Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.71 Billion |

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 4.74 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

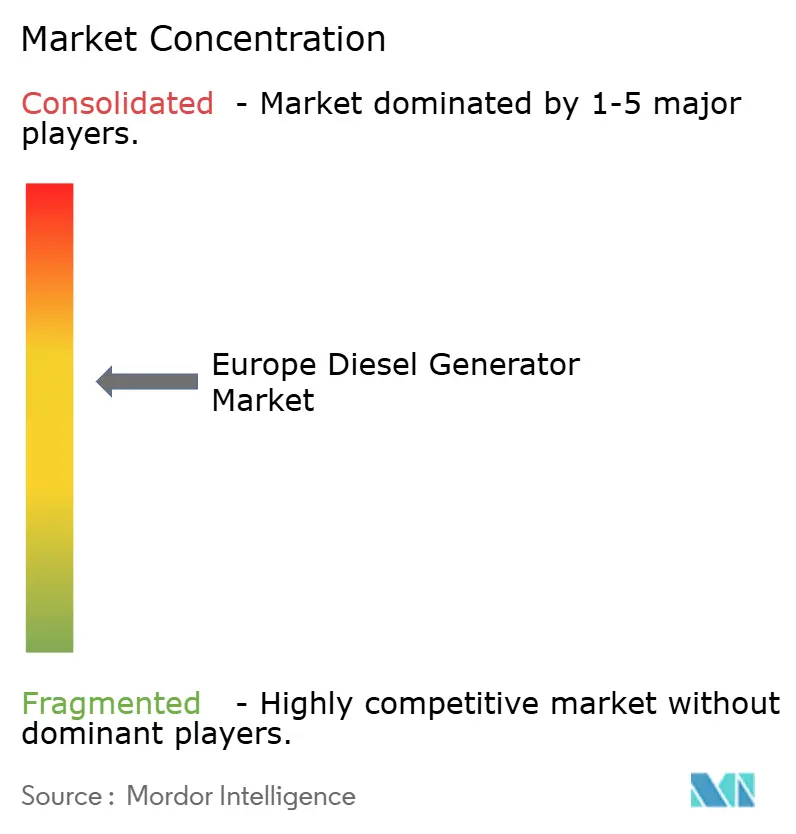

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Diesel Generator Market Analysis by Mordor Intelligence

The Europe Diesel Generator Market size is expected to grow from USD 3.71 billion in 2025 to USD 3.87 billion in 2026 and is forecast to reach USD 4.74 billion by 2031 at 4.18% CAGR over 2026-2031.

Grid reliability concerns, NATO-linked resilience rules, and surging data center construction are the strongest demand catalysts. Standby units dominate 2024 revenue, yet rising microgrid adoption is lifting prime-power sales and lengthening duty cycles. Generator rental penetration continues to expand as contractors favor pay-per-use fleets that bundle Stage V diesel sets with battery modules, reducing fuel bills and noise. Incumbent engine makers are upgrading their product lines for HVO100 compatibility to defend their market share while meeting the looming Stage VI emission caps. Structural headwinds stem from cheaper batteries and stringent exhaust rules, but hybrid diesel-battery systems are mitigating the impact.

Key Report Takeaways

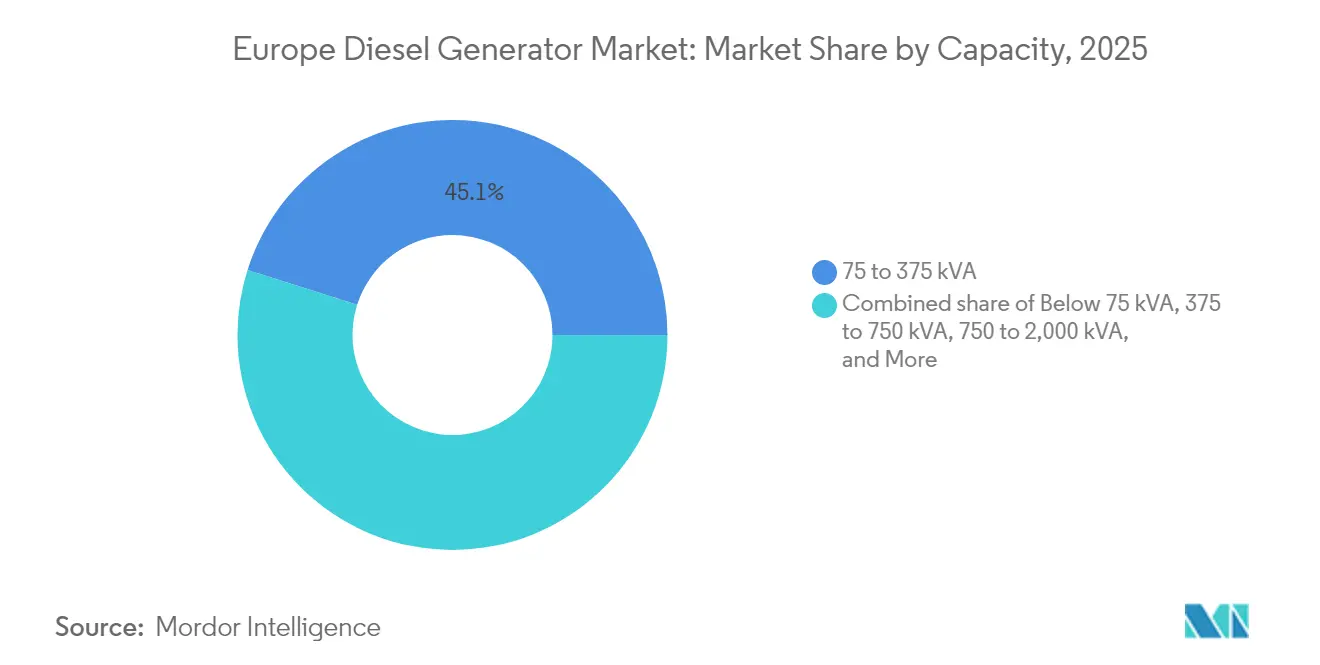

- By capacity, the 75-to-375 kVA tier commanded 45.12% of the European diesel generator market share in 2025; the 375-to-750 kVA class is forecast to expand at a 6.80% CAGR through 2031.

- By application, standby and backup captured 68.25% of the revenue in 2025, while prime and continuous duty are growing at a 6.52% CAGR to 2031.

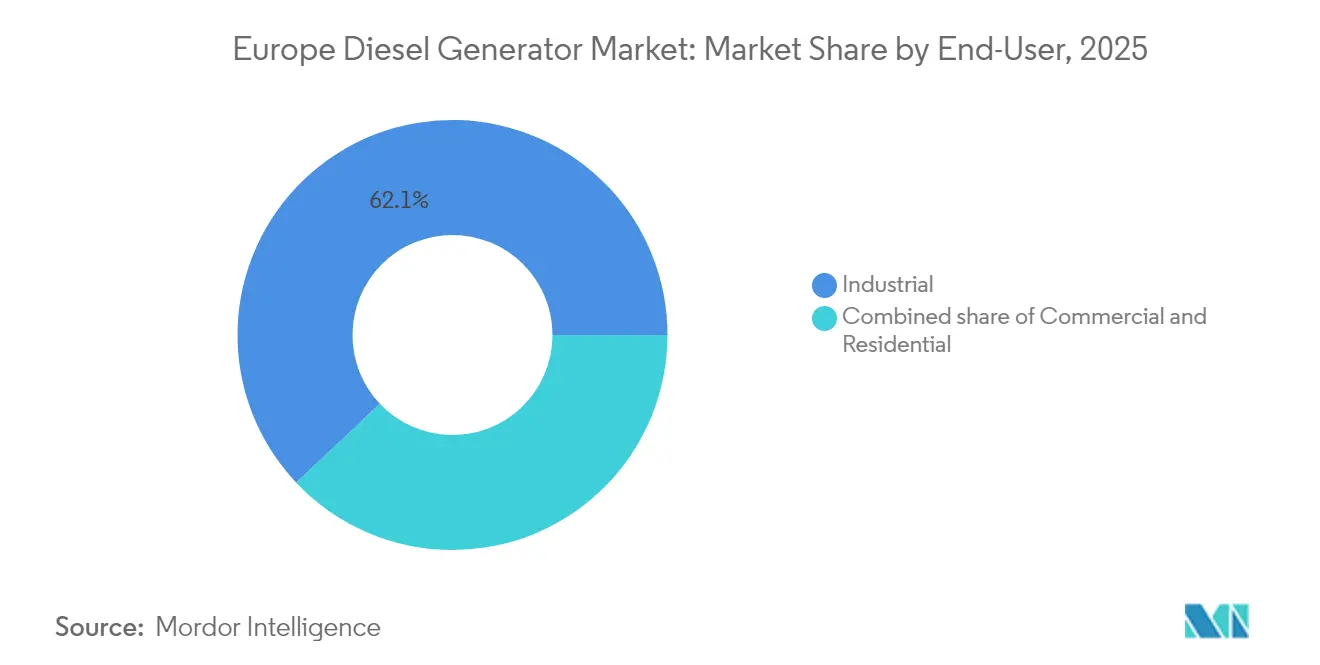

- By end user, industrial facilities held 62.05% of 2025 demand; commercial deployments are advancing at a 6.98% CAGR over the outlook.

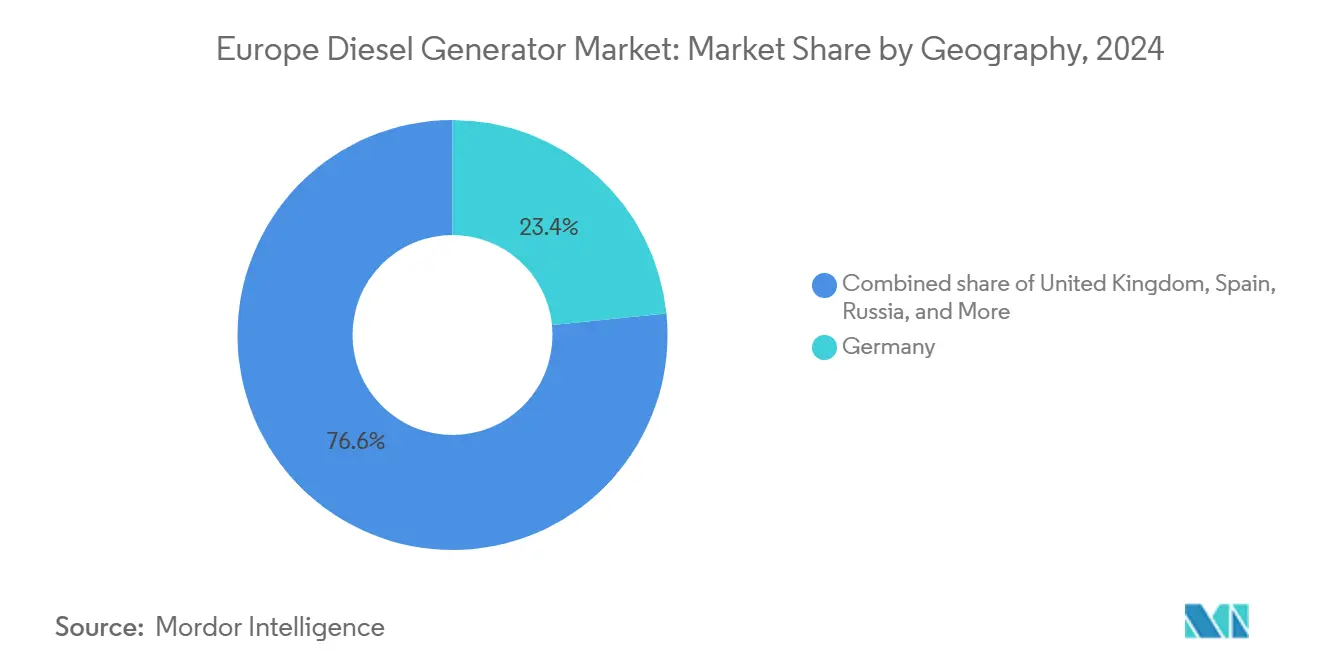

- By geography, Germany led with 23.10% of 2025 revenue, whereas Russia posted the fastest CAGR at 6.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Diesel Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-outage driven standby demand surge | +1.2% | Germany, UK, Nordics, with spillover to France and Benelux | Short term (≤ 2 years) |

| Industrial & commercial capacity expansion | +0.9% | Germany, France, Italy, Spain, Poland | Medium term (2-4 years) |

| Growth in generator-rental ecosystem | +0.7% | UK, Germany, France, Benelux, Nordics | Medium term (2-4 years) |

| Stage-V retrofit boom (2027–2029) | +0.6% | EU-27 countries, with highest uptake in Germany, France, Netherlands | Long term (≥ 4 years) |

| NATO energy-security stockpiles | +0.4% | NATO member states, concentrated in Germany, Poland, Baltics, UK | Medium term (2-4 years) |

| Residential back-up adoption (sub-75 kVA) | +0.3% | Spain, Italy, rural France, Greece, with limited urban penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Outage Driven Standby Demand Surge

Fourteen member states face capacity shortfalls in the 2024-2025 winter outlook, prompting hospitals, data centers, and telecom towers to secure new standby sets.(1)European Network of Transmission System Operators for Electricity, “Winter Outlook 2024-2025,” entsoe.eu The United Kingdom alone installed 1,200 hospital backup units in 2024 to satisfy a 72-hour autonomy rule.(2)NHS England, “Resilience Standards for Healthcare Facilities,” england.nhs.uk After the Baltic Sea cable sabotage, mobile gensets were dispatched to remote cell sites once fed only by the grid, underscoring how security threats convert into immediate equipment orders. Manufacturers have responded with automatic transfer switches that start within ten seconds to protect critical loads. This surge keeps the European diesel generator market at the forefront of emergency-power planning across the continent.

Industrial and Commercial Capacity Expansion

New semiconductor fabs, mixed-use towers, and logistics hubs require multi-megawatt contingencies that conventional grids cannot always guarantee.(3)Intel Corporation, “Magdeburg Semiconductor Fab Investment,” intel.com With every cleanroom spin valued in the millions, voltage dips are intolerable, so developers specify redundant diesel arrays during design. Paris and Milan high-rises are similarly pre-installing 200 to 500 kVA sets to secure lift and HVAC uptime. Because these projects lock in long-run demand, the European diesel generator market gains durable revenue streams even as operating profiles evolve toward hybrid duty.

Growth in Generator-Rental Ecosystem

Rental penetration increased to 38% in 2024, up seven percentage points since 2020.(4)European Rental Association, “Rental Market Report 2024,” erarental.org Aggreko grew European temporary-power sales 14% by pairing Stage-V units with battery packs that trim fuel use 30%, an approach well-received at Spanish wind-farm sites. Atlas Copco’s hybrid fleet matches this model, targeting projects that last weeks rather than days. OpEx models fit tight construction budgets and bypass emission-compliance paperwork, strengthening market stickiness.

Stage-V Retrofit Boom

EU Regulation 2016/1628 sets a January 2027 deadline for new Stage-V-compliant gensets and a 2029 switch for rental fleets. Retrofit kits priced between EUR 8,000 and EUR 15,000 prompt owners to opt for early replacement, thereby swelling OEM order books to 18-month lead times. Makers offering plug-and-play exhaust after-treatment enjoy clear pricing power. This retrofit wave is forecast to lift the European diesel generator market through the late decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewables + storage displacement | -0.8% | Germany, UK, Spain, Denmark, Netherlands | Medium term (2-4 years) |

| Stricter EU Stage V/VI emission caps | -0.5% | EU-27 countries, with highest compliance costs in urban Germany, France, Italy | Long term (≥ 4 years) |

| Bio-/eFuel & hybrid microgrid shift | -0.3% | Sweden, Finland, Netherlands, Denmark, Germany | Medium term (2-4 years) |

| Urban noise-ordinance bans (>90 dB) | -0.2% | Urban centers in Germany, France, Italy, UK, Spain, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renewables plus Storage Displacement

Battery energy-storage installations hit 9.2 GW in 2024, with 4-hour discharge systems now beating diesel variable costs in many markets. Data centers in Frankfurt and Amsterdam cut genset runtime by up to 70% by shifting short outages to lithium-ion banks. Residential and small commercial users with capacities below 200 kVA are adopting rooftop solar plus batteries, reducing demand for portable diesel. Price declines below EUR 150 per megawatt-hour put further pressure on traditional standby sets. Nonetheless, diesel remains the only economical choice for multi-day outages, which preserves a baseline for the European diesel generator market.

Stricter EU Stage V/VI Emission Caps

Stage VI rules proposed for 2028 will lower nitrogen-oxide limits to 0.4 g/kWh and impose real-world testing. Compliance adds EUR 12,000-20,000 per unit, raising barriers for small owners. Acoustic ordinances in major cities also require enclosures, which can increase project costs by up to 25%. These layers accelerate interest in HVO drop-in fuels, which slash particulates by 80% without hardware changes. While the rules temper growth, they also drive a shift toward premium hybrid and biofuel-ready models, supporting value in the European diesel generator market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Mid-Range Leads While High-Power Gains Pace

The 75-to-375 kVA band accounted for 45.12% of 2025 revenue, thanks to strong uptake in retail chains and municipal treatment plants. Rental fleets also favor this range because it strikes a balance between transport weight and fuel efficiency. Sub-75 kVA sets remain common on job sites, yet they face substitution from solar-battery combinations in subsidized markets. Above-750 kVA units serve oil refineries and mines that lack economical grid feeders, with Wärtsilä containerized modules delivering 20-MW blocks to Arctic locales.

Hybrid demand converges on 150-to-300 kVA, where batteries smooth load spikes and reduce fuel burn by roughly one-third. Stage-V rules accelerate turnover in the 200 to 500 kVA cohort, as pre-2019 engines prove cost-prohibitive to retrofit. Together, these mechanics underpin sustained volume in this core tranche of the European diesel generator market.

By Application: Standby Dominates Yet Prime-Power Accelerates

Standby arrays captured 68.25% of 2025 sales, especially in data centers and hospitals where 10-second start and 72-hour autonomy are mandated. Shorter outages are shifting toward batteries, but diesel still anchors compliance. Peak shaving remains a modest 7.00% slice, yet demand charges above EUR 100 per kW each month in Germany encourage factories to operate generators during grid peaks.

Prime-power units, which account for only 24.75% of the total in 2025, are projected to grow 6.52% annually through microgrids on islands and remote mines. OEMs now certify engines for HVO100 to address carbon targets at these sites. These developments expand the operational palette and increase the European diesel generator market size across various duty profiles.

By End User: Industrial Share Holds While Commercial Rises

Industrial plants consumed 62.05% of gensets in 2025, anchored by statutory backup obligations for high-load facilities. Cement, steel, and chemical operators regard diesel reliability as non-negotiable.

Commercial projects exhibit the fastest growth rate of 6.98%, fueled by hyperscale data hubs in Frankfurt, Amsterdam, and Dublin. Hospitals, telecom towers, and 5G cell sites add further tailwinds across the European diesel generator market.

Geography Analysis

Germany supplied 23.10% of 2025 revenue due to its export-heavy manufacturing base and stringent grid-code backup mandates. Intel’s EUR 30 billion Magdeburg fab alone booked multi-megawatt contingencies to avert wafer loss. Data centers in Frankfurt added 450 MW of standby capacity that same year. Renewable penetration above 55% increases the risk of intermittency, keeping diesel embedded even as battery capacity grows.

Russia is projected to show the highest 6.32% CAGR through 2031, as sanctions drive energy self-sufficiency and oil-field electrification, favoring localized engine supply. Domestic brands fill gaps left by export controls while Arctic oil projects order containerized gensets rated for extreme cold.

The United Kingdom accounts for 16.00% of the 2025 spend, led by London and Manchester colocation hubs with 99.99% uptime guarantees. France relies on backup sets during reactor maintenance cycles, sustaining regional demand near Lyon and Marseille. Italy and Spain combine for 19.00% share, where tourism and construction rebound fuel portable rentals. The Nordics hold 11.00% thanks to off-grid mines and island microgrids that rely on diesel safety nets. Benelux claims 8% growth in data centers and logistics near Rotterdam and Amsterdam. Remaining Central and Eastern markets advance 5.8% per year as EU funds and 5G rollout lift tower backup needs

Competitive Landscape

The top five suppliers, Caterpillar, Cummins, Rolls-Royce Power Systems, Kohler-SDMO, and Aggreko, collectively held about 48% revenue in 2024, pointing to moderate concentration. Each invests in Stage V engines and HVO certification to comply with EU regulations, while marketing hybrid packs that reduce runtime by 30% in urban areas. Aggreko and Atlas Copco increase share by bundling storage with rentals, an offering that undercuts ownership for multi-week jobs.

The technology race centers on emission compliance and digital diagnostics. Cummins’ Connected Diagnostics suite monitors 12,000 European sets for predictive maintenance, lowering unplanned outages. Rolls-Royce promotes MTU EnergyPack hybrids to hospitals and telecom towers, with a noise level cap of 90 dB.

Challengers such as AKSA and Pramac target price-sensitive segments with Stage-V sets priced up to 20% lower than those of Western rivals. Anticipated Stage VI rules are expected to widen compliance cost gaps and may spur additional consolidation within the European diesel generator market.

Europe Diesel Generator Industry Leaders

Caterpillar Inc

Cummins Inc

Rolls-Royce Power Systems (MTU)

Kohler-SDMO

Aggreko PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cummins has allocated EUR 45 million to expand its Daventry, UK, plant for Stage VI and hydrogen-dual-fuel gensets.

- December 2024: Aggreko won a £120 million temporary power award from Network Rail, pairing diesel and battery hybrids that cut runtime by 40%.

- November 2024: Rolls-Royce introduced the 1.5 MW mtu EnergyPack QG hybrid for urban data centers and hospitals.

- October 2024: Caterpillar upgraded its Kiel line to produce HVO100-ready C18 and C32 engines.

- September 2024: Kohler-SDMO acquired Spain’s Grupel to add 200 to 750 kVA of rental capacity.

- August 2024: Wärtsilä secured a EUR 65 million contract for 48 MW of modular diesel backup serving Norwegian offshore platforms.

Europe Diesel Generator Market Report Scope

A diesel generator is a mechanical-electrical machine that produces electrical energy (electricity) from diesel fuel. A diesel generator can be used as an emergency power supply in case of power cuts or in places where there is no connection to the power grid.

Capacity, end user, and geography are the market segments for diesel generators in Europe. By capacity, the market is segmented into below 75 kVA, 75-350 kVA, and above 350 kVA. By end-user, the market is segmented into residential, commercial, and industrial. By geography, the market is segmented into Germany, Russia, United Kingdom, Norway, and the Rest of Europe. The report offers the market size and forecasts for non-stick coatings in terms of revenue (USD) for all the above segments.

By Capacity (kVA)

| Below 75 kVA |

| 75 to 375 kVA |

| 375 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

By Application

| Stand-by/Backup Power |

| Prime/Continuous Power |

| Peak-shaving/Load Management |

By End User

| Residential |

| Commercial |

| Industrial |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Capacity (kVA) | Below 75 kVA |

| 75 to 375 kVA | |

| 375 to 750 kVA | |

| 750 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Application | Stand-by/Backup Power |

| Prime/Continuous Power | |

| Peak-shaving/Load Management | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe diesel generator market?

The Europe diesel generator market size was USD 3.87 billion in 2026 and is set to reach USD 4.74 billion by 2031.

Which capacity range sells the most units across Europe?

Sets rated 75-to-375 kVA led 2025 revenue, accounting for 45.12% share due to strong demand from retail chains and mid-sized factories.

Why are rental diesel generators gaining popularity?

Rental fleets let users avoid capital outlay and emission-compliance paperwork, while new hybrid models lower fuel consumption by around 30%.

How will Stage VI rules affect buyers?

Stage VI will mandate expensive after-treatment systems from 2028, adding up to EUR 20,000 per unit and accelerating fleet renewal toward compliant or hybrid models.

What fuels are emerging alternatives to conventional diesel?

Hydrotreated vegetable oil (HVO100) is the leading drop-in option, delivering up to 90% particulate reduction without engine modifications.

Which country is projected to grow fastest through 2031?

Russia shows the highest forecast CAGR at 6.32%, driven by localized energy infrastructure and oil-field electrification needs.

Page last updated on: