Dust Control Systems And Suppression Chemicals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

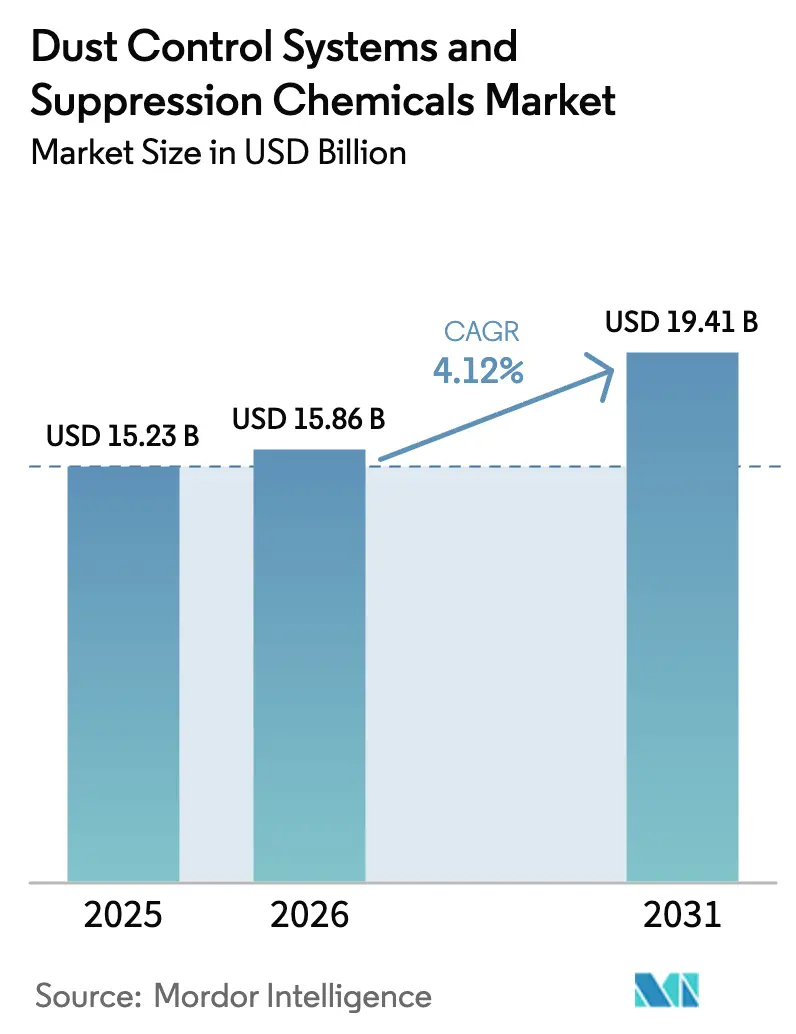

| Market Size (2026) | USD 15.86 Billion |

| Market Size (2031) | USD 19.41 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dust Control Systems And Suppression Chemicals Market Analysis by Mordor Intelligence

The Dust Control Systems and Suppression Chemicals Market size is expected to grow from USD 15.23 billion in 2025 to USD 15.86 billion in 2026 and is forecast to reach USD 19.41 billion by 2031 at 4.12% CAGR over 2026-2031. Urban logistics hubs now fall under particulate limits that were once confined to mining and construction, broadening the customer base and encouraging the adoption of polymeric emulsions that reduce water use. Investment is shifting from capital-intensive dry collectors toward flexible chemical platforms as operators seek to reduce both maintenance and freshwater demand amid fluctuations in feedstock prices. The Asia-Pacific region dominates revenue, thanks to simultaneous coal-mine expansion and aggressive PM10 enforcement. Europe and North America track steadier growth, led by retrofits and IoT-connected misting systems that reduce reagent waste.

Key Report Takeaways

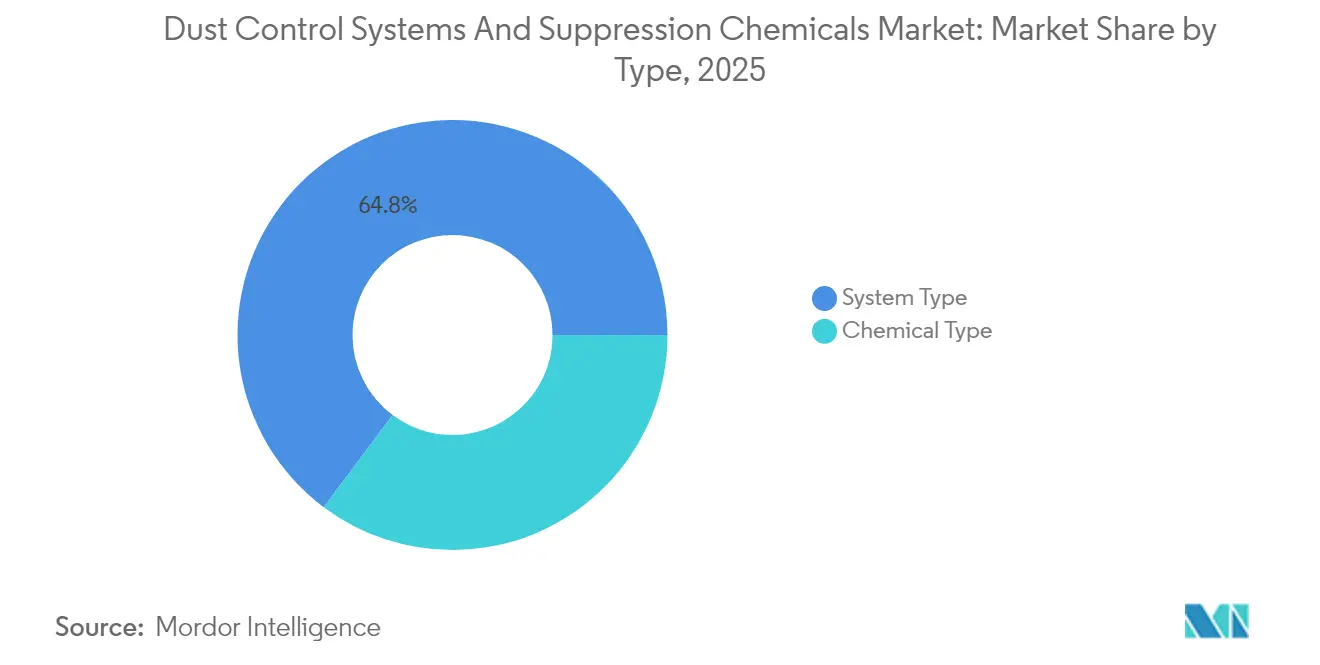

- By type, system type accounted for 64.78% of 2025 revenue, while chemical products recorded the fastest 4.52% CAGR through 2031.

- By end-user, the construction sector led with 35.28% of the dust control systems and suppression chemicals market share in 2025; this segment is also expected to expand at a 4.61% CAGR to 2031.

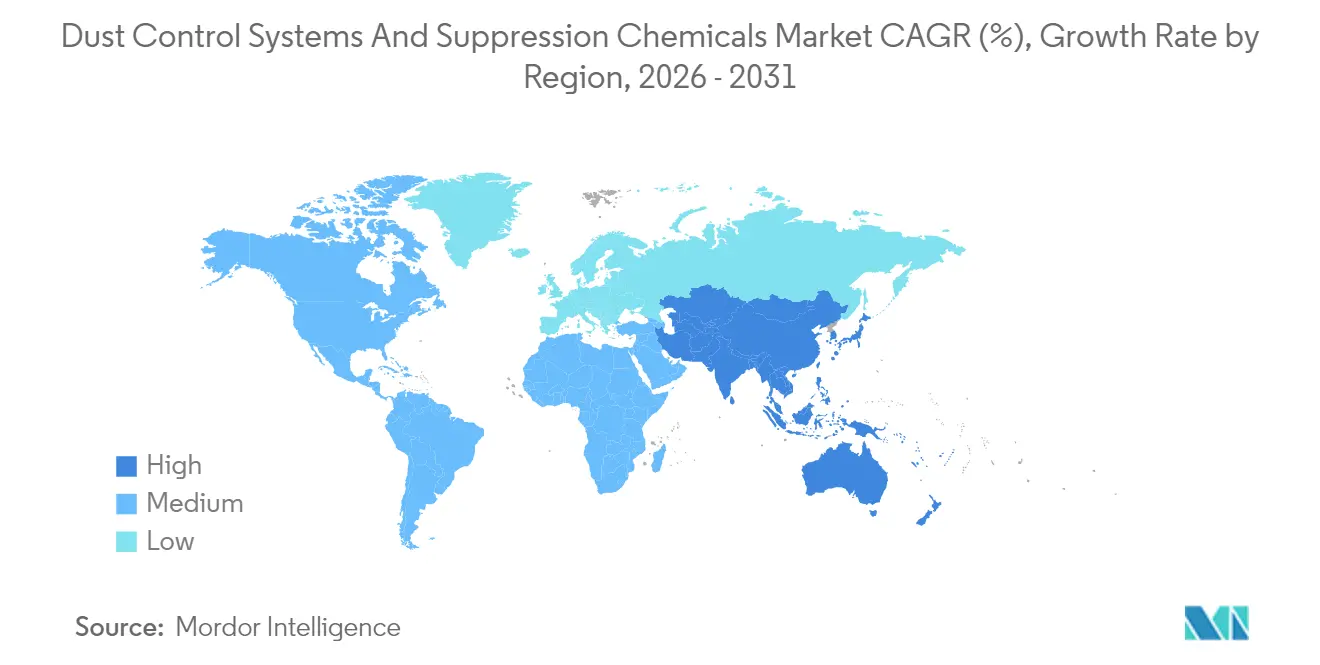

- By geography, Asia-Pacific captured 48.55% of global revenue in 2025 and is forecast to grow at a 4.44% CAGR, the highest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dust Control Systems And Suppression Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising infrastructure and mining activity in Asia-Pacific | +1.2% | Asia-Pacific core, spillover to Middle East | Medium term (2–4 years) |

| Stricter global PM10/PM2.5 emission standards | +1.5% | Global, with early enforcement in EU and North America | Short term (≤ 2 years) |

| Shift from water-only spraying to chemical binders | +0.9% | APAC, Middle East, Latin America (water-scarce zones) | Medium term (2–4 years) |

| Adoption of IoT-enabled smart misting and dosing systems | +0.6% | North America, Europe, urban APAC corridors | Long term (≥ 4 years) |

| Carbon-credit revenue for dust-reduction projects at mines | +0.3% | Australia, Canada, select EU jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infrastructure and Mining Activity in Asia-Pacific

Public spending on roads, rail, and ports is converting episodic chemical purchases into multi-year service contracts. India earmarked projects that now require real-time PM10 monitoring at site boundaries. China increased coal output and mandated the use of automated spray lines at pit heads, shifting demand away from manual water trucks. Nickel laterite mining in Sulawesi and Maluku generated refined nickel, with haul roads treated with polymer stabilizers to meet export permit terms. Thailand’s Eastern Economic Corridor tender favors ISO 14001-certified suppressants across rail and port developments. These projects collectively underpin long-run volume visibility for suppliers in the dust control systems and suppression chemicals market.

Stricter Global PM10/PM2.5 Emission Standards

The European Union has reduced its annual PM2.5 limit to 10 µg/m³ by 2030, requiring cement and aggregate plants to retrofit their collectors and chemical fog curtains[1]European Commission, “Ambient Air Quality Directive,” EC.europa.eu. The United States adopted a 9.0 µg/m³ standard in 2024, compelling Appalachian coal terminals to enclose conveyors. Euro 7 rules, effective 2026, capture brake and tire dust, pulling urban contractors into procurement frameworks that once served only heavy industry. Japan tightened PM2.5 limits in 2024 with enforcement at ports and demolition sites. Fines for non-compliance are accelerating uptake of high-efficacy binders, solidifying a premium pricing window for market leaders.

Shift from Water-Only Spraying to Chemical Binders

Groundwater limits in the Atacama Desert are prompting lithium mines to adopt magnesium chloride, which retains moisture for 72 hours, thereby reducing the need for spray runs. Pilbara iron-ore operators piloted lignin blends that lower dust while using one-third the water of traditional methods. Platinum mines in South Africa switched to acrylic copolymers, halving haul-road watering costs. Saudi Arabia’s NEOM site mandates bio-based suppressants to protect desalination capacity. The economics increasingly favor chemicals that deliver water savings alongside dust abatement, lifting chemical volumes inside the dust control systems and suppression chemicals market.

Adoption of IoT-Enabled Smart Misting and Dosing Systems

Epiroc’s 6th Sense platform-linked sensors trigger sprays only when PM10 exceeds thresholds, reducing chemical and diesel use. Nederman’s FX2 extraction arms adjust fan speed via machine learning, extending filter life. BossTek’s DB-100 Fusion logs GPS coordinates and spray metrics, making OSHA audits easier. South Korean 5G construction sites centrally manage multiple misting units, cutting on-site labor. Digitalization creates a data trail that validates emission reduction claims, a crucial step for crediting particulate offsets, as discussed later.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of chloride salts and lignin feedstock | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Corrosion concerns limiting chloride use on capital equipment | -0.5% | Mining-intensive regions (APAC, Latin America, Africa) | Medium term (2–4 years) |

| Fragmented regulations slowing product standardization | -0.4% | Global, pronounced in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Chloride Salts and Lignin Feedstock

Calcium chloride spot prices in North America surged in early 2024 after evaporation ponds closed at the Great Salt Lake. Magnesium chloride prices in Europe increased as Gulf producers prioritized magnesium metal. Lignin costs rose when pulp mills idled capacity amid weak packaging demand. Buyers are responding with multi-year fixed contracts and hybrid formulas that drop chloride content yet await regulatory clearance, adding uncertainty that weighs on the dust control systems and suppression chemicals market.

Corrosion Concerns Limiting Chloride Use on Capital Equipment

A Minnesota Department of Transportation study found that calcium chloride increased steel deck corrosion, prompting the establishment of exclusion zones near bridges[2]Minnesota Department of Transportation, “Research and Innovation,” Dot.state.mn.us. Pilbara audits found extra maintenance on chloride-exposed haul trucks, steering miners toward lignin blends. Food-grade factories ban chloride near stainless-steel equipment to avoid microbe-harboring pits, curbing market penetration. Corrosion inhibitors are added to formulations and require additional documentation, thereby increasing the total cost of ownership and slowing adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Lignin and Polymers Replace Pure Chlorides

Chemical types are projected to deliver a 4.52% CAGR outlook, outpacing mechanical systems as water scarcity increases. Lignin sulfonate has gained a share in Australia and Chile, where strict groundwater limits favor low-water binders that withstand winds of up to 40 km/h. Calcium and magnesium chloride remain volume leaders due to their hygroscopic properties, which retain surface dampness for up to 72 hours. Yet corrosion risk and price spikes are nudging buyers toward acrylic and styrene-butadiene emulsions, which form flexible films without chloride downsides and suit pharmaceutical cleaning standards.

Bio-based soy methyl ester emulsions are gaining popularity among California contractors after state rules tightened VOC limits on asphalt suppressants. Pilot projects in India and South Africa are testing xanthan gum and enzyme-based bio-cements that rival polymeric strength at one-third the cost, although six-month durability data are pending. These innovations broaden the chemical toolkit available to operators, enlarging the dust control systems and suppression chemicals market.

System solutions held 64.78% of 2025 revenue, reflecting OSHA and MSHA mandates for enclosed processes. Donaldson’s Downflo Evolution baghouse filters sub-micron particles at 99.97% efficiency while cutting pulse-air use. Camfil’s Gold Series meets ISO 16890 ePM1 for semiconductor cleanrooms, ensuring yield protection in sub-0.1 µm environments.

Wet-suppression rigs expand in open-pit mines and demolition sites where enclosure is impossible. BossTek’s DB-100 Fusion reaches 61 meters, capturing dust without over-wetting haul roads, and provides traceable compliance data. Nederman arms in welding bays reduce particulate and predict filter replacement to lower operating costs. IoT telemetry across these systems sews together performance data critical for carbon-credit validation, tying mechanical sales to emerging financial incentives.

By End-User Industry: Construction Leads on Infrastructure Pipelines

Construction accounted for 35.28% of end-user demand in 2025 and is projected to grow at a 4.61% CAGR through 2031, the fastest pace among verticals, driven by Asia-Pacific infrastructure pipelines and tightening urban air-quality enforcement. India's National Infrastructure Pipeline mandates real-time PM10 monitoring at all sites exceeding a specific size, with fines for non-compliance under the Central Pollution Control Board's guidelines. China's expressway network expanded further in 2024, with contractors deploying polymer-stabilized subgrades and automated misting rigs to meet Ministry of Ecology and Environment dust-control benchmarks. The Middle East's construction boom, anchored by Saudi Arabia's NEOM and the UAE's Expo City Dubai expansion, is creating demand for bio-based suppressants that preserve desalination capacity; NEOM's procurement guidelines mandate chloride-free formulations within coastal zones to protect marine ecosystems.

Mining is prioritizing water-saving chemical blends and electrified misting equipment to reduce diesel particulate matter and comply with carbon-reduction pledges. BHP's Pilbara iron-ore operations piloted lignin-sulfonate treatments in 2024, achieving significant reductions in dust generation with less water than conventional spraying. Glencore's copper mines in Chile and Peru are adopting magnesium-chloride formulations that extend haul-road moisture retention, cutting water-truck diesel consumption. Food and beverage facilities, which operate under Hazard Analysis and Critical Control Points (HACCP) protocols, require dust-collection systems with stainless steel construction and tool-free disassembly for easy sanitation. Camfil's Farr Gold Series filters, certified to FDA 21 CFR Part 11 for electronic record-keeping, are being used in dairy powder and flour milling plants. Oil, gas, and petrochemical sites deploy explosion-proof dust collectors rated to ATEX and IECEx standards for hazardous areas, with Nederman's DACS explosion suppression systems gaining a share in liquefied natural gas terminals. Pharmaceutical manufacturers face the most stringent requirements, with ISO 14644 cleanroom classifications mandating HEPA filtration and validated cleaning procedures. Donaldson's iCue service platform utilizes predictive analytics to schedule filter changes before pressure-drop thresholds are triggered, thereby reducing downtime.

Geography Analysis

The Asia-Pacific region held 48.55% of the global dust control systems and suppression chemicals market revenue in 2025 and is projected to grow at a 4.44% CAGR. China invested in transport and energy, mandating automated suppression on Tier-2 city projects. India’s budget, along with a particulate-reduction goal, drives the use of real-time monitors and polymeric sprays at sites in Delhi, Mumbai, and Bengaluru. Indonesia’s nickel surge and Thailand’s corridor projects add steady chemical demand.

North America and Europe advance at a steadier pace. The United States PM2.5 standard triggers the use of enclosed conveyors at coal and quarry sites. Canada’s mines in Quebec monetize lignin-based dust cuts through provincial carbon credits. Europe’s revised directive spurs retrofits across cement clusters in Germany, Poland, and Spain, while Euro 7 rules recruit road contractors into chemical procurement.

South America grows on mining activity. Vale applied acrylic crusting in Minas Gerais, halving watering costs. Argentina’s lithium triangle attracts capital with hygroscopic suppressants mandated under community pacts. In the Middle East and Africa, Saudi Arabia’s NEOM and post-World Cup projects in the Gulf utilize bio-based chemicals to conserve desalinated water. South African platinum mines are adopting polymer treatments that reduce watering costs.

Competitive Landscape

The dust control systems and suppression chemicals industry is moderately fragmented. White-space opportunities include carbon-credit monetization, chloride-free bio-suppressants, and AI dosing platforms. Niche formulators test xanthan hydrogels that match polymer strength at a lower cost, although durability beyond six months remains unverified. The technology bifurcation is clear: tier-1 miners and pharmaceutical plants deploy machine-learning dosing, while tier-2 contractors still rely on manual tankers, leaving room for suppliers with retrofit-friendly modules.

Dust Control Systems And Suppression Chemicals Industry Leaders

Ecolab

Quaker Houghton (Quaker Chemical Corporation)

Veolia

Borregaard

Hexion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Borregaard committed NOK 490 million to expand its Sarpsborg lignin-biopolymer capacity by up to 10% by 2027, with incremental output expected from late 2026. The investment specifically targets increasing capacity for lignin-based biopolymers, which are the key ingredient in their dust suppression product, Dustex.

- March 2024: Camfil Air Pollution Control (APC) has unveiled its newest offering, the Gold Series Timer (GST), an innovative-edge dust collection controller. The GST serves as a straightforward yet powerful tool for managing pulse-jet cleaning in various industrial dust collection systems, such as baghouses. With its state-of-the-art design, the GST provides an intuitive and easily implementable solution for pulse-jet cleaning in industrial dust collection systems.

Global Dust Control Systems And Suppression Chemicals Market Report Scope

Dust control systems and suppression chemicals are a set of solutions that are extensively deployed to remove emissions and dust particles/pollutants from the air or water.

The dust control systems and suppression chemicals market is segmented by type, end-user industry, and geography. By type, the market is segmented into chemical type and system type. The market is further segmented by chemical type, comprising lignin sulfonate, calcium chloride, magnesium chloride, asphalt emulsions, oil emulsions, polymeric emulsions, and other chemical types. By system type, the market is segmented into dry collection and wet suppression. By end-user industry, the market is segmented into mining, construction, food and beverage, oil and gas, petrochemical, pharmaceutical, and other end-user industries. The report also covers the market sizes and forecasts for the dust control systems and suppression chemicals market in 28 countries across major regions. For each segment, market sizing and forecasting have been conducted based on revenue (USD).

| By Chemical Type | Lignin Sulfonate |

| Calcium Chloride | |

| Magnesium Chloride | |

| Asphalt Emulsions | |

| Oil Emulsions | |

| Polymeric Emulsions | |

| Other Chemical Types | |

| By System Type | Dry Collection |

| Wet Suppression |

| Mining |

| Construction |

| Food and Beverage |

| Oil and Gas and Petrochemical |

| Pharmaceutical |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Type | By Chemical Type | Lignin Sulfonate |

| Calcium Chloride | ||

| Magnesium Chloride | ||

| Asphalt Emulsions | ||

| Oil Emulsions | ||

| Polymeric Emulsions | ||

| Other Chemical Types | ||

| By System Type | Dry Collection | |

| Wet Suppression | ||

| By End-user Industry | Mining | |

| Construction | ||

| Food and Beverage | ||

| Oil and Gas and Petrochemical | ||

| Pharmaceutical | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the dust control systems and suppression chemicals market?

The market is expected to reach USD 15.86 billion by 2026.

What is the market's expected growth rate through 2031?

It is forecast to register a 4.12% CAGR to reach USD 19.41 billion.

Which region contributes nearly half of global revenue?

The Asia-Pacific region holds 48.55% of 2025 revenue and leads the growth.

Which end-user segment is both the largest and the fastest growing?

Construction commands 35.28% of 2025 demand and is set to expand at a 4.61% CAGR.

Which chemicals are gaining favor where chloride corrosion is a concern?

Lignin sulfonate and acrylic polymer emulsions are preferred for non-corrosive performance.

Page last updated on: