Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.90 Billion |

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Sourdough Market Analysis by Mordor Intelligence

The European sourdough market size was valued at USD 0.90 billion in 2025 and estimated to grow from USD 0.95 billion in 2026 to reach USD 1.25 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031). The market expansion reflects increased consumer interest in traditional fermentation methods, driven by health awareness and demand for artisanal products. Belgium has emerged as a key player in the sourdough renaissance, with European manufacturers combining traditional methods with industrial production capabilities. The industry's shift toward scaled production has created opportunities for technological advancement, as demonstrated by Puratos' Sourdough Institute launch in Belgium in 2024 and Aryzta's USD 12 million investment in a stone oven facility at its Eisleben location. Market growth is primarily driven by demand for clean-label products, protein enrichment trends, and accessible home baking solutions. However, the market faces challenges including price competition with conventional bread products and production limitations among artisanal bakers in smaller markets. Raw material price fluctuations, particularly for specialty and rye flours, continue to impact profit margins, with German bakery prices rising by 33% between 2019 and 2023, as reported by the Federal Statistical Office (FinanzNachrichten.de). These factors highlight the market's progression from specialized artisanal production to mainstream manufacturing, supported by technological advancements and strategic investments.

Key Report Takeaways

- By form, dry mix and premix solutions led with 61.74% of the European sourdough market share in 2025, while ready-to-use liquid solutions recorded the highest projected CAGR at 6.48% through 2031.

- By application, bread and buns accounted for 67.98% of the European sourdough market size in 2025, while pizza crusts and bases recorded the highest projected CAGR at 7.54% through 2031.

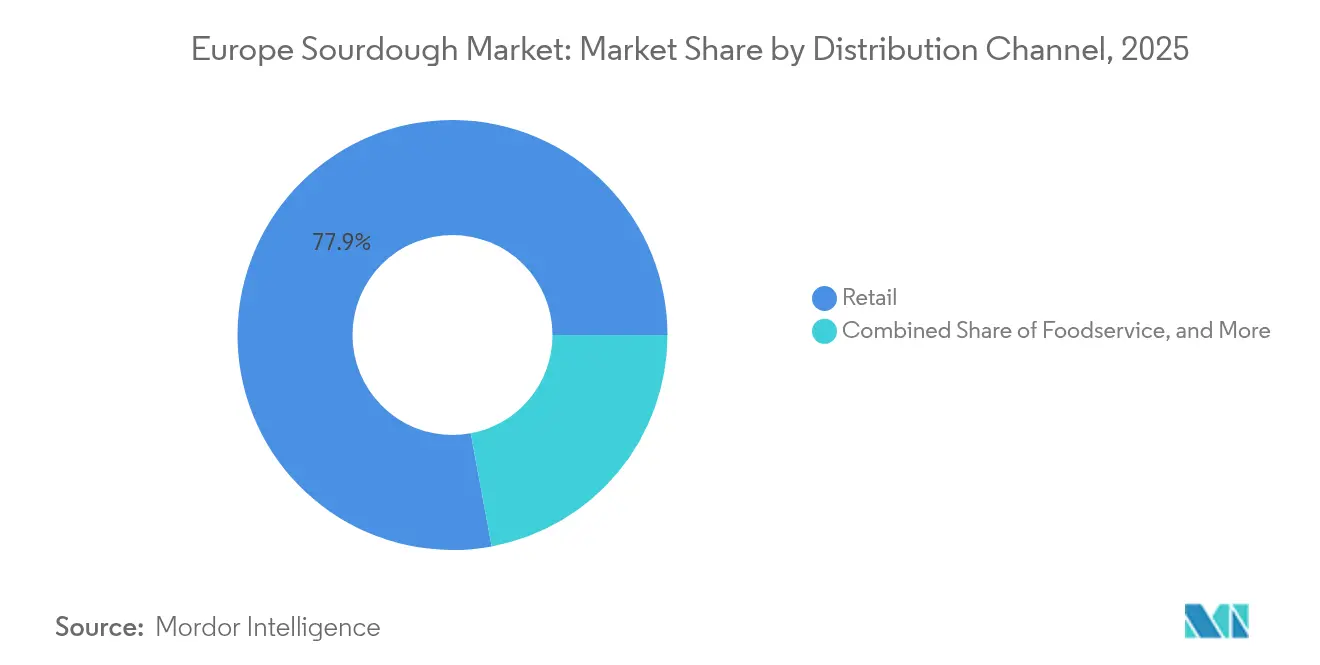

- By distribution channel, the retail segment commanded 77.92% of the European sourdough market size in 2025, and foodservice is advancing at a 6.87% CAGR to 2031.

- By geography, Germany held 22.63% of Europe's sourdough market share in 2025, while the United Kingdom is forecast to expand at an 7.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Sourdough Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for artisanal and traditional baking methods | +1.2% | Germany, Italy, France, Belgium | Medium term (2-4 years) |

| Growing demand for clean-label breads with longer shelf life | +1.1% | Global, with strongest uptake in UK, Netherlands | Short term (≤ 2 years) |

| Expansion of convenient formats and home baking solutions | +0.9% | North America and EU, particularly urban centers | Medium term (2-4 years) |

| Industrialised liquid and dried starters enabling scale | +0.8% | Germany, France, Netherlands, Belgium | Long term (≥ 4 years) |

| Regenerative and ancient-grain flour sourcing agreements | +0.7% | EU core markets, spill-over to Eastern Europe | Long term (≥ 4 years) |

| Increasing protein and nutrient fortification trends | +0.6% | UK, Germany, Nordics with health-focused consumers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Artisanal and Traditional Baking Methods

According to Puratos' tracking of Google trends data, searches for sourdough surged fivefold during the pandemic, underscoring a decisive shift in consumer preferences toward authentic fermentation processes[1]Source: Puratos, “Sourdough is on the Rise,” puratos.com. This heightened demand isn't limited to home bakers; commercial foodservice operators are now actively seeking out differentiated bread offerings that can command premium prices. In response to this trend, major industrial players are channeling investments into initiatives aimed at preserving culinary heritage. A prime example is Puratos, which maintains a library in Belgium housing 84 distinct sourdough cultures, alongside documentation of over 700 wild yeast strains and 1,500 lactic acid bacteria strains. By blending artisanal methods with industrial processes, suppliers gain a competitive edge, delivering consistent quality without compromising on traditional flavor profiles. In the UK, the Federation of Bakers has introduced a sourdough code of practice, offering regulatory clarity that not only sets quality standards for commercial production but also bolsters market expansion. This framework empowers smaller producers to compete on a level playing field, all while reinforcing consumer trust in the authenticity of the products.

Growing Demand for Clean-Label Breads with Longer Shelf Life

Driven by consumer scrutiny of ingredient lists and a demand for recognizable components, clean-label positioning has become essential for market access. Sourdough's natural fermentation process offers preservation benefits through organic acid production, which not only reduces the need for synthetic additives but also extends shelf life. In 2024, Kerry launched Biobake Fibre specifically for rye bread applications, showcasing how ingredient suppliers are meeting clean-label demands while fulfilling functional needs[2]Source: Kerry, “Biobake Fibre,” kerry.com. The European Union mandates comprehensive disclosure of processing aids and additives, creating a competitive edge for naturally fermented products that need fewer ingredient declarations. Corbion introduced natural mold inhibition solutions in April 2025, highlighting industry innovation in tackling shelf-life challenges while maintaining clean-label integrity[3]Source: Corbion, “Mold Inhibition Solutions,” corbion.com. This trend is especially advantageous for retail channels, as the extended shelf life of sourdough products not only reduces waste but also enhances distribution economics, allowing them to compete more effectively against conventional breads.

Expansion of Convenient Formats and Home Baking Solutions

Beyond pandemic-induced surges, the home baking segment has seen steady growth, driven by consumers' desire for convenient formats that yield artisanal results without demanding extensive time. Dry mix and premix formats, commanding a 62.38% market share, enable consistent home production while preserving the distinctive flavor development of sourdough. In response, industrial suppliers have crafted starter systems that streamline fermentation without compromising authentic taste. Addressing this demand, IREKS expanded its MONDO LIEVITO MADRE product line in 2025, offering standardized sourdough solutions for both commercial and home use. This trend of convenience isn't limited to home bakers; foodservice operators also seek dependable sourdough solutions that cut down prep time without sacrificing quality. Furthermore, collaborations between ingredient suppliers and grocery chains have broadened the reach of home baking solutions. These partnerships are bolstered by educational content, instilling confidence in consumers regarding sourdough preparation techniques.

Industrialized Liquid and Dried Starters Enabling Scale

Industrial-scale starter production has shifted sourdough from a niche craft to a mass-manufactured product, ensuring uniform quality even at large volumes. In September 2024, Lesaffre introduced Tradizy Durum, showcasing breakthroughs in starter stabilization technology that preserve microbial activity during storage and transit. Liquid starter systems streamline operations with less handling and better fermentation oversight, whereas dried formats boast a longer shelf life and easier logistics. The European Food Safety Authority has eased regulatory hurdles for small bakeries, promoting the use of starter-based production systems[4]Source: EFSA, “Qualified Presumption of Safety,” efsa.europa.eu. Cutting-edge fermentation monitoring tools allow for meticulous control over pH, temperature, and microbial activity, guaranteeing product consistency even as production scales up. Such advancements have piqued the interest of private equity firms, leading to a wave of mergers and acquisitions in Europe's bakery sector, as they aim to merge fragmented artisanal operations into unified, scalable entities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price elasticity versus conventional white breads | -1.8% | Eastern Europe, price-sensitive segments across EU | Short term (≤ 2 years) |

| Limited artisanal baker capacity in secondary cities | -1.4% | Secondary cities across Germany, France, Italy | Medium term (2-4 years) |

| Regulatory and labeling constraints | -0.9% | EU-wide, particularly affecting cross-border trade | Long term (≥ 4 years) |

| Volatile rye and speciality-flour costs | -1.2% | Northern Europe, particularly Germany, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Elasticity Versus Conventional White Breads

Sourdough products often carry a 20-40% price premium over regular breads, creating affordability challenges that hinder their appeal to budget-conscious consumers. Between 2019 and 2023, German bakery prices surged by about 33%, with specialty breads facing a steeper inflation, leading to a dip in demand elasticity, as reported by FinanzNachrichten.de. In Eastern Europe, economic constraints limit the uptake of premium breads, as households prioritize essential foods over artisanal options. The widening price gap stems from rising ingredient costs for specialty flours and longer fermentation processes, outpacing inflation for standard bread inputs. In response, retail chains have introduced private-label sourdoughs, aiming to bridge the price gap without compromising on quality, yet these products yield slimmer margins compared to their conventional counterparts. While consumer education on the nutritional and digestibility benefits of sourdoughs helps rationalize the premium pricing, broader market growth hinges on further cost reductions via industrial scaling and enhanced supply chain efficiencies.

Limited Artisanal Baker Capacity in Secondary Cities

Over the past decade, Germany has seen a significant contraction in its bakery sector, losing about 30% of its establishments and resulting in the loss of roughly 20,000 jobs. Meanwhile, France has witnessed a similar trend, with around 25% of its artisanal bakeries vanishing. Labor shortages have exacerbated these capacity challenges; in the Netherlands, nearly half of all bakeries report unfilled vacancies, and over 75% of their staff indicate heightened workloads. Secondary cities face unique challenges in sustaining artisanal bakeries, grappling with lower population densities and diminished demand for premium products, leading to noticeable gaps in sourdough availability. In Germany, the number of bakery apprenticeships has plummeted by half in the last decade, curtailing the influx of skilled artisans essential for sourdough production. Given the intricate nature of sourdough fermentation, which demands specialized knowledge and resists automation, there's a pronounced bottleneck in expanding production capacity. In response, industrial suppliers have rolled out technical support initiatives and streamlined production systems, aiming to lessen skill demands without compromising on product quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Dry Solutions Drive Industrial Adoption

In 2025, dry mix and premix formats dominate the market with a commanding 61.74% share, thanks to their convenience and scalability. Their extended shelf life not only minimizes inventory risks for distributors but also allows for wider geographic distribution without the need for cold chain logistics. Industrial bakeries prefer dry formats due to their consistent fermentation performance and simpler handling, unlike liquid starters that demand temperature control and precise timing. Meanwhile, ready-to-use liquids are on a growth trajectory, boasting a 6.48% CAGR through 2031. These liquid starters are particularly valued in artisanal settings, where their immediate fermentation and flavor depth are crucial. This is especially true for smaller bakeries aiming for authentic sourdough without the hassle of extensive starter upkeep.

Technological advancements in stabilization techniques have bolstered the segment's growth, ensuring microbial viability during dehydration and storage. This consistency in fermentation performance, regardless of environmental conditions, is a boon for manufacturers. Lesaffre's September 2024 launch of Tradizy Durum underscores this trend, introducing an innovative durum-based sourdough system that marries traditional fermentation with industrial reliability. Regulatory factors lean in favor of dry formats, which demand less stringent cold chain oversight and pose reduced microbiological transport risks. Furthermore, the European Food Safety Authority's safety framework, which eases regulatory hurdles for established microbial strains in dried starter production, further propels market expansion.

By Application: Pizza Innovation Accelerates Growth

In 2025, bread and buns applications command a dominant 67.98% market share, underscoring sourdough's deep-rooted ties to artisanal bread-making and the public's affinity for fermented bread products. Yet, it's the pizza crusts and bases that are witnessing the most rapid ascent, boasting a 7.54% CAGR through 2031. This surge is largely attributed to foodservice operators, who are on the hunt for unique offerings that can command a premium in the fiercely competitive restaurant landscape. Sourdough's advantages in pizza applications are manifold: it boasts better dough handling, richer flavor development, and longer holding times, all of which help minimize waste in bustling commercial kitchens. Specialty bakeries, eyeing the premium dessert market, continue to see steady demand for cakes and pastries. Meanwhile, flatbreads and other specialty baked goods are carving out niche spaces, appealing to both ethnic tastes and health-conscious consumers.

The pizza segment's rapid growth mirrors a larger movement in casual and fast-casual dining, where there's a pronounced emphasis on artisanal ingredients and genuine preparation techniques. Sourdough pizza crusts come with operational perks: they boast better freeze-thaw stability and a tolerance for extended fermentation. This means restaurants can prep their bases ahead of time without compromising on quality. Puratos' Sapore product line is making waves, specifically catering to the pizza segment with its high-temperature baking and flavor-enhancing formulations. The surge in this application is further bolstered by the public's perception of sourdough as a healthier choice compared to traditional pizza dough, allowing it to command a premium in health-centric markets. Moreover, in Italy and select European nations, regulatory frameworks championing traditional preparation methods pave the way for genuine sourdough pizza offerings, especially those meeting protected designation standards.

By Distribution Channel: Foodservice Momentum Builds

In 2025, retail channels dominate with a 77.92% market share, underscoring sourdough's robust foothold in supermarket bakeries and specialty food outlets. These outlets cater to health-conscious consumers gravitating towards artisanal choices. Retailers favor sourdough not just for its longer shelf life compared to regular bread, but also for its premium positioning, which boosts their profit margins. Supermarkets and hypermarkets leverage their scale in sourcing and distribution, allowing them to offer competitive prices without compromising on quality, thanks to their established cold chain logistics. Meanwhile, specialty stores focus on premium segments, offering curated sourdough selections and educational insights that foster consumer loyalty. Online retail is also on the rise, appealing to consumers who prioritize convenience and seek direct delivery of artisanal products.

Foodservice is emerging as the fastest-growing distribution channel, boasting a 6.87% CAGR through 2031. This surge is largely attributed to restaurants incorporating sourdough bases, enhancing both their menu diversity and operational efficiency. Sourdough's advantages in commercial kitchens—like longer holding times, better freeze-thaw stability, and richer flavor profiles—bolster its premium pricing. Ingredient suppliers are increasingly turning to sourdough-based solutions, especially for baked goods that demand longevity and consistent quality in large batches. Major producers, represented by the Belgian Federation of Industrial Bakeries, are supplying standardized sourdough products to both retail and foodservice sectors, ensuring they meet commercial standards. Partnerships, like Ulrick & Short's collaboration with Nordmann in early 2025, are broadening the market reach for specialized sourdough ingredients across various channels.

Geography Analysis

In 2025, Germany solidifies its status as Europe's leading sourdough market, commanding a 22.63% share. This dominance is bolstered by a robust consumer affinity for traditionally fermented breads and a significant industrial presence, notably in Saxony-Anhalt, home to one of Europe's largest bake-off facilities operated by Aryzta. The market thrives on well-established distribution channels and a cultural penchant for dense, flavorful breads, a hallmark of sourdough. Yet, Germany's sourdough landscape grapples with challenges: a decade-long 30% drop in bakery operations and pronounced labor shortages hindering artisanal production. Aryzta's commitment to the German market is underscored by its USD 12 million investment in a state-of-the-art stone oven facility in Eisleben, set to be fully operational by H2 2025, even amidst sector consolidation pressures. While prices surged by about 33% from 2019 to 2023, tightening demand elasticity, especially among price-sensitive consumers, the market still sees a viable premium segment for distinct sourdough offerings.

The United Kingdom stands out as the fastest-growing sourdough market in Europe, boasting an 7.91% CAGR projected through 2031. This growth is fueled by a surge in health consciousness and the Federation of Bakers' sourdough code of practice, which has brought much-needed regulatory clarity. Adjustments in the supply chain post-Brexit have not only bolstered domestic sourdough production but also diminished competition from EU imports, now facing new trade barriers. Strong retail collaborations further bolster the UK market, highlighted by Promise Gluten Free's partnerships with retail giants like Tesco, Sainsbury's, Morrisons, Aldi, and Lidl. In a move signaling consolidation trends, Mayfair, via its Ceres Group holding company, has proposed acquiring Pat the Baker and Irish Pride, a decision brought to the attention of Ireland's Competition and Consumer Protection Commission in December 2024. With the UK set to mandate folic acid fortification in December 2026, there's a burgeoning market for fortified sourdough products that align with these nutritional directives.

Italy, France, and Spain, with their deep-rooted cultural ties to traditional fermentation, are witnessing tempered growth rates as they mature and face heightened competition. Italy's dedication to its artisanal bread heritage is evident, with the Ministry of Agriculture highlighting 23 traditional flatbreads, including 2 Protected Geographical Indications and 20 Traditional Agri-food Products, bolstering the sourdough market's evolution. France, despite a robust consumer appetite for traditional products, grapples with a 25% decline in artisanal bakeries, constraining market expansion. Belgium, anchored by Puratos' Sourdough Library and research facilities in Saint-Vith, emerges as a pivotal innovation hub, shaping European sourdough trends. Meanwhile, the Netherlands, Poland, and Sweden present burgeoning opportunities, driven by health-conscious consumers and a rising appetite for premium bakery products, though they necessitate further investment in distribution and consumer education.

Competitive Landscape

In the European sourdough market, moderate fragmentation presents opportunities for both established players and emerging specialists to carve out market share through unique positioning and technological advancements. Leaders like Puratos Group, Aryzta AG, and Lesaffre focus on scaling industrial capabilities, offering technical support, and ensuring product consistency. In contrast, regional artisanal producers leverage their authentic positioning and deep local market insights for a competitive edge.

This competitive landscape illustrates a shift from craft production to industrial scalability. Success hinges on harmonizing traditional fermentation techniques with contemporary manufacturing efficiencies and stringent quality controls. Notable strategic moves include Puratos inaugurating its Sourdough Institute in Belgium in 2024 and curating the world's largest sourdough culture library, boasting 84 unique strains. Meanwhile, Aryzta's USD 12 million plunge into stone oven technology at its Eisleben site underscores how industry stalwarts meld capital investments with artisanal quality, as highlighted by Snack Food & Wholesale Bakery.

Smaller players eyeing the market can find untapped potential in niche areas like gluten-free sourdough, protein-enriched variants, and user-friendly home baking solutions, establishing footholds before larger entities roll out rival products. Mayfair's strategic acquisitions via its Ceres Group underscore the sector's allure, spotlighting its growth trajectory and the allure of consolidation amidst its fragmentation. Companies boasting stringent quality systems and adept regulatory compliance gain an edge, thanks to European Union food safety regulations. At the same time, smaller artisanal producers find favor with the European Food Safety Authority's lenient stance on traditional fermentation methods.

Europe Sourdough Industry Leaders

Puratos Group

Aryzta AG

Lesaffre

IREKS GmbH

Ernst Böcker GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Corbion launched natural mold inhibition solutions specifically designed for sourdough applications, addressing shelf-life challenges while maintaining clean-label credentials required by European retailers and foodservice operators.

- January 2025: Aryzta commissioned its innovation center at the Eisleben facility in Germany, serving as a Group center of excellence for product development with R&D facilities, quality monitoring, and pilot machines for small-quantity production and testing of new baked goods innovations.

- January 2025: IREKS expanded its MONDO LIEVITO MADRE product line to address growing demand for standardized sourdough solutions in both commercial and home baking applications across European markets.

- December 2024: Aryzta began construction of a large-scale 100-ton stone oven line at its Eisleben, Germany site, designed for energy efficiency and sustainability, with full operational capacity scheduled for H2 2025, representing a significant investment in artisanal-quality industrial production.

Europe Sourdough Market Report Scope

Sourdough is naturally leavened bread and does not use commercial yeast to rise. Sourdough bread acts as a prebiotic, which means that the fiber in the bread helps feed the 'good' bacteria in the intestines.

The market is segmented on the basis of application, end user, and geography. The European sourdough market is segmented by application into bread and buns, pizza bases, cakes, and other applications. By end user, the market is segmented into industrial bakeries, foodservice, and retail. By geography, the market is segmented into Spain, the United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts are provided in terms of value in USD million.

By Form

| Ready-to-Use Liquid |

| Dry Mix / Premix |

By Application

| Bread and Buns |

| Pizza Crusts and Bases |

| Cakes, and Pastries |

| Other Applications |

By Distribution Channel

| Food Processing | |

| Foodservice | |

| Retail | Supermarkets / Hypermarkets |

| Specialty Stores | |

| Online Retail | |

| Other Off-Trade Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Form | Ready-to-Use Liquid | |

| Dry Mix / Premix | ||

| By Application | Bread and Buns | |

| Pizza Crusts and Bases | ||

| Cakes, and Pastries | ||

| Other Applications | ||

| By Distribution Channel | Food Processing | |

| Foodservice | ||

| Retail | Supermarkets / Hypermarkets | |

| Specialty Stores | ||

| Online Retail | ||

| Other Off-Trade Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size and growth outlook for Europe’s sourdough sector?

The sector is valued at USD 0.95 billion in 2026 and is set to reach USD 1.25 billion by 2031, reflecting a 5.59% CAGR.

Which European country buys the most sourdough baked goods today?

Germany leads with 22.63% share of regional sales thanks to strong consumer preference for fermented rye and robust industrial capacity.

Where is demand expanding fastest over the next five years?

The United Kingdom shows the quickest growth, projected to advance at an 7.91% CAGR through 2031 on the back of health-driven consumption and clear labeling rules.

Why do dry mixes dominate commercial sourdough production?

Dry mixes hold 61.74% share because they offer long shelf life, easy transport without cold chain, and consistent fermentation control for large bakeries.

What is the key driver behind pizza-crust adoption of sourdough?

Foodservice operators favor sourdough crusts for richer flavor and extended holding times, pushing pizza applications to a 7.54% CAGR through 2031.

Page last updated on: