Dendritic Cell Cancer Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

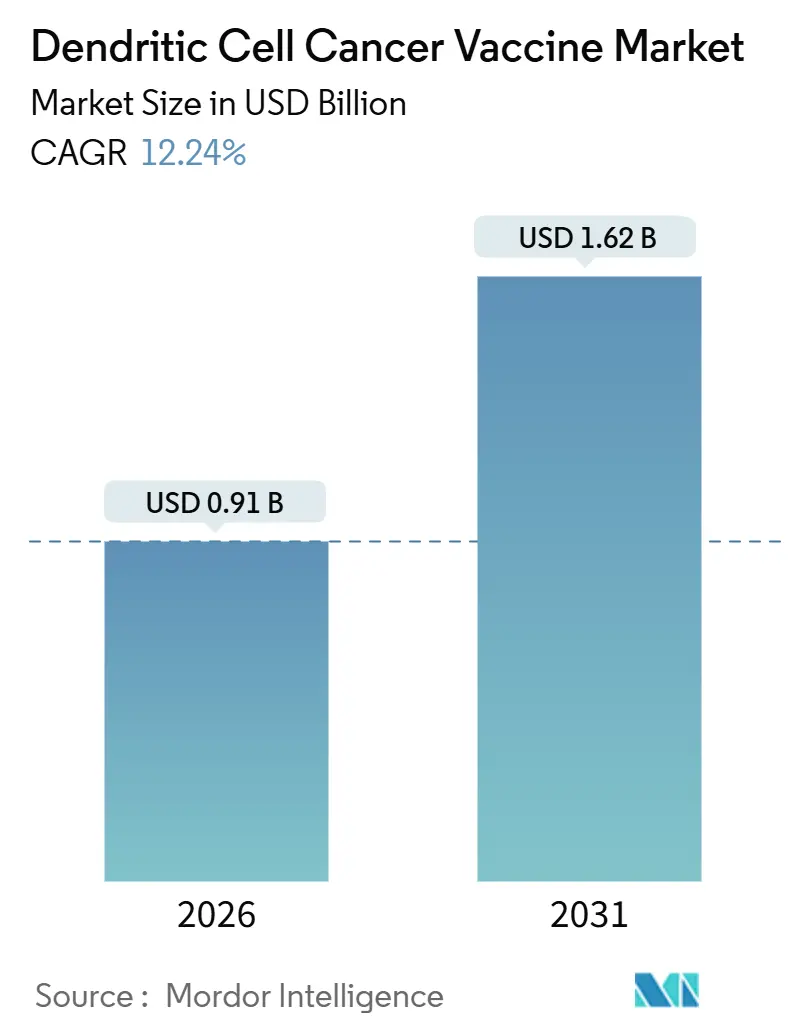

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 12.24% CAGR |

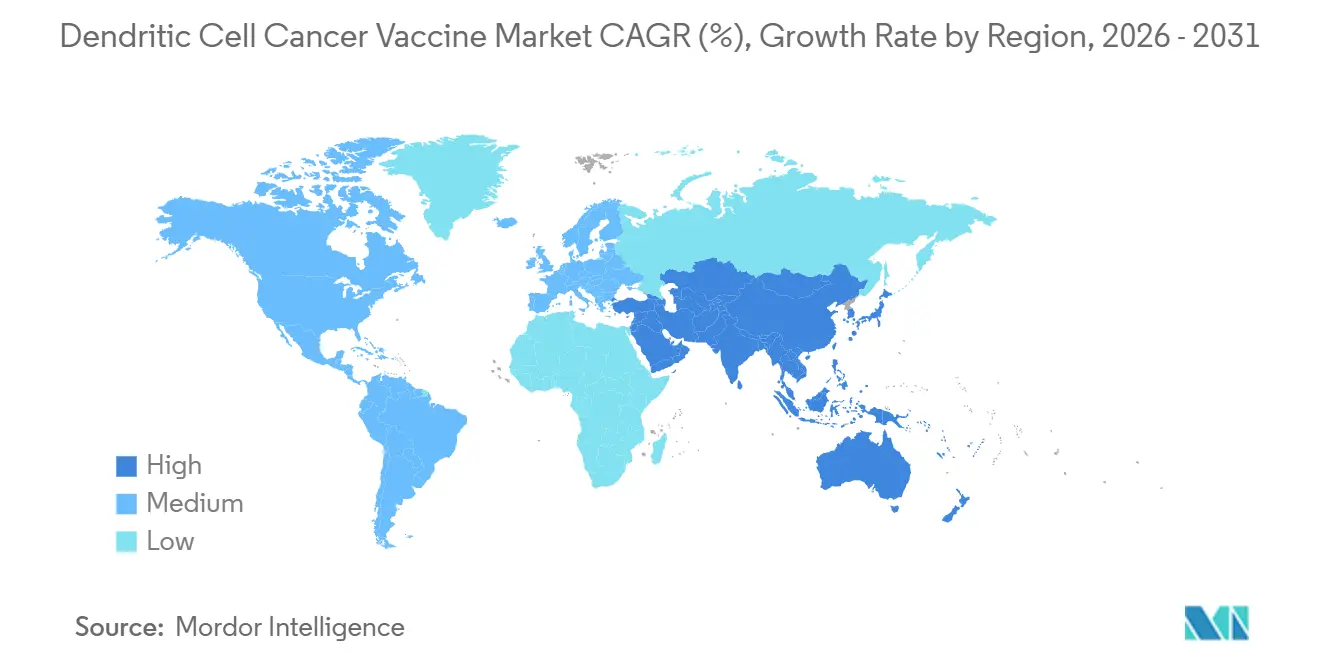

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dendritic Cell Cancer Vaccine Market Analysis by Mordor Intelligence

The Dendritic Cell Cancer Vaccine Market size is estimated at USD 0.91 billion in 2026, and is expected to reach USD 1.62 billion by 2031, at a CAGR of 12.24% during the forecast period (2026-2031).

This momentum reflects a pivotal shift toward closed, semi-automated bioreactor workflows and AI-driven antigen selection that lower cost per batch and shorten vein-to-vein timelines, two constraints that limited first-generation autologous platforms. Manufacturing labor, which once represented up to one-half of total production cost, is falling as single-use, software-guided systems integrate cell isolation, differentiation, and antigen loading in sealed modules that cut operator hands-on time by 25% to 50%. Regulatory agencies in Japan, China, and the United Kingdom are simultaneously offering conditional or accelerated pathways that shorten the development cycles of neo-antigen dendritic cell vaccines, expanding the addressable patient pool and enticing venture capital into off-the-shelf concepts. Competitive pressure from faster-acting CAR-T cells and bispecific antibodies remains intense; however, dendritic cell platforms continue to differentiate through multi-antigen presentation, addressing tumor heterogeneity in solid tumors such as glioblastoma, where other modalities face microenvironmental barriers. Market opportunity, therefore, hinges on proven cost containment, validated potency assays, and combination regimens that convert robust T-cell priming into durable clinical benefit.

Key Report Takeaways

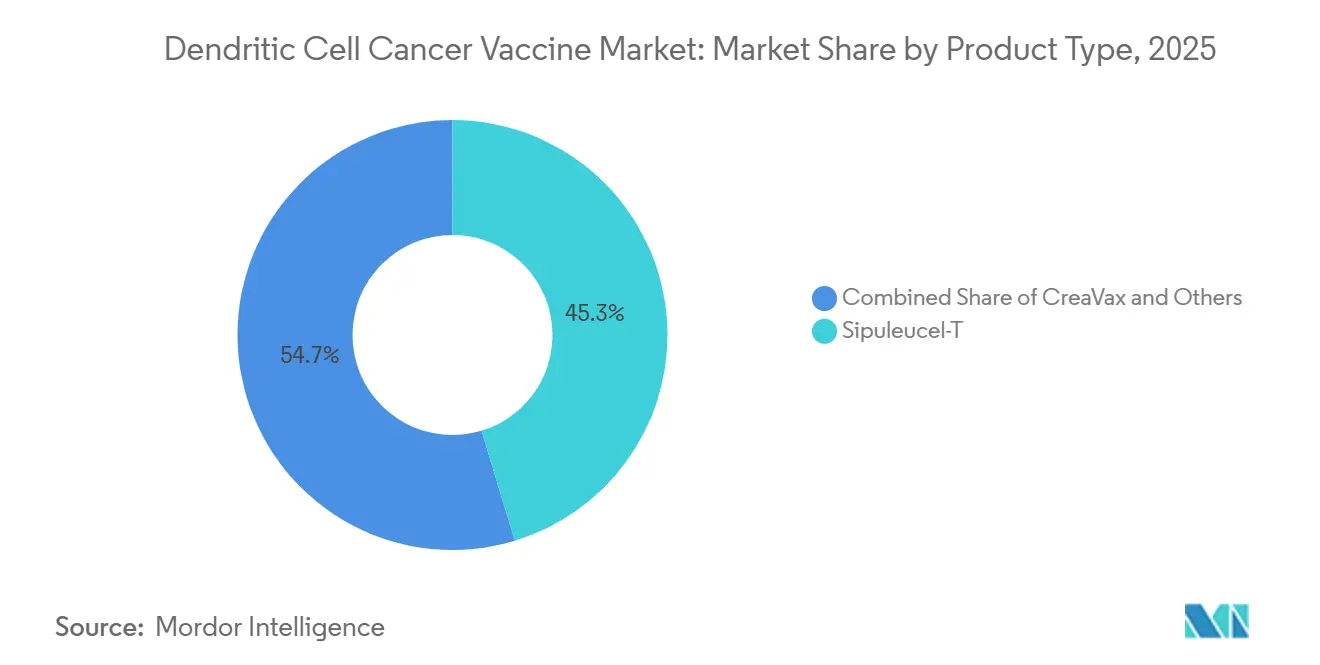

- By product type, sipuleucel-T held 45.31% of dendritic cell cancer vaccine market share in 2025, while CreaVax is forecast to grow at a 6.48% CAGR to 2031.

- By cancer type, prostate applications dominated with 36.07% revenue share in 2025; glioblastoma is expected to expand at a 7.12% CAGR through 2031.

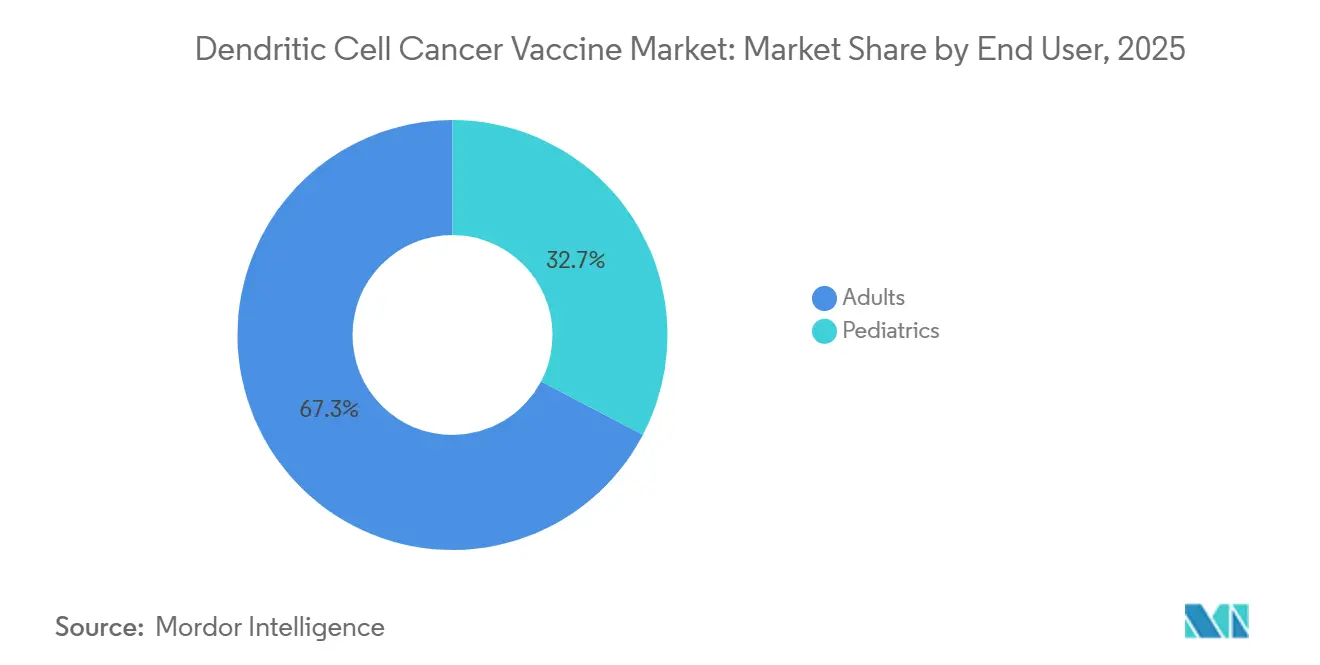

- By end user, adults represented 67.32% of 2025 demand, whereas pediatric indications are on track for an 8.87% CAGR.

- By geography, North America led with 44.03% share in 2025, yet Asia-Pacific is projected to advance at a 9.39% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dendritic Cell Cancer Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Clarity for Neo-Antigen DC Vaccines | +2.1% | Global, with early traction in Japan, China, EU conditional pathways | Medium term (2-4 years) |

| Integration of Semi-Automated GMP Bioreactors Cuts Cost/Time | +2.8% | North America & EU manufacturing hubs; APAC scale-up in China, Singapore | Short term (≤ 2 years) |

| Increase In Combination-Trial Success with Anti-PD-1 Agents | +1.9% | Global, concentrated in U.S. NCI-designated centers, EU academic consortia | Medium term (2-4 years) |

| Rapid Adoption of AI-Guided Epitope Selection Platforms | +1.6% | North America & EU early adopters; APAC following with domestic AI platforms | Medium term (2-4 years) |

| Venture Funding Surge for Off-The-Shelf Allogeneic Products | +1.4% | North America venture ecosystems; spillover to EU and APAC | Long term (≥ 4 years) |

| National Reimbursement for Provenge in Japan & France | +1.2% | Japan, France; potential spillover to Germany, Italy, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Clarity For Neo-Antigen DC Vaccines

Conditional approval frameworks in Japan and China now permit surrogate endpoints, such as T-cell clonal expansion or progression-free survival, reducing the time required for development programs that once required five-year overall survival data. Japan’s Pharmaceuticals and Medical Devices Agency lets regenerative medical products reach market under post-marketing surveillance obligations, while China’s 2022 chemistry, manufacturing, and controls guideline opened the door for Likang Life Sciences’ LK101 dendritic cell-mRNA candidate, cleared for trials in 2023. In Europe, the United Kingdom accepted Northwest Biotherapeutics’ DCVax-L application for a 150-day expedited review, underscoring the agency's growing comfort with external-control datasets in ultra-rare settings. Divergent evidence requirements persist the U.S. FDA still favors randomized trials—yet global developers can tailor strategies around these flexible jurisdictions to gain first-in-class footholds.

Integration Of Semi-Automated GMP Bioreactors Cuts Cost/Time

Closed, single-use bioreactors from leading suppliers integrate leukapheresis input, monocyte enrichment, differentiation, antigen loading, and maturation within a sterile cassette, eliminating clean-room transfers and trimming contamination-related batch failures to below 5%.[1]Alice Melocchi et al., “Automated manufacturing of cell therapies,” sciencedirect.com Inline sensors track pH, dissolved oxygen, and metabolite accumulation, allowing software algorithms to adjust feeds in real time and harmonize output across parallel patient lots. These engineering gains have reduced per-batch labor costs by roughly one-third and positioned autologous workflows as viable for decentralized regional centers. The National Cell Manufacturing Consortium highlighted dendritic cells as a priority cell type for automation in its technology roadmap, and early commercial rollouts confirm that operator training curves are shortened when step-by-step digital work instructions replace paper batch records.[2]National Cell Manufacturing Consortium, “Achieving Large-Scale, Cost-Effective, Reproducible Manufacturing of High-Quality Cells,” cellmanufacturingusa.org

Increase In Combination-Trial Success With Anti-PD-1 Agents

A 2024 meta-analysis in glioblastoma showed that dendritic cell vaccines combined with anti-PD-1 therapy yielded a hazard ratio of 0.71 for overall survival, demonstrating that priming diverse T-cell clones can rescue checkpoint-refractory tumors. Mechanistically, dendritic cells present hundreds of peptide antigens simultaneously, broadening immune coverage and mitigating escape via antigen loss. Durable complete responses reported in early melanoma combinations with talimogene laherparepvec reinforce this synergy potential. The trend is strongest at U.S. National Cancer Institute-designated centers and EU academic consortia where apheresis infrastructure and checkpoint backbones are readily available, creating geographic clusters of translational data that accelerate regulatory acceptance.

Rapid Adoption of AI-Guided Epitope Selection Platforms

Machine-learning pipelines, such as pVACtools, integrate whole-exome sequencing with HLA typing to rank neoantigens by predicted binding affinity and immunogenicity. Clinical investigators have cut design timelines from months to days, enabling near real-time personalization that dovetails with 21-day manufacturing cycles. A real-world glioblastoma study reported a median overall survival of 31.9 months among patients receiving AI-selected peptide vaccines, far exceeding historical controls. Challenges remain—most algorithms are trained on European and East Asian HLA libraries—but initiatives to enrich under-represented alleles are underway. Commercial uptake is most advanced in North America and Europe, with Asia-Pacific companies building domestic platforms that still require clinical validation to secure regulator confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High COGS Of Autologous DC Manufacture | -1.8% | Global, most acute in North America and EU where labor and reagent costs are highest | Short term (≤ 2 years) |

| Lack of Validated Potency Biomarkers for Batch Release | -1.3% | Global, regulatory scrutiny highest in U.S. FDA and EMA jurisdictions | Medium term (2-4 years) |

| Competition From Faster-Acting CAR-T & Bispecific Antibodies | -1.1% | North America & EU where CAR-T/bispecific infrastructure is mature; emerging in APAC | Short term (≤ 2 years) |

| Skills Gap in Cell-Therapy–Qualified Workforce | -0.9% | Global, most severe in APAC and Latin America with limited GMP training programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Autologous DC Manufacture

Even with automation, the cost of goods sold for an autologous dendritic cell batch still exceeds USD 30,000 when operator compensation, GMP reagents, quality control assays, and facility overhead are tallied. Magnetic beads for monocyte isolation alone can cost more than USD 5,000 per patient, while sterility, endotoxin, and mycoplasma testing adds both expense and time. Capital outlays for modular “GMP-in-a-box” units range from USD 2 million to USD 5 million, and acceptable payback periods require annual throughput of at least 100 patient lots, a scale achievable only in centralized hubs or multi-site networks staffed by experienced operators. Reimbursement bodies in France and Germany historically extend broad coverage only if manufacturers demonstrate cost reductions approaching 40%, reinforcing cost pressure on developers.

Lack of Validated Potency Biomarkers for Batch Release

Release testing currently relies on surface markers such as CD80, CD86, and HLA-DR that correlate poorly with clinical outcomes. Regulators now require functional assays such as mixed lymphocyte reactions or IFN-γ ELISpot to demonstrate T-cell priming capacity. Yet, these methods are labor-intensive, introduce donor-to-donor variability, and extend release timelines. Academic consortia are exploring automated microfluidic platforms that sample culture supernatant and feed cytokine data into predictive models, but no consensus assay has been validated across multiple products. Without a robust potency metric, batch-to-batch comparability and lot release remain regulatory pain points that can delay approvals and trigger post-marketing surveillance audits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sipuleucel-T Leadership Faces CreaVax Momentum

Sipuleucel-T maintained a 45.31% market share in the dendritic cell cancer vaccine market in 2025, buoyed by its status as the only FDA-approved product and its long-standing Medicare coverage. Its manufacturing process, however, still requires 3-to-5-week logistics that constrain community-based adoption. CreaVax is on a 6.48% CAGR trajectory, propelled by antigen-loading protocols that cut cycle time and improve inter-batch consistency. Investigational platforms, including DCVax-L and AV-GBM-1, are advancing through late-phase trials, with DCVax-L already under expedited review in the United Kingdom based on a median overall survival of 19.3 months in newly diagnosed glioblastoma.

Second-generation products integrate AI-selected neoantigens and closed-system manufacturing, features expected to trim per-patient costs by roughly 40% and meet European health-technology assessment thresholds for broad reimbursement. The dendritic cell cancer vaccine market size for the CreaVax segment is forecast to reach USD 0.27 billion by 2031, underscoring investor confidence in platforms that deliver faster turnaround without sacrificing antigen breadth. Sipuleucel-T remains strategically important as a proof-of-reimbursement template, yet ongoing head-to-head trials will clarify whether next-generation constructs can deliver superior progression-free survival and offset competitive pressure from androgen-receptor inhibitors in prostate oncology.

By Cancer Type: Glioblastoma Ascends On Late-Phase Evidence

Prostate cancer represented 36.07% of 2025 revenue, a lead built on sipuleucel-T but tempered by only 5% penetration of U.S. metastatic castration-resistant cases. The dendritic cell cancer vaccine market for glioblastoma is poised for rapid expansion, with a 7.12% CAGR through 2031, as DCVax-L, AV-GBM-1, and ERC1671 demonstrate survival outcomes that outperform historical temozolomide benchmarks. A meta-analysis showed a hazard ratio of 0.71 for overall survival when dendritic cell vaccines were added to standard therapy in glioblastoma, an effect regulators view favorably in an indication with few alternatives.

Heterogeneity in antigen expression and limitations of the blood-brain barrier impede the efficacy of conventional antibodies and cell therapies, allowing dendritic cell platforms to exploit their multi-epitope presentation advantage. Melanoma trials have shifted toward combination regimens after the MIND-DC monotherapy failure, illustrating the platform’s need for checkpoint co-administration in immunologically “hot” tumors. Pancreatic and ovarian programs remain early-stage but are integrating data-driven antigen selection with oncolytic vectors, signaling a pipeline pivot toward solid tumors, where CAR-T penetration remains low.

By End User: Pediatric Uptake Accelerates From A Low Base

Adults accounted for 67.32% of 2025 demand, reflecting the prevalence of prostate and glioblastoma cases as well as Medicare reimbursement patterns. Pediatric enrollment, historically limited to feasibility cohorts in neuroblastoma, is expanding at an 8.87% CAGR as sarcoma and brain tumor programs generate preliminary complete responses. Manufacturing challenges specific to small blood volumes are being addressed through optimized leukapheresis protocols and higher-efficiency monocyte-capture beads, enabling adequate yield for multiple vaccine doses from a single collection. The dendritic cell cancer vaccine market share for pediatric users remains modest. Yet, societal emphasis on reducing long-term chemotherapy toxicity supports strategic investment, particularly as regulators mandate Pediatric Investigation Plans for most new oncology biologics in Europe and the United States.

Geography Analysis

North America accounted for 44.03% of revenue in 2025, supported by the reimbursement infrastructure that followed sipuleucel-T’s 2010 approval and by the highest density of GMP cell-processing laboratories worldwide. However, escalating labor costs and intensifying competition from CAR-T therapies, which generated USD 4.1 billion globally in 2023, place pressure on price-sensitive hospital systems. Developers are therefore piloting decentralized manufacturing nodes linked by cloud-based quality management systems to reduce logistics delays and expand reach into community oncology networks.

Europe delivered a balanced mid-tier contribution, with Germany, France, and the United Kingdom forming a triad of early adopters. The United Kingdom’s expedited DCVax-L review exemplifies agency willingness to accept well-curated external controls, while France’s compassionate-access program now reimburses select cellular immunotherapies at full list price, encouraging hospital uptake ahead of formal market authorization. Nonetheless, heterogeneity in national health-technology assessments and reference pricing rules continues to fragment launch planning, obliging manufacturers to pursue country-specific dossiers and value-based agreements.

Asia-Pacific is the fastest-growing territory, forecast to grow at a 9.39% CAGR, driven by China’s harmonized CMC guidance and Japan’s regenerative medicine act, which grants conditional approvals contingent on post-marketing data. Multiple domestic facilities in Beijing, Seoul, and Singapore have installed modular clean-room suites purpose-built for autologous cell therapies, yet skilled labor shortages remain acute. Government co-investment in training centers and scholarship programs aims to bridge this gap. Still, near-term throughput will depend on automated bioreactors and standardized digital workflows to compensate for limited operator pools.

Competitive Landscape

Market concentration remains moderate: one approved product captures nearly half of global revenue, while more than a dozen late-stage developers pursue differentiated constructs. Northwest Biotherapeutics leads challengers with its UK filing, positioning glioblastoma as the next commercial frontier. SOTIO Biotech, Immunicum AB, and AIVITA Biomedical each operate GMP facilities capable of supplying pivotal studies and initial regional launches. Technology convergence is evident as newcomers license closed bioreactor hardware and algorithmic epitope engines rather than building bespoke solutions, lowering entry barriers yet creating capability parity.

Strategic differentiation now hinges on the outcomes of combination trials and cost-reduction milestones. Companies integrating non-viral gene-editing or flow-electroporation platforms report 10%-25% manufacturing savings and leverage the regulatory precedent set by exa-cel to streamline CMC review. Partnerships with contract manufacturing organizations provide surge capacity while minimizing capital risk, but also concentrate know-how in a handful of specialized vendors, raising long-term supply-chain dependency concerns. Overall, first movers that secure reimbursement in Japan, China, or the United Kingdom could lock in formulary positions ahead of U.S. entrants, shaping regional adoption curves for the remainder of the decade.

Dendritic Cell Cancer Vaccine Industry Leaders

Argos Therapeutics

Batavia Biosciences

GlaxoSmithKline plc

Northwest Biotherapeutics

Dendreon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Diakonos Oncology presented personalized dendritic cell therapy data showing immune activation in recurrent glioblastoma.

- June 2025: Northwest Biotherapeutics outlined next-generation dendritic cell strategies at the New York Academy of Sciences Frontiers in Cancer Immunotherapy conference.

- May 2025: A funding round led by strategic investors positioned a clinical-stage developer to scale its dendritic cell vaccine pipeline across solid tumor indications.

- April 2024: Diakonos Oncology secured capital to initiate a Phase II trial, extending operational runway into late 2025.

Global Dendritic Cell Cancer Vaccine Market Report Scope

The Dendritic Cell Cancer Vaccine Market Report is Segmented by Product Type (CreaVax, Sipuleucel-T, Others), Cancer Type (Prostate, Melanoma, Glioblastoma, Other Cancer Types), End User (Adults, Pediatrics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| CreaVax |

| Sipuleucel-T |

| Others |

| Prostate |

| Melanoma |

| Glioblastoma |

| Other Cancer Types |

| Adults |

| Pediatrics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | CreaVax | |

| Sipuleucel-T | ||

| Others | ||

| By Cancer Type | Prostate | |

| Melanoma | ||

| Glioblastoma | ||

| Other Cancer Types | ||

| By End User | Adults | |

| Pediatrics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the dendritic cell cancer vaccine market in 2026?

The dendritic cell cancer vaccine market size is USD 0.91 billion in 2026 with a 12.24% CAGR toward 2031.

Which product currently leads global revenue?

Sipuleucel-T holds 45.31% dendritic cell cancer vaccine market share due to its first-in-class approval and U.S. reimbursement foundation.

What is driving growth in glioblastoma applications?

Late-phase data showing median overall survival above 19 months and expedited U.K. review are steering investment into glioblastoma vaccines.

Why is Asia-Pacific considered the fastest-growing region?

Harmonized CMC guidelines in China and conditional approval frameworks in Japan lift regulatory barriers, supporting a 9.39% CAGR through 2031.

What cost target unlocks broader reimbursement in Europe?

Health-technology bodies signal that cutting per-patient manufacturing expense by roughly 40% positions dendritic cell vaccines for broader coverage.

Page last updated on: