France SLI Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

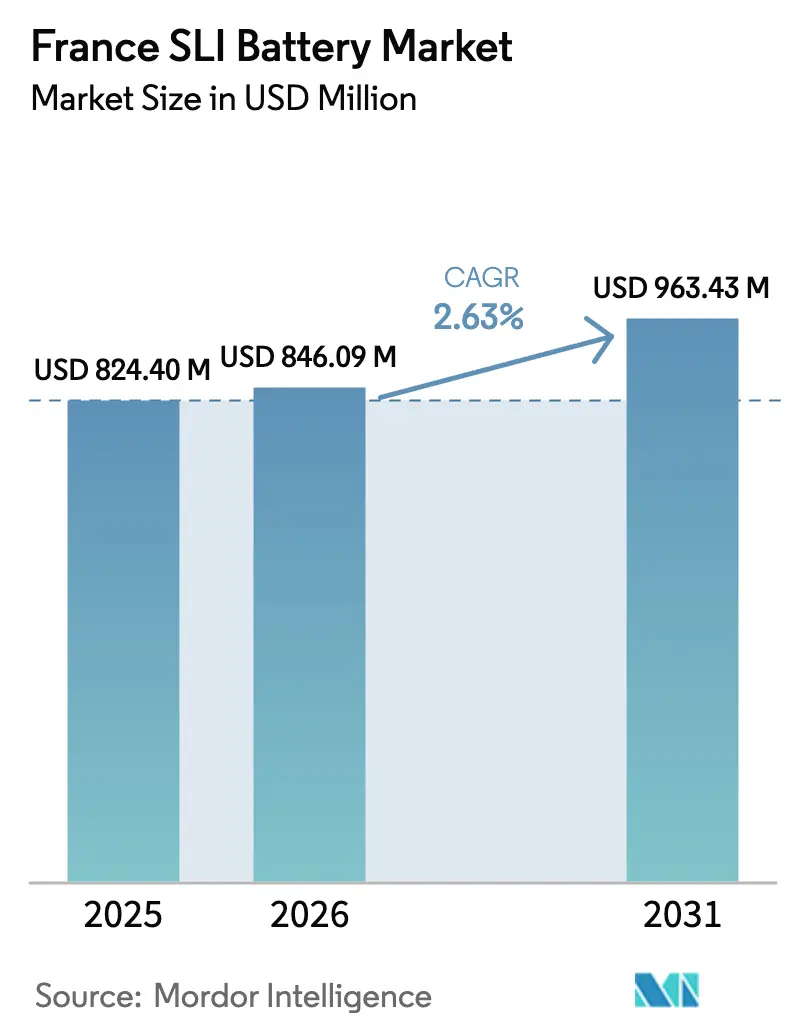

| Base Year Market Size (2025) | USD 824.40 Million |

| Market Size (2026) | USD 846.09 Million |

| Market Size (2031) | USD 963.43 Million |

| Growth Rate (2026 - 2031) | 2.63% CAGR |

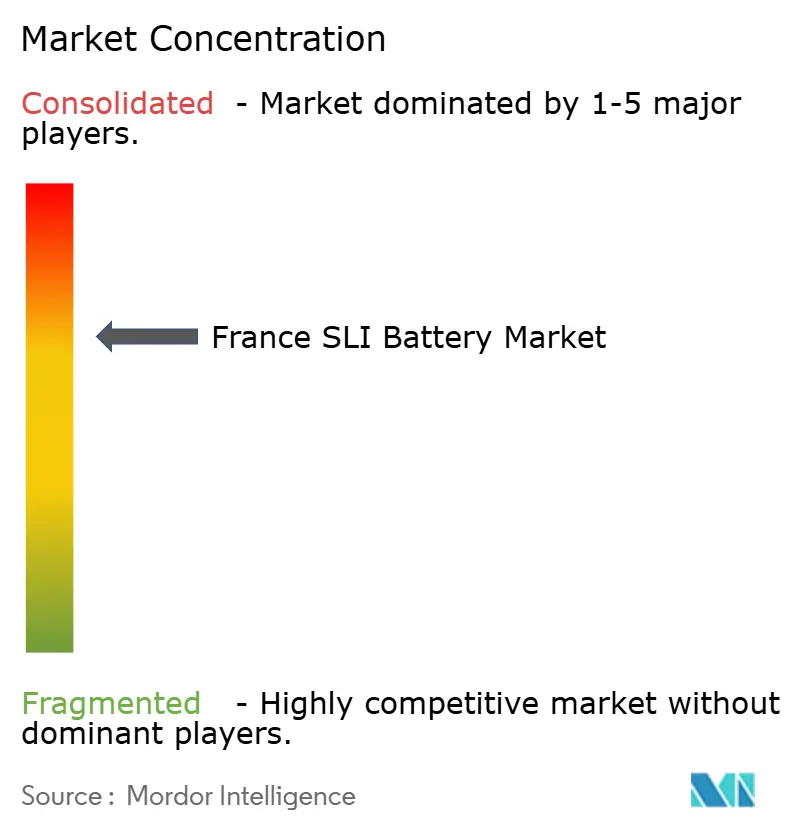

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France SLI Battery Market Analysis by Mordor Intelligence

The France SLI Battery Market size is expected to grow from USD 824.40 million in 2025 to USD 846.09 million in 2026 and is forecast to reach USD 963.43 million by 2031 at 2.63% CAGR over 2026-2031.

Demand remains tethered to the nation’s 30 million-plus vehicle park, yet value per unit is climbing as micro-hybrid and mild-hybrid platforms mandate higher-performing batteries that endure 3-5 times more charge-discharge cycles than legacy flooded cells. Regulation (EU) 2023/1542 adds further momentum by forcing every starter battery placed on the French market after August 18, 2025, to carry a digital passport and carbon-footprint label, accelerating inventory turnover at distributors and nudging end users toward sealed, maintenance-free products that simplify compliance. Simultaneously, the coexistence of 12 V auxiliary batteries in battery-electric vehicles safeguards baseline replacement volumes even as full electrification gains speed; EUROBAT estimates a 50 GWh 12 V SLI market across Europe, with lead-acid retaining a 96% share. Raw-material costs, especially lead, continue to sway margins: London Metal Exchange prices dipped to USD 1,968 per tonne in October 2025 amid a forecast supply surplus, intensifying price competition among aftermarket wholesalers.[1]International Lead and Zinc Study Group, “Lead and Zinc New Mine Projects,” ilzsg.org

Key Report Takeaways

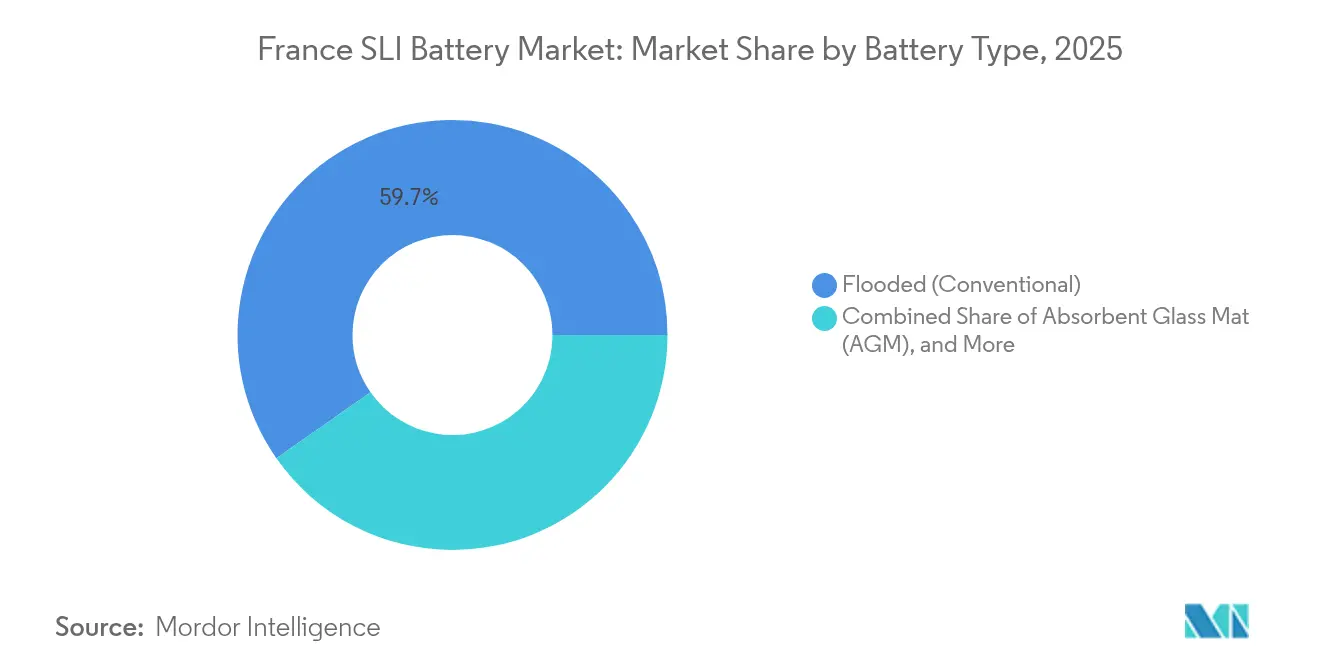

- By battery type, flooded lead-acid commanded 59.72% of the France SLI Battery market share in 2025, while Absorbent Glass Mat (AGM) units are expected to expand at a 6.74% CAGR through 2031.

- By voltage, 12 V systems held 70.25% of 2025 revenue; batteries supporting 48 V mild-hybrid architecture are forecast to advance at a 7.35% CAGR to 2031.

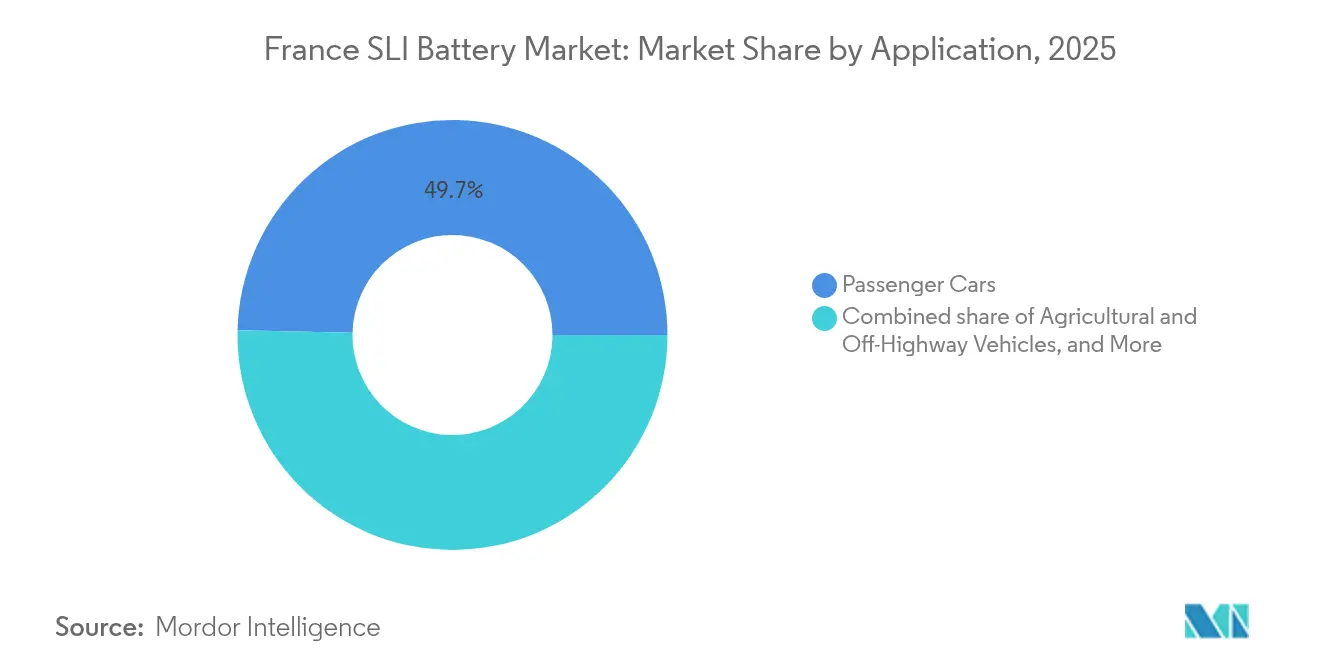

- By application, passenger cars accounted for 49.65% of 2025 demand, whereas agricultural and off-highway vehicles are projected to record the highest 6.12% CAGR over the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within France feed into a worldwide estimate while studying the global industry. Mordor Intelligence's sli battery market size captures this aggregation.

France SLI Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of micro-hybrid (start-stop) vehicles | +0.7% | France, with spillover to broader EU markets | Medium term (2-4 years) |

| Mandatory EU battery passport compliance accelerating replacement demand | +0.5% | EU-wide, France implementing via Decree 2024-1221 | Short term (≤ 2 years) |

| Growing rural mechanization driving demand from agricultural machinery | +0.4% | Rural France, particularly Hauts-de-France and agricultural regions | Long term (≥ 4 years) |

| Smart-grid ancillary-service pilots using repurposed SLI batteries | +0.3% | Urban France (Paris, Lyon) and industrial zones with V2G infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Micro-Hybrid (Start-Stop) Vehicles

Stellantis fielded 30 micro-hybrid models in 2024 and plans six more launches by 2026, each integrating a 21 kW motor and a 0.9 kWh 48 V pack that cuts CO₂ by up to 18% and necessitates AGM or Enhanced Flooded Batteries that endure triple the cycling of conventional designs. Renault mirrors this trajectory, equipping the Austral, Duster, Kangoo, and Jogger ranges with 48 V power distribution units supplied by MTA, embedding start-stop capability in high-volume segments. VARTA reports that seven in ten new EU vehicles fitted with start-stop systems ship with its AGM technology, underscoring a widespread OEM commitment to the chemistry. The result is a revenue mix shift: even modest gains in unit volume translate into materially higher market value because each AGM battery retails at a 40-60% premium to a flooded equivalent. Tier-1 suppliers are positioning accordingly; Eberspaecher and Farasis agreed in February 2025 to co-develop dual-voltage 12 V-48 V packs, viewing micro-hybrids as a multi-decade profit pool rather than a transitional curiosity.

Mandatory EU Battery Passport Compliance Accelerating Replacement Demand

Regulation (EU) 2023/1542 requires every SLI battery sold after August 18, 2025, to display a digital passport, carbon-footprint metrics, and eco-contribution information, with France enforcing the rule through Decree 2024-1221 and introducing penalties under Article R.543-129 of the Environment Code.[2]TwoBirds, "Towards a circular economy for all batteries: key points of the new European Regulation," twobirds.com The fixed cost of retooling labels, logistics systems, and IT infrastructure disproportionately burdens small distributors, driving a wave of stock rationalization that has compressed the normal 18-24-month replacement cycle into roughly 12-15 months heading into 2026. Passport data also tracks recycled-content thresholds, pushing supply chains toward closed-loop sourcing; GS Yuasa lifted its recycled-lead ratio to 38.7% in FY 2023 and is targeting 45% by FY 2025. Larger players with integrated recycling can thus amortize compliance spend across broader volumes, capturing share as smaller rivals exit. The regulation is therefore simultaneously a cost and a demand catalyst for the France SLI Battery market.

Growing Rural Mechanization Driving Demand from Agricultural Machinery

French agricultural machinery output is rebounding toward 2 million vehicles annually by the late-decade horizon, underpinned by farm modernization and equipment electrification road-maps from OEMs such as Manitou. Agricultural tractors, harvesters, and telehandlers typically specify Group 31 or larger batteries (80-120 Ah) to crank high-compression diesel engines and power auxiliary loads, a configuration still cost-optimized around lead-acid technology. Field equipment enjoys service lives of 10-15 years, translating into high-value replacement cycles that can offset urban declines tied to battery-electric car adoption. Renault’s assembly hubs in Hauts-de-France sit close to major farming regions, enabling distributors to overlap passenger-car and agricultural channels, reducing logistics overhead and accelerating inventory turns. These geographic efficiencies reinforce rural demand as a structurally important growth lever for the France SLI Battery market.

Smart-Grid Ancillary-Service Pilots Using Repurposed SLI Batteries

EDF and Renault Mobilize Power aggregate retired EV and SLI batteries into vehicle-to-grid fleets that deliver frequency-regulation services, with Fraunhofer ISE estimating EUR 400-600 in annual value per participating vehicle in France.[3]Transport & Environment, "Vehicle-to-Grid Economics and Battery Life Study - France Focus," transportenvironment.org The Clean Industry State Aid Framework adopted in February 2025 widened subsidy eligibility for short-duration storage assets, reducing payback periods for 1-2 hour projects. Repurposed AGM and gel VRLA batteries fit these niches, offering high power density and an established recycling path at lower upfront cost than new lithium-ion systems. European electrochemical storage additions reached 4.9 GW/12.1 GWh in 2024, with the average project duration extending from 1.5 hours to 2.5 hours, further aligning with lead-acid’s performance envelope. The emerging second-life avenue thus stretches product value across multiple use cases, anchoring end-of-life compliance within a circular economy model embraced by EU policymakers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of Li-ion 12V starter packs in premium models | -0.4% | France premium segment (Paris, Lyon, Côte d'Azur) | Medium term (2-4 years) |

| Lead-price volatility squeezing aftermarket margins | -0.3% | France aftermarket distribution, particularly independent retailers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Li-ion 12 V Starter Packs in Premium Models

EUROBAT anticipates lithium-ion 12 V capacity in Europe to exceed 5 GWh by 2030, supported by weight-sensitive luxury OEMs such as BMW, Mercedes-Benz, and Audi adopting lithium-iron-phosphate starter packs that are up to 50% lighter than lead-acid equivalents. The EU’s 2025 CO₂ fleet targets amplify this incentive; every kilogram saved reduces compliance pressure, making high-priced lithium solutions tolerable in premium segments.[4]European Parliament Research Service, “Fit-for-55: CO₂ Standards for Cars and Vans,” europarl.europa.eu Cold-cranking performance in sub-zero conditions remains a technical hurdle, limiting immediate mass-market migration, but scale learning may erode cost differentials post-2028. For the France SLI Battery market, displacement risk is therefore front-loaded in urban luxury clusters that already turn over vehicles frequently, trimming high-margin aftermarket sales by an estimated 3-5% in those districts between 2025-2027. Suppliers are hedging via dual-chemistry portfolios, yet the profit mix could narrow if lithium technology cascades into mid-range vehicles later in the decade.

Lead-Price Volatility Squeezing Aftermarket Margins

London Metal Exchange spot lead ended October 2025 at USD 1,968 per tonne, and the International Lead and Zinc Study Group forecasts global surpluses of 2% in 2025 and 1% in 2026, trends that push prices lower but not necessarily margins higher. Distributors lock in battery costs on quarterly contracts yet face monthly raw-material swings, exposing them to lag effects when lead rallies. Conversely, price drops prompt immediate demands from retailers for rebates, dulling any upside benefit. Surplus Asian production, enabled by lower energy and labor costs, has raised EU-bound lead-battery imports by 25.8% in 2024, intensifying price competition. Over time, the EU Battery Regulation’s recycled-content rules may stabilize volatility by elevating secondary lead use, but the transition period through 2027 leaves wholesalers navigating a profit squeeze that could accelerate consolidation in the France SLI Battery industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: AGM Captures Start-Stop Surge

Flooded lead-acid batteries accounted for 59.72% of 2025 demand, reflecting deep penetration in legacy internal-combustion vehicles where cost per ampere-hour dominates purchase criteria. AGM products are poised to outpace every other chemistry at a 6.74% CAGR to 2031, powered by OEM mandates for micro-hybrid compatibility and Clarios’ EUR 200 million program that lifts EMEA AGM capacity by roughly 50% by 2026.

The France SLI Battery market size linked to AGM replacement is therefore set to expand as the first wave of start-stop vehicles sold between 2019-2021 reaches the 4-7-year replacement window. Conventional flooded units will remain essential for budget-oriented buyers, yet product mix will swing toward sealed designs that reduce maintenance and comply with forthcoming carbon-footprint disclosures. Flooded products retain relevance in marine, recreational, and backup-power niches where deep-discharge needs are uncommon, but regulatory and performance tailwinds clearly favor AGM.

By Battery Voltage: 48 V Systems Redefine Architecture

Twelve-volt batteries still generated 70.25% of 2025 revenue thanks to the vast installed base of passenger cars and light commercial vehicles in France. However, systems incorporating a 48 V pack are forecast to log a 7.35% CAGR through 2031 as Stellantis scales production above 1.2 million mild-hybrid units per year from Metz, and Renault integrates 48 V power electronics across four model lines.

The 12 V unit is not disappearing; battery-electric vehicles still need a small lead-acid battery for legacy loads, anchoring a France SLI Battery market share that EUROBAT estimates at 96% for lead-acid within the 12 V segment. Yet for suppliers, portfolio balance is critical: they must defend mature 12 V volumes while investing in 48 V modules and managing the slower growth of above-60 V lead-acid units in industrial vehicles, where lithium-ion competes aggressively.

By Application: Agriculture Offsets Passenger-Car Maturity

Passenger cars supplied 49.65% of sales in 2025, sustained by replacement cycles averaging 4-6 years for flooded batteries and up to 7 years for AGM batteries. Light commercial vehicles add a stable mid-tier segment, while agricultural and off-highway machinery is the outlier, projected to deliver a 6.12% CAGR through 2031 on the back of rising rural mechanization and the shift toward higher-capacity Group 31 batteries for tractor and harvester fleets.

Industrial motive-power units, especially Class 3 forklifts, increasingly migrate to lithium-ion packs, trimming a once-steady SLI niche. Nonetheless, steady growth in agriculture and continued demand in standby power offset much of the industrial slippage, allowing diversified producers to re-allocate capacity as application mixes evolve within the France SLI Battery market.

Geography Analysis

France’s automotive recovery targets 2 million vehicle assemblies annually by 2027-2030, up from sub-1.5 million lows in 2022, centered on Stellantis and Renault plants in Hauts-de-France and the Paris basin. Local production anchors OEM-grade battery demand, while an installed base exceeding 30 million vehicles drives predictable aftermarket volumes. Proximity of battery makers to assembly plants shortens transit times, enabling just-in-time delivery and curbing working-capital needs for distributors.

Rural growth poles in Normandy and Nouvelle-Aquitaine fuel higher-capacity battery sales to agricultural equipment dealers. Urban hubs, Paris, Lyon, Marseille, lead adoption of micro-hybrid and BEV models, accelerating AGM mix and introducing nascent lithium-ion 12 V demand in premium fleets. The August 2025 battery-passport deadline is prompting distributors nationwide to cleanse inventory of non-compliant product, sparking a transient restocking wave that peaks in 2025-2026.

France also benefits from EU funding for battery manufacturing and recycling; Automotive Cells Company’s gigafactory at Douvrin is ramping 15 GWh of lithium-ion capacity with another 13 GWh under construction, solidifying a domestic supply chain that can spill over into 48 V packs for mild hybrids. Cross-border flows remain influential: German premium-model imports shape aftermarket chemistry demand, while Spanish and Italian component plants offer cost-effective sub-assemblies that feed French pack integrators.

Mordor Intelligence evaluates the sli battery market across all key regional markets, including Europe and Middle East and Africa, with deeper country-level insights covering Italy, Germany, China, United States, United Kingdom, and India.

Competitive Landscape

Four multinationals, Clarios, Exide Technologies, GS Yuasa, and EnerSys, collectively hold roughly 60-70% of the France SLI Battery market, leaving a long tail of regional distributors and imports to contest the balance. Clarios’ 50% AGM capacity lift across EMEA by 2026 illustrates the scale now required to service micro-hybrid demand, while GS Yuasa’s drive to raise recycled-lead content to 45% by 2025 showcases the operational pivot needed for EU compliance.

Technology differentiation is emerging: VARTA’s PowerFrame design improves charge acceptance, aiding OEMs in hitting stringent CO₂ targets, whereas XAP Technology’s French-made Battery Management Unit opens software-based value capture in retrofit and stationary segments. Adjusting to regulatory complexity, large players leverage ISO 14001 and Industrial Emissions Directive certifications to secure OEM and aftermarket contracts, a barrier that smaller firms struggle to clear.

Disruptive entrants include Asian lithium-ion 12 V suppliers exporting surplus capacity, and niche French startups repurposing used batteries for grid services under EDF and Renault Mobilize pilots. Mergers remain muted until lead-price volatility abates, but partnership activity signals strategic hedging: Eberspaecher and Farasis blend thermal-management and cell expertise to pursue dual-voltage packs, providing a template for collaboration in an uncertain chemistry landscape.

France SLI Battery Industry Leaders

-

Exide Technologies

-

GS Yuasa International Ltd.

-

Clarios

-

EnerSys

-

Varta AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Exide announced it will halt lead-acid battery production at its long-standing Lille plant, citing economic challenges, market declines, and an oversupply in the industrial traction battery market.

- November 2024: Exide Technologies has expanded its Absorbed Glass Mat (AGM) range, now covering nearly one million more vehicles across Europe. The newly introduced AGM EK454 and EK457 (45Ah/380A, size B24) feature terminals: standard ones meet European Norm (EN) standards, while the thin taper terminals align with the Japanese Industrial Standard (JIS).

- July 2024: The EU finalized Regulation 2023/1542 timelines; France codified requirements through Decree 2024-1221, mandating digital passports for SLI batteries by Aug 18 2025.

France SLI Battery Market Report Scope

An SLI (starting, lighting, and ignition) battery is a type of rechargeable battery designed primarily for automotive applications. It is used to start the engine, power the vehicle's lighting system, and ignite the fuel. These batteries are typically lead-acid batteries, favored for their reliability and ability to deliver high surge currents needed to start an engine.

The France SLI battery market is segmented by battery type, battery voltage, and application. By battery type, the market is segmented into flooded, enhanced flooded, absorbent glass mat (AGM), and gel cell VRLA. By battery voltage, the market is segmented into up to 12V, 12V, 48V, and above 60V. By application, the market is segment into passenger cars, light commercial vehicles, heavy commercial vehicles, two-/three-wheelers, agricultural & off-highway vehicles, industrial motive power (forklifts, material-handling), and stand-by/backup (telecom, UPS). For each segment, market sizing and forecasts are presented on a value (USD) basis.

| Flooded (Conventional) |

| Enhanced Flooded (EFB) |

| Absorbent Glass Mat (AGM) |

| Gel Cell VRLA |

| Up to 12 V |

| 12 V |

| 48 V |

| Above 60 V |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-/Three-Wheelers |

| Agricultural and Off-Highway Vehicles |

| Industrial Motive Power (Forklifts, Material-Handling) |

| Stand-by/Backup (Telecom, UPS) |

| By Battery Type | Flooded (Conventional) |

| Enhanced Flooded (EFB) | |

| Absorbent Glass Mat (AGM) | |

| Gel Cell VRLA | |

| By Battery Voltage | Up to 12 V |

| 12 V | |

| 48 V | |

| Above 60 V | |

| By Application | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Two-/Three-Wheelers | |

| Agricultural and Off-Highway Vehicles | |

| Industrial Motive Power (Forklifts, Material-Handling) | |

| Stand-by/Backup (Telecom, UPS) |

Key Questions Answered in the Report

How large is the France SLI Battery market in 2026?

The France SLI Battery market size is USD 846.09 million in 2026 and is forecast to reach USD 963.43 million by 2031.

Which chemistry is growing fastest in France?

Absorbent Glass Mat batteries are projected to grow at a 6.74% CAGR through 2031, driven by start-stop vehicle adoption.

Why is 48 V architecture important for French automakers?

A 48 V mild-hybrid system delivers 15-18% CO₂ cuts while coexisting with a 12 V battery, offering a cost-effective bridge to full electrification.

How will EU Regulation 2023/1542 influence battery sales?

Mandatory digital passports and recycled-content disclosures from August 2025 are bringing forward replacement purchases and favoring compliant suppliers.

What impact does lead-price volatility have on distributors?

Quarterly contract pricing versus monthly metal swings compresses margins, incentivizing broader use of secondary lead and driving consolidation.

Are lithium-ion 12 V starter batteries a threat?

Penetration is rising first in premium models; volumes stay modest through 2027 but could widen if costs fall and cold-cranking performance improves.

Page last updated on: