Domestic Booster Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

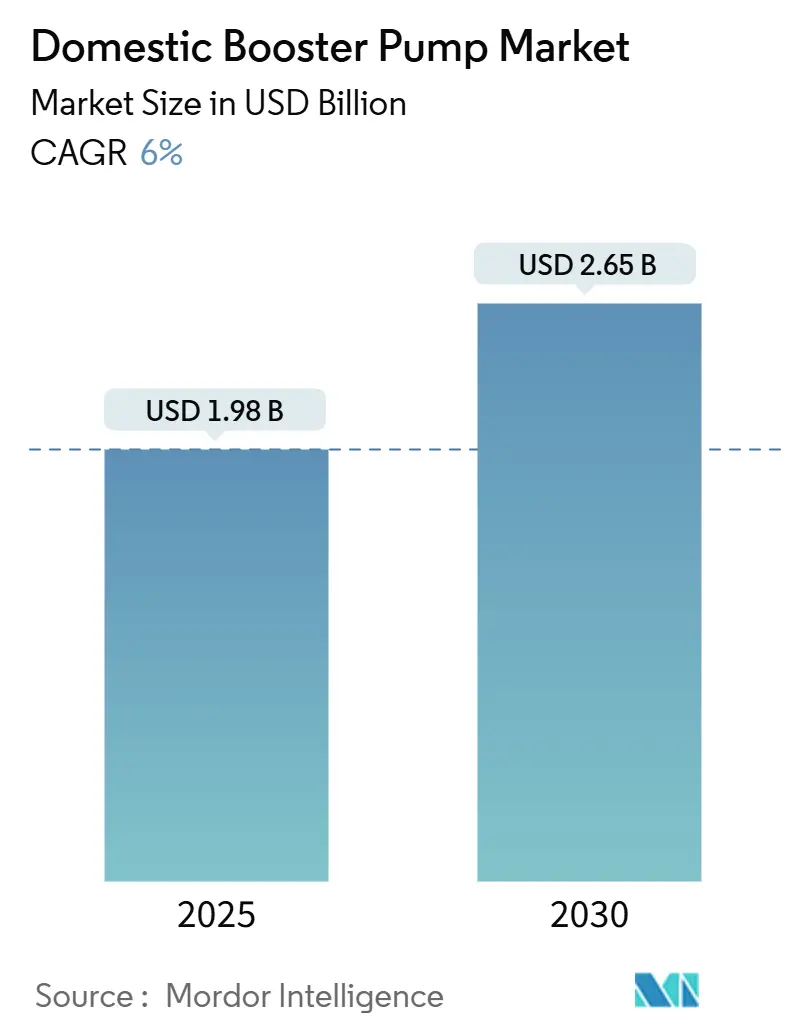

| Market Size (2025) | USD 1.98 Billion |

| Market Size (2030) | USD 2.65 Billion |

| Growth Rate (2025 - 2030) | 6.00% CAGR |

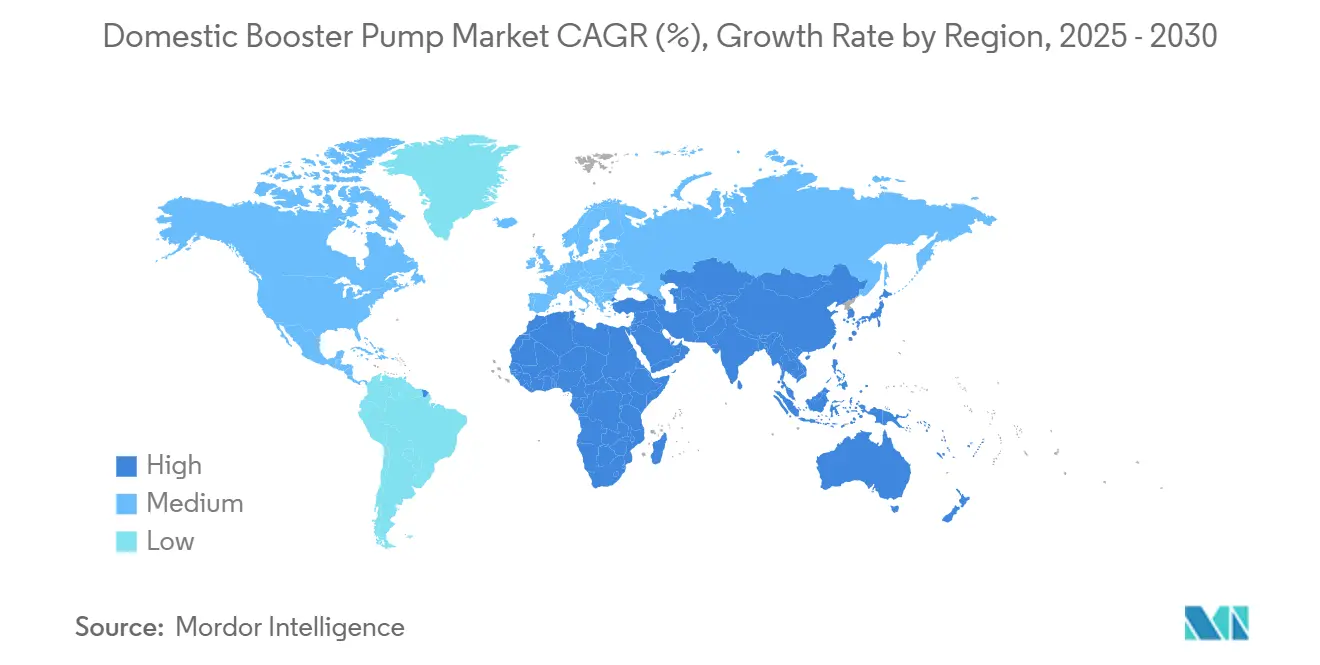

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Domestic Booster Pump Market Analysis by Mordor Intelligence

The domestic booster pumps market size reached USD 1.98 billion in 2025 and is projected to touch USD 2.65 billion in 2030, reflecting a 6.0% CAGR over the forecast period. Today, homeowners expect steady shower pressure, while many municipal networks struggle to deliver more than 40 psi, especially in dense suburbs and high-rise apartments. Aging water mains in North America and Europe, rapid urbanization in Asia-Pacific and the Middle East, and the spread of rooftop solar-water-heating systems are converging to lift replacement and first-install demand. IoT-ready pumps that communicate with smartphones are helping residents cut energy bills by up to 30 % through variable-speed operation, making connectivity a decisive buying factor. In parallel, the supply chain is shifting; e-commerce storefronts and big-box DIY chains now stock plug-and-play packages that let owners size, purchase, and install a pressure solution without a plumber, widening the addressable user base.

Key Report Takeaways

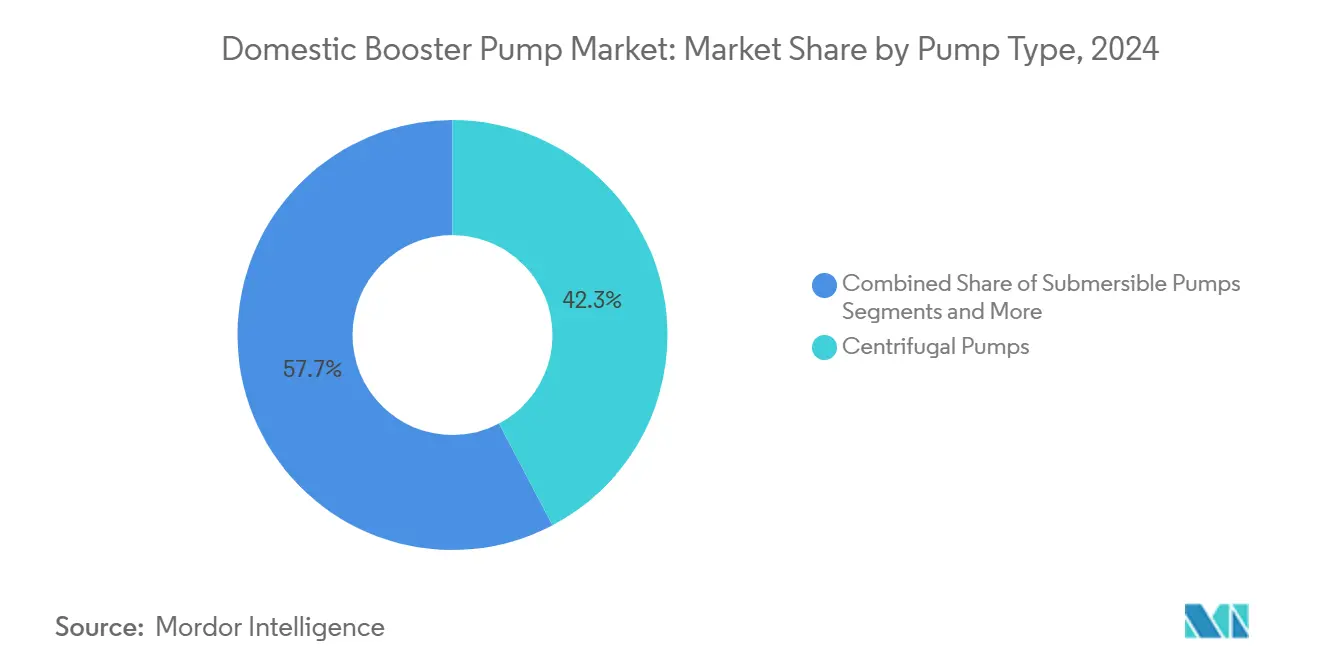

- By pump type, centrifugal models led with 42.3 % domestic booster pumps market share in 2024, while inline circulators are set to expand at a 12.40 % CAGR through 2030.

- By power rating, 1–3 HP units commanded 48.1 % of the domestic booster pumps market size in 2024 and below-1 HP pumps are advancing at an 11.20 % CAGR to 2030.

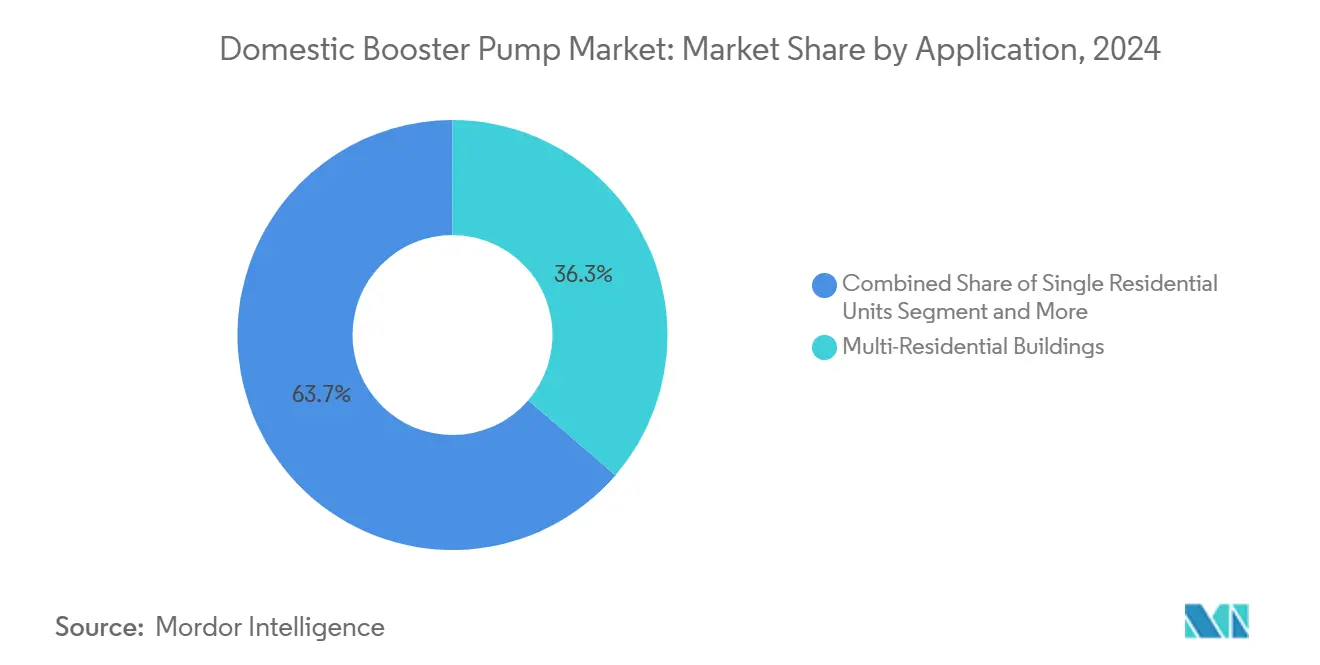

- By application, multi-residential buildings accounted for 36.3 % of demand in 2024; single residential units are forecast to post the fastest 10.80 % CAGR to 2030.

- By distribution channel, retail captured 44.1 % revenue in 2024, but e-commerce is accelerating at a 14.30 % CAGR through 2030.

- By geography, Asia-Pacific captured 38.2% revenue in 2024, but Africa is accelerating at a 13.50% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Domestic Booster Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban high-rise construction | +1.8% | Asia-Pacific, Middle East, North America urban cores | Medium term (2-4 years) |

| Growth in private rooftop solar water-heating adoption | +0.9% | Global, with concentration in Europe, India, China | Medium term (2-4 years) |

| Adoption of IoT-enabled smart pumps | +1.2% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Tightening municipal water-pressure standards | +1.0% | North America, Europe, select Middle East jurisdictions | Long term (≥ 4 years) |

| Rapid expansion of organized DIY retail chains | +0.7% | North America, Europe, Urban Asia-Pacific | Short term (≤ 2 years) |

| Green-building certification incentives | +0.6% | North America, Europe, select Asia-Pacific cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban High-Rise Construction

Tower living in Chinese, Indian, and Gulf cities now dominates residential starts, yet municipal gravity networks rarely push water much higher than the fifth floor. Developers are therefore specifying multi-stage centrifugal sets with heads above 100 m to guarantee shower performance on upper stories. Saudi Arabia alone approved more than USD 14 billion of water contracts in 2024 that feed new apartment clusters, accelerating packaged-set demand. Suppliers with factory-built skids and variable-speed drives capture most tower projects because consulting engineers prefer pre-certified, space-saving designs that simplify vertical piping layouts. The knock-on effect is robust OEM order backlogs that extend through 2027, particularly for manufacturers with regional service depots.

Growth in Private Rooftop Solar-Water-Heating Adoption

Households in India and southern Europe continue to pair solar thermal panels with below-1 HP circulators that lift hot water from rooftop tanks to ground-floor bathrooms. Compatibility with photovoltaic controllers and low idle watt draw rank above flow rate when owners choose a unit, since utility tariffs reward daytime self-consumption. Pump makers are bundling booster packages with collectors and storage tanks to capture the full spend and to upsell remote monitoring. As electricity rates rise, subsidy programs steer single-family homeowners toward these integrated kits, giving compact pumps a double-digit growth runway.

Adoption of IoT-Enabled Smart Pumps

Every major brand now embeds pressure, flow, and vibration sensors inside its domestic line, enabling predictive maintenance alerts on a homeowner’s phone. Xylem tags its residential boosters to the company’s cloud, where algorithms tweak speed set-points to shave energy costs by as much as 30 %. Grundfos pairs Bluetooth modules with its GO app so residents can commission the unit in under five minutes and receive automatic freeze warnings. The ability to validate performance data is also easing warranty claims, trimming service dispatch times. These connected features create subscription revenue streams—a value shift from hardware margin to SaaS-style monitoring contracts.

Tightening Municipal Water-Pressure Standards

Regulators now codify minimum residual pressures to protect hygiene and fire safety. Texas enforces a 20 psi floor during emergencies, compelling many homeowners in older suburbs to add domestic boosters when peak-hour pressure dips[1]Texas Commission on Environmental Quality, “Fire-Flow Safety Standards,” tceq.texas.gov. Massachusetts plumbing code lists fixture flow thresholds up to 45 psi for flush valves, again pushing remodelers toward pump retrofits. LEED guidance tests faucets at 60 psi, so builders aiming for points often install compact variable-speed sets to meet the benchmark while maintaining water-efficiency fixtures. Codes additionally require low-pressure cut-off switches to prevent back-siphon contamination, raising the bill of materials but anchoring long-term public-health benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile stainless-steel prices | -1.1% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Counterfeit low-cost imports in Asia-Pacific and Africa | -0.8% | Asia-Pacific, Africa, select Middle East markets | Medium term (2-4 years) |

| High replacement cost versus pressure regulators | -0.5% | North America, Europe mature markets | Long term (≥ 4 years) |

| Grid-electricity shortages in developing regions | -0.6% | Sub-Saharan Africa, South Asia, select Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Stainless-Steel Prices

Pump casings and impellers rely on grades 304 and 316. Base-metal swings therefore decide OEM margin. European hot-rolled 304 averaged EUR 2,207 per t in February 2025 and slid to a forecast EUR 2,054 by June, yet the multi-year range exceeds 30 %[2]MEPS International, “European Stainless Steel Price Forecasts,” mepsinternational.com . Franklin Electric cites the same volatility as a headwind that price surcharges only partly offset. Buyers of entry-level models are sensitive to even a USD 20 list increase, so any sustained upturn risks demand deferral.

Counterfeit Low-Cost Imports in Asia-Pacific and Africa

Unauthorized factories ship look-alike boosters that lack CE or ISO stamps and often use thin-gauge sheet, leading to failures within one year. Informal markets and online listings blur authenticity, trapping homeowners in costly replacements and tarnishing reputable brands. Wilo and Kirloskar now engrave QR codes on nameplates that link to warranty registration pages, helping inspectors and buyers verify lineage. Broader enforcement remains uneven, leaving certified suppliers to redouble educational campaigns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Inline Circulators Gain on Residential Retrofits

Centrifugal designs accounted for 42.3 % of domestic booster pumps market share in 2024 thanks to their proven reliability and broad service network. Inline circulators, however, are forecast to expand at a 12.40 % CAGR because their slender form fits tight utility rooms. The Wilo-CO MVI retrofit in a Florida high-rise demonstrated noise and energy gains that resonate with condominium boards[3]Wilo USA LLC, “Florida High-Rise Retrofit Newsletter,” wilo.com . Submersibles address rural borewells yet remain niche in urban contexts given higher maintenance overhead.

The domestic booster pumps market size for inline circulators is projected to rise from USD 0.57 billion in 2025 to USD 1.03 billion in 2030, reflecting escalating owner-driven retrofits. Motor advances to IE5 efficiency and built-in variable-speed drives cut consumption enough to meet emerging household energy codes, strengthening the segment’s long-term appeal.

By Power Rating: Compact Units Surge in Single-Home Retrofits

Units rated 1–3 HP represented 48.1 % of 2024 revenue, balancing flow and cost for most multi-bath apartments. Pumps under 1 HP, though, are registering an 11.20 % CAGR as aging single-family housing stock struggles with declining street pressure. Kirloskar’s autoprime series from 0.33 HP upward carries India’s BEE five-star badge, saving electricity for price-sensitive owners.

Below-1 HP domestic booster pumps market size is expected to double by 2030, buoyed by solar-water-heating tie-ins and DIY installs sold through e-commerce kits. Conversely, above-3 HP units stay limited to luxury villas and large condominiums that run central booster farms, capping their share.

By Application: Single Residential Units Accelerate on Aging Housing Stock

Multi-family complexes still formed 36.3 % of demand in 2024, largely through packaged skids with dual pumps and duty-standby logic. Yet single homes will register the fastest 10.80 % CAGR as water-main deterioration lowers street pressure in mature suburbs. Residents adopt compact, plug-and-play sets to regain 50–60 psi at showers and to power lawn sprinklers.

From a revenue lens, the domestic booster pumps market size in single-unit dwellings is forecast to reach USD 1.05 billion by 2030. Green-retrofit rebates in Europe and state clean-water grants in the U.S. widen affordability, while connected-pump analytics reassure users with leak detection and freeze alerts.

By Distribution Channel: E-Commerce Disrupts Traditional Plumbing Wholesalers

Retail shelves at Home Depot, Lowe’s, and B&Q captured 44.1 % of 2024 turnover, but online portals grew even faster. E-commerce is projected to log a 14.30 % CAGR as filters, sizing calculators, and next-day shipping compress decision cycles for millennials comfortable with self-install videos. Manufacturers leverage direct-to-consumer sites to collect homeowner data, upsell service plans, and sidestep distributor margins.

Despite the surge, complex apartment booster farms still favor direct OEM quotes because engineers need hydraulic calculations, redundancy layouts, and commissioning services. Consequently, channel diversity persists even as online volume climbs.

Geography Analysis

Asia-Pacific garnered 38.2 % of 2024 revenue, anchored by high-rise construction in China and India and government subsidies for water-efficient buildings. Local production hubs in Jiangsu and Karnataka enable rapid customization, while middle-class expansion lifts unit sales in Vietnam, Indonesia, and the Philippines. North America shows steady replacement demand as 1960s suburban mains corrode; Grundfos’s new Texas plant will cut lead times nationally once lines start in 2027.

Europe’s mature housing stock necessitates refurbishments that often pair variable-speed boosters with smart meters to earn LEED or BREEAM points. Municipal codes in Germany and France now instruct designers to prove 60 psi at top-floor fixtures, keeping retrofit pipelines full. The domestic booster pumps market share across Europe is expected to remain stable, yet revenue rises with premium smart-pump content.

Africa represents the fastest trajectory at a 13.50 % CAGR through 2030 as urban households gain piped connections and development banks underwrite new water grids. South Africa, Kenya, and Nigeria lead retail sales, although grid-electricity gaps push suppliers to bundle solar panels and lithium packs. Middle Eastern demand rides record desalination and pipeline investment, funneling high-head orders into coastal towers from Dubai to Jeddah. Latin America and smaller emerging regions post mid-single-digit growth constrained by volatile currencies yet bolstered by rising e-commerce penetration.

Competitive Landscape

The domestic booster pumps market remains moderately concentrated. Global majors—Grundfos, Xylem, Wilo, Franklin Electric, Pentair, and KSB—control upward of 55 % of revenue, leveraging multichannel reach, R&D heft, and long warranties. Grundfos is investing millions in Brookshire, Texas to double U.S. production capacity and localize supply. Xylem integrates its boosters into a unified digital platform that spans meters, treatment, and pressure systems, reinforcing cross-selling to residential plumbers.

Strategic moves focus on intelligent controls and localized assembly. Wilo’s purchase of QuantumFlo added UL-listed pump packs and seismic-certified panels, which are popular in U.S. residential towers. Pentair complements water boosters with heat-pump acquisitions to widen its home-comfort basket. Regional challengers—Kirloskar in India and emerging solar-pump specialists—compete on price and after-sales reach; Kirloskar’s IoT dashboard, KirloSmart, now covers more than 1,400 domestic units.

Technology leadership gravitates toward IE5 motors, adaptive control loops, and cybersecurity-hardened firmware. As sensors commoditize, brands shift to service contracts, promising uptime guarantees and energy-savings audits for a monthly fee. Counterfeit erosion in Asia-Pacific and Africa spurs OEMs to adopt laser-etched QR authentication and to lobby customs for stricter checks.

Domestic Booster Pump Industry Leaders

Grundfos Holding A/S

Xylem Inc.

Wilo SE

Franklin Electric Co., Inc.

Pentair plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Grundfos announced a multi-million-dollar expansion of its Brookshire, Texas plant, with first residential lines slated for Q4 2027, aiming to double U.S. business by 2030.

- April 2025: Ebara Corporation introduced the wall-cabinet “PURE FRESSURE” booster series targeting compact residential spaces.

- March 2025: Saudi Water Partnership Company awarded the USD 2.2 billion Jubail-Buraydah pipeline to a local consortium, adding 650,000 m³/day of capacity for new housing zones.

- February 2025: Franklin Electric posted USD 1.184 billion 2024 water-systems revenue and outlined a 2025 focus on residential solutions.

Global Domestic Booster Pump Market Report Scope

The Domestic Booster Pump Market Report is Segmented by Pump Type (Centrifugal Pumps, Submersible Pumps, and More), Power Rating (Below 1 HP, 1 – 3 HP, and Above 3 HP), Application (Single Residential Units, Multi-Residential Buildings, and More), Distribution Channel (Direct Sales (OEM), Retail and E-Commerce), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) and for all the Above Segments.

| Centrifugal Pumps |

| Submersible Pumps |

| Inline Circulator Pumps |

| Others |

| Below 1 HP |

| 1 – 3 HP |

| Above 3 HP |

| Single Residential Units |

| Multi-Residential Buildings |

| HVAC Systems |

| Water Heaters / Solar Water Heating |

| Direct Sales (OEM) |

| Retail (Home-Improvement Stores) |

| E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pump Type | Centrifugal Pumps | |

| Submersible Pumps | ||

| Inline Circulator Pumps | ||

| Others | ||

| By Power Rating | Below 1 HP | |

| 1 – 3 HP | ||

| Above 3 HP | ||

| By Application | Single Residential Units | |

| Multi-Residential Buildings | ||

| HVAC Systems | ||

| Water Heaters / Solar Water Heating | ||

| By Distribution Channel | Direct Sales (OEM) | |

| Retail (Home-Improvement Stores) | ||

| E-commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the domestic booster pumps market in 2025 and how fast is it growing?

The domestic booster pumps market size stands at USD 1.98 billion in 2025 and is set to expand at a 6.0% CAGR to USD 2.65 billion by 2030.

Which pump type is gaining the most momentum in residential retrofits?

Inline circulator boosters are registering a 12.40% CAGR through 2030 because their slim profile fits tight utility spaces and they ship with variable-speed drives.

Why are below-1 HP models becoming popular among homeowners?

Aging suburban mains and rooftop solar-water-heater loops need modest flow at low cost, making compact, single-phase boosters ideal for do-it-yourself installs.

What is driving double-digit growth in e-commerce sales of domestic booster pumps?

Big-box chains and manufacturer web shops now offer sizing calculators, how-to videos, and next-day delivery, letting owners bypass plumbing wholesalers and install units themselves.

Which region is expected to record the fastest growth to 2030?

Africa is forecast to grow at 13.50% CAGR, propelled by rapid urbanization, new piped-water connections, and multilateral funding support for residential infrastructure.

How are leading brands adding value beyond the pump hardware?

Firms such as Xylem and Grundfos bundle IoT telemetry, predictive maintenance apps, and extended warranties, shifting revenue toward recurring service contracts that enhance homeowner experience.

Page last updated on: