Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

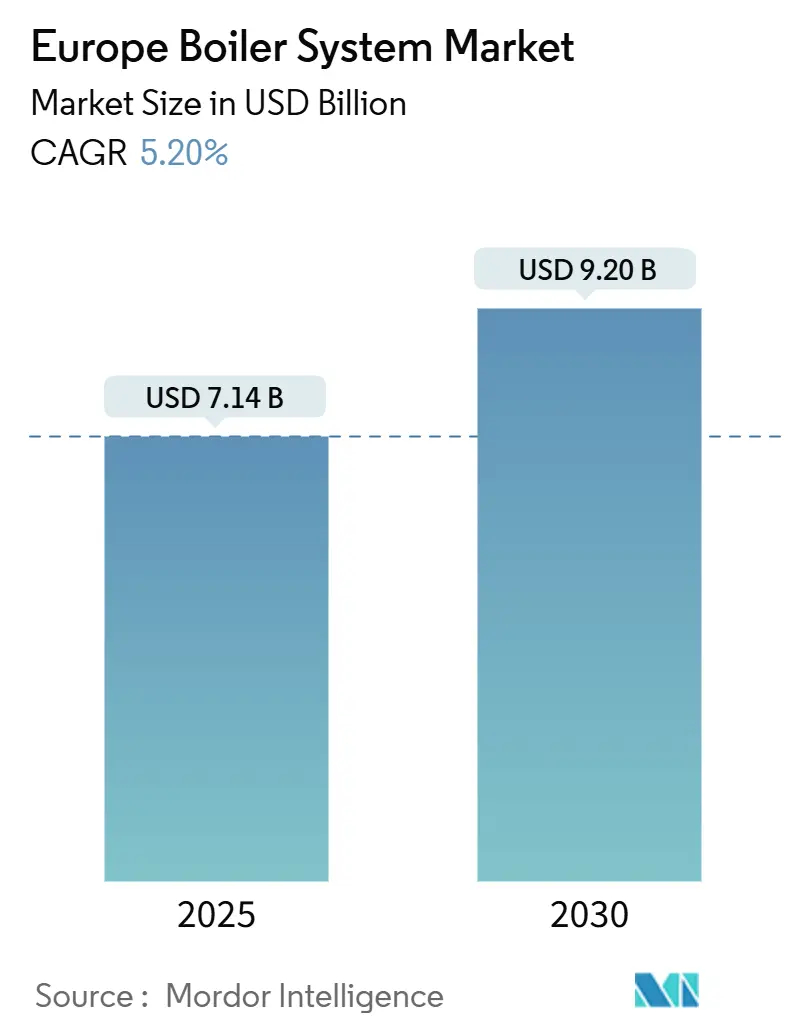

| Market Size (2025) | USD 7.14 Billion |

| Market Size (2030) | USD 9.20 Billion |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Boiler System Market Analysis by Mordor Intelligence

The Europe boiler system market size is estimated at USD 7.14 billion in 2025 and is projected to reach USD 9.20 billion by 2030, reflecting a 5.20% CAGR. The growth path is underpinned by strict European Union energy performance mandates, rising building renovation activity, and aggressive decarbonization targets that collectively accelerate technology refresh cycles. Condensing and hydrogen-ready designs are gaining ground because they meet tightening lifecycle emissions thresholds, while smart controls unlock additional fuel savings through demand-responsive operation. Operators weigh carbon-pricing trajectories when planning capital projects, and many defer large fossil-fuel upgrades in favor of modular electrification that can migrate to green generation over time. Regional implementation differences still shape technology uptake; Western European nations enforce higher efficiency baselines, whereas cost-conscious Eastern markets adopt incremental improvements first. Nevertheless, the overarching policy direction remains uniform—phase out aging, high-emission assets, and replace them with connected, future-fuel-compatible solutions that lower the total cost of ownership.

Key Report Takeaways

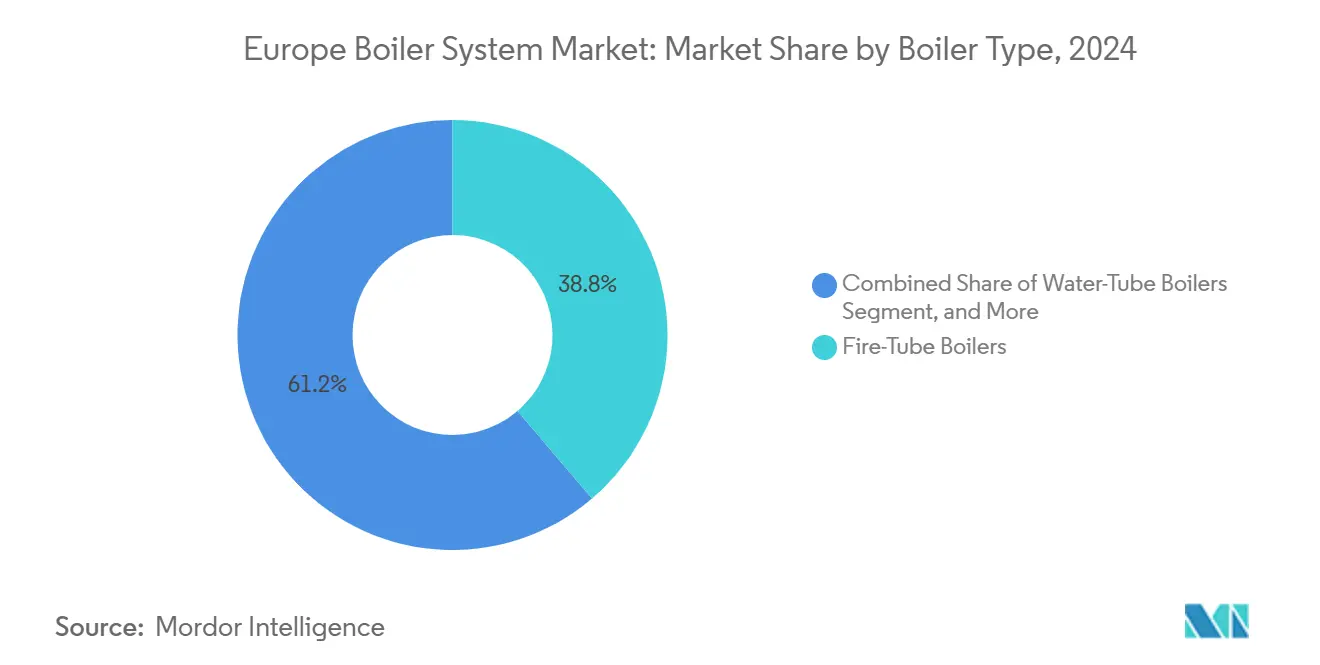

- By boiler type, fire-tube designs captured 38.76% of the Europe boiler system market share in 2024, while electric units are forecast to expand at a 6.23% CAGR through 2030.

- By fuel type, natural gas accounted for 47.91% of the Europe boiler system market size in 2024; hydrogen-blend solutions posted the fastest growth at a 6.11% CAGR from 2024 to 2030.

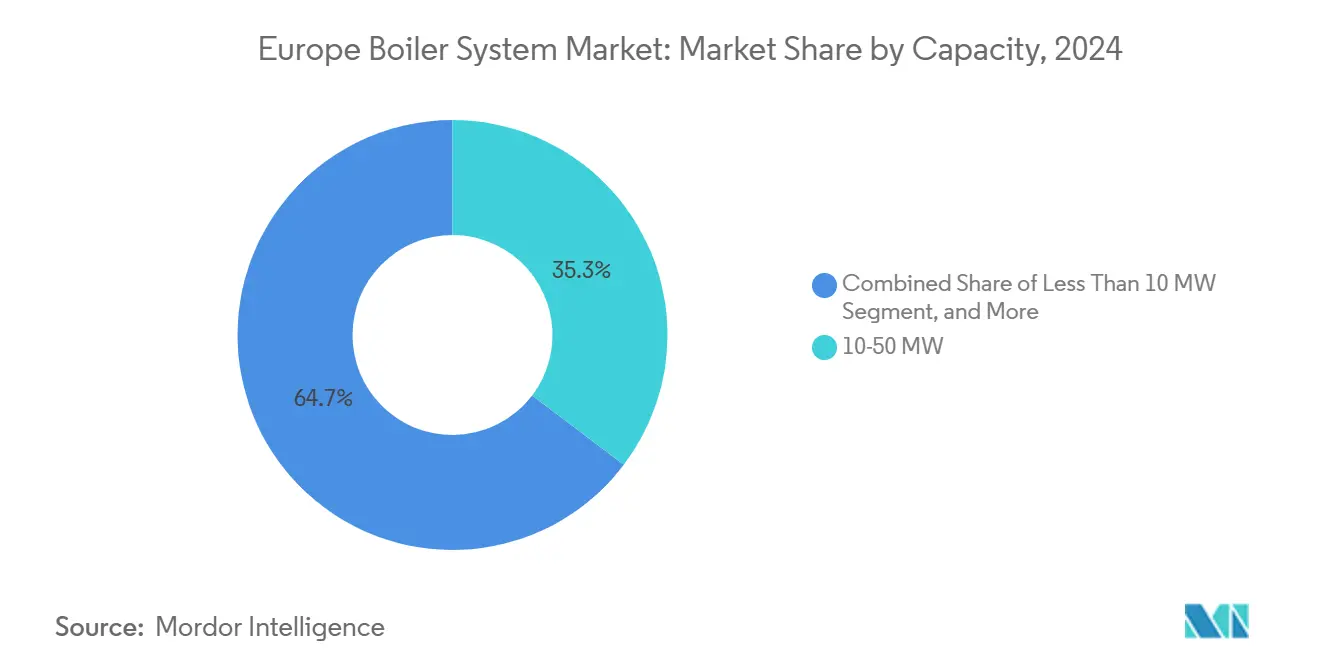

- By capacity, the 10-50 MW segment led with a 35.32% revenue share in 2024; however, systems below 10 MW are projected to advance at a 6.37% CAGR during the same period.

- By end-user, residential installations accounted for a 42.66% share of the Europe boiler system market size in 2024, whereas industrial demand is projected to show the highest CAGR at 6.89%.

- By country, Germany commanded 23.13% of 2024 revenue, while Spain is expected to record a 5.33% CAGR through 2030.

Europe Boiler System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Energy Efficient Heating Systems | +1.2% | EU-wide, strongest in Germany, Netherlands, Denmark | Medium term (2-4 years) |

| Technological Advancements in Heating Equipment | +0.9% | Global, concentrated in Western Europe manufacturing hubs | Long term (≥ 4 years) |

| Government Incentives for Low-Carbon Heating | +0.8% | National programs across EU, varying intensity by country | Short term (≤ 2 years) |

| Aging Boiler Fleet Replacement Demand | +0.7% | EU-wide, particularly acute in Eastern Europe | Medium term (2-4 years) |

| Emergence of Heat-as-a-Service Business Models | +0.4% | Early adoption in UK, Germany, Netherlands | Long term (≥ 4 years) |

| Hydrogen-Ready Boiler Deployment Targets | +0.3% | Concentrated in hydrogen valley regions, North Sea countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Energy-Efficient Heating Systems

EU building-performance legislation obliges member states to reduce their average primary energy use by 16% by 2030 and up to 22% by 2035, triggering a broad replacement push toward condensing assets that routinely deliver efficiencies above 95%.[1]European Parliament, “Buildings: MEPs Adopt Plans to Reduce Energy Consumption and Emissions,” europarl.europa.eu Municipal networks are installing high-output condensing modules on district grids, enabling operators to modulate flow and reduce seasonal fuel fluctuations. Manufacturers respond to the policy signal with bundled solutions that combine boilers, thermal storage, and solar thermal collectors under a single control platform that orchestrates load shifting against real-time tariff feeds. Industrial plants achieve rapid payback by exploiting continuous-load profiles; cost avoidance from gas savings offsets the premium of hardware within three to five heating seasons. The efficiency mandate also fuels innovation in flue-gas-recapture devices that reclaim latent heat, raising overall system returns to near-heat-pump levels without requiring wholesale site redesign.

Technological Advancements in Heating Equipment

Europe’s push for a hydrogen economy accelerates rollout of boilers certified for 100% H₂ operation from 2025, led by Viessmann’s commercial range.[2]Viessmann, “Viessmann Presents Multibrand Strategy at ISH 2025,” viessmann.com Coupled smart controllers integrate weather forecasts and occupancy analytics, trimming runtime hours while protecting comfort. Electric units merge with high-temperature heat pumps and on-site battery storage to capitalize on renewable-heavy grid windows, and modular layouts enable plants to stack 250 kW cartridges until demand peaks, then scale back without incurring efficiency penalties. Biomass innovations focus on auger-fed combustion and auto-cleaning heat exchangers, improving uptime for variable-quality pellets. Across categories, predictive-maintenance algorithms utilize vibration and flue-gas data to prevent service interruptions and reduce unplanned outages, a crucial requirement for process-critical industrial lines.

Government Incentives for Low-Carbon Heating

Direct subsidies spur immediate procurement decisions: the United Kingdom’s Boiler Upgrade Scheme reimburses up to GBP 7,500 (USD 9,375) per qualified installation, and Germany earmarks EUR 13.5 billion (USD 14.9 billion) through 2030 for equipment swaps with bonus rates reaching 70% for hydrogen-ready devices.[3]UK Government, “Check If You May Be Eligible for the Boiler Upgrade Scheme,” gov.uk EU Innovation Fund grants underwrite demonstration-scale industrial conversions that derisk early adoption. Tax credits complement cash transfers, allowing small firms to amortize premium technology without eroding their cash flow. Geographic asymmetry in incentive value prompts clusters of activity, as neighboring businesses coordinate bulk purchases, negotiate installer discounts, and share commissioning expertise to compress project timelines.

Aging Boiler Fleet Replacement Demand

Roughly 40% of installed European boilers exceed the 15-year service threshold. Maintenance budgets swell, and unscheduled downtime jeopardizes production continuity, pushing facilities to pre-empt catastrophic failure. Regulatory phase-outs of non-condensing models tighten upgrade windows, causing periodic installation bottlenecks and labor shortages. Commercial landlords target certification milestones, recognizing that outdated systems depress asset valuations and deter prospective tenants seeking green-building credentials. Eastern European states confront the sharpest curve because legacy Soviet-era plants now breach emission caps; Western suppliers exploit first-mover advantage, supplying turnkey kits plus operator training to navigate standards unfamiliar to local technicians.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Emission Regulations Tightening Boiler Standards | -0.6% | EU-wide, varying enforcement intensity by member state | Short term (≤ 2 years) |

| High Upfront Capital Expenditure for Condensing Boilers | -0.4% | Particularly acute in Eastern Europe, SME segments | Medium term (2-4 years) |

| Skilled Labour Shortage in Advanced Boiler Installation | -0.3% | Germany, Netherlands, UK with highest shortage intensity | Medium term (2-4 years) |

| Volatility in EU Carbon Prices Delaying Investments | -0.2% | Industrial segments across EU, concentrated in carbon-intensive sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Emission Regulations Tightening Boiler Standards

Successive updates to the EU Ecodesign Directive ratchet NOx ceilings and energy-label thresholds, inflating R&D costs and prolonging conformity assessment cycles. Different member-state test regimens obstruct seamless product rollout and raise inventory-holding risk. Industrial operators weigh retrofits against full replacements but often pause investment until the final rule language is clarified, slowing order books for large-capacity fabricators.

High Upfront Capital Expenditure for Condensing Boilers

Premium pricing, combined with venting and drainage retrofits, stretches payback periods beyond the five-year horizon acceptable to many small and medium-sized enterprises. Eastern European installers face additional financing barriers as local credit costs remain above Western averages. Even when fuel-saving math is clear, cash-constrained owners prolong the life of atmospheric units, thereby diluting near-term demand and pressuring vendors to introduce leasing or heat-as-a-service options that shift costs from CAPEX to OPEX.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Boiler Type: Electric Systems Drive Technology Transition

Fire-tube units retained 38.76% of 2024 revenue, but electric variants deliver the highest momentum with a 6.23% CAGR. This advance reflects corporate electrification agendas, grid-balancing incentives, and falling renewable power costs that narrow the operational expense gap. Many plants adopt hybrid layouts, pairing existing gas shells with resistive banks that absorb surplus solar output in shoulder seasons. Performance data underpin management decisions; continuous monitoring demonstrates that hybrid stacks achieve CO₂ emissions per megawatt-hour below internal targets without compromising steam quality.

Across Western Europe, industrial campuses link electric modules to campus microgrids equipped with wind and solar energy, allowing for the on-site consumption of self-generated kilowatt-hours during peak production. Modular skids simplify phased expansions, allowing owners to add 500 kW blocks for incremental capacity rather than overspecifying a 10 MW shell. The controller firmware adjusts firing sequences to exploit intraday electricity price troughs, and automatic duty cycling lengthens the service life of the legacy fire-tube stages.

By Fuel Type: Hydrogen Blend Systems Signal Future Direction

Natural gas dominated with a 47.91% share, thanks to its pervasive pipeline networks, transparent spot pricing, and installer familiarity. Even so, hydrogen-blend lines score a 6.11% CAGR, driven by the European Hydrogen Backbone initiative, which aims to upgrade transmission corridors for 20% H₂ blends by mid-decade. Viessmann’s portfolio shift to boilers that tolerate incremental hydrogen percentages de-risks customer investment, as the equipment installed today will meet future fuel rules without requiring swaps.

Pilot projects in the Netherlands and Germany report stable combustion dynamics at 30% blends, easing safety concerns and accelerating regulatory approvals. Industrial complexes co-located with electrolyzers integrate direct hydrogen streams, sidestepping grid fees. In Spain, utilities tender combined heat and power contracts that stipulate hydrogen readiness to ensure compliance with 2030 emission quotas. Oil-fired and biomass niches persist in off-grid locations, yet even these applications explore synthetic fuel blends and waste-heat capture as a means of mitigating supply volatility.

By Capacity: Small-Scale Systems Capture Distributed Demand

The 10-50 MW bracket led at 35.32% in 2024, catering to mid-size district heat loops, university campuses, and light-industry clusters. Below-10 MW packages grow at the fastest rate of 6.37% as electrified and modular concepts permeate multifamily housing and craft-scale manufacturing. Decentralized plants curtail transmission losses and qualify for feed-in tariffs when integrated with rooftop photovoltaics, improving owner economics.

Heat-as-a-service operators target these smaller nodes, deploying fleets of standardized 1.5 MW modules monitored from central control rooms. Predictive analytics schedule maintenance when spare capacity exists elsewhere in the network, maximizing uptime while reducing technician mileage. In the heavy industry, giants exceeding 100 MW remain essential for chemical crackers and paper mills. Yet, even in these settings, managers subdivide capacity into modular clusters that can gradually shift to green fuels without a single-point failure scenario.

By End-User: Industrial Sector Leads Growth Acceleration

Residential stock still accounts for 42.66% of installed value, but industrial demand moves ahead at a 6.89% CAGR. Energy-intensive sectors face annual increases in EU Emissions Trading System costs, making high-efficiency or hydrogen-ready assets pivotal to maintaining margins. Continuous-process lines for food sterilization, pharmaceuticals, and metals annealing embrace electrification to achieve tighter temperature windows and shorter ramp-up times, thereby reducing scrap rates.

Commercial landlords, by contrast, stage upgrades primarily at lease break junctures when tenant improvement budgets are active. They prefer condensing gas systems supplemented with air-source heat pumps to secure BREEAM or LEED badges that enhance rental premiums. Data-center operators blend redundant gas and electric boilers to fulfill winter-peak heating plus year-round humidity control duties, while tapping waste-server heat for neighboring greenhouses.

Geography Analysis

Germany retains its leadership position with a 23.13% share in 2024, owing to its sizable industrial load, high renovation rates, and an EUR 13.5 billion incentive pool that reimburses up to 70% of hydrogen-ready installations. Federal building codes mandate low-NOx stacks and minimum seasonal efficiency thresholds, accelerating change-outs in office retrofits and public infrastructure. Manufacturers use home-market credibility to export turnkey packages across Central Europe, reinforcing scale economies and domestic employment.

Spain posts the fastest climb at 5.33% CAGR as its National Energy and Climate Plan channels subsidies toward electrified and renewable-heat options. Residential rebates reaching 70% of device cost unleash bulk procurement waves each quarter; regional installers struggle to satisfy demand, prompting consolidation and joint ventures with equipment suppliers. Mediterranean grid profiles rich in solar generation offer lower time-of-use electricity tariffs midday, encouraging the installation of electric and hybrid boilers that capitalize on the abundant supply.

Eastern Europe’s aging stock represents a latent boom. Poland and the Czech Republic replace Soviet-era coal and oil stacks with condensing gas units tied to expanding pipeline grids, drawing on EU cohesion funds. Nordic states enhance already-robust district loops by adding large hydrogen-ready blocks that enable seasonal fuel switching between biogas, excess wind power, and future synthetic methane. Diverse regulatory tempos across the continent require vendors to maintain multicountry certification arsenals and localized sales engineering to interpret constantly shifting compliance bulletins.

Competitive Landscape

The Europe boiler system market features moderate concentration. Vaillant Group, Robert Bosch, Viessmann Climate Solutions, and BDR Thermea collectively supply a broad range of technologies from 15 kW wall-hung residential combis to 2 GW district plant trains offering multi-brand coverage that aligns with varied price points. Competitive intensity spikes around condensing and hydrogen-ready models where regulatory hurdles deter smaller entrants. Vendors allocate 5-8% of their annual revenue to R&D, prioritizing burner redesigns, control logic upgrades, and materials capable of withstanding hydrogen embrittlement.

Strategic moves tilt toward vertical integration and recurring-revenue models. Heat-as-a-service contracts bundle asset finance, fuel procurement, and predictive maintenance into per-megawatt-hour fees, thereby smoothing cash flow for end-users and locking in multi-year relationships. Bosch expands its IoT suite by embedding edge analytics gateways that push real-time diagnostics to cloud dashboards, trimming onsite service calls by 30%. BDR Thermea’s EUR 50 million Netherlands expansion doubles hydrogen-ready output, meeting 2025 tender requirements in North Sea energy valleys.

Mergers and acquisitions reshape supply chains. Carrier Global’s EUR 12 billion takeover of Viessmann Climate Solutions boosts scale and unites complementary portfolios spanning hydronic distribution, pumps, and digital controls. Boccard’s Leroux Lotz acquisition augments its capabilities in high-pressure industrial spheres. Adaptive capacity investments reflect anticipation of a mid-decade spike in hydrogen-compatible demand once corridor infrastructure matures across Belgium, Germany, and Denmark.

Europe Boiler System Industry Leaders

Daikin Industries Ltd.

Robert Bosch GmbH

Mitsubishi Electric Europe B.V.

Danfoss A/S

Vaillant Group GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Vaillant Group launched a cloud-based predictive-maintenance platform that integrates with its commercial boiler portfolio and guarantees 98% fleet uptime under new service-as-a-subscription contracts.

- July 2025: BDR Thermea partnered with Gasunie to pilot a 100% hydrogen district heating project in the Netherlands, installing three 15 MW boilers that will feed a municipal network by winter 2026.

- April 2025: Bosch began construction of a EUR 85 million (USD 92 million) hydrogen-ready boiler manufacturing line in Bavaria, targeting a 2026 start-up capacity of 120,000 units per year.

- February 2025: Viessmann unveiled a compact hydrogen-ready residential boiler rated at 20 kW that achieves 99% seasonal efficiency and is scheduled for mass production in Q4 2025.

Europe Boiler System Market Report Scope

Heating equipment is equipment designed to supply heat for different operations and is used in various residential, commercial, and industrial applications, which include boilers, radiators, heat pumps, and other applications. The industrial end-users include food and beverage, oil and gas, pharmaceutical, chemical industries, etc.

The Europe Boiler System Market Report is Segmented by Boiler Type (Fire-Tube Boilers, Water-Tube Boilers, Electric Boilers, Condensing Boilers), Fuel Type (Natural Gas, Oil, Biomass, Electric, Hydrogen Blend), Capacity (Less Than 10 MW, 10-50 MW, 51-100 MW, Above 100 MW), End-User (Residential, Commercial, Industrial), and Geography (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

By Boiler Type

| Fire-Tube Boilers |

| Water-Tube Boilers |

| Electric Boilers |

| Condensing Boilers |

By Fuel Type

| Natural Gas |

| Oil |

| Biomass |

| Electric |

| Hydrogen Blend |

By Capacity

| Less Than 10 MW |

| 10 - 50 MW |

| 51 - 100 MW |

| Above 100 MW |

By End-User

| Residential |

| Commercial |

| Industrial |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Netherlands |

| Belgium |

| Denmark |

| Sweden |

| Norway |

| Finland |

| Poland |

| Czech Republic |

| Austria |

| Switzerland |

| Russia |

| Rest of Europe |

| By Boiler Type | Fire-Tube Boilers |

| Water-Tube Boilers | |

| Electric Boilers | |

| Condensing Boilers | |

| By Fuel Type | Natural Gas |

| Oil | |

| Biomass | |

| Electric | |

| Hydrogen Blend | |

| By Capacity | Less Than 10 MW |

| 10 - 50 MW | |

| 51 - 100 MW | |

| Above 100 MW | |

| By End-User | Residential |

| Commercial | |

| Industrial | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Belgium | |

| Denmark | |

| Sweden | |

| Norway | |

| Finland | |

| Poland | |

| Czech Republic | |

| Austria | |

| Switzerland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe boiler system market?

The market is valued at USD 7.14 billion in 2025 and is projected to reach USD 9.20 billion by 2030.

Which boiler type is growing fastest in Europe?

Electric designs register the highest forecast growth at a 6.23% CAGR to 2030, driven by industrial electrification objectives.

How are EU incentives influencing boiler upgrades?

Programs such as Germany’s EUR 13.5 billion fund and the UK’s GBP 7,500 grants accelerate adoption of hydrogen-ready and heat-pump-linked systems by cutting upfront costs.

Why is Spain the fastest-growing national market?

Robust subsidies that reimburse up to 70% of device cost and high solar generation that lowers electric-heat economics push Spain to a 5.33% CAGR through 2030.

What fuels will dominate future boiler installations?

Natural gas remains prevalent, but hydrogen-blend and fully hydrogen-capable systems post the strongest growth due to EU decarbonization pathways.

How fragmented is the competitive landscape?

The market shows moderate concentration; the top five players control near-60% of revenue, while niche firms thrive in specialized segments such as biomass and micro-modular electric units.

Page last updated on: