Creatinine Measurement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

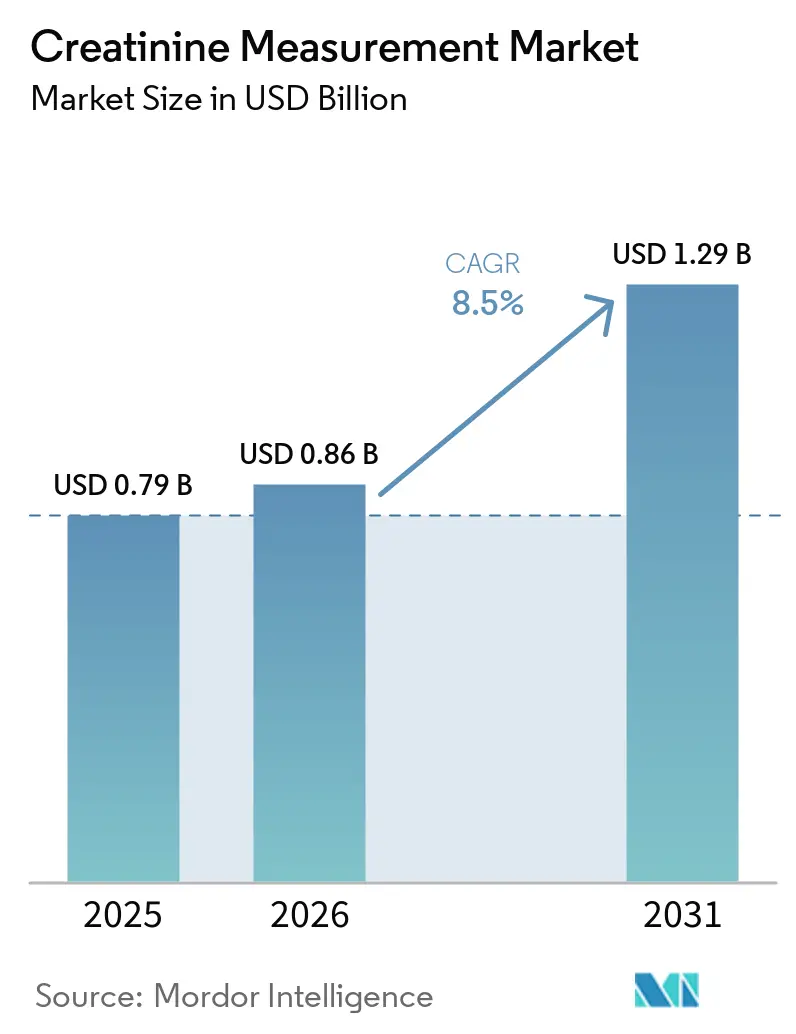

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Creatinine Measurement Market Analysis by Mordor Intelligence

The Creatinine Measurement Market size is projected to be USD 0.79 billion in 2025, USD 0.86 billion in 2026, and reach USD 1.29 billion by 2031, growing at a CAGR of 8.5% from 2026 to 2031.

This expansion is underpinned by a growing chronic kidney disease (CKD) patient pool, regulatory mandates that favor race-free eGFR reporting, and the shift of testing from core laboratories to bedside and imaging-suite point-of-care devices that deliver results in under two minutes. Hospitals are upgrading laboratory information systems to accommodate radiology units adopting pre-contrast creatinine screening protocols, and dialysis centers are embedding fingerstick meters into home hemodialysis programs. Vendors that offer isotope-dilution mass-spectrometry (IDMS), traceable enzymatic assays, along with middleware for recalculating legacy data, are positioned to capture incremental demand. Supply-chain resilience investments, such as Roche’s EUR 600 million input-materials plant slated for 2028, reinforce confidence in long-term reagent availability.

Key Report Takeaways

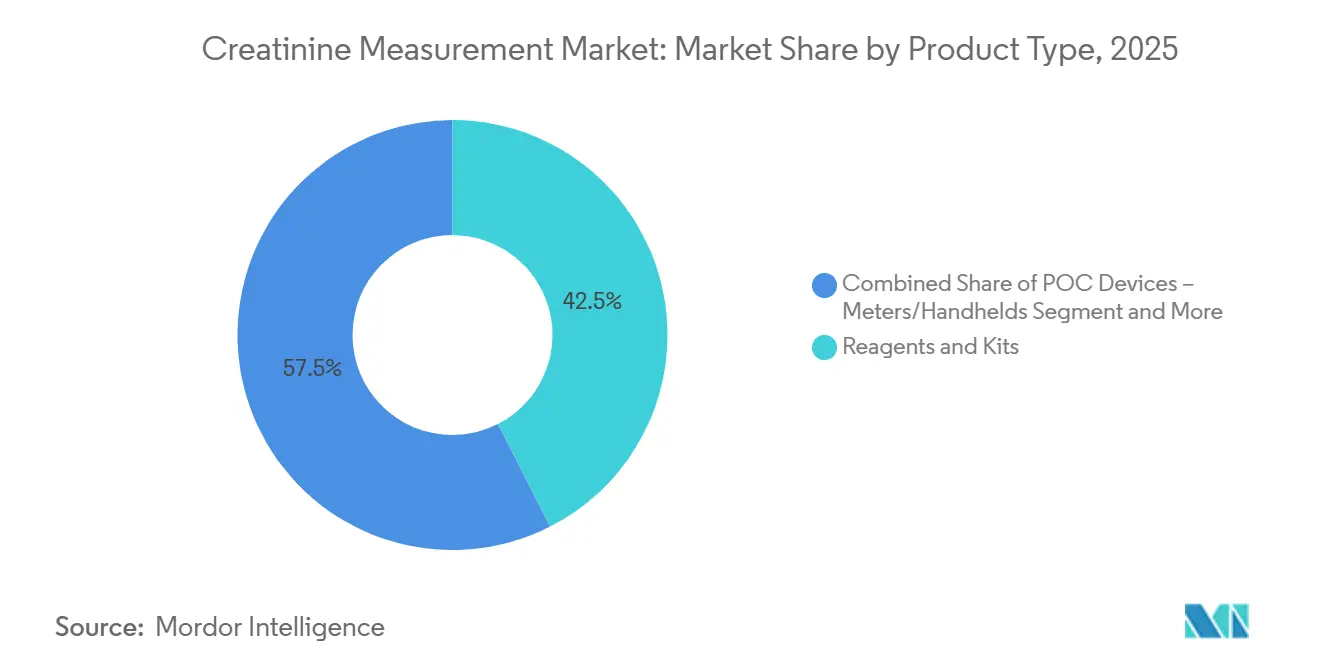

- By product type, reagents and kits led with 42.55% revenue share in 2025; point-of-care meters and handhelds are projected to expand at a 9.25% CAGR through 2031.

- By test method, Jaffe chemistry retained 54.53% of the creatinine measurement market share in 2025, while IDMS-traceable enzymatic assays are advancing at a 9.05% CAGR to 2031.

- By end user, hospitals and clinics held 45.15% of 2025 revenue; dialysis centers are forecast to grow at a 9.82% CAGR as home hemodialysis gains traction.

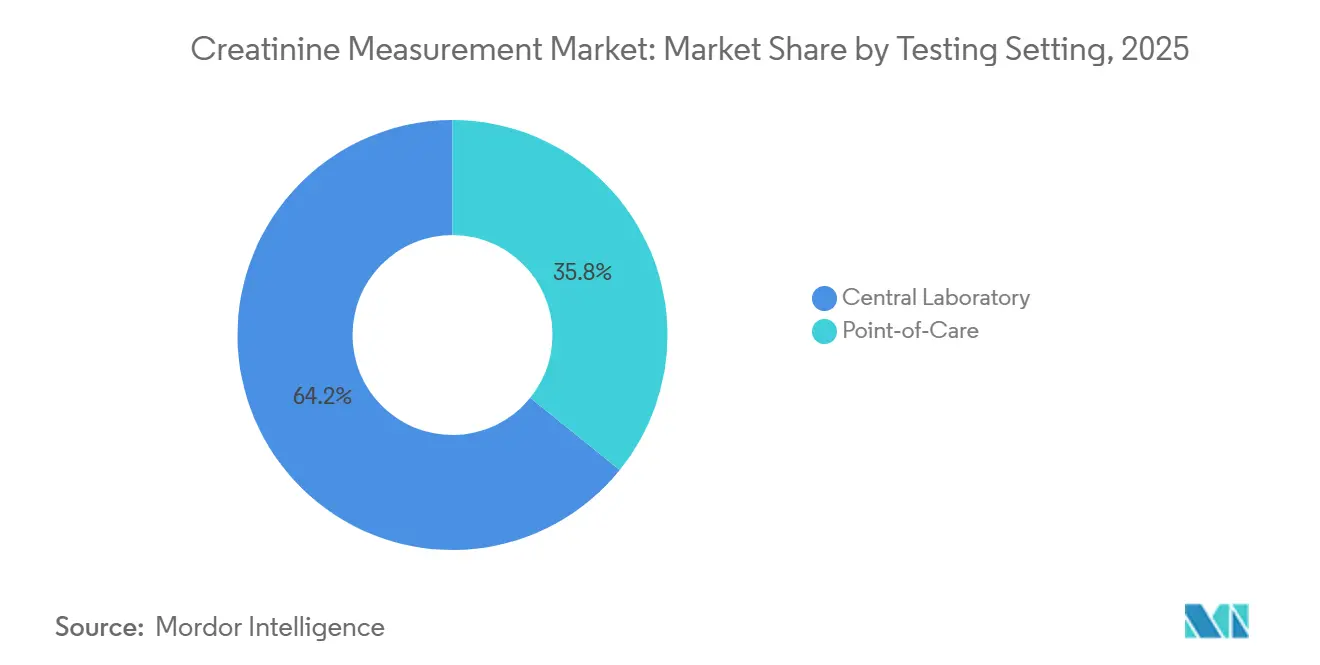

- By testing setting, central laboratories accounted for 64.25% of the creatinine measurement market size in 2025; point-of-care settings are rising at a 9.22% CAGR to 2031.

- By sample type, serum and plasma dominated with 69.23% share in 2025, whereas whole-blood point-of-care assays are expanding at a 9.33% CAGR through 2031.

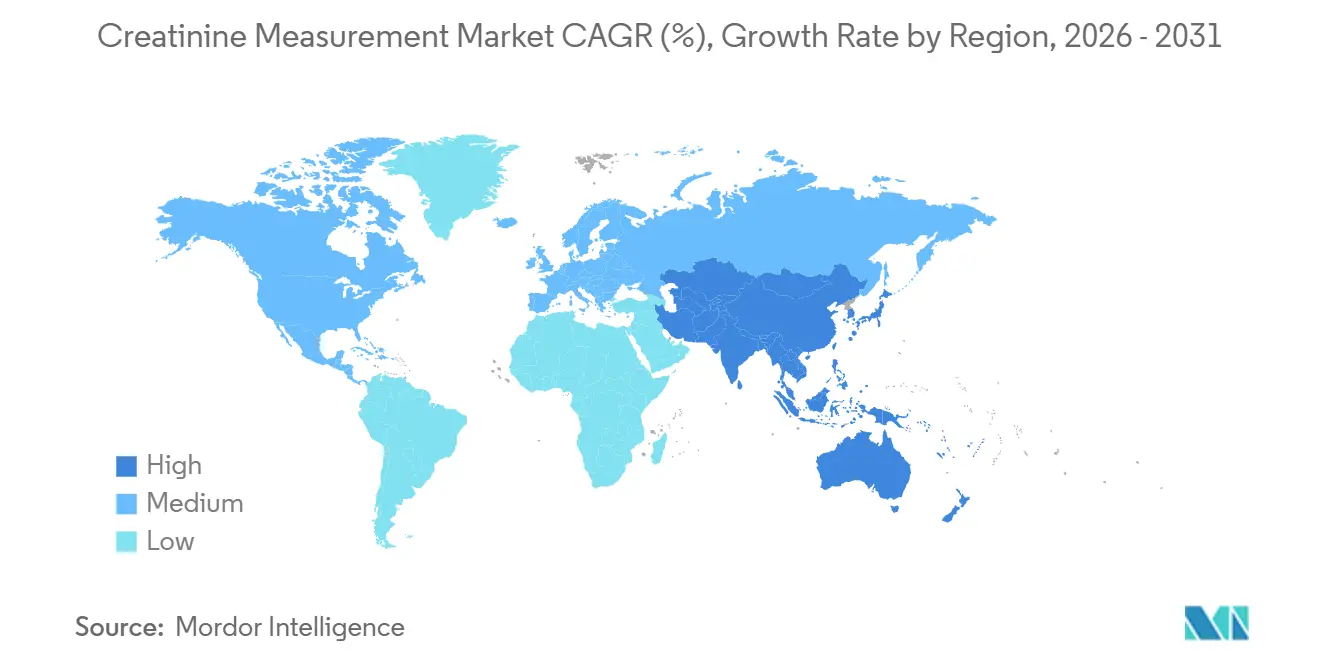

- By geography, North America generated 41.15% of 2025 value and Asia-Pacific is the fastest-growing region with a 9.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Creatinine Measurement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CKD prevalence and screening intensity | +2.0% | Global, acute needs in North America, China, India | Medium term (2–4 years) |

| Adoption of point-of-care testing in radiology and critical care | +1.5% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Shift from Jaffe to IDMS-traceable enzymatic assays | +1.2% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| Expansion of ACR screening in diabetes and hypertension programs | +1.3% | North America, Europe, spillover to APAC & Latin America | Medium term (2–4 years) |

| Implementation of race-free CKD-EPI reporting | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising CKD Prevalence And Screening Intensity

CKD affects more than 35 million adults in the United States, while China counts 132 million citizens with reduced kidney function, yet only 12.5% of Chinese patients are aware of their condition. National health agencies now embed creatinine and eGFR testing into primary-care protocols, and China’s 2024 community-health guidelines direct mass screening with portable analyzers. Japan’s dialysis registry reported 349,700 patients in 2023, each undergoing monthly creatinine checks to fine-tune treatment adequacy[1]Japanese Society for Dialysis Therapy, “2023 Annual Dialysis Data Report,” jsdt.or.jp. In the United States, Medicare’s Merit-based Incentive Payment System rewards physicians who document albumin-to-creatinine ratio results, lifting outpatient test volumes. Together, these programs funnel high-frequency samples into both laboratories and point-of-care channels, sustaining the creatinine measurement market.

Adoption Of Point-Of-Care Creatinine/eGFR Testing In Radiology And Critical Care

Radiology and intensive-care teams are relocating creatinine testing from central labs to bedside devices, shrinking turnaround from hours to minutes. Abbott’s i-STAT cartridge delivers results in two minutes from 65 µL of whole blood and demonstrated an R² = 0.99 correlation with core-lab assays in a 2024 Queensland ICU study. The U.K. National Institute for Health and Care Excellence endorses point-of-care creatinine devices for pre-contrast CT workflows, accelerating adoption in emergency imaging. Nova Biomedical’s StatSensor generates eGFR on-device in 30 seconds from a fingerstick, expanding use in community pharmacies and low-resource HIV clinics in Tanzania. These capabilities reinforce the value proposition of the creatinine measurement market where rapid decision making prevents contrast-induced nephropathy and accelerates patient throughput.

Shift From Jaffe To IDMS-Traceable Enzymatic Assays

The move toward enzymatic assays addresses the 7–9% inter-laboratory variation typical of compensated Jaffe methods. UK National External Quality Assessment Service data from 2024 show enzymatic tests meeting the KDIGO 5.6% bias goal more consistently. The FDA’s 2024 kidney-function guidance promotes eGFR derived from IDMS-aligned creatinine values, nudging laboratories toward enzymatic reagents. Vendors now support dual workflows: Roche’s CREP2 enzymatic reagent co-exists with its CREJ2 Jaffe formulation, facilitating phased upgrades. As standardization pressures mount, enzymatic assays capture rising reagent share inside the creatinine measurement market.

Expansion Of ACR Screening In Diabetes And Hypertension Programs

The American Diabetes Association, American College of Cardiology, and KDIGO mandate annual urine albumin-to-creatinine ratio testing for adults with diabetes and high-risk hypertension. Because ACR requires both urine albumin and urine creatinine readings, every additional urine sample multiplies creatinine reagent demand. The uptake of sodium-glucose co-transporter-2 inhibitors, empagliflozin posted USD 7.3 billion in 2023 sales and dapagliflozin USD 5.8 billion, has heightened the need for baseline and follow-up creatinine checks to monitor therapy safety. Payers reward timely ACR documentation, reinforcing a structural tailwind for the creatinine measurement market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Jaffe method interferences and between-method variability | −0.5% | Global, especially labs with legacy Jaffe platforms | Medium term (2–4 years) |

| Reagent price pressure and commoditization in clinical chemistry | −0.6% | Global, acute in North America & Europe; intensifying in APAC | Long term (≥ 4 years) |

| Substitution risk from renal biomarkers such as cystatin C or NGAL | −0.3% | North America, Europe, affluent APAC markets | Long term (≥ 4 years) |

| Guideline shifts reducing routine pre-contrast testing in low-risk cases | −0.4% | Europe (ESUR), possible spillover to North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Jaffe Method Interferences And Between-Method Variability

Positive interference from bilirubin and hemoglobin can inflate Jaffe results by up to 20%, while antibiotics may suppress readings, risking medication errors[2]UK National External Quality Assessment Service, “Creatinine Assay Performance Study 2024,” ukneqas.org.uk. A 2025 Annals of Laboratory Medicine review showed 4.6% LOINC mapping errors when aggregating multi-site results, underscoring how unharmonized methods can compromise longitudinal data. Siemens’ Atellica CH Creatinine 3 assay introduces rate blanking and a 0.3 mg/dL bias correction but still faces cost-driven inertia compared with enzymatic reagents. These issues temper the otherwise robust outlook for the creatinine measurement market.

Substitution Risk From Alternative Renal Biomarkers

Cystatin C delivers superior accuracy in patients with atypical muscle mass, and NGAL rises within hours of renal insult, yet their tests cost USD 20–40 against creatinine’s USD 1–3 price point. Limited standardization and reimbursement curtail widespread uptake, but specialty pathways, such as cardiac surgery and ICU bundles, could divert niche volumes. Studies integrating NGAL and cystatin C into AI-enhanced prediction models point to future multi-analyte panels rather than outright replacement, providing only a modest headwind to the creatinine measurement market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents Anchor Recurring Revenue Streams

Reagents and kits contributed 42.55% of 2025 revenue, establishing the largest slice of the creatinine measurement market size as laboratories lock into multi-year consumable contracts. Point-of-care meters and handhelds are forecast to rise 9.25% annually to 2031, propelled by imaging-suite protocols that demand under-two-minute turnaround. Clinical chemistry analyzers like Beckman Coulter’s DxC 500i run 800 tests per hour, safeguarding core-lab dominance, while Roche’s cobas c 703 doubles throughput to 2,000 tests per hour, underpinning reagent demand.

Calibrators and controls, though smaller in sales, secure assay traceability to NIST’s SRM 967b and satisfy CLIA quality mandates. Roche’s EUR 600 million facility under construction in Penzberg will automate antibody and enzyme production, reinforcing supply lines for global customers. Siemens promises 98% uptime on e-connected Atellica systems, sharpening service differentiation. In emerging economies, generic reagents from Asia introduce price pressure, yet bundled service contracts and uptime guarantees keep multinationals competitive within the creatinine measurement market.

By Test Method: Enzymatic Assays Gain Share Despite Jaffe’s Installed Base

Jaffe chemistry controlled 54.53% of the creatinine measurement market share in 2025 thanks to entrenched analyzer fleets and a 20–30% cost edge. Enzymatic assays are advancing at a 9.05% CAGR to 2031 as laboratories seek tighter alignment with IDMS standards and lower interference. The creatinine measurement industry also benefits from regulatory nudges; the FDA’s dosing guidance effectively favors enzymatic methods for drug-label compliance.

Vendors pursue a dual-track strategy. Roche and Beckman Coulter list both Jaffe and enzymatic reagents, allowing budget-constrained labs to transition gradually. Siemens’ modified Jaffe assay extends the life of legacy systems while offering rate blanking to cut bilirubin interference. As multi-center research networks demand harmonized data, enzymatic uptake will continue to erode Jaffe dominance, reinforcing momentum in the creatinine measurement market.

By Sample Type: Whole Blood POC Gains As Venipuncture Declines

Serum and plasma held 69.23% of 2025 revenue, reflecting routine venipuncture workflows on high-throughput analyzers. Whole-blood point-of-care assays, however, are growing at 9.33% CAGR on the back of devices like Abbott’s i-STAT and Nova Biomedical’s StatSensor that eliminate centrifugation and deliver real-time eGFR.

Urine testing supports albumin-to-creatinine ratio calculations that primary-care guidelines now mandate annually for millions of diabetic and hypertensive patients. FDA-cleared analyzers such as URIT’s UC-1800 integrate semi-quantitative urine creatinine into automated panels, widening cartridge pull-through. Smartphone-enabled fingerstick assays and dried-blood-spot LC–MS/MS methods, validated in 2024, hint at decentralized models that could redistribute sample volumes without shrinking the overall creatinine measurement market size.

By Testing Setting: Central Labs Retain Volume, POC Captures Urgency Premium

Central laboratories accounted for 64.25% of 2025 revenue, leveraging automation scale and broad test menus that drive reagent throughput at low unit cost. Point-of-care settings are expanding at 9.22% CAGR, capitalizing on premium pricing justified by immediate decision support in emergency imaging, dialysis, and primary care.

QuidelOrtho’s VITROS platform family can address 90% of routine laboratory needs, underscoring centralized efficiency. Yet every pre-contrast CT scan or urgent home-dialysis adjustment that bypasses the core lab sends high-margin cartridges through bedside meters. Reimbursement structures generally honor the convenience premium, although payer rules vary by state and indication. This dual-channel equilibrium sustains value creation across the creatinine measurement market.

By End User: Dialysis Centers Lead Growth As Home Hemodialysis Expands

Hospitals and clinics generated 45.15% of 2025 revenue, but dialysis centers are poised for 9.82% CAGR growth through 2031 as monthly creatinine monitoring for 571,000 U.S. dialysis patients converges with rising home hemodialysis adoption. DaVita runs 2,713 U.S. centers and Fresenius 2,236, each embedding fingerstick meters into routine care to adjust Kt/V targets.

Diagnostic laboratories remain backbone suppliers for outpatient volumes, but pharmacy-based CKD programs and HIV clinics in Tanzania illustrate how non-traditional channels are diversifying end-user demand. In this context, the creatinine measurement industry must balance high-volume lab accounts with fragmented, faster-growing niches that prize portability and integration with electronic health records.

Geography Analysis

North America held 41.15% of 2025 revenue, propelled by 571,000 dialysis patients, Medicare incentives for ACR testing, and FDA guidance that prioritizes eGFR reporting[3]United States Renal Data System, “2024 Annual Data Report,” usrds.org. Canada invests in point-of-care devices to cut emergency wait times, while Mexico’s expanding private diagnostic sector taps mid-range analyzers.

Europe’s universal health systems and IVDR regulations guide method standardization. UK NEQAS data affirm enzymatic assays meet KDIGO bias targets better than Jaffe methods, shaping National Health Service procurement. Roche’s Penzberg facility will bolster continental reagent supply chains by 2028. Yet ESUR risk-stratification protocols may temper radiology-point-of-care volumes.

Asia-Pacific is forecast to post a 9.51% CAGR, the fastest among regions. China’s 132 million-patient CKD burden, India’s expanding lab chains, and Japan’s world-leading dialysis prevalence fuel demand. Community-health screening directives and tiered care models favor portable analyzers. South Korea and Australia, though smaller, feature rapid AI adoption and regulatory clarity, fostering early uptake of IDMS-aligned assays. Middle East, Africa, and South America contribute modest volumes but adopt refurbished analyzers and lower-priced reagents, while Gulf Cooperation Council countries invest in premium hospital infrastructure.

Competitive Landscape

Five multinational firms, Roche, Siemens Healthineers, Beckman Coulter, Abbott, and Thermo Fisher Scientific, anchor the analyzer base, leveraging razor-and-blade models that bind consumable revenue to service contracts. Siemens guarantees 98% uptime for its e-connected Atellica systems, underscoring service differentiation. Roche’s EUR 600 million vertical-integration project signals commitment to safeguarding raw-material supply. Beckman Coulter’s FDA-cleared DxC 500i and Siemens’ Atellica CH Creatinine_3 refresh legacy fleets without forcing immediate method migration.

Niche players, Nova Biomedical, Randox, DiaSys, focus on handheld meters, cost-effective reagents, or specialty assays. AI-powered middleware that flags assay drift or anomalous results provides a new frontier for differentiation, especially as the EU AI Act imposes stringent post-market monitoring requirements. QuidelOrtho’s VITROS Results Management platform and remote analyzer monitoring embody value-added service trends.

Emerging innovations include smartphone-enabled fingerstick assays and dried-blood-spot LC–MS/MS workflows presented at Kidney Week 2024, pointing toward patient-initiated testing models. As decentralization accelerates, suppliers able to straddle high-volume lab contracts and fragmented point-of-care channels will shape the future trajectory of the creatinine measurement market.

Creatinine Measurement Industry Leaders

Roche Diagnostics

Siemens Healthineers

Beckman Coulter (Danaher)

Abbott

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Boehringer Ingelheim and the Detect The SOS Collective launched a campaign to elevate albumin-to-creatinine ratio screening awareness for CKD and cardiovascular risk.

- January 2026: Truvian Health secured FDA 510(k) clearances for nine analytes on TruVerus, including creatinine and eGFR, marking the first multimodal benchtop analyzer with comprehensive kidney-health coverage.

Global Creatinine Measurement Market Report Scope

As per the scope of the report, creatinine measurement is a laboratory test that quantifies the level of creatinine in the blood or urine. Creatinine is a waste product produced by muscle metabolism and is excreted by the kidneys. The test is commonly used to assess kidney function and to diagnose and monitor kidney disease.

The segmentation of the creatinine measurement market is categorized by product type, test method, sample type, testing setting, end user, and geography. By product type, the market includes reagents & kits, clinical chemistry analyzers, POC devices – meters/handhelds, POC cartridges/strips, and calibrators & controls. By test method, it is segmented into Jaffe (kinetic/compensated) and enzymatic (IDMS‑traceable). By sample type, the market is divided into blood (serum/plasma), whole blood (POC), and urine. By testing setting, it is classified into central laboratory and point‑of‑care. By end user, the market comprises hospitals & clinics, diagnostic laboratories, primary care/outpatient, and dialysis centers. By geography, the segmentation includes North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Reagents & Kits |

| Clinical Chemistry Analyzers |

| POC Devices - Meters/Handhelds |

| POC Cartridges/Strips |

| Calibrators & Controls |

| Jaffe (kinetic/compensated) |

| Enzymatic (IDMS-traceable) |

| Blood (Serum/Plasma) |

| Whole Blood (POC) |

| Urine |

| Central Laboratory |

| Point-of-Care |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Primary Care/Outpatient |

| Dialysis Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Reagents & Kits | |

| Clinical Chemistry Analyzers | ||

| POC Devices - Meters/Handhelds | ||

| POC Cartridges/Strips | ||

| Calibrators & Controls | ||

| By Test Method | Jaffe (kinetic/compensated) | |

| Enzymatic (IDMS-traceable) | ||

| By Sample Type | Blood (Serum/Plasma) | |

| Whole Blood (POC) | ||

| Urine | ||

| By Testing Setting | Central Laboratory | |

| Point-of-Care | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Primary Care/Outpatient | ||

| Dialysis Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving global demand for creatinine testing?

Rising CKD prevalence, regulatory mandates for race-free eGFR, and wider point-of-care adoption are propelling the creatinine measurement market.

How large will the creatinine measurement market be by 2031?

The creatinine measurement market size is forecast to reach USD 1.29 billion by 2031 at an 8.5% CAGR.

Why are enzymatic assays gaining share over Jaffe methods?

Laboratories seek lower interference and tighter IDMS traceability, and FDA eGFR dosing guidance indirectly favors enzymatic assays.

Which end-user segment is expanding fastest?

Dialysis centers lead growth at a 9.82% CAGR through 2031 due to monthly monitoring needs and home hemodialysis expansion.

Which region is expected to grow the quickest?

Asia-Pacific is projected to post a 9.51% CAGR through 2031, driven by China's unmet CKD burden and Indias laboratory expansion.

How does point-of-care testing impact turnaround times?

Bedside devices deliver creatinine and eGFR results in 30 seconds to two minutes, cutting hours off traditional lab workflows and improving clinical decisions.

Page last updated on: