Cybersecurity For Retail and E-commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 40.49 Billion |

| Market Size (2031) | USD 67.34 Billion |

| Growth Rate (2026 - 2031) | 10.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity For Retail and E-commerce Market Analysis by Mordor Intelligence

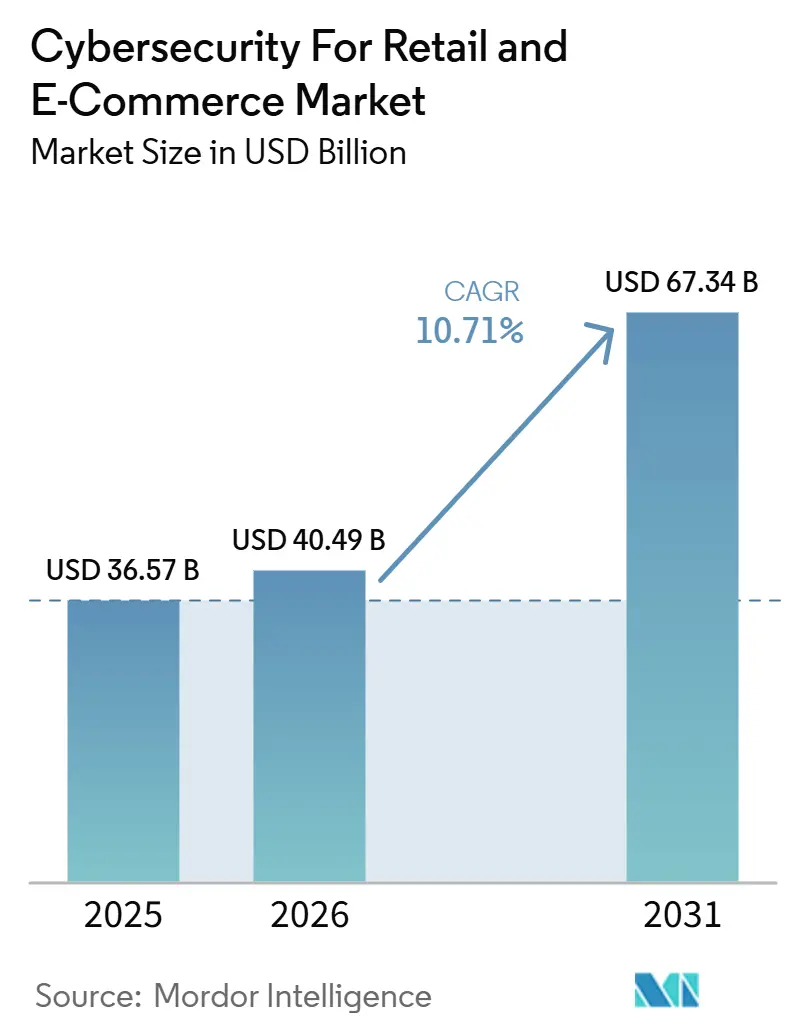

The Cybersecurity For Retail and E-commerce Market size is projected to be USD 36.57 billion in 2025, USD 40.49 billion in 2026, and reach USD 67.34 billion by 2031, growing at a CAGR of 10.71% from 2026 to 2031. The Cybersecurity For Retail and E-commerce Market is being pushed by a threat environment that is broader than in prior cycles, with account fraud, bot abuse, API attacks, and cloud workload exposure all rising at the same time. Retailers are no longer treating cybersecurity as a narrow IT control, because fraud costs, checkout disruption, and customer trust loss now affect revenue more directly. The Cybersecurity For Retail and E-commerce Market is also benefiting from a clear shift away from isolated tools toward integrated platforms that combine identity, fraud prevention, cloud protection, and application security. Competitive activity is centered on platform consolidation for large retailers and specialized fraud and bot protection for merchant-specific use cases. The strongest near-term opportunities in the Cybersecurity For Retail and E-commerce Market sit in mid-sized retailers, cloud-native deployments, agentic AI security, and payment security tied to tokenization and conversion performance.

Key Report Takeaways

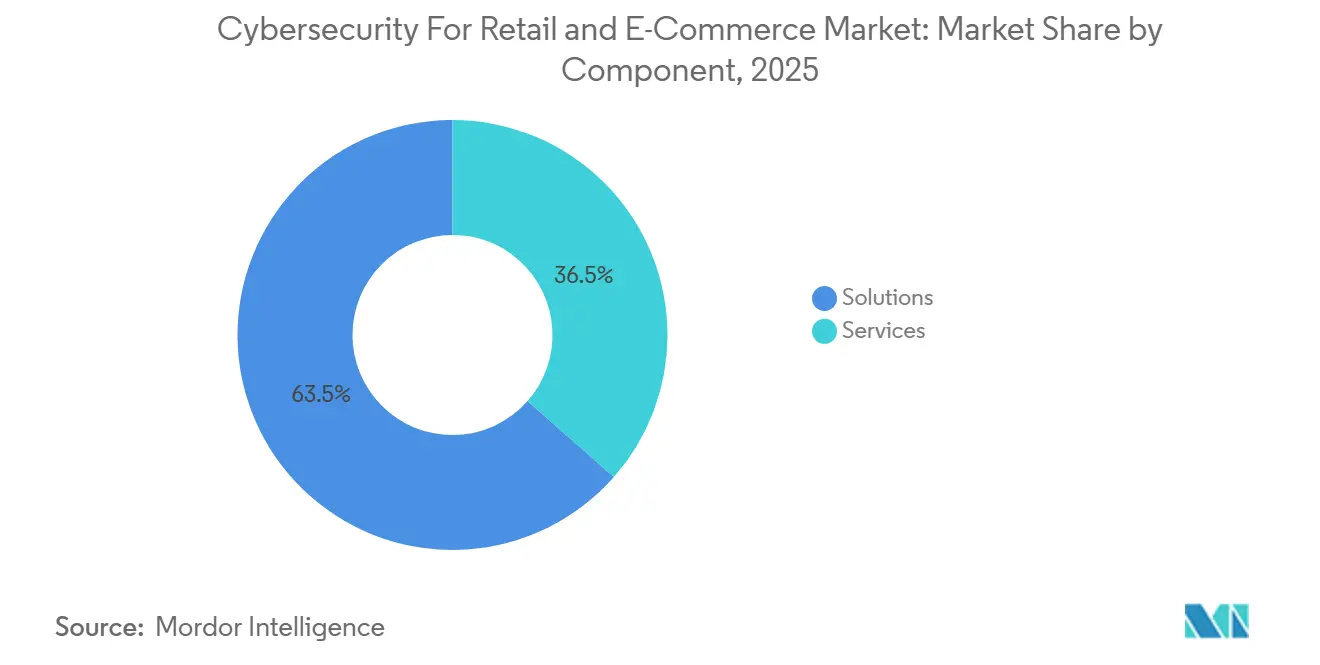

- By component, solutions held 63.51% of the Cybersecurity For Retail and E-commerce Market in 2025, while services are projected to expand at a 15.97% CAGR through 2031.

- By security type, application security accounted for a 26.73% share in 2025, while cloud security is expected to record the highest CAGR at 17.61% through 2031.

- By deployment mode, cloud captured 67.49% share in 2025 and is also projected to remain the fastest-growing deployment model at a 16.63% CAGR to 2031.

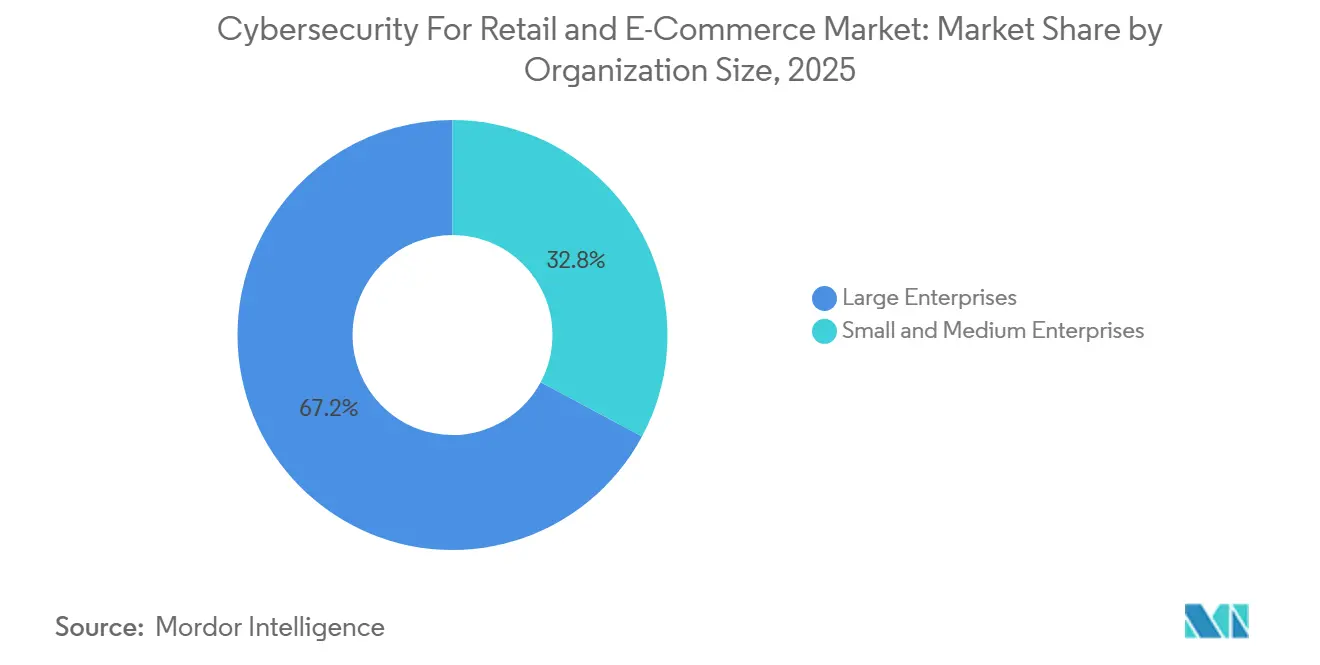

- By organization size, large enterprises held 67.17% of the Cybersecurity For Retail and E-commerce Market in 2025, while SMEs are projected to expand at a 16.27% CAGR through 2031.

- By application, payment security led with a 24.96% share in 2025, while bot mitigation is projected to grow at the fastest CAGR of 18.43% through 2031.

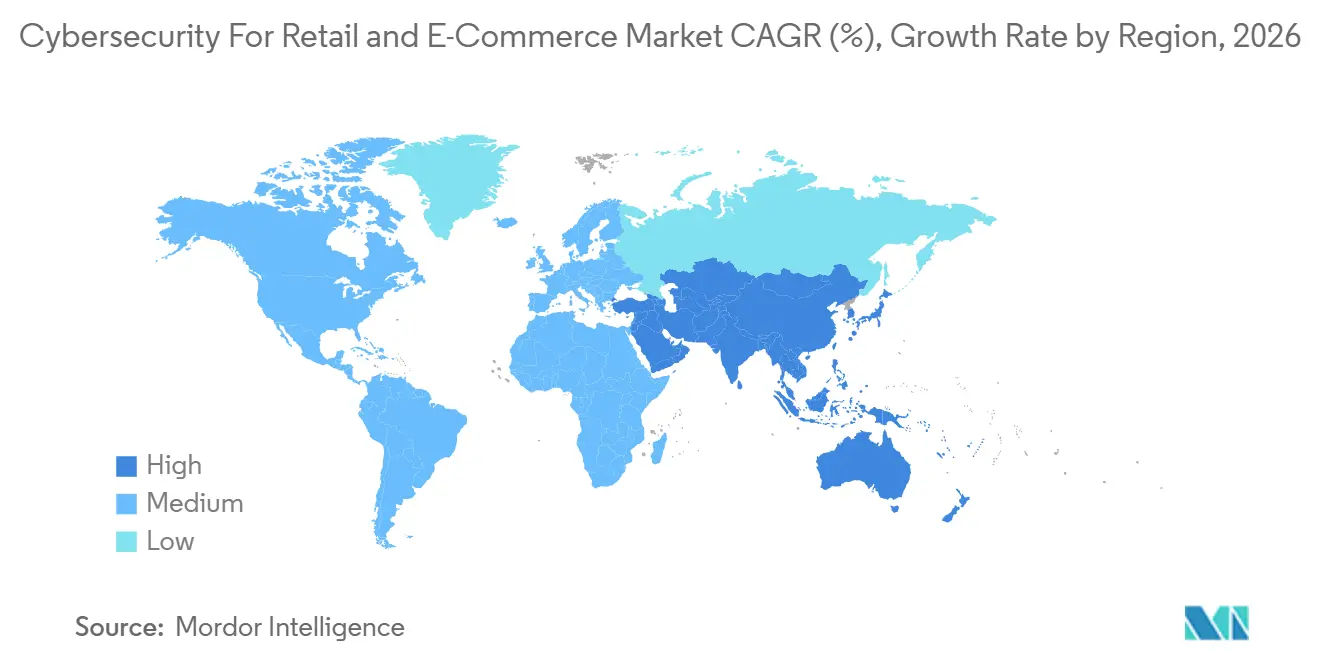

- By geography, North America held 38.19% share in 2025, while Asia-Pacific is projected to expand at the highest CAGR of 17.64% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cybersecurity For Retail and E-commerce Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Frequency of Retail Account Fraud and Data Breaches | +3.2% | Global | Short term (≤ 2 years) |

| AI-Assisted Fraud and Bot Operations | +2.8% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Omnichannel Retail and Attack Surface Complexity | +2.1% | Global | Medium term (2-4 years) |

| Mainstreaming of Cloud-Native Retail Platforms | +1.5% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Tokenization and Secure Payment Frameworks | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Increasing Board-Level Focus on Cybersecurity Governance | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Frequency of Retail Account Fraud and Data Breaches

Retail remains a favored target because merchants process large transaction volumes, hold dense pools of credentials, and face predictable traffic spikes during major shopping periods. Annual retail security incidents rose to 837 in 2024 from 725 in 2023, and confirmed breaches increased to 419 from 369 over the same period.[1]Retail and Hospitality Information Sharing and Analysis Center, “CISO Benchmark Report Finds AI Driving New Era of Cybersecurity Risk and Investment,” RH-ISAC, rhisac.org The financial burden is also getting heavier, with LexisNexis Risk Solutions reporting that total fraud costs reached USD 5.13 for every USD 1 of direct loss for United States retail and e-commerce businesses in 2026. Credential phishing still remains a large part of the threat mix, and the FBI received 193,407 phishing complaints in 2024.[2]Federal Bureau of Investigation Internet Crime Complaint Center, “2024 IC3 Annual Report,” IC3, ic3.gov This is changing buying behavior inside the Cybersecurity For Retail and E-commerce Market, because merchants increasingly want tools that connect identity, fraud, and security telemetry instead of separate point controls. The result is a stronger demand for identity-centric platforms, managed detection, and response services that can lower both breach exposure and downstream fraud losses across digital retail operations.

AI-Assisted Fraud and Bot Operations

Generative AI has reduced the time, skill, and cost needed to launch large automated attacks against merchants and online marketplaces. HUMAN Security found that AI-driven traffic on retail and e-commerce platforms grew 187% from January to December 2025, while agentic browser traffic surged 7,851% year over year. The detection problem is becoming harder because only 0.5 percentage points separate the behavioral fingerprint of benign automation from malicious automation. Retail and e-commerce absorbed 54.92% of attempted account takeover attacks and 71.75% of carding attacks in 2025, which shows how central this sector has become in automated fraud campaigns.[3]HUMAN Security, “2026 State of AI Traffic and Cyberthreat Benchmark Report,” HUMAN Security, humansecurity.com Visa also reported a 25% increase in malicious bot-initiated transactions over recent months, with United States e-commerce seeing a 40% increase as agentic commerce expands. This is widening the role of cybersecurity for the retail and e-commerce market beyond standard perimeter defense and toward behavioral AI, transaction intent analysis, and agent identity control.

Expansion of Omnichannel Retail and Attack Surface Complexity

Retailers now serve customers through websites, mobile apps, social commerce, voice interfaces, loyalty systems, and marketplace integrations, and each added touchpoint creates another path for attack. Akamai documented more than 311 billion web application and API attacks globally in 2024, up 33% year over year, and commerce absorbed more than 230 billion of those attacks. Commerce represented more than 40% of all observed web attacks globally, which placed it far ahead of the next most targeted sector. API vulnerabilities have become a major weak point in this model, and Akamai estimated that API security incidents cost organizations USD 87 billion annually and are projected to exceed USD 100 billion by 2026. Many retailers have expanded omnichannel features faster than they have expanded API security, which leaves persistent gaps at third-party integration points. Japan’s launch of Ryutsu ISAC in April 2026 shows that parts of the Cybersecurity For Retail and E-commerce Market are starting to move from isolated enterprise defense to coordinated sector-level response.

Mainstreaming of Cloud-Native Retail Platforms

Cloud migration in retail has moved past a simple hosting decision and now shapes how merchants secure checkout, identity, inventory, and customer data flows. Thales reported in 2025 that 55% of organizations viewed cloud environments as more complex to secure than on-premises infrastructure, with enterprises using 2.1 public cloud providers and 85 SaaS applications on average. For retailers, this complexity is more visible because customer journeys, inventory feeds, and payment interfaces now run across hybrid and distributed environments. PCI DSS 4.0 became mandatory in March 2025, and its stronger authentication and web application control requirements fit more naturally with cloud-native security models built on encryption, identity orchestration, and continuous monitoring. This is helping cloud-native deployments hold a larger place in the Cybersecurity For Retail and E-commerce Market, while purpose-built cloud security tools keep gaining preference over retrofitted on-premises products. The demand story is no longer only about infrastructure migration, because merchants also need cloud security products that can scale with seasonal spikes and integrate directly with SaaS commerce platforms.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Security Tool Sprawl and Integration Complexity | -1.8% | Global | Medium term (2-4 years) |

| Shortage of Retail-Specific Security Talent | -1.5% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Budget Sensitivity in Mid-Market Retailers | -0.9% | North America and Europe | Short term (≤ 2 years) |

| Security Controls That add Friction to Checkout Flows | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Security Tool Sprawl and Integration Complexity

Retail security teams often manage too many overlapping tools, and that creates visibility gaps instead of stronger control. The average enterprise uses 85 SaaS applications, and 55% of security teams say cloud environments are harder to manage than on-premises environments, which adds to the integration burden. In retail, that burden is spread across point-of-sale systems, online storefronts, mobile apps, loyalty programs, and third-party APIs, all with separate vendors and different security needs. Threat signals become harder to correlate when each control works from a separate data model, and that delay can let a small incident expand into a broad breach. RH-ISAC found that 70% of retail and hospitality CISOs had AI governance added to their existing responsibilities, while team size expectations for 2026 stayed largely unchanged. This makes consolidation a clear theme across the Cybersecurity For Retail and E-commerce Market, but the shift takes time and holds back near-term deployment efficiency.

Shortage of Retail-Specific Security Talent

The talent gap in retail has a practical edge because merchants need people who understand fraud, checkout flow, customer experience, and security architecture at the same time. General cybersecurity skills are not enough in many cases, because retail teams also need to balance conversion, abuse prevention, payment trust, and identity verification inside live commerce systems. RH-ISAC reported that competing IT priorities and budget constraints were the top barriers to executing security initiatives, even as security spending rose from 0.57% to 0.75% of revenue in 2025. This pressure is sharper for mid-sized merchants that face the same threat patterns as large retailers but lack the scale to recruit or retain specialist talent. As a result, more organizations are turning to managed services, external consulting support for AI governance, and cloud-delivered security operations instead of building everything in-house. The labor gap does not stop spending in the Cybersecurity For Retail and E-commerce Market, but it does shift more demand toward service-led and automation-heavy offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Anchor Spending as Services Accelerate

Solutions held 63.51% of the Cybersecurity For Retail and E-commerce Market in 2025, which shows that retailers still place most spending behind software and platform deployments. That lead reflects enterprise demand for integrated architectures that combine identity management, bot mitigation, application security, fraud prevention, and detection workflows inside one operating model. Large merchants with bigger IT teams continue to favor these integrated solution stacks because they need broad control across physical and digital channels. The solutions side also benefits from platform consolidation, since retailers increasingly want fewer vendors and a cleaner data model across customer-facing and internal systems. That keeps the core of the Cybersecurity For Retail and E-commerce Market tied to product-led spending, even as the operating environment grows more complex.

Services are projected to grow at a 15.97% CAGR from 2026 to 2031, which makes this the stronger expansion story within the component split. Retail CISOs most often outsource penetration testing and security operations center functions, indicating that staffing pressure is directly driving service demand. The need for outside help is rising further because AI governance has been added to existing leadership workloads, while team sizes are not expanding at the same pace. Mid-market merchants are a major part of this trend because many do not have a dedicated in-house security team and need managed detection and response support. Over time, that pattern should narrow the solutions-to-services gap across the Cybersecurity For Retail and E-commerce Market without displacing the central role of software platforms.

By Security Type: Application and Cloud Security Define the Frontlines

Application security held 26.73% of the Cybersecurity For Retail and E-commerce Market share in 2025, making it the largest security type because the retail attack surface starts at the application layer. Akamai’s 2025 report showed that commerce drew more than 230 billion web application and API attacks in 2024, which kept web, API, and checkout protection at the center of merchant spending. That position also reflects the simple fact that customer logins, shopping carts, loyalty portals, and payment pages remain the most exposed parts of modern commerce systems.[4]Akamai Technologies, “State of Apps and API Security 2025, Web Application Attacks and API Attacks Report,” Akamai Technologies, akamai.com Endpoint and network security still matter, but they now serve more as foundational layers than as the main line of retail defense. Bot management, identity and access management, data security, and SIEM are all benefiting from the same shift toward user-facing, transaction-linked risk control.

Cloud security is forecast to grow at a 17.61% CAGR from 2026 to 2031, making it the fastest-growing security type in this market. This pace reflects the migration of retail workloads to hyperscaler and SaaS environments, where older tools do not fit well with elastic and API-driven operations. Retailers need cloud controls that can protect real-time inventory APIs, customer identity stores, and checkout systems without adding too much latency. PCI DSS 4.0 is also reinforcing this move, because stronger authentication and application protection rules are easier to maintain in cloud-native environments with built-in automation. As the cybersecurity market for retail and e-commerce expands, cloud security should continue to gain share from slower, retrofitted models built for earlier infrastructure patterns.

By Deployment Mode: Cloud Leads on Both Share and Growth

Cloud accounted for 67.49% of the cybersecurity market share for retail and e-commerce in 2025, confirming that it has become the default deployment model for new retail security rollouts. Retailers value cloud delivery because it can scale during peak shopping periods, absorb continuous threat intelligence updates, and connect quickly with modern commerce stacks. This model also matches the faster release cycles now used across digital storefronts, payment systems, and loyalty features. Thales found that 52% of AI security spending was already displacing traditional tools in 2025, and that cloud was the primary surface on which these newer controls were being deployed. The scale advantage keeps cloud at the center of cybersecurity for the retail and e-commerce market, serving both large chains and expanding digital merchants.

Cloud is also projected to expand at a 16.63% CAGR from 2026 to 2031, which means it leads on both current share and future momentum. Hyperscaler investment in retail-specific services and prebuilt marketplace integrations is making cloud security easier to adopt across different merchant sizes. On-premises deployments still remain relevant for retailers with data sovereignty needs or latency-sensitive payment systems. Hybrid deployment reflects the transition stage of large retailers that are moving legacy store and back-office systems to the cloud in phases. Even with those legacy anchors, the Cybersecurity For Retail and E-commerce Market is clearly moving toward cloud as the long-term operating baseline.

By Organization Size: Large Enterprises Set Scale While SMEs Drive Expansion

Large enterprises held 67.17% of market value in 2025, which shows how much spending still comes from retailers with bigger footprints, higher transaction volumes, and more layered technology estates. These organizations often operate across several countries and channels, so they need broader security architectures that can manage identity, cloud exposure, payment risk, and incident response together. Executive commitment also remains strong in this group, with 54% of retail and hospitality CISOs expecting budget increases in 2026 and close to 90% expecting higher AI security spending. Large retailers, therefore, continue to shape demand for consolidated platforms, broader telemetry, and integrated security operations. Their scale keeps them central to the Cybersecurity For Retail and E-commerce Market, even as faster growth shifts elsewhere.

SMEs are projected to grow at a 16.27% CAGR from 2026 to 2031, and that pace makes them the main acceleration segment by organization size. Smaller merchants face the same threats as enterprise retailers, including credential stuffing, scraping, account takeover, and API abuse, but usually operate with far fewer security resources. SaaS pricing, managed services, and plug-in integrations are lowering the access barrier for these merchants and are bringing stronger protection to smaller storefronts. The growth of SME-focused offerings from fraud vendors such as Riskified and Signifyd shows how suppliers are adapting products and commercial models for this customer base. That shift should widen the demand base of cybersecurity for the retail and e-commerce market without changing the fact that large enterprises still account for most current spending.

By Application: Payment Security Holds Scale While Bot Mitigation Surges

Payment security accounted for a 24.96% share of the Cybersecurity For Retail and E-commerce Market size in 2025, which kept it as the largest application area. Its leadership reflects the direct link between payment protection, fraud loss, authorization rates, and checkout trust in online retail. Visa’s July 2026 tokenization enforcement for card-on-file transactions has made this segment more strategic because compliant merchants can see a clearer connection between security readiness and payment performance.[5]Visa, “Visa Announces New AI, Stablecoin and Token Innovations to Power Intelligent, Programmable Commerce at Visa Payments Forum,” Visa, visa.com Fraud detection and prevention, account takeover prevention, and API security remain tightly connected to this spending because payment abuse rarely happens in isolation. As a result, the cybersecurity for the retail and e-commerce market continues to treat payment security as both a revenue protection layer and a core trust control.

Bot mitigation is projected to expand at an 18.43% CAGR from 2026 to 2031, making it the fastest-growing application area. HUMAN Security documented more than 150 billion scraping attack attempts against retail and e-commerce businesses in 2025, and heavily targeted businesses saw scraping rates above 57% of all product-page traffic. Radware also reported that bad bots made up 43% of all traffic on retail platforms during the 2025 peak shopping season, which shows how close malicious automation is to human traffic volumes. This scale explains why bot mitigation has moved from an optional add-on to an operational requirement for merchants trying to protect product pages, promotions, logins, and payment flows. The growth of this segment should remain one of the clearest demand engines within the Cybersecurity For Retail and E-commerce Market through the forecast period.

Geography Analysis

North America held 38.19% of the Cybersecurity For Retail and E-commerce Market share in 2025, which kept it as the largest regional market. The region benefits from a dense base of enterprise retailers, a mature vendor ecosystem, and a high burden of digital fraud. Visa reported a 40% increase in malicious bot-initiated e-commerce transactions in the United States over recent months, which shows how active the threat environment remains. LexisNexis found that card transactions accounted for 31% of fraud costs for United States e-commerce merchants, while Canada’s fraud cost multiplier reached USD 5.23 for every USD 1 of direct loss. Board-level oversight is also supporting demand, with the 2026 Director’s Handbook on Cyber-Risk Oversight reinforcing governance expectations around cyber resilience and risk visibility.

Europe shows a split demand pattern that is being shaped by regulation, supply chain obligations, and heavy API exposure in commerce systems. Germany’s revised BSI Act extended NIS2 obligations from December 6, 2025, and expanded the affected entity base from 4,500 to 29,500 enterprises, which materially widened the compliance market. Akamai reported that EMEA recorded 116 billion web attacks across 2023 and 2024, with commerce accounting for 54 billion and 63% of attacks against EMEA commerce targeting APIs. Germany, the United Kingdom, and France, therefore, remain the core European demand centers for application security, managed detection, and compliance-linked retail security services.

Asia-Pacific is projected to grow at a 17.64% CAGR from 2026 to 2031, which makes it the fastest-growing regional segment in the Cybersecurity For Retail and E-commerce Market. LexisNexis reported that the region’s fraud attack rate rose 12% year over year in 2025 to 1.7%, which was above the global average. Super-app ecosystems in China, India, and Southeast Asia combine payments, social interaction, and commerce in one environment, which raises the value of each compromised account. China’s PIPL and India’s Digital Personal Data Protection Act are also shaping how retailers design data security and customer identity architecture. Japan’s Ryutsu ISAC launch in April 2026 shows a regional move toward coordinated retail cyber defense, while South Korea and Australia remain strong adopters of cloud-native controls.

Competitive Landscape

Cybersecurity in the retail and e-commerce market is moderately consolidated at the enterprise platform tier and fragmented across specialist applications and the mid-market. Fortinet, Palo Alto Networks, CrowdStrike, Cisco Systems, and Microsoft compete for large retail accounts by offering broader architectures that can reduce tool sprawl and unify detection across channels. Specialist vendors such as Riskified, Signifyd, Forter, HUMAN Security, and DataDome continue to matter because retail fraud patterns often require narrower domain expertise and commerce-specific training data. Microsoft keeps an important reach advantage through its link across Microsoft 365 Defender, Azure, and broader enterprise workflows, which makes it harder for pure-play vendors to match platform breadth alone. The market therefore rewards both scale and specialization, depending on retailer size, integration needs, and the share of fraud risk tied to customer-facing transactions.

Strategic moves in 2026 show that vendors are increasingly building around AI-native threats and machine-speed identity control. CrowdStrike introduced Continuous Identity for AI Agents in June 2026 and later expanded its platform capabilities with Falcon Data Security and the Charlotte AI AgentWorks Ecosystem, which strengthened its position around non-human identity and data theft protection. Palo Alto Networks launched Prisma AIRS 3.0 in March 2026 to secure the full agentic AI lifecycle through a unified control plane, which reflected the same industry direction. Fortinet launched FortiOS 8.0 and previewed FortiSOC in 2026, which showed a parallel focus on AI-driven security and unified operations for distributed environments. IBM joined the OpenAI Daybreak Cyber Partner Program in June 2026, giving its security stack access to frontier AI models for faster vulnerability identification and validation.

Another major competitive shift is the growing overlap between cybersecurity and payment authentication. Cloudflare’s work with Visa, Mastercard, and other payment companies on the Web Bot Authentication protocol created a new layer where payment trust, bot verification, and merchant security spending now intersect. HUMAN Security and Riskified also partnered in August 2025 to build a unified framework for trusted AI shopping agent commerce, which shows how fraud vendors are moving deeper into agentic transaction control. White space remains strongest in AI-native compliance automation for mid-market retailers, supply chain security for omnichannel APIs, and return-fraud detection, because vendor coverage is still uneven across those needs.

Cybersecurity For Retail and E-commerce Industry Leaders

Fortinet, Inc.

Palo Alto Networks, Inc.

Check Point Software Technologies Ltd.

Cisco Systems, Inc.

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: IBM joined the OpenAI Daybreak Cyber Partner Program, launching a new application security service using OpenAI's frontier AI models to help enterprises identify and validate software vulnerabilities with greater speed and precision. The collaboration brings machine-speed threat detection capabilities to IBM's security operations stack, directly addressing the agentic fraud exposure retail enterprises face.

- June 2026: CrowdStrike unveiled Continuous Identity for AI Agents, a Falcon Next-Gen Identity Security capability that grants, denies, and revokes access based on real-time risk for human, non-human, and AI agent identities. Built on technology from CrowdStrike's acquisition of SGNL, the capability directly addresses the identity governance gap created by autonomous agents operating at machine speed in retail and e-commerce environments.

- May 2026: Proofpoint integrated its platform with the Claude Compliance API, extending its data security, DLP, insider risk, and AI runtime security controls directly into Claude enterprise deployments. The integration enables retailers and commerce organizations to apply consistent governance policies across employee activity, e-mail, cloud, and AI-assisted workflows on a single platform.

- March 2026: CrowdStrike introduced Falcon Data Security at RSA Conference 2026, a new data protection solution powered by adversary intelligence and unified Falcon platform context to discover, classify, and stop data theft in real time. The solution targets the data exfiltration risk profile that retail organizations face from insiders, AI agents with valid credentials, and external adversaries operating with compromised access.

- March 2026: Fortinet launched FortiOS 8.0, the latest release of its Security Fabric operating system, delivering AI-driven security, next-generation SASE, and quantum-safe capabilities for organizations managing complex distributed retail architectures. The release was accompanied by the preview of FortiSOC, a cloud-delivered SaaS platform unifying FortiAnalyzer, FortiSIEM, FortiSOAR, and FortiTIP under a single integrated service.

Global Cybersecurity For Retail and E-commerce Market Report Scope

The Cybersecurity For Retail and E-commerce Market comprises technologies, solutions, and services that help online and physical retail businesses protect their digital assets, payment systems, customer data, and transaction environments from cyber threats. The market covers payment security, customer data protection, fraud prevention, secure transaction processing, and protection against cyberattacks such as phishing, ransomware, and bot-driven fraud. In the retail and e-commerce industry, cybersecurity enables secure shopping experiences, supports regulatory compliance, and strengthens customer trust by safeguarding sensitive information, including credit card details, personal data, and loyalty program accounts, across digital platforms and omnichannel environments.

The Cybersecurity For Retail and E-commerce Market Report is Segmented by Component (Solutions, and Services), Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Identity and Access Management, Data Security and Encryption, Bot Management and Fraud Prevention, and Security Information and Event Management), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Payment Security, Account Takeover Prevention, Fraud Detection and Prevention, Bot Mitigation, Data Protection and Privacy, API Security, Compliance Management, and Brand Protection and Anti-Phishing), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Network Security |

| Endpoint Security |

| Application Security |

| Cloud Security |

| Identity and Access Management (IAM) |

| Data Security and Encryption |

| Bot Management |

| Security Information and Event Management (SIEM) |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Payment Security |

| Fraud Detection and Prevention |

| Account Takeover Prevention |

| Bot Mitigation |

| API Security |

| Data Protection and Privacy |

| Compliance Management |

| Brand Protection and Anti-Phishing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Security Type | Network Security | ||

| Endpoint Security | |||

| Application Security | |||

| Cloud Security | |||

| Identity and Access Management (IAM) | |||

| Data Security and Encryption | |||

| Bot Management | |||

| Security Information and Event Management (SIEM) | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application | Payment Security | ||

| Fraud Detection and Prevention | |||

| Account Takeover Prevention | |||

| Bot Mitigation | |||

| API Security | |||

| Data Protection and Privacy | |||

| Compliance Management | |||

| Brand Protection and Anti-Phishing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the cybersecurity for retail and e-commerce space?

The Cybersecurity For Retail and E-commerce Market stands at USD 36.57 billion in 2025, and USD 40.49 billion in 2026 and is projected to reach USD 67.34 billion by 2031 at a CAGR of 10.71%.

Which region leads spending on cybersecurity for retail and e-commerce?

North America led with 38.19% share in 2025, supported by a dense enterprise retail base, high fraud exposure, and a mature vendor ecosystem.

Which regional market is growing the fastest through 2031?

Asia-Pacific is projected to expand at a 17.64% CAGR through 2031 as e-commerce volumes rise and fraud attack rates remain above the global average.

Why is cloud security growing faster than other security types in retail?

Cloud security is forecast to grow at 17.61% CAGR because retailers are shifting workloads to cloud-native and SaaS environments that require purpose-built controls instead of retrofitted legacy tools.

Which application area is seeing the fastest growth?

Bot mitigation is projected to grow at 18.43% CAGR through 2031 as scraping, account takeover, and agentic automation place sustained pressure on digital storefronts.

Why are SMEs becoming more important buyers of cybersecurity tools?

SMEs are expected to grow at a 16.27% CAGR because SaaS delivery, managed services, and easier platform integrations are making stronger protection more accessible to smaller merchants.

Page last updated on: