ECG Cables And Lead Wires Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

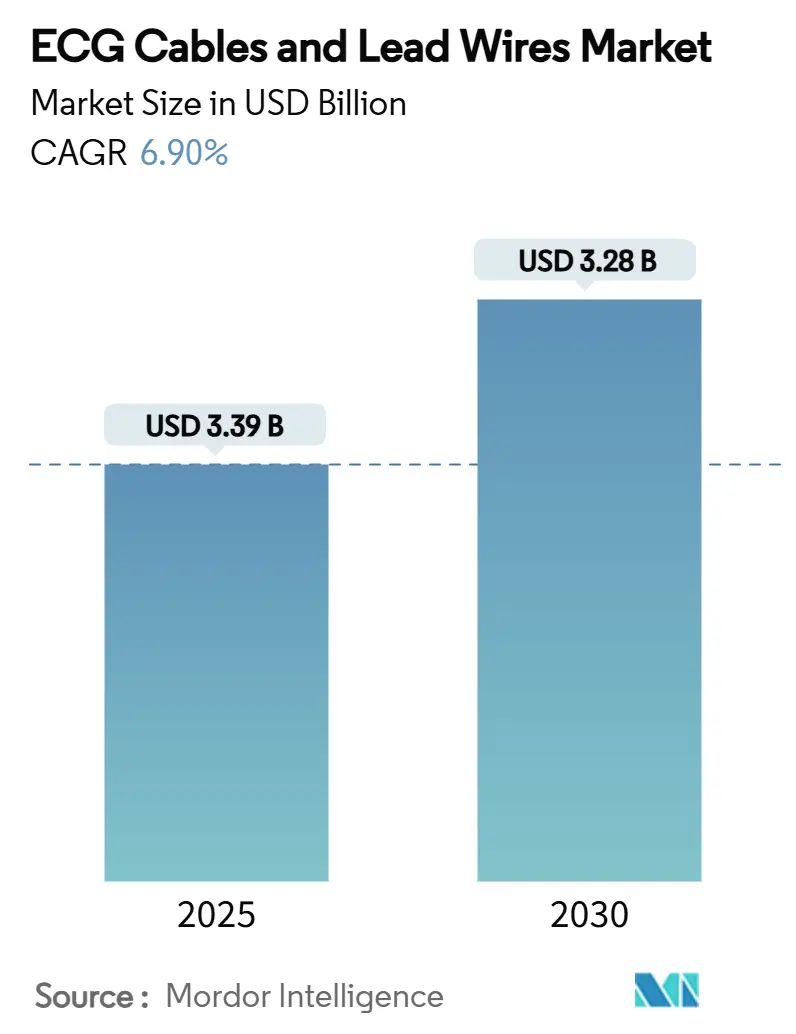

| Market Size (2025) | USD 3.39 Billion |

| Market Size (2030) | USD 3.28 Billion |

| Growth Rate (2025 - 2030) | 6.90% CAGR |

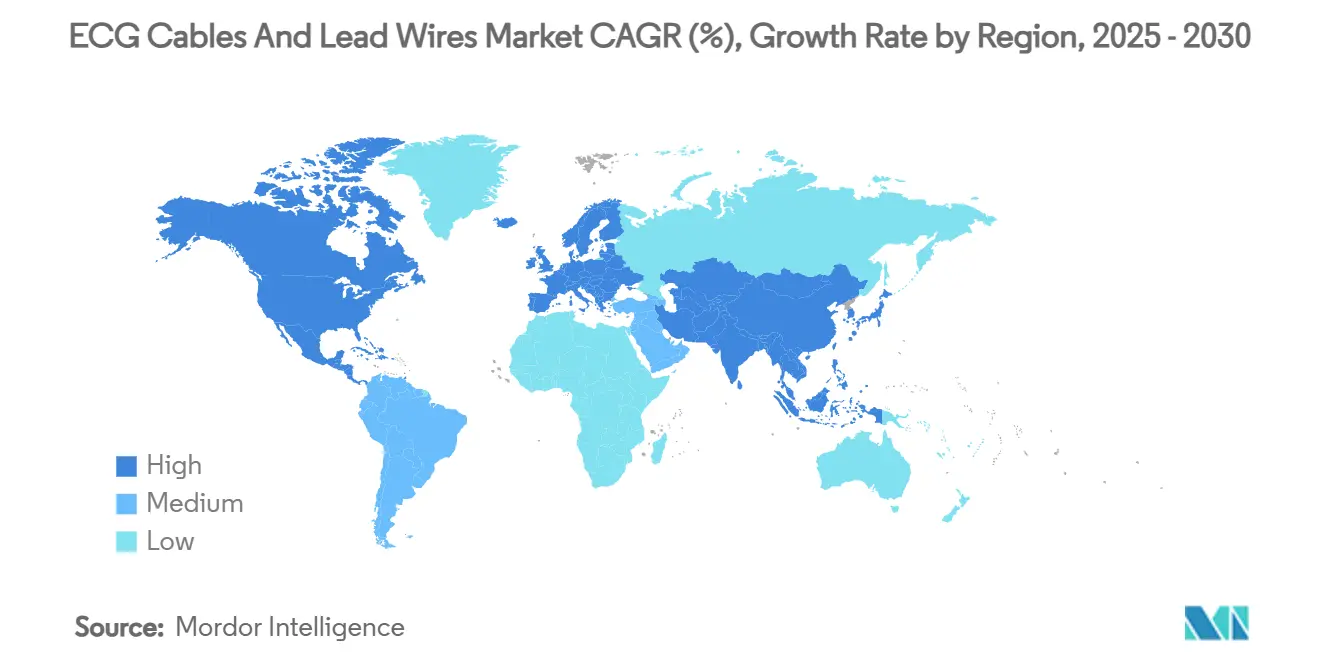

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ECG Cables And Lead Wires Market Analysis by Mordor Intelligence

The ECG cables and leads market size stood at USD 2.39 billion in 2025 and is forecast to reach USD 3.28 billion in 2030, advancing at a 6.9% CAGR. Steady demand stems from the high global cardiovascular disease burden, a fast-growing elderly population, and escalating requirements for continuous cardiac monitoring across hospitals and home-care environments. Regulatory momentum toward PVC-free materials, combined with hospital initiatives to limit healthcare-associated infections, accelerates product replacement cycles and opens avenues for premium, sustainable materials. Disposable, single-patient-use ECG leads are gaining traction as infection-control policies tighten, while artificial intelligence and IoT integration in patient monitoring platforms raise expectations for data accuracy, workflow efficiency, and actionable clinical insights. Consolidation among leading suppliers continues, with large-scale acquisitions redirecting R&D budgets toward smart, connected solutions and widening the competitive gap versus smaller regional manufacturers.

Key Report Takeaways

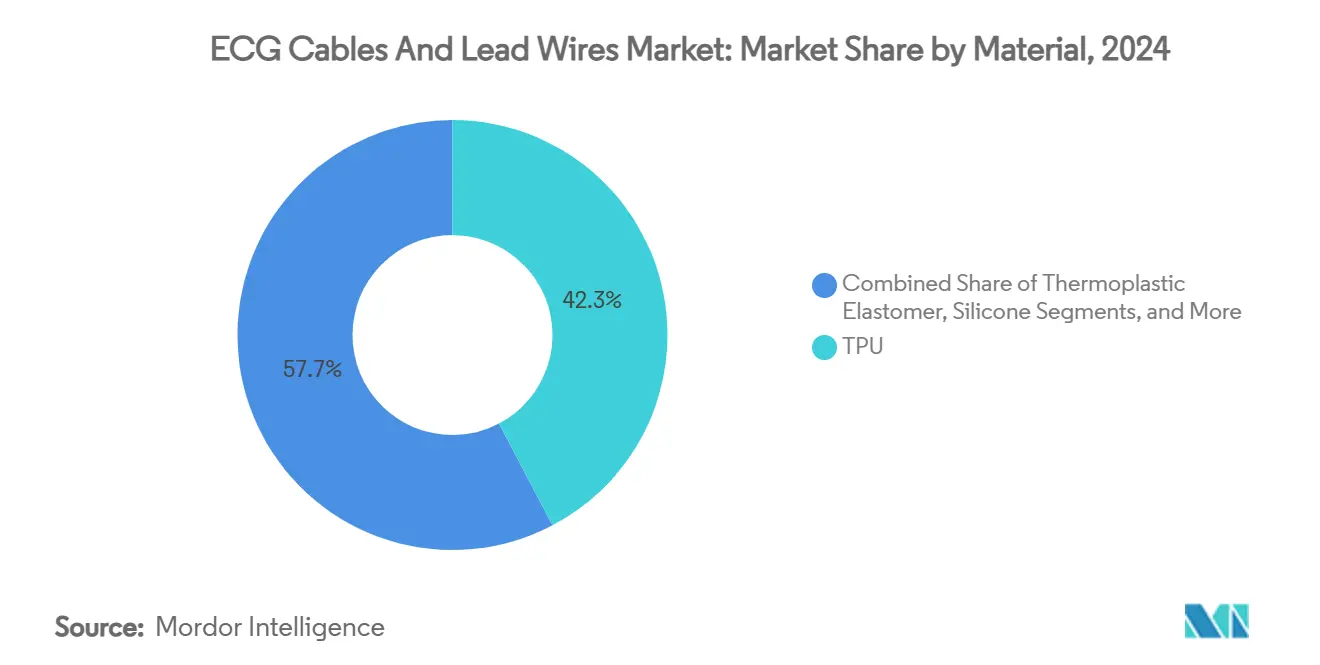

- By material, thermoplastic polyurethane held 42.3% of the ECG cables and leads market share in 2024; thermoplastic elastomer is projected to register a 9.8% CAGR to 2030.

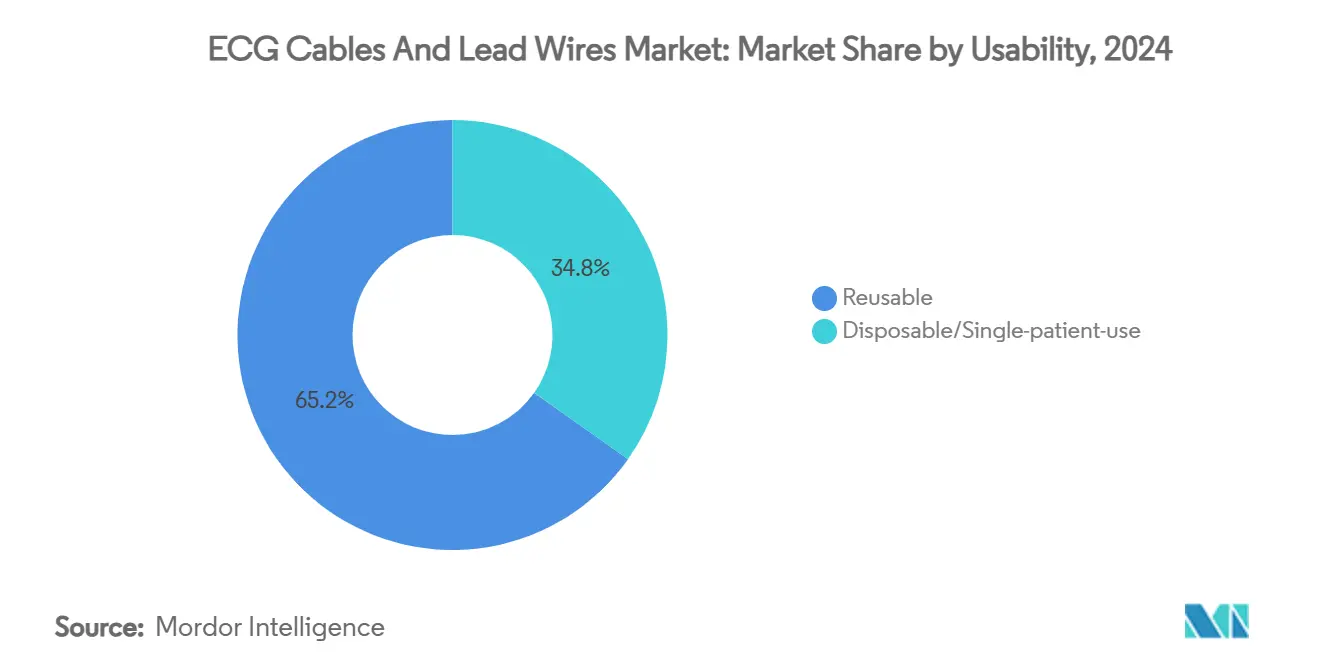

- By usability, reusable products commanded 65.2% share of the ECG cables and leads market size in 2024, while single-patient-use leads are forecast to grow at a 10.6% CAGR through 2030.

- By geography, North America led with 38.7% revenue share in 2024; Asia Pacific displays the fastest expansion at an 8.9% CAGR during 2025-2030.

Global ECG Cables And Lead Wires Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population and cardiovascular burden | +1.80% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Hospital shift to single-patient-use leads | +1.20% | Global, led by developed markets | Medium term (2-4 years) |

| Expansion of remote/telemetry fleets | +1.50% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| OEM cable replacement under PVC-free mandates | +0.90% | Europe and North America | Short term (≤ 2 years) |

| Emergence of RFID/IoT-enabled smart cables | +0.80% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| Warranty expiries fuelling aftermarket demand | +0.70% | Asia Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Cardiovascular Disease Burden

Cardiovascular disease remains the leading global cause of death, and rising life expectancy lifts the prevalence of chronic cardiac conditions that require continuous ECG surveillance. Demand extends from acute-care units to ambulatory and consumer settings, evidenced by regulatory clearances for smartwatch-based ECG functions. Vendors respond with high-bandwidth leads compatible with multi-parameter monitors and imaging platforms, improving diagnostic precision for arrhythmia and ischemia detection. Public health agencies emphasize early intervention programs that rely on efficient data transfer from patient to clinician, cementing the ECG cables and leads market as an essential pillar of long-term disease management. The resulting uplift in monitoring volumes underpins sustained revenue visibility for both capital equipment and disposables suppliers.

Hospital Shift to Single-Patient-Use Leads to Curb HAIs

Growing scrutiny of healthcare-associated infections intensifies preference for disposable ECG leads despite mixed evidence on clinical benefits.[1]Critical Care Medicine, “A RCT of Infection Rates in ICU Environments by EKG Lead Wire Type,” journals.lww.com Procurement teams weigh perceived infection risk reduction against higher recurring costs, often choosing disposables to satisfy risk-management committees. Operational advantages include streamlined re-processing workflows and lower cross-contamination liability, which resonate with hospital executives. Meanwhile, reusable products evolve through advanced disinfectant-resistant jacketing and antimicrobial additives, while UVC-LED cabinets capable of 99.9999% pathogen reduction enter central-sterile departments. The coexistence of these models sustains dual-track growth in the ECG cables and leads market, allowing suppliers to cater to divergent infection-control strategies.

Expansion of Remote / Telemetry Monitoring Fleets

Remote patient monitoring is expected to grow significantly, illustrating the scale of out-of-hospital cardiac care. Reimbursement codes introduced by federal payers boost provider adoption, though only one in four practices currently deploy remote solutions due to data-security and workflow hurdles.[2]IntuitionLabs, “Remote Patient Monitoring in the United States: 2025 Landscape Report,” intuitionlabs.ai Wearable ECG devices achieve high accuracy in arrhythmia detection, feeding actionable data into cloud dashboards that clinicians can access in near real time. Rising telemetry bed installations across step-down units reinforce demand for durable multi-lead cables, while ambulatory kits require lightweight, patient-friendly connectors. Vendors combine traditional copper wiring with Bluetooth Low Energy transponders to relay high-resolution waveforms, bridging bedside and home-care ecosystems within the ECG cables and leads market.

OEM Cable Replacement Cycle Triggered by PVC-Free Mandates

European Union Regulation 923/2023 limits lead in PVC to below 0.1%, forcing manufacturers to reformulate and pushing healthcare providers to swap non-compliant inventories before November 2024. Thermoplastic polyurethane and thermoplastic elastomer emerge as preferred substitutes given their flexibility, biocompatibility, and processing ease. Compliance costs accelerate OEM demand for qualified contract molders, while hospitals budget for accelerated refresh cycles. Dual product lines surface as manufacturers balance legacy markets that still accept PVC with regulated regions. In turn, the ECG cables and leads market enjoys a near-term revenue uplift tied to mandated material conversion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price commoditisation and tender pressures | -1.40% | Global, most severe in Europe and emerging markets | Medium term (2-4 years) |

| Reimbursement uncertainty for outpatient ECG | -0.80% | North America, select European markets | Short term (≤ 2 years) |

| Medical-grade TPU supply chain fragility | -0.60% | Global, highest impact in APAC manufacturing hubs | Medium term (2-4 years) |

| Cyber-security compliance costs for connected cables | -0.40% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Commoditization & Tender Pressures

Global cost-containment programs compress average selling prices as procurement shifts from clinician-centred evaluation to competitive tenders driven by finance teams. Standardized specifications weaken brand differentiation, while regional distributors undercut multinationals with low-margin offerings. Inflation in raw materials and logistics has pushed some suppliers’ cost of goods up by 20%, yet hospitals demand annual price concessions, stretching operating margins. Portfolio optimization programs concentrate production on high-volume SKUs, and multi-year supply contracts are tied to performance metrics on delivery lead-time and technical support. Such dynamics moderate revenue expansion across the ECG cables and leads market.

Reimbursement Uncertainty for Outpatient ECG

Coverage rules for remote ECG supplies in outpatient settings remain inconsistent, creating financial risk for providers. Medicare’s incident-to provisions require direct clinical supervision, limiting reimbursement in home environments, while private insurers vary widely in their policies.[3]eCFR, “Services and Supplies Incident to a Physician’s Professional Services,” ecfr.gov Providers hesitate to scale monitoring programs without clear payment pathways, tempering near-term volumes. Industry coalitions lobby for additional HCPCS codes specific to connected cables and leads, yet regulatory timelines remain uncertain. Accordingly, the ECG cables and leads market experiences demand gaps in the outpatient segment despite evident clinical need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Sustainable Polymers Reshape Product Mix

Thermoplastic polyurethane held a 42.3% ECG cables and leads market share in 2024, owing to flexibility, kink resistance, and skin-contact biocompatibility. Strict EU lead limits propel procurement officers to accelerate PVC substitution, which elevates thermoplastic elastomer demand at a 9.8% CAGR during 2025-2030. The ECG cables and leads market size attributable to TPE solutions is forecast to expand sharply as OEMs retool extrusion lines for halogen-free compounds. Silicone maintains a niche in long-term monitoring and neonatal care because of its hypoallergenic properties. At the same time, PET and PEEK address specialty electrophysiology applications that demand high tensile strength or radiopacity. Cost and processing complexity limit these high-performance resins to small-batch runs, but their strategic value lies in serving mission-critical procedures where product failure carries elevated clinical risk.

Material decisions influence weight, flexibility, and dielectric properties that directly affect signal fidelity and patient comfort. Due to their predictable mechanical durability, TPU-based assemblies remain the gold standard for general ward and telemetry use. TPE’s low-temperature fold capability advances cold-chain transport safety, easing distribution to remote geographies. Emerging bio-derived TPU skews toward sustainability targets in corporate ESG programs, hinting at new differentiation opportunities for suppliers in the ECG cables and leads market.

By Usability: Disposable Growth Versus Reusable Dominance

Reusable assemblies accounted for 65.2% of the ECG cables and leads market size in 2024, reflecting budgetary preference for capitalized assets in high-volume inpatient units. Sterilization-friendly jacketing and connector designs withstand hundreds of cleaning cycles, enabling favourable total cost of ownership in facilities with robust central-sterile operations. Yet single-patient-use leads will post the fastest 10.6% CAGR through 2030 as infection-prevention committees favour disposables for critical-care and post-surgical wards. Adoption is further spurred by bundled-pricing contracts that integrate consumables with monitoring equipment capital leases, easing procurement approval. RFID tagging in reusable cables supports tracking and loss prevention, giving hospital engineers data for usage analytics and timely replacement. Meanwhile, advanced disinfection cabinets deliver near-total pathogen eradication, potentially slowing disposable uptake if cost pressures intensify.

Patient comfort remains central as smaller electrodes and lighter cabling reduce skin irritation during prolonged telemetry. Suppliers refine ergonomics and colour-coding to improve bedside workflow, and single-click connectors shorten nurse changeover times, strengthening user loyalty within the ECG cables and leads market.

Geography Analysis

North America generated the highest 38.7% revenue share in 2024, sustained by sophisticated care delivery networks, multi-payer reimbursement structures, and early adoption of telemetry and RPM billing codes. Providers favour integrated device platforms that pair ECG leads with SpO₂ and NIBP, creating demand for high-quality multipurpose cables. Material-compliance mandates are less stringent than Europe’s, yet sustainability commitments from hospital groups catalyse voluntary PVC phase-outs, reinforcing replacement sales in the ECG cables and leads market.

Asia Pacific is the fastest-growing territory, set to deliver an 8.9% CAGR to 2030 as demographic shifts enlarge chronic-disease caseloads and government health reforms raise expenditure ceilings. China’s double-digit medical device expansion and India’s insurance coverage rollout boost baseline demand. Regional OEMs partner with multinational brands to localize assembly, improving price competitiveness and skirting import duties. The ASEAN Medical Device Directive advances regulatory harmonization, yet disparate in-country license procedures prolong certification cycles, influencing product-launch pacing across the ECG cables and leads market.

Europe juggles tight reimbursement growth and rigorous regulatory regimes. The Medical Device Regulation heightens documentation requirements, and EU Regulation 923/2023 forces material changes that raise unit costs. Nevertheless, government procurement frameworks often reward sustainability, giving PVC-free leads a competitive edge. Middle East & Africa and South America display rising device penetration as private hospital networks expand. Warranty expiries on legacy monitors acquired during pandemic surges fuel aftermarket cable demand, although currency-rate swings can impede import affordability. Collectively, these dynamics diversify revenue streams and mitigate single-region exposure for suppliers active in the ECG cables and leads market.

Competitive Landscape

The ECG cables and leads industry shows moderate fragmentation. 3M, Cardinal Health, GE Healthcare, Philips, and Medtronic anchor the upper tier with global distribution scale and deep telemetry portfolios. Acquisition activity accelerated through 2024-2025: BD paid USD 4.2 billion for Edwards Lifesciences’ Critical Care unit, and Teleflex acquired BIOTRONIK’s vascular operation for €760 million, combining supply-chain synergies with broader hospital-solution offerings. Ecosystem partnerships such as Medtronic’s alliance with Philips embed lead consumables inside comprehensive monitoring bundles, driving account stickiness.

Technology roadmaps prioritise smart features that help escape price commoditization. Vendors integrate RFID, Bluetooth, and cloud APIs to tap analytics service revenues, while cyber-secure firmware differentiates hospital-grade from consumer products. Regional producers in China and Southeast Asia compete on low-cost PVC designs, but regulatory shifts toward heavy-metal limits could constrain their export options. Supply-chain resilience strategies include dual-sourcing of medical-grade TPU and near-shoring final assembly in North America and Europe to mitigate freight volatility. These manoeuvres underline a competitive race in the ECG cables and leads market to balance innovation, compliance, and cost efficiency.

ECG Cables And Lead Wires Industry Leaders

GE Healthcare

Philips Healthcare

Cardinal Health

3M

Becton, Dickinson & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Medtronic signed a multi-year partnership with Philips to integrate Medtronic technologies into Philips monitoring systems and bundle ECG cables with compatible hardware, broadening global reach.

- March 2025: GE HealthCare introduced the Revolution Vibe CT with AI-driven Unlimited One-Beat Cardiac imaging, enabling ECG-less workflows.

- June 2024: BD agreed to purchase Edwards Lifesciences’ Critical Care business for USD 4.2 billion, expanding its smart-connected monitoring footprint.

Global ECG Cables And Lead Wires Market Report Scope

| Thermoplastic Polyurethane (TPU) |

| Thermoplastic Elastomer (TPE) |

| Silicone |

| Polyvinyl Chloride (PVC) |

| Others (PET, PEEK) |

| Reusable Cables & Leads |

| Disposable / Single-patient-use |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Thermoplastic Polyurethane (TPU) | |

| Thermoplastic Elastomer (TPE) | ||

| Silicone | ||

| Polyvinyl Chloride (PVC) | ||

| Others (PET, PEEK) | ||

| By Usability | Reusable Cables & Leads | |

| Disposable / Single-patient-use | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of global ECG cables and leads demand in 2030?

The ECG cables and leads market size is forecast to reach USD 3.28 billion by 2030 at a 6.9% CAGR.

Which region is forecast to grow the fastest for ECG cables and leads between 2025 and 2030?

Asia Pacific is expected to post an 8.9% CAGR during the period thanks to healthcare modernization and demographic expansion.

Which material currently dominates ECG cable production?

Thermoplastic polyurethane led with 42.3% market share in 2024 due to flexibility and biocompatibility advantages.

Are disposable ECG leads gaining traction over reusable designs?

Yes, single-patient-use leads are projected to advance at a 10.6% CAGR through 2030, outpacing reusable alternatives although reusables still hold the majority share.

How are sustainability regulations influencing product replacement cycles?

EU restrictions on lead in PVC have triggered accelerated replacement of legacy cables with PVC-free alternatives, directly boosting near-term sales volumes.

Which companies recently made notable acquisitions in the monitoring segment?

BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care unit and Teleflex’s €760 million acquisition of BIOTRONIK’s vascular business exemplify the period’s consolidation trend.

Page last updated on: