Cuffless Blood Pressure Monitor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

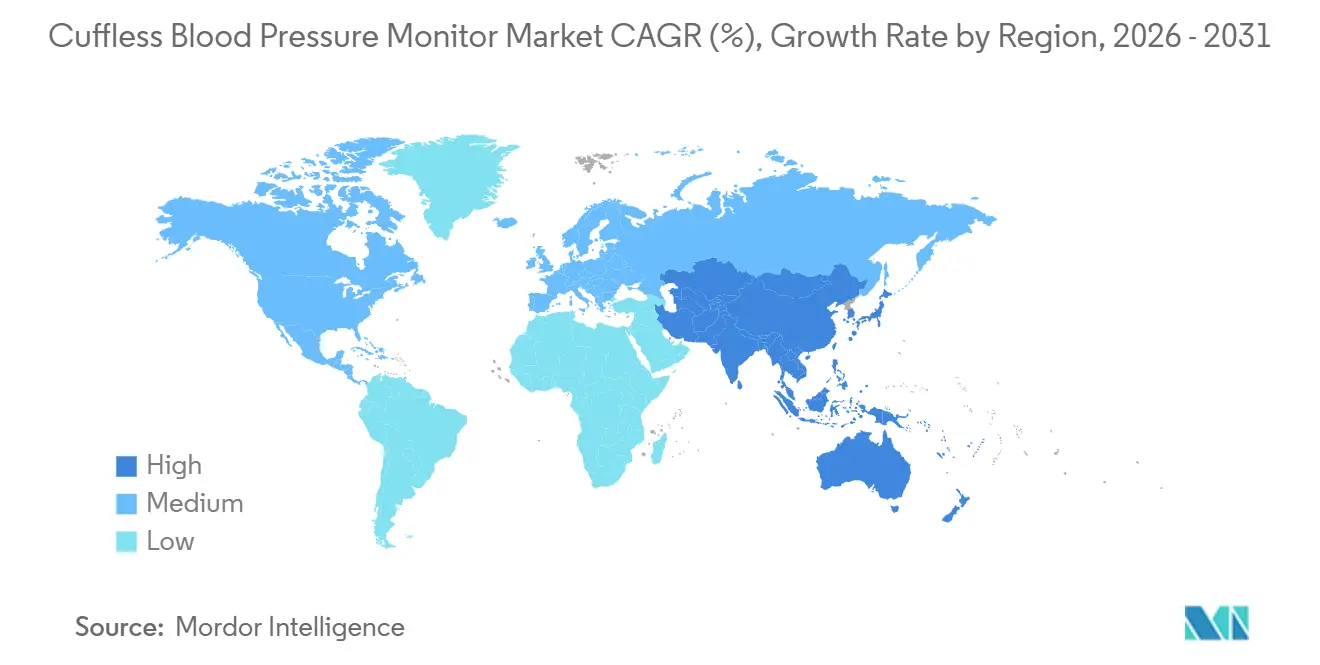

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cuffless Blood Pressure Monitor Market Analysis by Mordor Intelligence

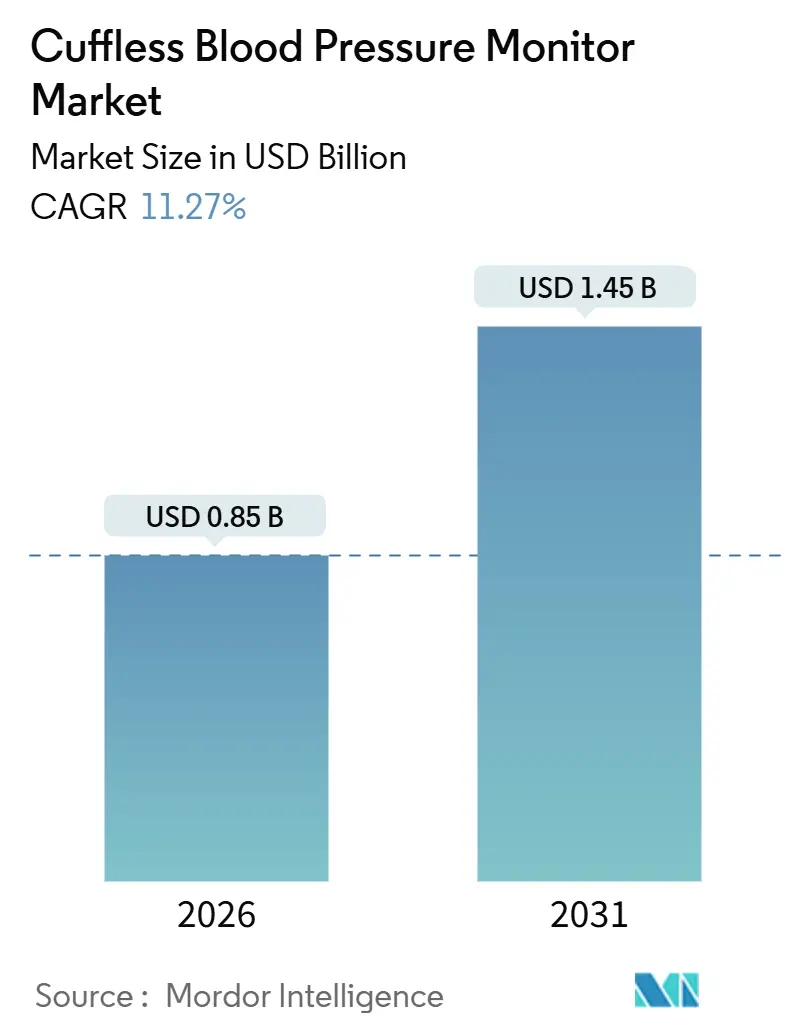

The Cuffless Blood Pressure Monitor Market size is estimated at USD 0.85 billion in 2026, and is expected to reach USD 1.45 billion by 2031, at a CAGR of 11.27% during the forecast period (2026-2031).

Continuous ambulatory surveillance is replacing episodic clinic checks as photonic sensor miniaturization, machine learning calibration, and supportive regulatory pathways converge. Wrist-, patch-, and ring-based devices now blend into daily routines, enabling large data sets that feed tele-health dashboards and clinical decision support tools. Consumer-electronics majors are scaling supply chains while clinical specialists race to validate accuracy, creating overlapping yet distinct competitive tracks. Hospital procurement teams and corporate wellness managers are shifting to subscription models that bundle hardware, analytics, and service, unlocking new recurring revenue streams for suppliers.

Key Report Takeaways

- By product type, wrist wear led with 60.23% revenue share in 2025, while patch-based sensors are expected to advance at an 18.25% CAGR through 2031.

- By technology, photoplethysmography captured 54.53% of 2025 revenue, while bio-impedance is forecast to accelerate at a 15.85% CAGR to 2031.

- By form factor, wrist wear commanded 60.23% share in 2025, while ring devices are projected to expand at an 18.55% CAGR over the same period.

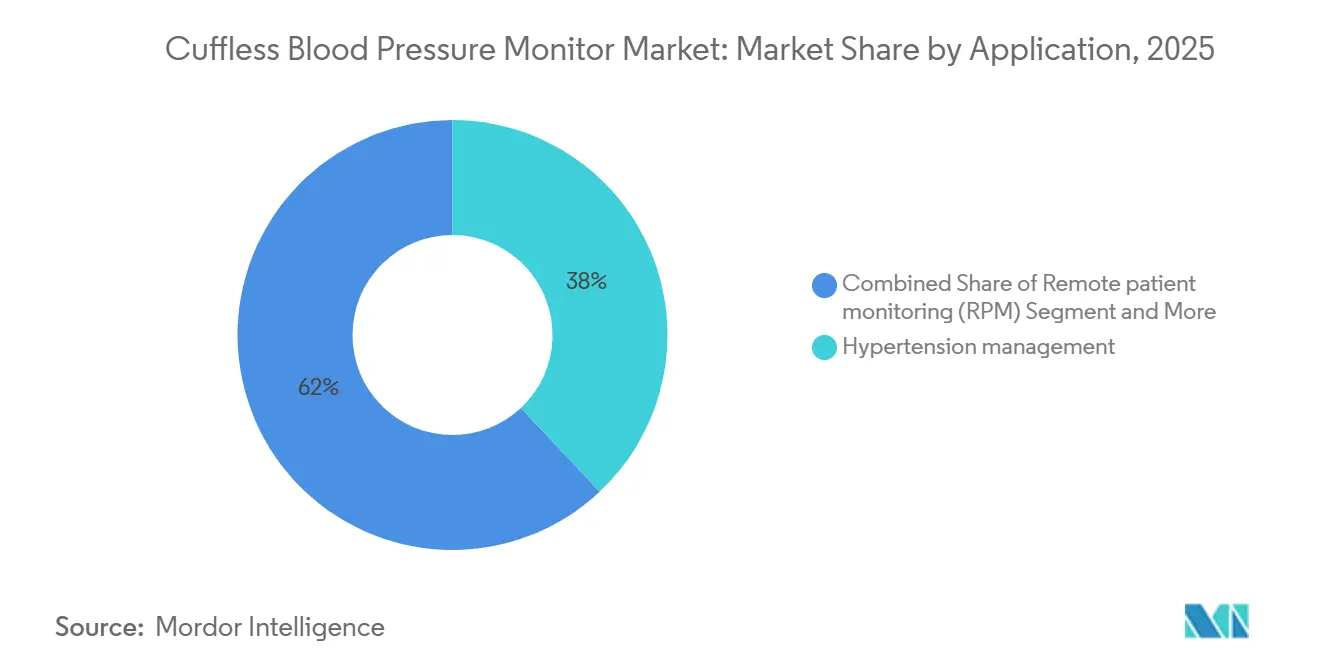

- By application, hypertension management held 38.03% of 2025 revenue, while remote patient monitoring is advancing at a 15.11% CAGR to 2031.

- By end user, home-care patients delivered 45.32% of 2025 revenue, while research institutes are rising at a 14.81% CAGR through 2031.

- By distribution channel, online retail controlled 58.53% of 2025 revenue, while direct B2B sales are projected to grow at a 12.61% CAGR by 2031.

- By geography, North America accounted for 41.25% revenue share in 2025, while Asia-Pacific is poised to climb at a 16.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cuffless Blood Pressure Monitor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hypertension & cardiovascular risk | +2.8% | Global, with acute burden in Asia-Pacific | Long term (≥ 4 years) |

| Rapid adoption of consumer wearables for preventive healthcare | +2.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Regulatory clearances for cuff-free devices | +1.9% | North America, Europe, selective APAC markets | Short term (≤ 2 years) |

| Integration with tele-health & remote patient monitoring platforms | +1.7% | North America, spill-over to EU and urban APAC | Medium term (2-4 years) |

| AI-driven calibration-free algorithms lowering usage friction | +1.4% | Global, led by North America and China | Long term (≥ 4 years) |

| Photonic chip cost reductions enabling lower price points | +1.0% | Global, accelerating in APAC manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hypertension And Cardiovascular Risk

The World Health Organization reported that 1.4 billion adults lived with hypertension in 2024, with only 320 million under control, underscoring a vast management gap. Urbanization and dietary changes in Asia-Pacific increase cardiovascular risk among younger cohorts who often skip clinic visits. Continuous wearable measurement embeds blood-pressure checks into daily life, turning passive patients into data contributors. ISO 81060-3 and IEEE 1708a are now acknowledging pulse-transit-time and optical methods as legitimate, further lifting adoption barriers[1]International Organization for Standardization, “ISO 81060-3,” iso.org. These factors collectively add 2.8% to the forecast CAGR as clinical protocols adapt to continuous data streams.

Rapid Adoption of Consumer Wearables for Preventive Healthcare

Global shipments of smartwatches and fitness bands passed 500 million units in 2024. Once wearables reach mass pockets, firmware updates or low-cost modules can activate blood-pressure features without new hardware purchases. Huawei’s Watch D2 launched in 2024 at EUR 399 (USD 444) with 24-hour ambulatory monitoring, proving premium devices can absorb extra sensor costs. Xiaomi followed with the CNY 1,899 Watch H1 E, gaining Beijing medical certification and signaling an aggressive domestic strategy. The category’s mainstream appeal delivers a 2.5% lift to the cuffless blood pressure monitor market CAGR.

Regulatory Clearances For Cuff-Free Devices

Aktiia’s Hilo Band obtained FDA 510(k) clearance in July 2025, becoming the first over-the-counter cuffless device approved in the United States. Nanowear’s textile SimpleSense-BP won clearance in January 2024, showing new form factors can satisfy accuracy rules. Omron earned De Novo status for IntelliSense AFib detection in October 2024, proving hybrid cuff-plus-optical approaches can speed approvals. Each clearance lowers perceived risk for the next applicant and prompts investors to back new contenders. The immediate effect raises CAGR by 1.9% in the short term.

Integration with Tele-Health & Remote Patient Monitoring Platforms

CMS remote physiologic monitoring codes require at least 16 transmitted readings each month, turning automated data flow into a reimbursement prerequisite[2]Centers for Medicare & Medicaid Services, “Remote Physiologic Monitoring Codes,” cms.gov. MedM’s software kit now hosts more than 900 device types, easing hospital IT burdens when adding cuffless monitors. A Nature Biomedical Engineering study from November 2024 verified an ultrasound patch that matched arterial-line readings in post-surgery patients, demonstrating hospital-grade fidelity. These shifts enlarge demand, adding 1.7% to CAGR over a medium timeframe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy & validation standard gaps vs. cuffed methods | -1.8% | Global, most acute in North America & EU | Medium term (2-4 years) |

| Uncertain reimbursement for non-invasive BP measurements | -1.2% | North America, selective EU markets | Short term (≤ 2 years) |

| Data-privacy / cybersecurity concerns in cloud-linked devices | -0.9% | EU (GDPR), North America (HIPAA), expanding APAC | Medium term (2-4 years) |

| Skin-tone & perfusion variability impacting PPG accuracy | -0.7% | Global, critical for diverse populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accuracy And Validation Standard Gaps Vs Cuffed Methods

The STRIDE-BP trial covering 500 patients found mean errors ranging from 4.2 mmHg to 8.7 mmHg compared with reference cuffs, especially in arrhythmia subgroups. FDA only partially recognizes IEEE 1708a, asking for further clinical data to match AAMI and ISO standards. The ARTERY Society recommends publishing uncertainty intervals, yet few consumer devices comply. These gaps slow physician adoption and trim CAGR by 1.8% in the medium term.

Uncertain Reimbursement For Non-Invasive BP Measurements

CMS billing codes do not distinguish between cuffed and cuffless devices, prompting some payers to deny claims for newer products. Private insurers cover cuffless tools only when patients cannot tolerate cuffs, limiting early volumes. Hospitals hesitate to approve capital outlays without clear payback schedules. Europe’s bundled payment systems soften the blow, yet U.S. providers feel immediate budget pressure. The result cuts 1.2% off near-term CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hospitals Embrace Patches For Continuous Data

Patch sensors generated the highest forecast momentum, expanding at an 18.25% CAGR from 2026 to 2031 as clinical buyers seek uninterrupted readings in post-surgical and step-down settings. Smartwatches and fitness bands still delivered 42.55% of 2025 revenue, leveraging their multipurpose appeal. Stand-alone devices and emerging ear or head wearables trail due to limited channels and ecosystem gaps.

The ultrasound patch validated by the University of California San Diego matched arterial lines across 117 cardiac-surgery patients, proving critical-care reliability. Textile sleeves and thoracic PPG patches add options that mitigate motion artifacts while improving comfort. This patient-centric design philosophy underpins demand and positions patches as the fastest mover within the cuffless blood pressure monitor market.

By Technology: Bio-Impedance Rises As Power Budgets Shrink

Photoplethysmography held 54.53% revenue in 2025, resting on its ubiquity in current smartwatches. Bio-impedance is forecast to climb 15.85% annually, benefiting from single-channel circuits that stretch battery life in rings and patches. Pulse-transit-time stays niche because it needs dual synchronized sensors.

Hybrid fusion models that merge PPG with impedance or ultrasound have demonstrated mean errors below 3.3 mmHg in peer-reviewed trials. Regulatory clarity for multi-sensor algorithms remains incomplete, yet the performance gains attract product teams. These advances widen the toolbox and strengthen the cuffless blood pressure monitor market foundation.

By Form Factor: Rings Gain As Discreet Wear Spurs Adoption

Wrist wear controlled 60.23% of 2025 revenue, anchored by the installed smartwatch base. Rings are expected to grow 18.55% per year through 2031 as users favor devices that charge weekly and blend with jewelry. Upper-arm options offer higher accuracy but suffer from bulky designs and higher pricing.

Patent filings from the University of Michigan and a wave of start-ups such as Aurora Motion illustrate growing R&D interest in finger-based sensing[3]University of Michigan, “Ring-Based Monitor Patent,” uspto.gov. The PMDA approval of CIRCUL RING 2 MAX in Japan signals formal recognition of the form factor. This discreet profile converts style-conscious consumers and fuels segment growth within the cuffless blood pressure monitor market.

By Application: Remote Patient Monitoring Gathers Pace

Hypertension management captured 38.03% of 2025 revenue, but remote patient monitoring is forecast to advance 15.11% annually, buoyed by CMS billing codes that reward continuous data flow. Cardiology diagnostics, sleep, and stress tracking build secondary traction as analytics identify nocturnal dipping and autonomic trends.

Clinical evidence shows automated transmissions improve medication adherence by 18% versus manual logs in home monitors, raising care quality. Hospitals deploying ultrasound or PPG patches at discharge reduce readmissions and align with value-based contracts. These outcomes reinforce the application’s high-growth path inside the cuffless blood pressure monitor market.

By End User: Academia Drives Validation Momentum

Home-care patients delivered 45.32% of 2025 revenue, yet research institutes hold the fastest outlook at 14.81% CAGR as multi-site trials seek calibration protocols for diverse skin tones. Hospitals adopt continuous monitoring in ICUs and step-down units to prevent adverse events.

Defense agencies sponsor ruggedized piezoelectric microsystems able to withstand 50 g shocks, hinting at first-responder deployment. Corporate wellness programs tie cuffless BP readings to insurance incentives, widening enterprise demand. This layered user base broadens addressable volume for the cuffless blood pressure monitor market.

By Distribution Channel: Enterprise Contracts Accelerate Volumes

Online retail held 58.53% share in 2025 due to consumer ease of comparing products on manufacturer sites. Direct B2B sales are set to climb 12.61% annually as employers and hospital chains negotiate fleet purchases bundled with software and support. Pharmacy counters remain relevant for less digitally savvy buyers, especially after FDA cleared over-the-counter sales in 2025.

Enterprise buyers favor lease models that shift spending from capital budgets to operating expenses, mirroring software as a service trends. Integration tools such as MedM’s SDK reduce onboarding effort, sustaining channel expansion. These dynamics build a robust pipeline for the cuffless blood pressure monitor market.

Geography Analysis

North America controlled 41.25% of 2025 revenue, backed by clear FDA pathways that now cover textile, optical, and hybrid devices. CMS reimbursement rules embed continuous readings into fee schedules, stimulating provider demand. A sizable installed base of 150 million smartwatches accelerates feature uptake through firmware upgrades. Canada and Mexico follow U.S. precedents yet progress more gradually due to smaller payer pools.

Asia-Pacific is forecast to rise at a 16.21% CAGR through 2031, the quickest regional climb for the cuffless blood pressure monitor market. China’s Class II device registration and India’s 2024 MedTech policy drive local manufacturing hubs that churn out lower-priced units. Japan’s PMDA approval of ring solutions and South Korea’s advanced telecom infrastructure speed remote monitoring pilots. Affordability remains challenging in parts of Southeast Asia, although urban health systems are beginning digital expansions.

Europe occupies a mid-tier position, structured by CE marking under MDR 2017/745 and stringent GDPR data-residency rules. Germany and France test reimbursement frameworks that could fund remote monitoring if cost-efficacy is proven. Middle East and Africa plus South America stay emergent, with Gulf Cooperation Council countries piloting corporate wellness integrations and Brazilian insurers trialing value-based contracts. These converging paths underline the global dispersion of the cuffless blood pressure monitor market.

Competitive Landscape

Consumer-electronics leaders—Apple, Samsung, Huawei, Xiaomi—pursue sensor fusion and ecosystem leverage to add blood-pressure functions to mass devices. Apple filed patents for liquid-filled chambers yet still limits WatchOS 26 to hypertension alerts without numeric readings, hinting at unresolved validation work. Samsung has approvals in 31 countries but not the United States, reflecting divergent regulatory hurdles.

Clinical specialists such as Omron, Masimo, and Biobeat defend hospital channels through FDA clearances and algorithm transparency. Omron’s IntelliSense AFib detection achieved 95% sensitivity and 98% specificity during cuff readings, proving a hybrid route to premium placements. Masimo’s tie-up with Qualcomm embeds signal processing into reference designs, opening white-label paths for smaller brands.

Start-ups including Aktiia, CardieX, and Sky Labs exploit niche form factors, corporate wellness deals, and academic validations. Patent landscapes around PPG processing, pulse-transit-time, and calibration diversify intellectual property barriers, potentially steering smaller entrants toward licensing. Competitive intensity sits at a moderate level as no single vendor exceeds 20% share, allowing innovation clusters to flourish inside the cuffless blood pressure monitor market.

Cuffless Blood Pressure Monitor Industry Leaders

Apple Inc.

Samsung Electronics Co. Ltd.

Huawei Technologies Co. Ltd.

Xiaomi Corp.

Omron Healthcare Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Biozen presented the Biozen BP1000 cuffless monitor at the American Heart Association Hypertension Sessions.

- July 2025: Aktiia obtained FDA 510(k) clearance for the Hilo Band, enabling U.S. over-the-counter distribution.

Global Cuffless Blood Pressure Monitor Market Report Scope

As per the scope of the report, a cuffless blood pressure monitor is a device that measures blood pressure without a traditional inflatable cuff. Instead, it uses alternative technologies such as sensors that detect physiological signals (e.g., pulse wave velocity, photoplethysmography, or electrocardiogram) to estimate blood pressure levels non-invasively and continuously.

The segmentation of the cuffless blood pressure monitor market is categorized by product type, technology, form factor, application, end-user, distribution channel, and geography. By product type, the market includes stand-alone cuffless BP monitors, smartwatches and fitness bands with BP, patch-based sensors, and other devices. By technology, it is segmented into photoplethysmography (PPG), pulse-transit-time (PTT), ultrasound/doppler, bio-impedance, and applanation tonometry algorithms. By form factor, the market is divided into wrist-wear, upper-arm wearable, ring/finger, and ear/head. By application, it covers hypertension management, cardiology diagnostics, sleep and stress monitoring, sports and fitness optimization, and remote patient monitoring (RPM). By end-user, the market includes hospitals, ambulatory surgical centers and clinics, home-care patients, corporate and fitness centers, research institutes and universities, and military and first responders. By distribution channel, it is segmented into online retail and brand web-stores, pharmacy/OTC retail, and direct B2B/enterprise sales. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Stand-alone cuffless BP monitors |

| Smartwatches & fitness bands with BP |

| Patch-based sensors |

| Other devices |

| Photoplethysmography (PPG) |

| Pulse-Transit-Time (PTT) |

| Ultrasound / Doppler |

| Bio-impedance |

| Applanation tonometry algorithms |

| Wrist-wear |

| Upper-arm wearable |

| Ring / finger |

| Ear / head |

| Hypertension management |

| Cardiology diagnostics |

| Sleep & stress monitoring |

| Sports & fitness optimisation |

| Remote patient monitoring (RPM) |

| Hospitals |

| Ambulatory surgical centres & clinics |

| Home-care patients |

| Corporate & fitness centres |

| Research institutes & universities |

| Military & first-responders |

| Online retail & brand web-stores |

| Pharmacy / OTC retail |

| Direct B2B / enterprise sales |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Stand-alone cuffless BP monitors | |

| Smartwatches & fitness bands with BP | ||

| Patch-based sensors | ||

| Other devices | ||

| By Technology | Photoplethysmography (PPG) | |

| Pulse-Transit-Time (PTT) | ||

| Ultrasound / Doppler | ||

| Bio-impedance | ||

| Applanation tonometry algorithms | ||

| By Form Factor | Wrist-wear | |

| Upper-arm wearable | ||

| Ring / finger | ||

| Ear / head | ||

| By Application | Hypertension management | |

| Cardiology diagnostics | ||

| Sleep & stress monitoring | ||

| Sports & fitness optimisation | ||

| Remote patient monitoring (RPM) | ||

| By End-user | Hospitals | |

| Ambulatory surgical centres & clinics | ||

| Home-care patients | ||

| Corporate & fitness centres | ||

| Research institutes & universities | ||

| Military & first-responders | ||

| By Distribution Channel | Online retail & brand web-stores | |

| Pharmacy / OTC retail | ||

| Direct B2B / enterprise sales | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the cuffless blood pressure monitor market in 2026?

The cuffless blood pressure monitor market size stands at USD 0.85 billion in 2026 with an expected CAGR of 11.27% to 2031.

Which product type is growing fastest?

Patch-based sensors are the fastest-growing product type, projected to rise at an 18.25% CAGR between 2026 and 2031.

Why is Asia-Pacific attractive for vendors?

Supportive regulations, lower production costs, and rising hypertension prevalence drive a 16.21% regional CAGR, the highest worldwide.

What limits adoption in hospitals today?

Validation gaps versus cuffed devices and reimbursement uncertainties are the main hurdles, particularly in North America and Europe.

Which companies hold leading positions?

Apple, Samsung, Huawei, Xiaomi, Omron, Masimo, and Biobeat currently shape the competitive field.

Page last updated on: