Market Overview

| Study Period | 2021 - 2031 |

|---|---|

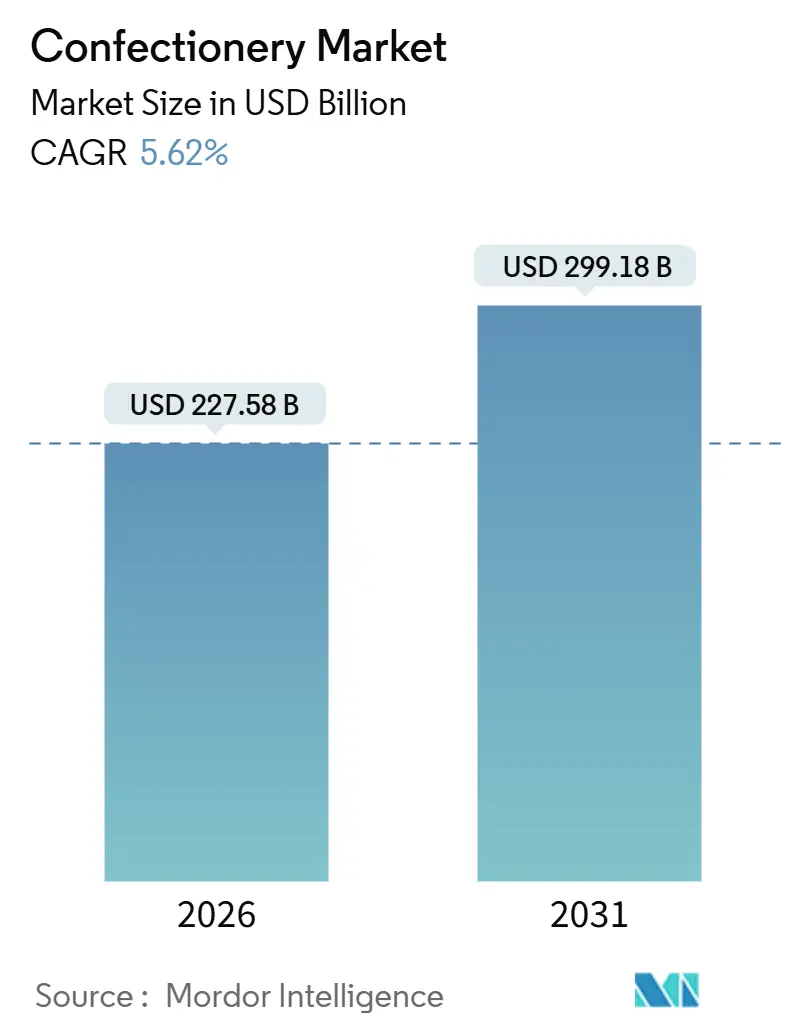

| Market Size (2026) | USD 227.58 Billion |

| Market Size (2031) | USD 299.18 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

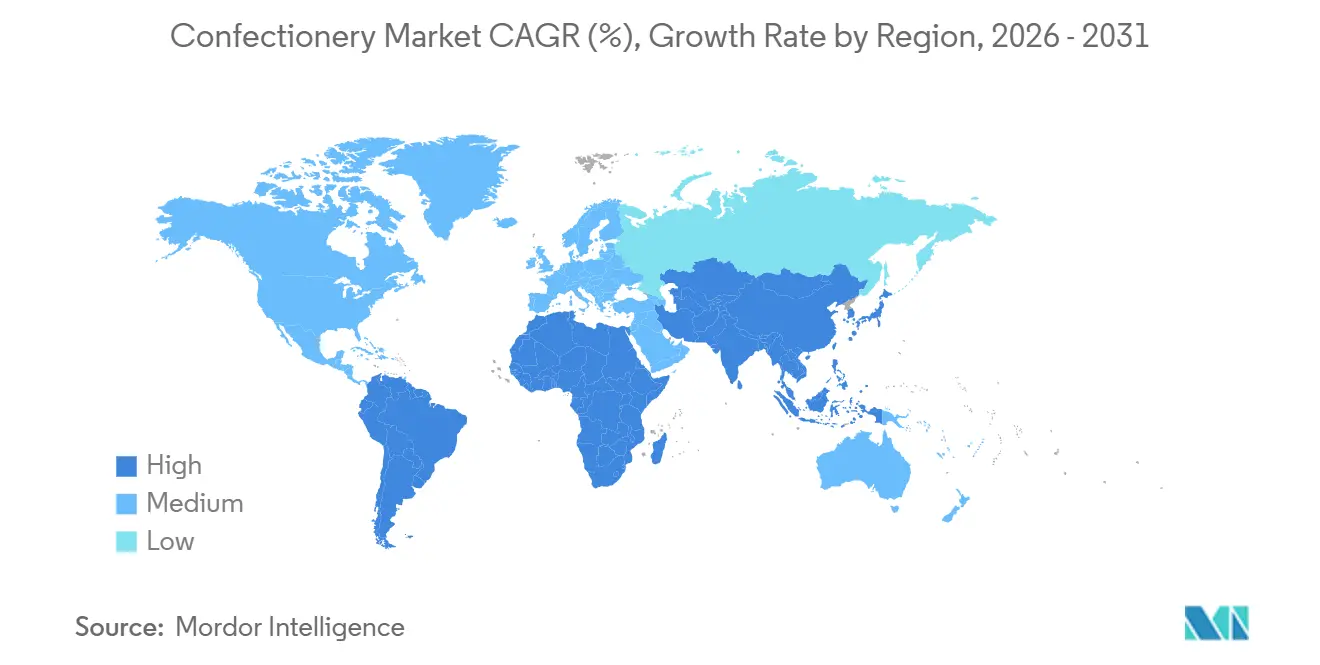

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Confectionery Market Analysis by Mordor Intelligence

The confectionery market size stood at USD 227.58 billion in 2026 and is projected to reach USD 299.18 billion by 2031, advancing at a 5.62% CAGR. Several factors are driving this growth, including fluctuations in cocoa prices, a growing focus on health-conscious product reformulations, an increasing demand for premium gifting options, and the implementation of stricter sustainability mandates. These evolving dynamics are compelling manufacturers to mitigate rising costs by introducing value-added products and adopting ethical sourcing practices. Although cocoa futures have recently eased, the long-term supply chain remains vulnerable due to the aging cocoa trees in West Africa and the persistent impact of climate variability. To address these challenges and maintain their market share, brands are innovating by incorporating plant-based dairy alternatives, adding functional ingredients, and utilizing recyclable packaging solutions. These strategies aim to strengthen their position in the highly competitive confectionery market. Additionally, leading industry players are significantly increasing their capital investments, highlighting a strategic effort to absorb raw material price shocks and sustain a robust pace of innovation.

Key Report Takeaways

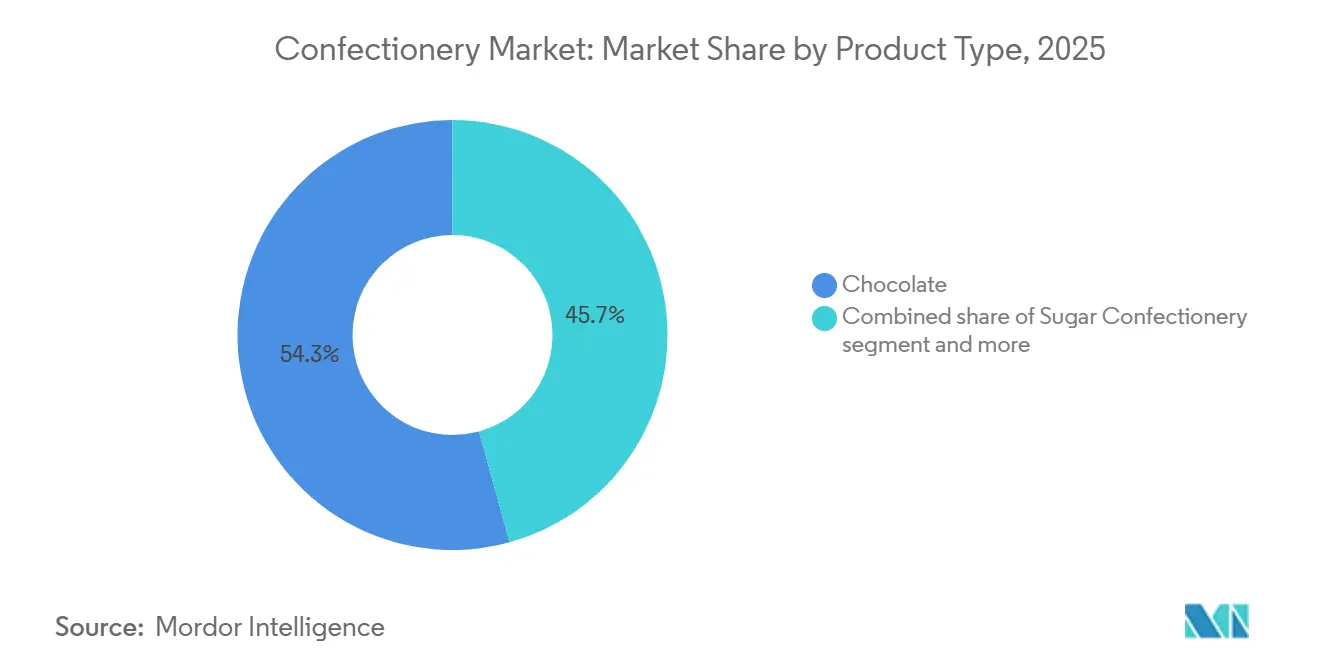

- By product type, chocolate captured 54.28% of the confectionery market share in 2025; sugar confectionery is forecast to expand at a 6.10% CAGR to 2031.

- By packaging type, single-serve formats held 58.97% of the confectionery market size in 2025, while multipacks are advancing at a 6.38% CAGR through 2031.

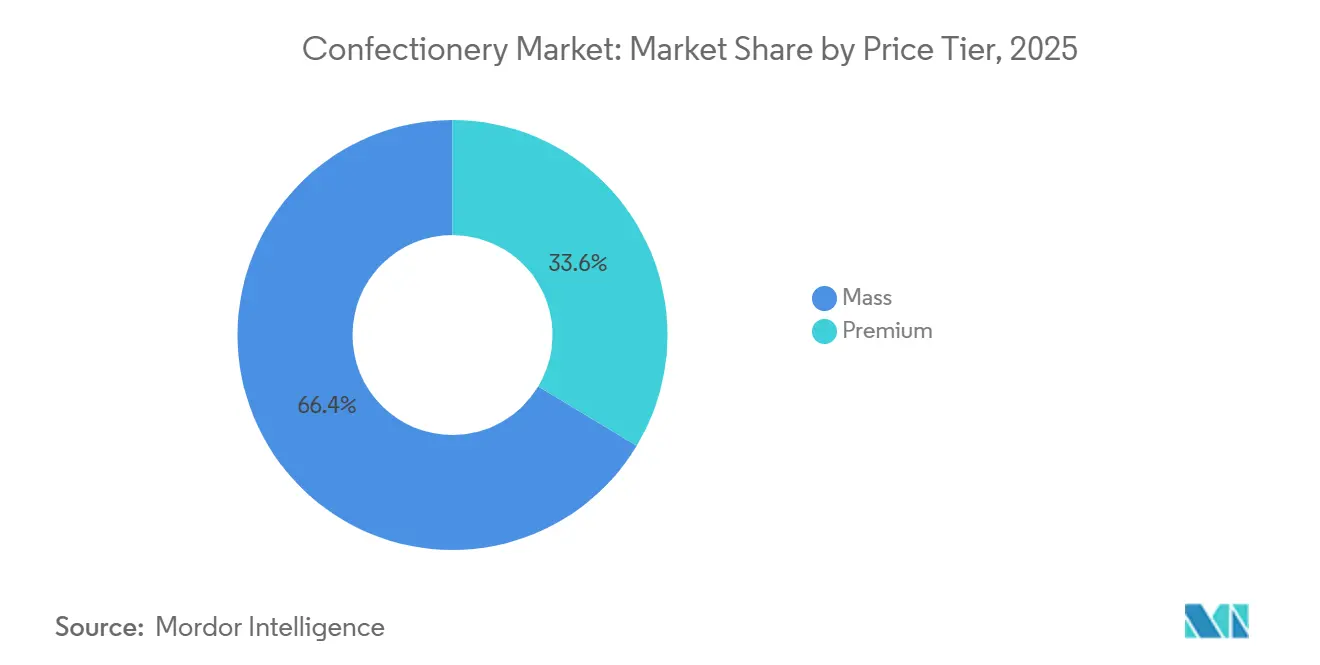

- By price tier, mass-tier products accounted for 66.38% share of the confectionery market size in 2025, and premium offerings are projected to grow at a 6.84% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets commanded 36.54% of the confectionery market size in 2025, yet online retail stores are set to post the fastest 6.81% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Confectionery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and experiential gifting boom | +1.2% | Global, with premium concentration in North America, Western Europe, and Middle East urban centers | Medium term (2-4 years) |

| Demand surges for reduced-sugar, sugar-free, and functional confectionery | +0.9% | Global, led by North America and Europe; accelerating in Asia-Pacific urban markets | Short term (≤ 2 years) |

| Continuous flavor, texture, and health innovation | +0.8% | Global, with R and D hubs in North America and Europe; rapid adoption in Asia-Pacific | Medium term (2-4 years) |

| Packaging and convenience support growth | +0.7% | Global, especially North America and Asia-Pacific convenience channels | Short term (≤ 2 years) |

| Ethical sourcing of ingredients and eco-friendly packaging | +0.6% | Europe and North America regulatory-driven; emerging in Latin America and Asia-Pacific | Long term (≥ 4 years) |

| Advent-calendar-style seasonal bundling | +0.5% | North America and Europe peak impact; growing in Middle East (Ramadan) and Asia-Pacific (Lunar New Year) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Premiumization and experiential gifting boom

Consumers are increasingly allocating their discretionary spending to confectioneries that convey status and provide memorable unboxing experiences, a trend amplified by social media and the growing practice of self-gifting. This shift is particularly evident in the Middle East, where Ramadan and Eid drive demand for luxury chocolate boxes that combine dates with Belgian pralines. Brands like Godiva and Patchi have expanded their retail presence in Dubai and Riyadh to capture high-margin sales during these festive periods. The premiumization trend focuses less on volume growth and more on revenue concentration, as manufacturers recognize that affluent urban consumers in North America, Europe, and the Gulf Cooperation Council are willing to pay a higher price per gram for products offering provenance, craftsmanship, and visually appealing aesthetics. The emotional and experiential value of craft chocolates further drives premiumization, positioning these products as both indulgent treats and gifting options. Brands differentiate themselves through compelling narratives, innovative packaging, and curated flavor profiles. For instance, in June 2025, Cacao Hunters, a premium chocolate brand renowned for its award-winning single-origin chocolates and ethical sourcing, entered the U.S. market, highlighting the growing demand for premium, ethically produced chocolate products.

Demand surges for reduced-sugar, sugar-free, and functional confectionery

Health-conscious consumers, spurred by regulatory mandates, are driving a swift shift in the chocolate, candy, and gum industries towards lower-sugar and sugar-free options. With diseases like diabetes on the rise, consumers are gravitating towards confectionery products with reduced sugar content. According to the latest International Diabetes Federation (IDF) Diabetes Atlas (2025), a notable 11.1% of adults aged 20-79, equating to 1 in 9, are currently living with diabetes [1]Source: International Diabetes Federation, "Facts and figures", idf.org. In 2024, the World Health Organization reiterated its stance that free sugars should make up less than 10% of total energy intake, ideally dropping below 5%. This guideline amplifies the urgency for manufacturers to explore and innovate with alternative sweeteners such as allulose, stevia, and erythritol. Beyond just sugar reduction, the realm of functional confectionery is broadening its horizons. In 2024, South Korea witnessed a surge in popularity for taurine-infused candies and probiotic gummies, as consumers increasingly favor snacks that offer wellness benefits alongside their indulgent nature. The gum segment has nearly transitioned entirely to sugar-free variants. Brands like Mars Wrigley are now introducing caffeine-infused and CBD-infused gums, elevating the category's perception from merely a breath freshener to a functional delivery system. When scaled effectively, this pivot proves lucrative; functional ingredients not only command premium price points but also foster repeat purchases from health-conscious consumers, a demographic that traditional candies often find challenging to retain.

Continuous flavor, texture, and health innovation

To differentiate themselves in a crowded market, manufacturers are leveraging advanced food science. They are utilizing techniques such as surface structuring, deflavored cocoa, and plant-based milk alternatives to create unique sensory experiences. A 2024 patent revealed a method for producing sugar confectionery with structured surfaces, enhancing both mouthfeel and visual appeal. These innovations allow brands to charge premium prices by giving products an artisanal feel, even when produced at an industrial scale. The strategic takeaway is evident: brands that prioritize development and collaborate with ingredient suppliers like Barry Callebaut or Cargill are well-positioned to capture significant market share in fast-growing segments such as vegan chocolate and functional gummies. Manufacturers are also expanding their ingredient portfolios by incorporating a wide variety of exotic elements, including spices, botanicals, fruits, nuts, and regional delicacies. This approach caters to evolving consumer preferences while helping brands create distinctive products in competitive markets. The trend is further driven by increasing demand for experiential consumption, where chocolate serves as a medium for exploring diverse culinary influences and uncovering origin stories. For instance, in November 2024, Lindt introduced its limited-edition Dubai-Inspired Pistachio Chocolate Bar in Düsseldorf. By blending Middle Eastern flavors with premium chocolate, Lindt aimed to captivate European consumers. This example highlights how brands are strategically drawing on cultural inspirations to enhance product appeal, foster stronger consumer engagement, and expand their global presence.

Packaging and convenience support growth

Urbanization, longer commutes, and evolving snacking habits are reshaping traditional meal patterns, driving the growth of single-serve and on-the-go formats. At the same time, manufacturers are increasingly adopting recyclable and compostable materials to meet sustainable packaging mandates. In 2024, Mondelez launched paper-based packaging for Toblerone in select European markets, supporting its goal to make 95% of its packaging recyclable or reusable by 2025. Similarly, Mars introduced compostable M and M's pouches that decompose within 12 weeks in industrial composting facilities. Convenience stores and vending machines remain key distribution channels for single-serve products. Brands are focusing on packaging that can withstand temperature variations and rough handling while featuring bold graphics to encourage impulse purchases. The transition to sustainable materials is not solely driven by environmental concerns; European Union regulations and Extended Producer Responsibility schemes impose financial penalties on non-recyclable packaging. As a result, eco-friendly formats have become both a cost-saving measure and a branding opportunity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cocoa and sugar cost volatility | -0.8% | Global, acute in West Africa cocoa origins and sugar-importing regions | Short term (≤ 2 years) |

| Sugar-content and child-marketing regulation | -0.6% | Europe, UK, Latin America (Chile, Mexico); emerging in Asia-Pacific | Medium term (2-4 years) |

| Carbon-credit land competition squeezing cocoa supply | -0.4% | West Africa (Ivory Coast, Ghana); emerging in Latin America (Ecuador, Peru) | Long term (≥ 4 years) |

| Price-elastic volume drops after sharp hikes | -0.5% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cocoa and sugar cost volatility

Manufacturers are facing significant challenges as fluctuating raw-material prices compress profit margins and necessitate product reformulations, which risk alienating consumers accustomed to established taste profiles. In March 2025, cocoa futures experienced a sharp increase due to export concerns in Ivory Coast, according to the International Cocoa Organization. During their 2024 earnings calls, Mondelez and Hershey emphasized the adverse impact of rising cocoa prices on consumer demand. Both companies indicated that chocolate prices could increase by as much as 50%, with Hershey explicitly stating that it was reformulating its products to reduce cocoa content as a cost-saving measure. Similarly, sugar prices have shown considerable volatility, driven by factors such as unpredictable weather conditions in Brazil and India, biofuel mandates, and currency fluctuations. These dynamics force manufacturers to adopt aggressive hedging strategies or absorb margin compression. However, passing these costs to retailers is not always feasible, as it could result in the loss of valuable shelf space, further complicating the situation for manufacturers.

Sugar-content and child-marketing regulation

Governments across the globe are imposing stricter regulations on sugar content and limiting advertising targeted at children. These measures are driving manufacturers to reformulate their products and cut marketing expenditures in key demographics. The World Health Organization, in its 2024 guidelines, emphasized that free sugars should account for less than 10% of total energy intake, with a preferred target of below 5%. This guidance enables national agencies to introduce taxes, enforce labeling requirements, and implement advertising bans. In 2020, Mexico adopted front-of-pack warning labels and banned child-focused marketing, prompting brands to revamp their packaging and shift advertising efforts toward adult audiences. The European Union is updating nutrient profiles for health claims and strengthening restrictions on child-directed marketing, with implementation expected by 2026. In contrast, India's Food Safety and Standards Authority is enhancing sugar-labeling regulations but has not yet introduced a confectionery-specific tax. These varying regulations worldwide require brands to develop region-specific formulations and packaging, increasing operational complexity and reducing economies of scale.

Segment Analysis

By Product Type: Plant-Based Variants Reshape Chocolate Leadership

In 2025, chocolate accounted for 54.28% of the market value, reinforcing its position as the premium anchor of the category. However, the Sugar Confectionery segment is expected to grow faster, with a projected 6.10% CAGR through 2031. This growth is fueled by health-conscious consumers seeking functional mints, probiotic gummies, and portion-controlled hard candies. The International Cocoa Organization (ICCO) reported that Africa produced approximately 3.46 million tons of cocoa beans in the 2024/2025 season [2]Source: International Cocoa Organization (ICCO), "Production of cocoa beans worldwide", icco.org.. This highlights Africa's critical role in the global cocoa supply chain and emphasizes the need for sustainable practices in these key producing regions. By integrating sustainability into their sourcing strategies, chocolate manufacturers can mitigate reputational and supply risks while capitalizing on the expanding segment of ethically conscious consumers, positioning sustainability as a key growth driver. Dark Chocolate is steadily gaining market share within the chocolate segment, as brands focus on its antioxidant benefits and reduced sugar content. Milk and White Chocolate remain the volume leaders but are under pressure to reformulate due to WHO guidelines and national regulations advocating for sugar reduction. The rapid growth of Sugar Confectionery reflects its versatility: Pastilles, Gummies, and Jellies are now infused with vitamins, probiotics, and adaptogens, transforming them from children's treats into functional snacks for adults.

Snack Bars are a high-growth subsegment. Protein Bars and Energy Bars are increasingly used as meal replacements and post-workout recovery options, while Cereal Bars and Fruit and Nut Bars cater to families seeking convenient breakfast solutions. General Mills and Kellogg lead the Cereal Bar market with brands like Nature Valley and Nutri-Grain but face growing competition from startups promoting clean labels and single-ingredient formulations. Gums, including both Chewing Gum and Bubble Gum, experienced declines during the pandemic as mask-wearing reduced consumption, and recovery has been slow. In response, Mars Wrigley and Mondelez are pivoting toward functional gums infused with caffeine, CBD, or teeth-whitening agents to justify premium pricing and reposition the category as a wellness product rather than a commodity breath freshener. This trend reflects a broader shift: product-type boundaries are becoming less distinct. Chocolate bars now compete with protein bars for on-the-go nutrition, and gummies rival vitamin supplements for functional benefits. This shift is pushing manufacturers to redefine their categories and invest in cross-category innovation.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Type: E-Commerce Rewards Multipack Economics

In 2025, single-serve formats accounted for 58.97% of the market value, driven by convenience stores, vending machines, and impulse purchases at checkout counters. However, multipacks are expected to grow faster, with a projected 6.38% CAGR through 2031. This growth is primarily fueled by e-commerce platforms and warehouse clubs, which attract consumers by offering lower per-unit costs for bulk purchases. To address the needs of online shoppers, who cannot physically inspect products, confectionery brands are redesigning multipacks with features such as resealable closures, transparent windows, and portion-control options. Mondelez introduced paper-based Toblerone packaging in select European markets in 2024, aligning with its goal to make 95% of its packaging recyclable or reusable by 2025. The shift toward sustainable materials is gaining momentum, particularly as Europe’s Extended Producer Responsibility schemes impose financial penalties on non-recyclable packaging. Innovations in single-serve packaging emphasize portability and shelf appeal. Mars tested compostable M and M's pouches that decompose within 12 weeks in industrial composting facilities, while Nestlé launched paper-based KitKat wrappers in several countries, aiming to eliminate plastic entirely.

Multipacks are transitioning from simple bundling to variety packs that combine multiple flavors or formats. This approach not only encourages product trials but also reduces decision fatigue for consumers shopping online or at warehouse clubs. Ferrero's Kinder variety packs, which include Kinder Bueno, Kinder Chocolate, and Kinder Joy in one box, illustrate this strategy. The distribution of packaging types highlights channel dynamics: convenience stores and gas stations prefer single-serve formats for impulse purchases, while supermarkets and hypermarkets allocate shelf space to both formats. Online retailers prioritize multipacks to distribute shipping costs across higher order values. Manufacturers face the challenge of managing SKU proliferation, since each packaging format requires separate production runs and inventory management, while meeting the demands of diverse channels and occasions. This challenge often benefits larger players with flexible manufacturing capabilities and advanced demand-planning systems.

By Price Tier: Premium Gains Outpace Mass Despite Economic Headwinds

In 2025, mass-tier products represented 66.38% of the market value, highlighting confectionery's traditional role as an affordable indulgence. However, the premium segment is expected to grow faster, with a projected 6.84% CAGR through 2031. This growth is fueled by affluent consumers opting for single-origin chocolates, artisanal flavors, and ethically certified products, which often command price premiums of 3 to 5 times over mass-market alternatives. In 2024, Lindt launched its 'Excellence Plant-Based Milk Chocolate', targeting affluent flexitarians seeking premium taste without dairy, priced 40% higher than conventional milk chocolates. Meanwhile, Godiva and Hotel Chocolat are expanding their retail presence in Middle Eastern cities like Dubai and Riyadh. Here, occasions such as Ramadan and Eid drive demand for luxury chocolate boxes that combine dates with Belgian pralines. These seasonal peaks, while accounting for a small portion of annual volume, generate a significant share of revenue.

Mass-tier products are under pressure from two key factors: rising cocoa costs that compress margins and regulatory requirements to reduce sugar content in formulations. These challenges threaten the segment's core attributes of simplicity and affordability. Hershey's reformulation strategy, adjusting cocoa content to maintain affordability, illustrates the trade-offs involved in protecting mass-market share. While such changes aim to keep prices competitive, they risk alienating loyal consumers due to potential taste alterations. The market is increasingly bifurcating: premium brands can pass on cost increases as their consumers prioritize quality and provenance over price, while mass brands must either absorb costs or risk losing volume to private-label competitors offering lower prices. Ferrero's 2024 acquisition of Nestlé's US confectionery brands, such as Butterfinger, BabyRuth, and Crunch, reflects a strategic bet that scaling mass-tier manufacturing can mitigate margin pressures. Conversely, Lindt's focus on premium single-origin bars underscores a strategy of differentiation to guard against commoditization. The price-tier divide also varies by region: North America and Europe show strong trends toward premiumization, while Asia-Pacific and Latin America remain dominated by mass-market products. However, urban centers in India, China, and Brazil are witnessing the emergence of premium segments, driven by rising middle-class incomes.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Surge Reshapes Shelf-Space Economics

Supermarkets and Hypermarkets held a 36.54% share of the distribution value in 2025, leveraging their scale, promotional efforts, and strategic placement of impulse items at checkout counters. However, Online Retail Stores are expected to grow at a faster rate, with a projected 6.81% CAGR through 2031. E-commerce platforms are introducing subscription models, providing personalized recommendations, and ensuring ingredient transparency, advantages that traditional retail struggles to replicate on a large scale. These online channels enable brands to emphasize their sustainability efforts, detail ingredient sourcing, and present customer reviews in ways that physical stores cannot. Additionally, subscription models such as monthly curated deliveries of chocolate or snack bars create consistent revenue streams, reducing reliance on seasonal sales peaks. This growth in online retail is supported by increasing digital penetration and evolving consumer purchasing behaviors. The International Telecommunication Union (ITU) reported that in 2024, 5.5 billion people were using the internet, accounting for 68% of the global population, up from 65% in the previous year [3]Source: International Telecommunication Union (ITU), "Internet use continues to grow", itu.int.. This rise in connectivity has significantly expanded the potential consumer base for e-commerce.

Convenience Stores remain essential in urban areas and transit hubs, catering to single-serve impulse purchases. Brands are focusing on packaging that can withstand temperature changes and rough handling while featuring bold graphics to encourage unplanned purchases. Other Distribution Channels, such as vending machines, specialty stores, and duty-free outlets, serve niche occasions but collectively contribute significant volume, particularly in airports and tourist destinations where premium pricing is widely accepted. A strategic challenge arises from channel conflict: direct-to-consumer sales can erode retailer volume, forcing brands to balance margin capture against the risk of retailer pushback, such as reduced shelf space or promotional support. The distribution-channel dynamics also reflect generational preferences: millennials and Gen Z favor online shopping and value transparency, while older consumers prefer in-store browsing and immediate gratification. This generational divide requires brands to implement omnichannel strategies that address the needs of both groups without compromising brand equity.

Geography Analysis

North America represented 36.57% of the global confectionery market in 2025, supported by the U.S.'s strong per-capita consumption and established retail infrastructure. However, the region's growth is slowing as health trends and regulatory pressures drive consumers toward reduced-sugar and functional alternatives. While Canada and Mexico hold smaller shares, they exhibit unique characteristics: Canada's market increasingly reflects U.S. trends, with a focus on premiumization and plant-based options. As the region matures, growth will primarily come from premiumization, functional innovations, and shifts in sales channels rather than volume increases. Brands that fail to address the health-conscious shift risk losing market share to agile startups and private labels.

Asia-Pacific is projected to achieve a strong 6.54% CAGR through 2031, fueled by rising incomes in India, Indonesia, and Vietnam amid expanding GDP in developing Asia. Multinational brands are attracting first-time buyers with localized flavors such as cardamom chocolate and mango gummies. South Korea and Japan emphasize functional and premium offerings, while China's slower consumption growth tempers the regional average. In 2024, Barry Callebaut launched an innovation hub in Singapore to deliver customized coatings and capitalize on the region's growing momentum. In many Southeast Asian cities, digital commerce has surpassed traditional retail, making mobile-first strategies critical for capturing confectionery market growth.

Europe maintains stable volumes but faces stricter nutrient requirements and sustainability regulations. In 2024, Mondelez introduced Cadbury Dairy Milk 30% Less Sugar in the U.K. to anticipate tighter sugar guidelines. Seasonal demand, such as Easter eggs and Christmas pralines, drives markets in Germany, France, and Italy. Meanwhile, Switzerland and Belgium leverage their heritage to secure premium pricing. Nestlé, under cost pressures, invested over CHF 100 million to modernize its Swiss factories and sustain regional production. Eastern European facilities, benefiting from lower labor costs, meet Western demand, enhancing their competitiveness within the broader confectionery market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The confectionery market exhibits moderate fragmentation. Global leaders such as Ferrero International S.A., Mars Incorporated, Mondelēz International Inc., Nestlé S.A., and The Hershey Company hold a dominant position in the confectionery market, accounting for a substantial share of its global value. However, their profitability is being challenged by volatile raw material prices and the increasing costs associated with sustainability-focused investments. To strengthen its distribution network in a market governed by strict front-of-pack labeling regulations and to expand its product offerings beyond chocolate, Mondelez strategically acquired Mexico’s Ricolino.

In the B2B processing segment, Barry Callebaut and Cargill maintain a leading position. They differentiate themselves by introducing innovative solutions such as patented plant-based milks and deflavored cocoa, which allow their clients to scale up clean-label claims effectively. To address the growing demand for vegan products without compromising on taste, Mars has collaborated with Perfect Day, leveraging precision fermentation technology to produce dairy proteins without the use of cows. Concurrently, Nestlé and Ferrero are piloting blockchain technology to enhance traceability at the farm level, ensuring their product portfolios align with the requirements of the EU Deforestation Regulation.

Emerging players are gaining momentum with innovative offerings such as protein snack bars, CBD-infused gums, and single-origin bean-to-bar chocolates. During periods of inflation, private labels are utilizing warehouse clubs to provide cost-effective alternatives to mainstream brands. Established companies face the strategic decision of pursuing acquisitions or investing in greenfield innovations. However, their extensive global reach, strong marketing capabilities, and expertise in commodity hedging provide them with a competitive edge. Overall, the confectionery market remains moderately concentrated, where factors such as scale, advanced R and D capabilities, and a focus on responsible sourcing are critical for achieving long-term resilience and success.

Confectionery Industry Leaders

-

Mars Incorporated

-

Mondelēz International Inc.

-

The Hershey Company

-

Nestlé S.A.

-

Ferrero International S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Mars Inc. has unveiled a fresh lineup of confectionery products, including M and M's, Twix, and more. Among the new offerings, M and M's introduces 'Winter Blend', a flavor crafted specifically for winter-themed baking and gifting.

- September 2025: Cadbury Dairy Milk has expanded its portfolio in India with the launch of Milkinis, a crème-filled chocolate bar targeting younger, on-the-go consumers. It is available in single and twin packs.

- September 2025: Ferrero Rocher introduced new Ferrero Rocher chocolate squares, offering a modern variation of the brand's iconic gold-wrapped praline. The range includes Milk Hazelnut, Dark Hazelnut, White Hazelnut, Caramel Hazelnut, and an assorted selection.

- May 2025: Nestle has introduced new chocolate bar flavors such as Aero Strawberry, Milkybar Chokito, and Milkybar Crunch Block. The Milkybar Chokito features caramel nougat combined with cereal balls, while the Milkybar Crunch Block contains crunchy cereal pieces coated in white chocolate.

Global Confectionery Market Report Scope

By Product Type

| Chocolate | Dark Chocolate | |

| Milk and White Chocolate | ||

| Sugar Confectionery | Hard Candy | |

| Mints | ||

| Pastilles, Gummies, and Jellies | ||

| Toffees and Nougats | ||

| Lollipops | ||

| Other | ||

| Snack Bar | Cereal Bar | |

| Energy Bar | ||

| Protein Bar | ||

| Fruit and Nut Bar | ||

| Gums | Chewing Gum | Sugar Chewing Gum |

| Sugar-free Chewing Gum | ||

| Bubble Gum | ||

Packaging type

| Single-serve |

| Multipacks |

Price Tier

| Mass |

| Premium |

Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Chocolate | Dark Chocolate | |

| Milk and White Chocolate | |||

| Sugar Confectionery | Hard Candy | ||

| Mints | |||

| Pastilles, Gummies, and Jellies | |||

| Toffees and Nougats | |||

| Lollipops | |||

| Other | |||

| Snack Bar | Cereal Bar | ||

| Energy Bar | |||

| Protein Bar | |||

| Fruit and Nut Bar | |||

| Gums | Chewing Gum | Sugar Chewing Gum | |

| Sugar-free Chewing Gum | |||

| Bubble Gum | |||

| Packaging type | Single-serve | ||

| Multipacks | |||

| Price Tier | Mass | ||

| Premium | |||

| Distribution Channel | Supermarket/Hypermarket | ||

| Online Retail Store | |||

| Convenience Store | |||

| Other Distribution Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Sweden | |||

| Belgium | |||

| Poland | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Thailand | |||

| Singapore | |||

| Indonesia | |||

| South Korea | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| South Africa | |||

| Saudi Arabia | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF