Ethyl Acetate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

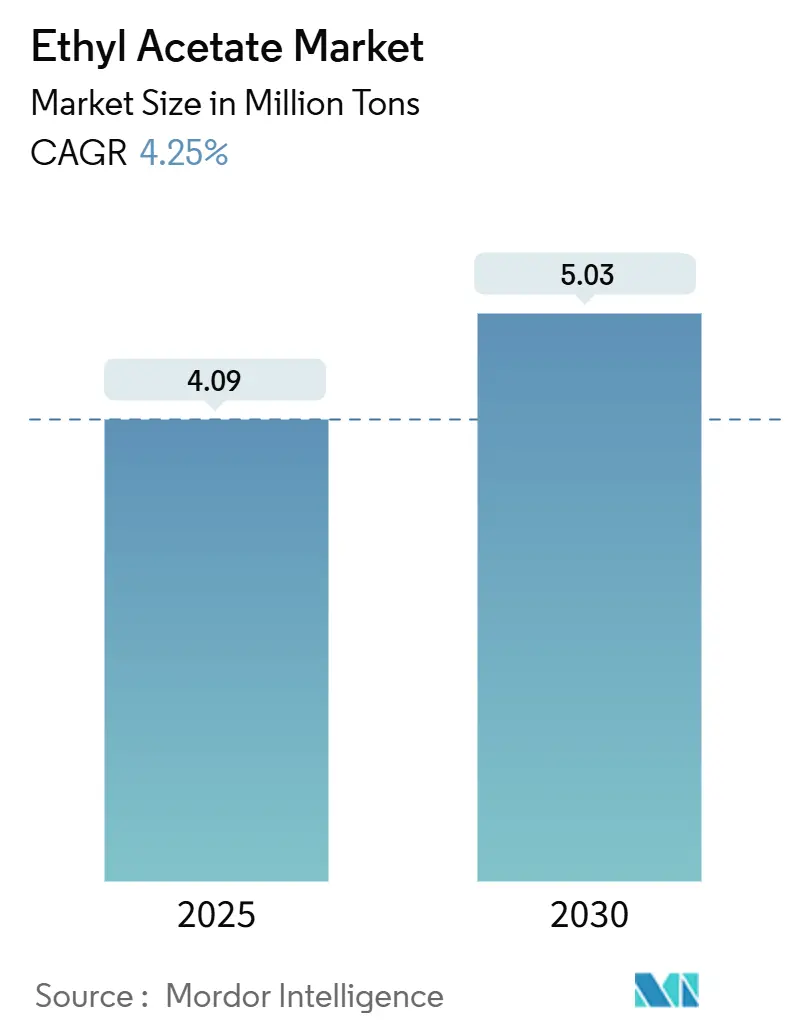

| Market Volume (2025) | 4.09 Million tons |

| Market Volume (2030) | 5.03 Million tons |

| Growth Rate (2025 - 2030) | 4.25% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ethyl Acetate Market Analysis by Mordor Intelligence

The ethyl acetate market stands at 4.09 million tons in 2025 and is forecast to reach 5.03 million tons by 2030, registering a 4.25% CAGR between 2025 and 2030. Growth is anchored in the solvent segment of paints and coatings, pharmaceutical‐grade demand, and the European shift to low-VOC formulations. Capacity additions in China are holding global prices down, prompting Western producers to pivot toward specialty and bio-based grades. North America benefits from pharmaceutical expansion and emerging renewable routes, yet faces feedstock price swings. Competitive success increasingly depends on vertical integration, premium-grade positioning, and agile compliance with fragmented regulatory regimes.

Key Report Takeaways

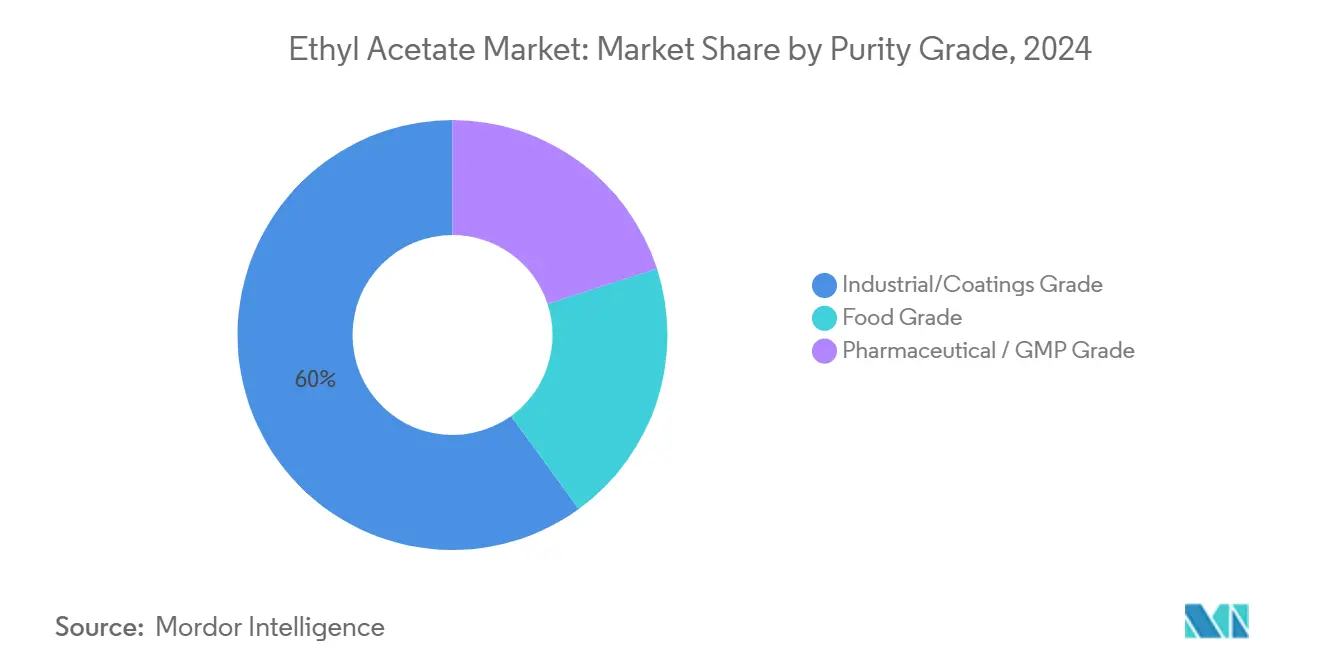

- By purity grade, the industrial/coatings grade accounted for 60% of the ethyl acetate market share in 2024; pharmaceutical/GMP grade is advancing at a 5.3% CAGR through 2030.

- By source, petro-based products held 90% share of the ethyl acetate market in 2024, whereas the bio-based route is forecast to grow at a 6.30% CAGR to 2030.

- By application, paints and coatings led with 53% ethyl acetate market share in 2024, while adhesives and sealants are projected to expand at a 5.25% CAGR to 2030.

- By end-user industry, automotive captured 52% share of the ethyl acetate market size in 2024; food and beverage is on track for a 5.10% CAGR between 2025 and 2030.

- By geography, Asia-Pacific dominated with 73% ethyl acetate market share in 2024, but North America is set to post the fastest 5.40% CAGR through 2030.

Global Ethyl Acetate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand in Solvent Applications | +1.2 | Global, with emphasis on Asia Pacific | Short term (≤ 2 years) |

| Growth of the Pharmaceutical Sector | +0.8 | North America & EU | Medium term (2-4 years) |

| EU shift to low-VOC solvents boosting offset-printing consumption | +0.6 | EU | Medium term (2-4 years) |

| Increasing Demand for Personal Care Products | +0.3 | Global | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Demand in Solvent Applications

Paints and coatings, construction recovery, and automotive refinishing keep solvent usage at the center of ethyl acetate market expansion. The segment commands reliable demand because the solvent balances fast flash-off with high solvency power, delivering high-gloss finishes. Formulators are reformulating to meet low-VOC targets without losing performance, and ethyl acetate’s relatively low toxicity encourages further substitution from ketones. Integrated producers have invested in upstream acetic acid to secure margin stability, shielding them from feedstock uncertainty. Asia-Pacific construction projects and automotive export growth amplify volumes, while Europe prizes compliant formulations that align with tightening emission caps[1]Celanese Corporation, “Ethyl Acetate,” celanese.com

Growth of the Pharmaceutical Sector

Demand for pharmaceutical/GMP grade material is climbing faster than overall consumption, as complex active pharmaceutical ingredients require consistent solvent quality. Continuous manufacturing lines specify narrow impurity profiles, raising barriers for non-specialized suppliers. Producers are upgrading purification technologies, including fractional distillation and adsorptive polishing, to meet pharmacopoeial monographs. Higher margins insulate this niche from commodity price swings that weigh on industrial grades. North American investments in API capacity and Europe’s focus on reshoring critical medicine supply strengthen regional consumption.

EU Shift to Low-VOC Solvents

European regulators have tightened VOC limits through the Industrial Emissions Directive and BAT conclusions, spurring printers to replace aromatics with ethyl acetate. Offset presses need a solvent that evaporates predictably yet supports ink transfer, and ethyl acetate offers a balanced profile. Compliance carries a premium, enabling European formulators to accept higher input costs. The Packaging and Packaging Waste Regulation, finalized in March 2024, adds momentum because recyclable packaging inks often rely on ethyl acetate for fast drying. As a result, European demand grows even while regional production costs rise[2]USDA Foreign Agricultural Service, “European Union Finalizes New Rules for Packaging and Packaging Waste Reduction,” apps.fas.usda.gov .

Increasing Demand for Personal Care Products

Nail polish, fragrance carriers, and clean beauty launches have elevated solvent consumption in personal care. Ethyl acetate’s fast dry-down supports quick-setting varnishes favored by salons, while its fruity odor harmonizes with perfume bases. Brand owners prefer food-grade variants that provide label-friendly traceability and gain consumer approval. The sector’s marketing cycles are short, so formulators choose a solvent with global registrations to minimize reformulation risk. Demand extends beyond high-income markets as middle-class consumers in Asia and Latin America adopt premium cosmetics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Conversion to water-borne adhesives in Europe | -0.70% | Europe | Medium term (2-4 years) |

| Volatile acetic-acid feedstock prices in North America | -0.50% | North America | Short term (≤ 2 years) |

| Global oversupply from recent Chinese capacity additions pressuring prices | -1.00% | Global, with highest impact in Asia | Short term (≤ 2 years) |

| Stringent Environmental Regulations | -0.30% | EU & North America | Long term (≥ 4 years) |

Source: Mordor Intelligence

Conversion to Water-borne Adhesives in Europe

European packaging and woodworking lines are moving to acrylic dispersions to meet internal sustainability pledges. As water-borne chemistries gain share, industrial buyers cut orders for solvent-based adhesives that typically contain ethyl acetate. Performance gaps are narrowing but remain for high-speed laminations, so displacement is uneven across sub-segments. Solvent demand now concentrates in specialty niches where peel strength and heat resistance matter most. Suppliers are countering volume losses by launching bio-based ethyl acetate grades that complement corporate greenhouse-gas targets.

Volatile Acetic Acid Feedstock Prices

Acetic acid accounts for as much as 65% of variable cost. Force majeure events, natural-gas swings, and shifting global trade routes have whipsawed prices since 2024. Non-integrated producers experience margin compression or curtail runs in low-price cycles, tightening spot supply. Vertically integrated firms such as Celanese secure stability through captive acid capacity, evidenced by the 1.3 million ton expansion in Clear Lake. Persistent volatility encourages geographic diversification of supply contracts but raises working-capital needs, challenging smaller market participants.

Segment Analysis

By Purity Grade: Pharmaceutical Production Outpaces Commodity Use

The industrial/coatings grade retained a 60% ethyl acetate market share during 2024, supported by broad deployment in paints, inks, and general solvents. Competitive pricing from Chinese exporters keeps this segment commoditized, pressuring Western operators to lift efficiency and explore downstream specialty blends. Pharmaceutical/GMP grade, though smaller in volume, registered a 5.3% CAGR and is forecast to stay ahead of overall ethyl acetate market growth. Heightened regulatory scrutiny of residual solvents in drug manufacture is driving investment in advanced purification columns and online quality monitoring. Producers with validated GMP systems enjoy premium pricing and stickier customer contracts. Continuous manufacturing in large North American API plants further entrenches demand for high-purity lots that arrive on just-in-time schedules. The resilience of this niche points to a gradual shift in ethyl acetate industry capacity planning toward fewer, higher margin molecules that shield participants from commodity price cycles.

Regulators in the EU and the United States require full traceability of solvent provenance, compelling suppliers to certify agricultural ethanol or acetic acid raw materials. As a result, pharma-grade producers are deepening ties with feedstock suppliers to guarantee consistent isotopic fingerprints. This alignment enhances supply security while signaling adherence to environmental, social, and governance expectations. Capital requirements for clean-room packaging and dedicated storage tanks limit new entrants, effectively raising barriers that defend incumbent margins.

Note: Segment shares of all individual segments available upon report purchase

By Source: Bio-based Route Gains Momentum

Petro-based variants dominated 2024 with 90% volume, benefiting from integrated acetic acid routes and favorable scale economies. Yet the bio-based pathway is expanding at a 6.30% CAGR, comfortably outperforming the ethyl acetate market. Suppliers exploit ethanol fermentation from sugarcane, corn, or residual biomass to reduce carbon intensity. Godavari Biorefineries is ramping up its distillery to 1,000 KLPD, enabling greater output of renewable ester grades that qualify for low-carbon labeling. Early adopters in flexible packaging are willing to pay a green premium when carbon disclosures influence brand perception.

Investment continues in enzymatic esterification and solid acid catalysis that lower energy footprints versus conventional Fischer esterification. European producers also benefit from the Renewable Energy Directive that values bio-based content in chemicals. Although feedstock logistics constrain absolute scale, policy incentives and corporate climate goals safeguard offtake agreements. Over the medium term, bio-based volumes are expected to erode petro-based share gradually, especially in markets with carbon taxation or mandated renewable quotas.

By Application: Adhesives Register Fastest Growth

Paints and coatings absorbed 53% of global demand in 2024, underpinning ethyl acetate market size leadership at the application level. Architectural repaint activity in Asia and refurbishing of vehicle fleets worldwide sustain baseline consumption even when new construction plateaus. Meanwhile, adhesives and sealants, though a smaller slice, are on track for a 5.25% CAGR through 2030, making them the fastest-growing user. Laminated flexible packaging lines require precise drying profiles to maintain bond strength, and ethyl acetate excels due to its moderate boiling point and low residual odor.

Substitution pressure from water-borne systems is significant in Europe, yet adhesive users in high-speed gravure or extrusion coating lines retain solvent grades where open time and peel resistance are critical. Producers counter VOC concerns by optimizing capture systems and offering bio-based ethanol routes that improve the sustainability narrative. Specialty hot-melt adhesives also incorporate ethyl acetate in primer blends that promote surface wetting on low-energy films, ensuring niche resilience even as bulk consumption evolves.

By End-user Industry: Food & Beverage Shows Highest CAGR

Automotive manufacturing kept its position as the largest end-use, accounting for 52% ethyl acetate market share in 2024 thanks to extensive use in body coatings and interior trim adhesives. The sector benefits from gradual global production recovery and rising adhesive content in lightweight platforms. Conversely, food and beverage applications are slated for a 5.10% CAGR, surpassing overall ethyl acetate market growth. The solvent’s GRAS status under FDA regulations supports flavor extraction in coffee decaffeination and fruit essence capture[3]Food and Drug Administration, “21 CFR 173.228 — Ethyl Acetate,” ecfr.gov .

Growing consumer interest in natural flavors and recyclable packaging drives sustained solvent demand in this vertical. The new EU recycling thresholds reinforce the role of ethyl acetate in inks for mono-material flexible structures that must withstand high-speed filling lines. Pharmaceutical end users, while smaller by volume, deliver superior value per ton, incentivizing suppliers to allocate capacity selectively. Artificial leather remains a notable buyer in Asia, leveraging the solvent for polyurethane dispersions that simulate genuine hide feel at lower cost.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commanded 73% of global volume in 2024 and anchors pricing. China’s recently commissioned plants operate below optimal utilization, creating export pressure that influences delivered costs worldwide. Regional demand spans automotive coatings, artificial leather, and packaging inks, ensuring large internal offtake even as exports climb. India emerges as a demand bright spot, buoyed by national pharmaceutical expansion and government incentives for bio-fuel-derived chemicals. Corporations such as Godavari Biorefineries leverage abundant sugarcane feedstock to support renewable ethyl acetate, diversifying supply away from purely fossil routes.

North America is projected to record the quickest 5.40% CAGR through 2030. The region enjoys shale-advantaged feedstock pricing, partial backward integration, and proximity to a robust pharmaceutical sector that requires GMP-grade solvent. Nevertheless, acetic acid volatility remains a recurring risk. Celanese’s Clear Lake expansion helps cushion supply shocks, yet non-integrated producers continue to hedge with multi-supplier contracts. Increasing environmental scrutiny promotes pilot-scale bio-based projects that could capture policy incentives under federal low-carbon initiatives.

Europe presents a dual reality of stringent regulation and premium applications. Demand is stable in offset printing, flexible packaging, and high-purity pharmaceutical uses, but conversion to water-borne adhesives restrains solvent volumes in construction. The Industrial Emissions Directive accelerates low-VOC solvent substitution, favoring ethyl acetate over aromatic alternatives. Producers emphasize specialty grades to offset rising energy and carbon costs, ensuring the region remains an importer despite local capacity. Exporters from Asia must navigate anti-dumping duties that the European Commission periodically reviews to protect domestic margins.

Competitive Landscape

Global supply is consolidated, with the top five suppliers controlling roughly 57% of total capacity. Chinese enterprises focus on scale and cost leadership, leveraging integrated coal-to-chemical routes that deliver low-cost acetic acid. Western companies differentiate through vertical integration and premium grades. Celanese expanded acetic acid capacity by 1.3 million tons in Texas to secure downstream margin and reduce sensitivity to feedstock swings. INEOS deploys flexible feedstock procurement and maintains European capacity to serve niche pharmaceutical clients who demand short supply chains.

Corporate strategies increasingly center on sustainability. Celanese initiated a carbon capture and utilization project that channels CO₂ back into acetic acid synthesis, thereby lowering product carbon footprints. Godavari Biorefineries markets cradle-to-gate lifecycle assessments for its renewable grades, courting multinational brand owners that carry Scope 3 emission targets. Sipchem’s EVA plant expansion illustrates adjacent diversification, as acetyl intermediates feed into value-added polymers. Smaller Asian producers compete on price but are starting to offer bio-based volumes to access higher margin export markets.

Ethyl Acetate Industry Leaders

-

Celanese Corporation

-

Daicel Corporation

-

Eastman Chemical Company

-

INEOS

-

Jiangsu SOPO (Group) Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Viridis Chemical, one of the leading developers of bio-based, low-carbon chemical technology and recipient of the U.S. Environmental Protection Agency’s 2024 Green Chemistry Challenge Award, has announced the relocation of its renewable chemicals plant from Columbus, Nebraska, to Peoria, Illinois, United States.

- March 2024: GODAVARI BIOREFINERIES LTD. has obtained environmental clearance to expand its distillery capacity from 600 KLPD to 1,000 KLPD, strengthening the supply of bio-based ethyl acetate feedstock. This expansion is expected to positively influence the ethyl acetate market by enhancing the availability of raw materials.

Global Ethyl Acetate Market Report Scope

Ethyl acetate is a colorless fragrant volatile flammable liquid ester C4H8O2 used especially as a solvent. It is an organic compound, a colorless liquid having a characteristic sweet smell, and it is used as a solvent and in glues and nail polish removers. The ethyl acetate market is segmented by application, end-user industry, and geography. By application, the market is segmented into adhesives and sealants, paints and coatings, pigments, process solvents, intermediates, and other applications (flavor enhancers, inks). By end-user industry, the market is segmented into automotive, artificial leather, food and beverage, pharmaceuticals, and other end-user industries (packaging). The report also covers the size and forecasts for the market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilo ton).

| Segmentation by Purity Grade | Industrial/Coatings Grade | ||

| Food Grade | |||

| Pharmaceutical/GMP Grade | |||

| Segmentation by Source | Petro-based | ||

| Bio-based | |||

| Segmentation by Application | Paints and Coatings | ||

| Flexible-Packaging Inks | |||

| Adhesives and Sealants | |||

| Pigments and Dyes | |||

| Process Solvents | |||

| Others (Flavor and Fragrance Enhancers, Inks) | |||

| Segmentation by End-user Industry | Automotive | ||

| Artificial Leather | |||

| Food and Beverage | |||

| Pharmaceuticals | |||

| Others (Packaging) | |||

| Segmentation by Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Nordics (Sweden, Norway, Finland, Denmark) | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| South Africa | |||

| Nigeria | |||

| Rest of East and Africa | |||

| Industrial/Coatings Grade |

| Food Grade |

| Pharmaceutical/GMP Grade |

| Petro-based |

| Bio-based |

| Paints and Coatings |

| Flexible-Packaging Inks |

| Adhesives and Sealants |

| Pigments and Dyes |

| Process Solvents |

| Others (Flavor and Fragrance Enhancers, Inks) |

| Automotive |

| Artificial Leather |

| Food and Beverage |

| Pharmaceuticals |

| Others (Packaging) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordics (Sweden, Norway, Finland, Denmark) | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of East and Africa |

Key Questions Answered in the Report

What is the current size of the ethyl acetate market?

The ethyl acetate market stands at 4.09 million tons in 2025 and is projected to reach 5.03 million tons by 2030.

Which region leads global consumption of ethyl acetate?

Asia-Pacific dominates with 73% share in 2024, driven by China’s large manufacturing base.

Why is pharmaceutical-grade ethyl acetate growing faster than industrial grades?

Stringent impurity limits and growing API capacity in North America and Europe are driving a 5.30% CAGR for pharmaceutical/GMP grade, exceeding overall market growth.

How are environmental regulations affecting ethyl acetate demand in Europe?

Tighter VOC limits under the Industrial Emissions Directive are pushing printers and coating formulators to adopt ethyl acetate as a compliant solvent.

What is the outlook for bio-based ethyl acetate?

Bio-based volumes are forecast to expand at a 6.30% CAGR because renewable feedstocks help users meet carbon reduction targets and justify premium pricing.

How volatile are feedstock costs for ethyl acetate producers?

Acetic acid prices remain volatile due to natural-gas fluctuations and supply disruptions, trimming margins for non-integrated producers while rewarding vertically integrated firms.

Page last updated on: June 26, 2025