estimated to grow from USD 147.2 billion in 2026 to reach USD 226.5 billion by 2031, at a CAGR of 9.02% during the forecast period (2026-2031). Robust upside stems from the government’s EUR 54 billion France 2030 program, complementary private AI investments topping EUR 109 billion, and pervasive 5G and fiber coverage that now blankets 95% of the population. These factors converge with strict sovereign-cloud mandates to anchor the France ICT market in Europe’s digital-sovereignty agenda. Fiber-to-the-home (FTTH) penetration of 90% eligibility and 75.4% subscription has moved competition away from basic connectivity toward data-intensive services, while a nationwide 5G standalone footprint enables industrial IoT, network slicing, and edge-computing use cases. Rising power-efficient data-center builds, supported by France’s low-carbon nuclear grid, are further lowering the total cost of compute and meeting corporate decarbonization targets. Together, these structural shifts accelerate cloud migration, AI adoption, and green-IT demand, setting the stage for sustained double-digit expansion across the France ICT market.

Key Report Takeaways

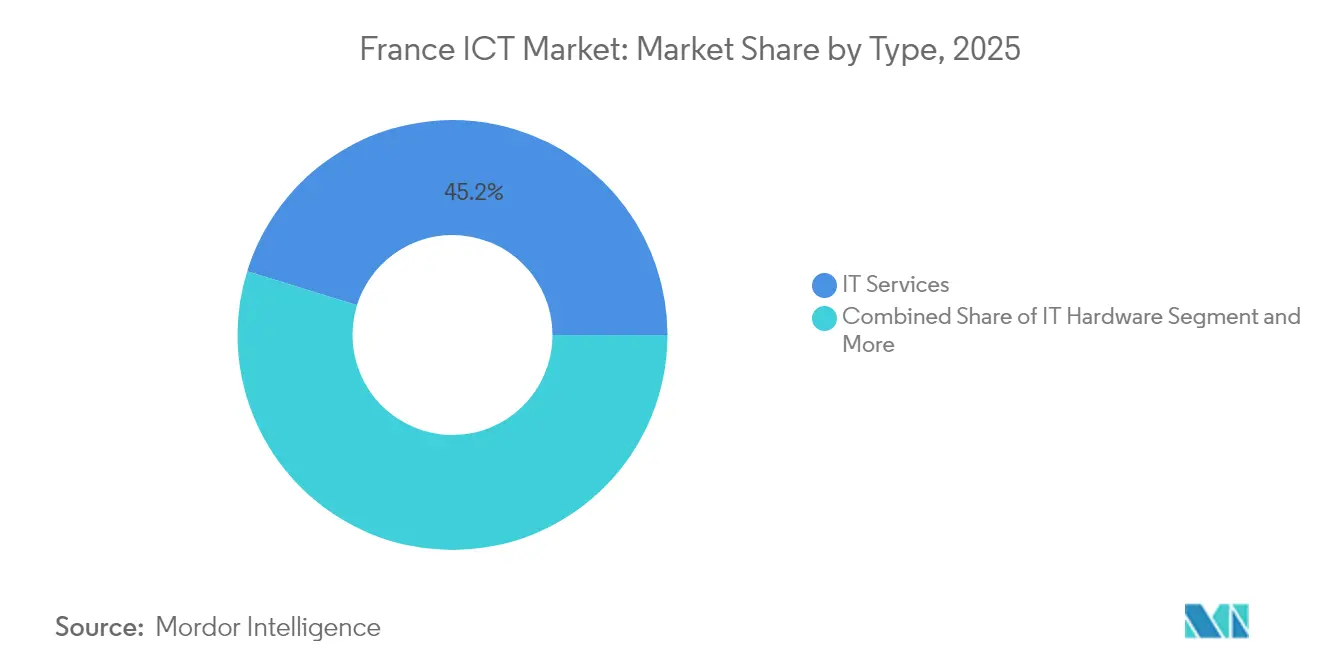

- By type, IT Services led with 45.20% of the France ICT market share in 2025, while Cloud Services is advancing at a 12.10% CAGR through 2031.

- By enterprise size, large enterprises controlled 70.30% of the France ICT market size in 2025; small and medium enterprises (SMEs) posted the fastest 9.55% CAGR to 2031.

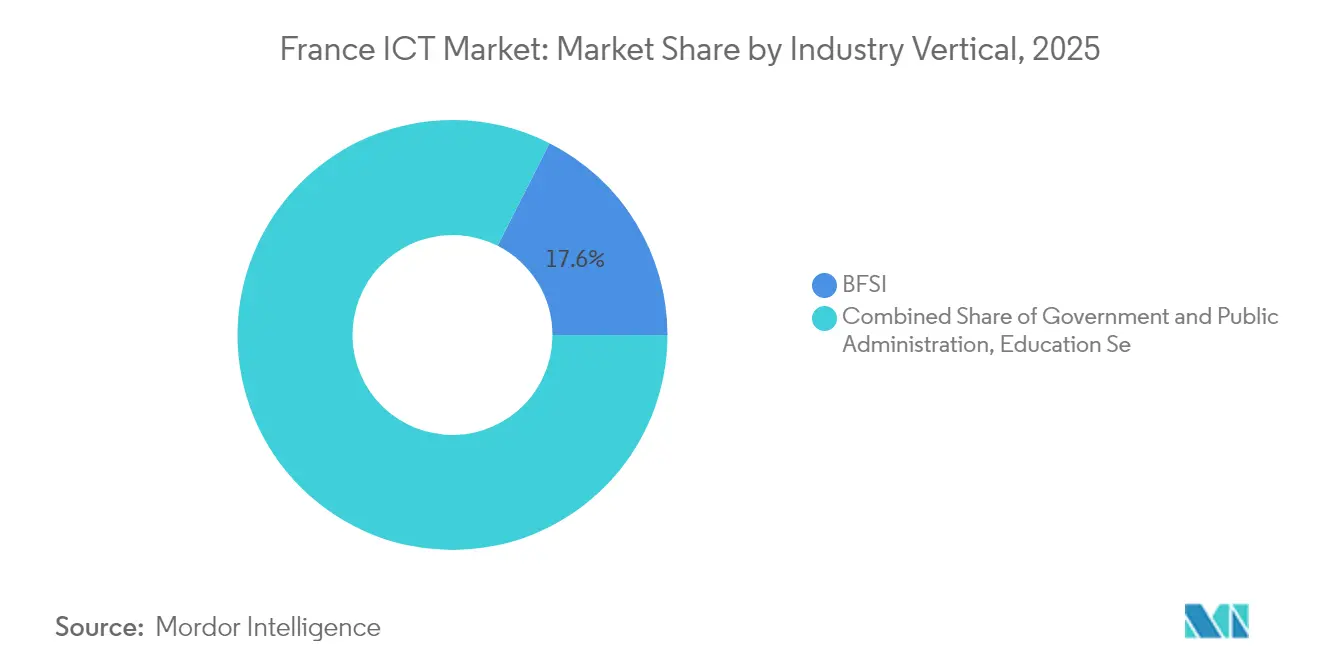

- By industry vertical, BFSI contributed 17.55% of the France ICT market size in 2025, whereas Gaming and Esports is expanding at a 14.35% CAGR through 2031.

- By deployment model, cloud-only solutions captured 56.85% of the France ICT market share in 2025, with the public-cloud segment forecast to climb at an 17.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G spectrum auctions and network build-outs | +1.8% | National, with urban concentration in Paris, Lyon, Marseille | Medium term (2-4 years) |

| France's "Cloud de Confiance" certification drives sovereign-cloud uptake | +1.5% | National, with public sector priority | Long term (≥ 4 years) |

| EU Chips Act incentives accelerate local semiconductor design hubs | +0.9% | Regional clusters in Grenoble, Toulouse, Paris | Long term (≥ 4 years) |

| Corporate decarbonisation targets boost demand for green data-centres | +1.2% | National, with concentration in renewable energy regions | Medium term (2-4 years) |

| Nationwide fibre-to-the-home (FTTH) completion unlocking higher-value services | +2.1% | National, with rural area emphasis | Short term (≤ 2 years) |

| Rise of AI-powered language models tailored for French public sector | +1.3% | National, with government sector focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in 5G Spectrum Auctions and Network Build-Outs Drive Enterprise Transformation

Free Mobile’s national 5G-SA launch over 20,000 sites in 2024 triggered a wave of competitive deployments, lifting authorized 5G sites to 50,268 by March 2025 and extending coverage to 95% of residents[1]Telecoms, “France’s Free makes bold 5G standalone claims,” telecoms.com. Standalone architecture brings network-slicing that lets manufacturers, logistics operators, and public-safety agencies reserve deterministic bandwidth. Orange, SFR, and Bouygues Telecom are refarming 700 MHz and 2.1 GHz spectrum while ARCEP prepares new 3.8-4.2 GHz allocations to accommodate edge-AI workloads. Latency-sensitive use cases such as collaborative robotics and autonomous guided vehicles that stalled under 4G now move to commercial pilots. In parallel, systems integrators bundle 5G private-network design with managed-edge services, monetizing the connectivity-plus-compute stack across the France ICT market.

France’s “Cloud de Confiance” Certification Creates a Sovereign-Computing Paradigm

The Bleu platform, a EUR 525 million joint venture of Capgemini and Orange using Microsoft technology, began commercial operations in 2024 to serve workloads subject to French data-sovereignty statutes. The ANSSI SecNumCloud framework enforces 360 controls spanning administrative isolation and European legal immunity, guiding tender criteria in defense, healthcare, and critical-infrastructure domains. Hyperscalers without SecNumCloud status now partner with certified operators or lose access to public contracts, reshaping vendor shortlists across the France ICT market. Organizations handling sensitive workloads must therefore weigh sovereignty alongside cost and feature sets, elevating compliance as a decisive buying factor. The national stance also influences EU regulation: Paris resists broader, less stringent schemes, aiming to preserve its first-mover advantage in sovereign-cloud services.

Corporate Decarbonization Targets Reshape Data-Center Investment Patterns

Energy-intensive AI workloads push data-center load to 10 TWh—2.2% of France’s power draw in 2022—with forecasts calling for a 74% surge by 2050[2]RTE, “Data centers: 11 figures on growth and power needs,” rte-france.com. Operators exploit the nation’s 90% low-carbon electricity mix and nuclear baseload to market “green-compute” placements that help multinationals meet science-based-target pledges. Modern campuses post power-usage-effectiveness (PUE) scores near 1.1, halving energy waste versus legacy halls. Mandatory energy-performance audits for facilities above 500 kW, effective April 2025, accelerate retrofit cycles, favoring liquid cooling and heat-reuse schemes. Enterprises now bundle carbon-footprint audits with hosting contracts, embedding sustainability metrics into vendor scorecards. This green premium reinforces France’s competitive edge as cloud providers scale GPU farms for generative-AI services within the France ICT market.

Nationwide FTTH Completion Enables Service Innovation Beyond Connectivity

FTTH eligibility reached 92% of premises in March 2025, with 25.1 million active lines making up 77% of fixed subscriptions. Copper switch-off began in 162 municipalities, pushing legacy DSL users toward gigabit packages and freeing operators to refocus capital on service differentiation. SLA-grade fiber now anchors bundled offerings that integrate direct public-cloud peering, SD-WAN orchestration, and managed security. SMEs in rural communes gain symmetric bandwidth essential for SaaS ERPs and video-first collaboration, slicing through historic urban–rural digital divides. As ubiquitous fiber removes last-mile bottlenecks, developers roll out high-bandwidth apps such as immersive tele-health and virtual vocational training, enhancing addressable demand for the France ICT market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly fragmented SME channel inflates go-to-market costs | -1.4% | National, with rural concentration | Medium term (2-4 years) |

| Shortage of bilingual (FR/EN) cyber-security talent limits project delivery | -1.8% | National, with Paris region concentration | Long term (≥ 4 years) |

| Legacy mainframe estates in BFSI slow cloud migration | -0.9% | National, concentrated in financial districts | Long term (≥ 4 years) |

| Growing dependence on non-EU hyperscalers raises data-sovereignty concerns | -1.1% | National, with public sector emphasis | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented SME Channel Creates Scale Disadvantages for Technology Providers

Only 52% of French SMEs meet the EU’s basic-digital-intensity benchmark despite 73% enjoying fiber access, forcing vendors into high-touch education cycles that erode margins[3]France Num, “Baromètre 2024: perception et usages,” francenum.gouv.fr. Procurement is splintered across 4 million firms, each demanding tailored support yet generating modest contract values. Marketing spend per euro booked, therefore, remains multiples higher than enterprise business, deterring scale-out SaaS models. Government grants and France Num coaching temper the barrier, but suffer from fragmented awareness campaigns. Unless channel aggregators or regional digital-advisory hubs mature, friction around discovery, onboarding, and change management will continue to trim momentum for the France ICT market.

Cybersecurity Talent Shortage Constrains Market Growth Despite Rising Demand

The economy lacks 15,000 cybersecurity professionals even after 89% headcount growth since 2021, with dual-language skills most acute at[4]Government of France, “Attirer les jeunes vers les métiers de la cybersécurité,” info.gouv.fr . Median salaries of EUR 70,000 outstrip general ICT wages by 40%, inflating project costs and delaying cloud-migration timelines. Banks and utilities postpone zero-trust initiatives for want of certified engineers, and MSPs cap new logo intake when staffing pipelines dry up. Universities expand curricula, but certification paths such as CISSP and CISM extend learning cycles, slowing supply elasticity. Until international talent-mobility rules loosen or vocational fast-tracks scale, security bottlenecks will temper upside in the France ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Dominance Accelerates Cloud Transformation

IT Services contributed 45.20% to the France ICT market share in 2025 as enterprises outsourced complex digital-transformation workloads. Price-premium mandates around AI integration, cybersecurity hardening, and legacy modernization are locked in multiyear managed-service contracts. Cloud Services, advancing at a 12.10% CAGR, benefit directly from sovereign-cloud mandates and green-data-center preferences. The France ICT market size for Cloud Services is projected to rise in tandem with Bleu’s roll-out as ministries port sensitive workloads from on-premise stacks to SecNumCloud-ready environments. Hardware refresh cycles persist around edge gateways and enterprise Wi-Fi 7 upgrades, yet value shifts decisively toward X-as-a-Service models that monetize talent scarcity rather than physical assets.

The mid-term narrative centers on platform orchestration: providers bundling observability, FinOps, and AI-ops capabilities out-compete pure-play resellers. Software vendors embed generative-AI copilots into ERP and CRM suites, lifting attach revenues. Communication-service providers reposition into digital-experience orchestrators, fusing 5G-MEC capacity with SaaS marketplaces. Collectively, these trends reinforce the service-weighted composition of the France ICT market and tilt margins toward knowledge-intensive offerings.

By Enterprise Size: SME Growth Momentum Challenges Large-Enterprise Dominance

Large enterprises retained 70.30% of the France ICT market size in 2025 but face slower expansion as mainframe remediation and compliance reviews elongate project cycles. SMEs, posting a 9.55% CAGR, leverage cloud marketplaces and low-code tooling to bypass legacy constraints. Subscription-priced cybersecurity bundles and all-inclusive managed-LAN packages flatten upfront cost barriers, letting SMEs achieve digital parity.

Government vouchers under France Num subsidize hardware refreshes and digital-skills training, widening the funnel of qualified buyers. Marketplace aggregators that pre-integrate accounting, e-commerce, and cyber-insurance serve as one-stop shops, sidestepping the fragmented reseller ecosystem. As FTTH penetration removes last-mile constraints, rural micro-enterprises adopt SaaS POS and cloud storage. This groundswell narrows the digital-intensity gap and reallocates incremental spending toward the SME cohort within the France ICT market.

By Industry Vertical: BFSI Leadership Faces Gaming-Sector Disruption

BFSI owned 17.55% of the France ICT market share in 2025, channeling budgets into core-bank modernization, open-finance APIs, and real-time payment compliance. However, Gaming and Esports, fueled by a EUR 6.1 billion domestic games market, is on track for a 14.35% CAGR, positioning consumer-experience workloads as the next demand frontier SELL.FR.

Banks pilot quantum-ready encryption and federated-learning fraud models, yet must divert OpEx to remediate 84% of legacy mainframe estates. Conversely, studios and esports platforms exploit 5G-edge rendering and AI-generated content pipelines that require elastic GPU capacity. The divergent growth trajectories widen the sector-mix shift: by 2030, entertainment workloads could surpass regulated-finance use in incremental cloud consumption, redefining workload prioritization across the France ICT market.

By Deployment Model: Cloud-Only Dominance Accelerates Public-Cloud Adoption

Cloud-only architectures represented 56.85% of the France ICT market in 2025 as boards endorsed cloud-first mandates to access advanced analytics and generative-AI toolchains. Public-cloud consumption is forecast at an 17.60% CAGR, assisted by sovereign instances that satisfy data-residency clauses while retaining hyperscaler innovation velocity. The France ICT market size for public-cloud workloads will therefore expand faster than hybrid or private counterparts.

On-premise environments linger in defense and utilities where latency or national-security statutes dictate physical control. Nevertheless, as SecNumCloud certifications proliferate and dual-region redundancy becomes turnkey, even mission-critical workloads migrate. Edge mini-data-centers supplement public-cloud backbones for deterministic latency, letting service providers offer “local cloud” zones to manufacturing sites. Consequently, cloud-only paradigms will predominate in new workload placement across the France ICT market.

Geography Analysis

The Île-de-France region concentrates over 70 tier-III and higher data centers worth EUR 1.2 billion and serves as the backbone for continental traffic exchange. The France ICT market size for the capital cluster, therefore, dwarfs provincial hubs, yet the balance is shifting. In Auvergne-Rhône-Alpes, Lyon combines automotive and biotech verticals, sparking edge-data-center builds and 5G testbeds. Grenoble attracts EU-Chips-Act subsidies, anchoring a semiconductor design corridor that catalyzes specialized EDA and HPC software demand. Occitanie’s Toulouse aerospace complex employs digital-twin platforms and predictive-maintenance AI, lifting regional ICT outlays.

Fiber-to-the-home completion equalizes rural connectivity: Grand Est and Nouvelle-Aquitaine SMEs now procure SaaS tools previously out of reach, raising per-capita ICT spend. Brittany and Normandy leverage offshore wind and tidal energy to lure green-compute campuses, aligning with data-center decarbonization strategies. Cross-border submarine-cable landing points at Marseille foster Middle East and Africa traffic, transforming Provence-Alpes-Côte d’Azur into a latency-optimized hub for streaming and gaming workloads. Nationally, the France ICT market benefits from France’s EU membership while wielding independent sovereignty controls, striking a balance between continental scale and domestic governance that few peers replicate.

Competitive Landscape

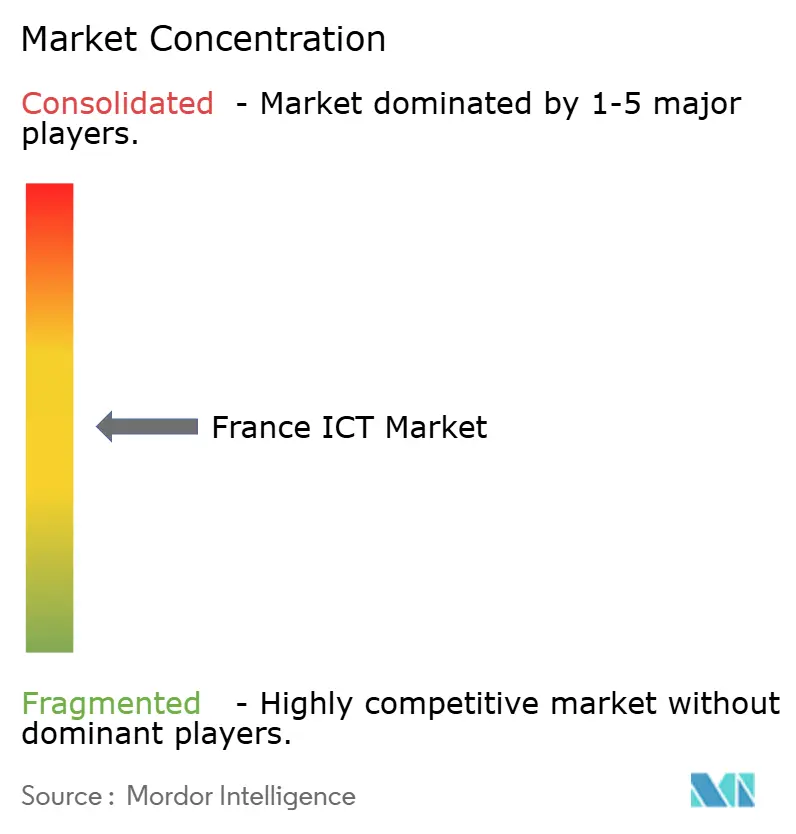

France’s ICT arena is moderately concentrated: the top five providers hold an estimated 48% revenue share across connectivity, cloud, and services. Orange leads fixed and mobile access, monetizing FTTH and 5G-SA upgrades, while SFR, Bouygues Telecom, and Free Mobile defend share via aggressive unlimited-data bundles. Microsoft, IBM, and AWS capitalize on enterprise-cloud migrations, yet SecNumCloud qualifiers Capgemini-Orange (Bleu) and Thales-Google (S3NS) carve out protected niches. OVHcloud leverages European roots to market sovereign-ready IaaS and has opened liquid-cooling GPU clusters in Roubaix.

Strategic pivots focus on regulatory differentiation more than raw price. Orange bundles sovereign-cloud resell with managed-MEC security; Capgemini invests in generative-AI centers to offset slower consulting growth; Dassault Systèmes layers cloud-delivered PLM with sustainability metrics for manufacturing clients. Carlyle’s planned acquisition of Ciril Group underscores private-equity appetite for sovereign providers amid rising compliance spend. Talent scarcity drives M&A for specialized skills: HCLTech acquired Zeenea to secure data-governance IP, and ChapsVision bought Sinequa to embed AI-search into defense analytics stacks.

Emerging challengers include Mistral, developing French-language large language models, and Foxway, scaling circular-IT refurb services to satisfy ESG procurement rules. Overall, competition hinges on who best fuses sovereignty, sustainability, and sector-specific AI, a triad redefining value capture in the France ICT market.

France ICT Industry Leaders

Samsung Electronics Co., Ltd

Microsoft Corporation

IBM Corporation

Infosys Limited

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Brookfield pledged EUR 20 billion for AI-ready data-center capacity, including a Cambrai mega-campus slated to come online by 2028.

- February 2025: Orange delivered 2024 net income of EUR 2.35 billion and outlined a 3% EBITDAaL growth target for 2025, sustaining a EUR 0.75 dividend floor.

- February 2025: Capgemini posted a softer 2025 outlook after 2024 sales resilience, doubling down on generative-AI capability centers.

- January 2025: Orange began copper network switch-off in 162 communes, accelerating FTTH migration toward 90% premises coverage.

France ICT Market Report Scope

ICT refers to a range of technological applications used to transmit and process information. Information, communication, and technology are combined to produce the term ICT.

France ICT market is segmented by type (IT hardware (computer hardware, networking equipment, peripherals), IT software, IT services (managed services, business process services, business consulting services, cloud services), IT infrastructure/data centers (colocation data centers, data center storage, data center servers, data center compute), IT security/ cybersecurity (application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, endpoint security), communication services), by enterprise size (small and medium enterprises, large enterprises), by industry vertical (BFSI, IT & Telecom, government, retail & e-commerce, manufacturing, energy & utilities, others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

France ICT market tracks revenue accrued through the sale of ICT offerings including IT hardware, IT software, IT services, IT infrastructure and communication services that are being used in various end-user industry across the France.

The study tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from the various ICT types that are used in various industry verticals across France. Additionally, the study provides the France ICT market trends, along with key vendor profiles. The study further analyses the overall impact of COVID-19 on the ecosystem.

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

By Deployment Model

| On-Premise |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

By Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| Banking, Financial Services and Insurance (BFSI) |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Energy and Utilities |

| Healthcare and Life Sciences |

| Gaming and Esports |

| Education |

| Other Verticals |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Deployment Model | On-Premise | |

| Public Cloud | ||

| Private Cloud | ||

| Hybrid Cloud | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Energy and Utilities | ||

| Healthcare and Life Sciences | ||

| Gaming and Esports | ||

| Education | ||

| Other Verticals | ||

Key Questions Answered in the Report

What is the current value of the France ICT market?

The France ICT market size is USD 147.2 billion in 2026.

How fast is ICT spending growing in France?

Market value is projected to expand at a 9.02% CAGR, reaching USD 226.5 billion in 2031.

Which segment is growing the fastest?

Cloud Services is the fastest-growing type, posting a 12.10% CAGR through 2031.

Why is sovereign cloud important in France?

SecNumCloud standards and the Bleu platform ensure data residency and legal immunity from non-EU jurisdictions, driving adoption in public and regulated sectors.

Page last updated on: