Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

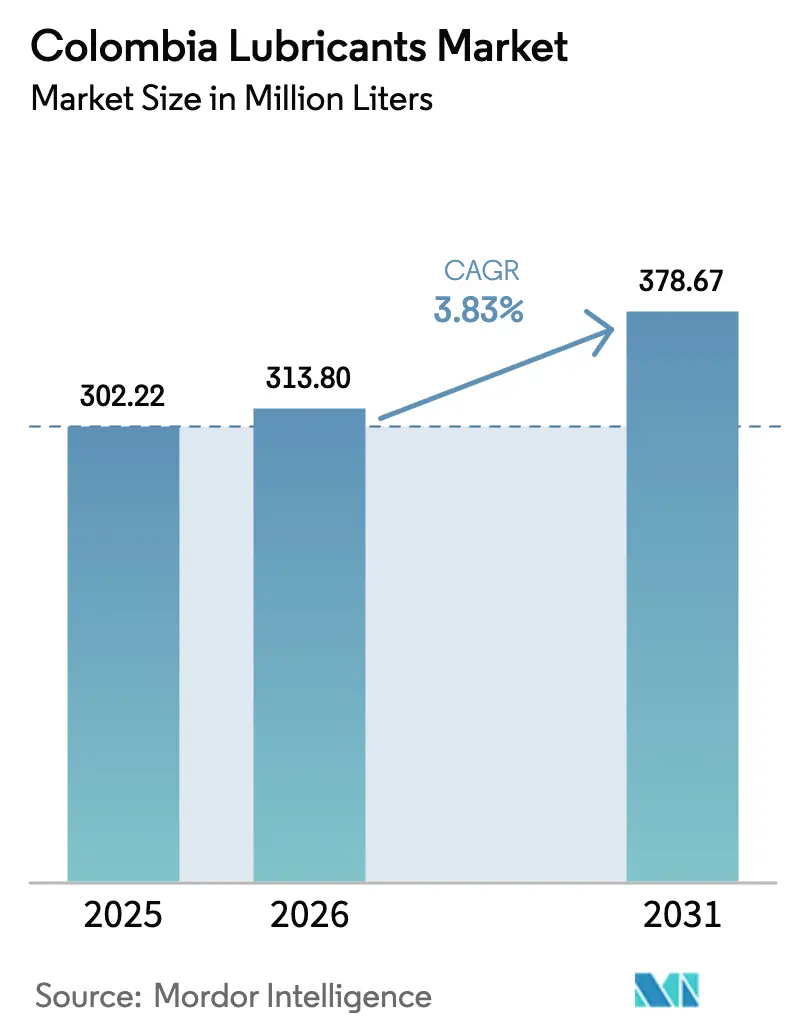

| Base Year Market Size (2025) | 302.22 Million liters |

| Market Volume (2026) | 313.80 Million liters |

| Market Volume (2031) | 378.67 Million liters |

| Growth Rate (2026 - 2031) | 3.83% CAGR |

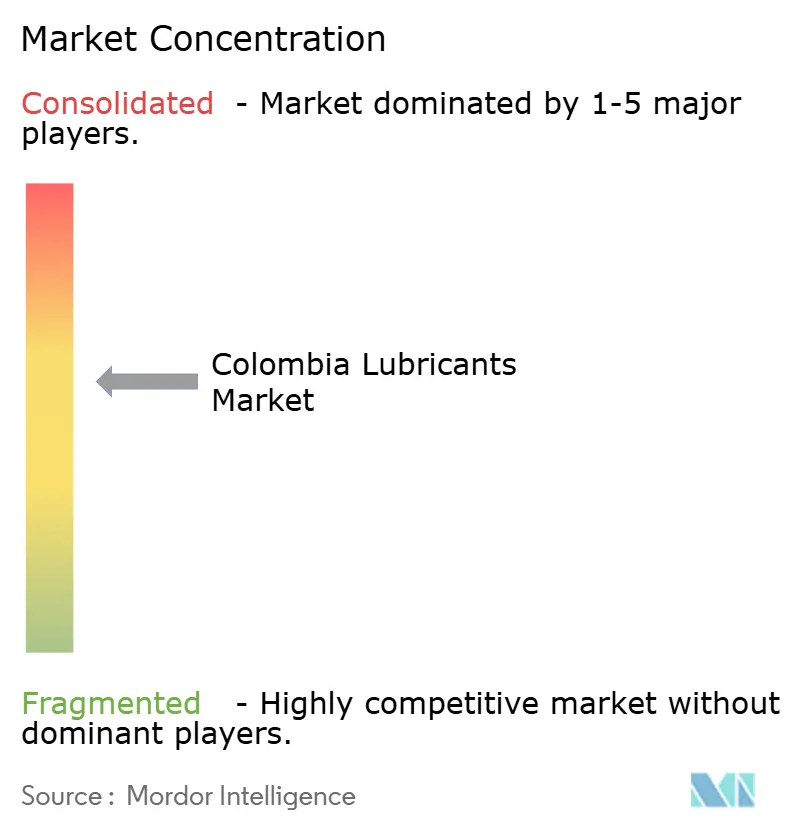

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Lubricants Market Analysis by Mordor Intelligence

The Colombia Lubricants Market size is expected to grow from 302.22 Million liters in 2025 to 313.80 Million liters in 2026 and is forecast to reach 378.67 Million liters by 2031 at 3.83% CAGR over 2026-2031. The primary driver of short-term growth is the rebound in new vehicle and motorcycle registrations. Medium-term growth is influenced by Ecopetrol’s significant industrial capital expenditures, which are increasing demand for turbine, hydraulic, and transformer oils. The shift toward continuously variable and dual-clutch transmissions is driving demand for specialty automatic transmission fluid (ATF) grades. Additionally, warranty-backed OEM programs are promoting the adoption of synthetic oils, although mineral oils continue to dominate in rural areas. Competitive dynamics are intensifying as Terpel integrates ExxonMobil’s local assets, Saudi Aramco restructures Primax, and global players defend their market share with high-performance product portfolios that comply with API SP and ILSAC GF-6B standards. Base-oil supply remains a structural challenge, with Group III imports subject to freight volatility and occasional lead times of up to eight weeks.

Key Report Takeaways

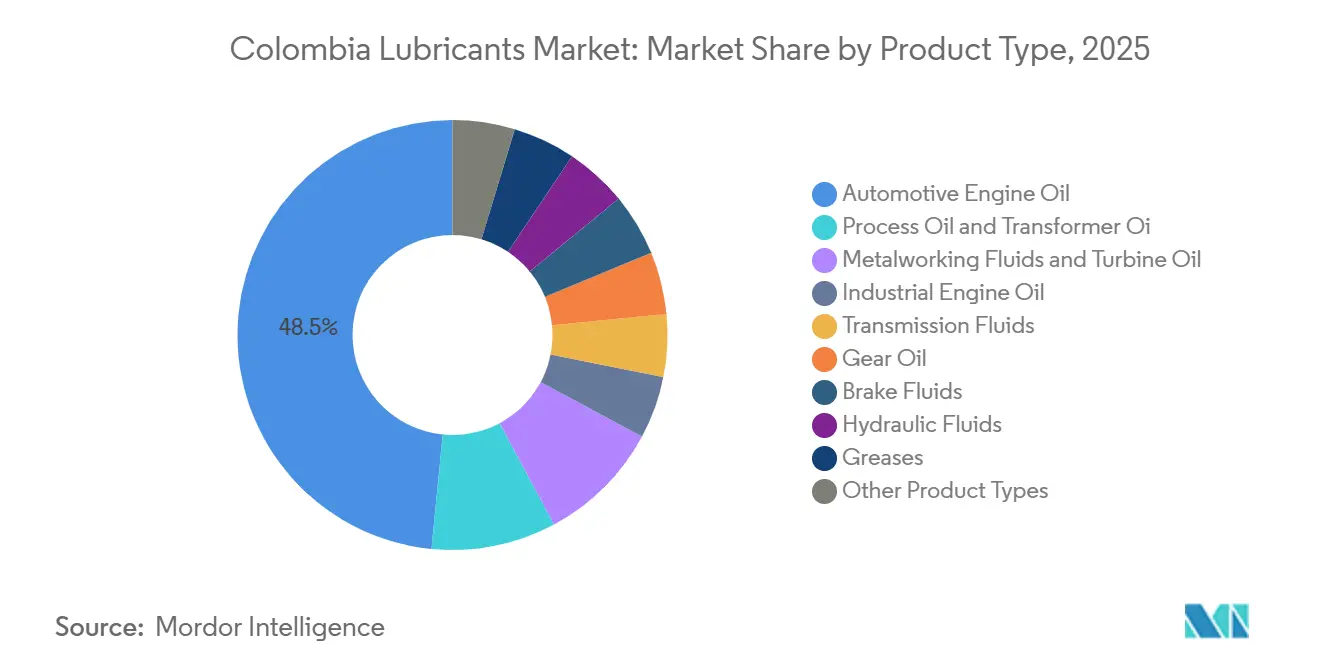

- By product type, automotive engine oil led with 48.45% of the Colombia lubricants market share in 2025, while transmission fluids are forecast to expand at a 4.68% CAGR through 2031.

- By base stock type, mineral oil-based lubricants accounted for 63.50% of the Colombia lubricants market share in 2025, while synthetic lubricants are set to grow at a 4.38% CAGR through 2031.

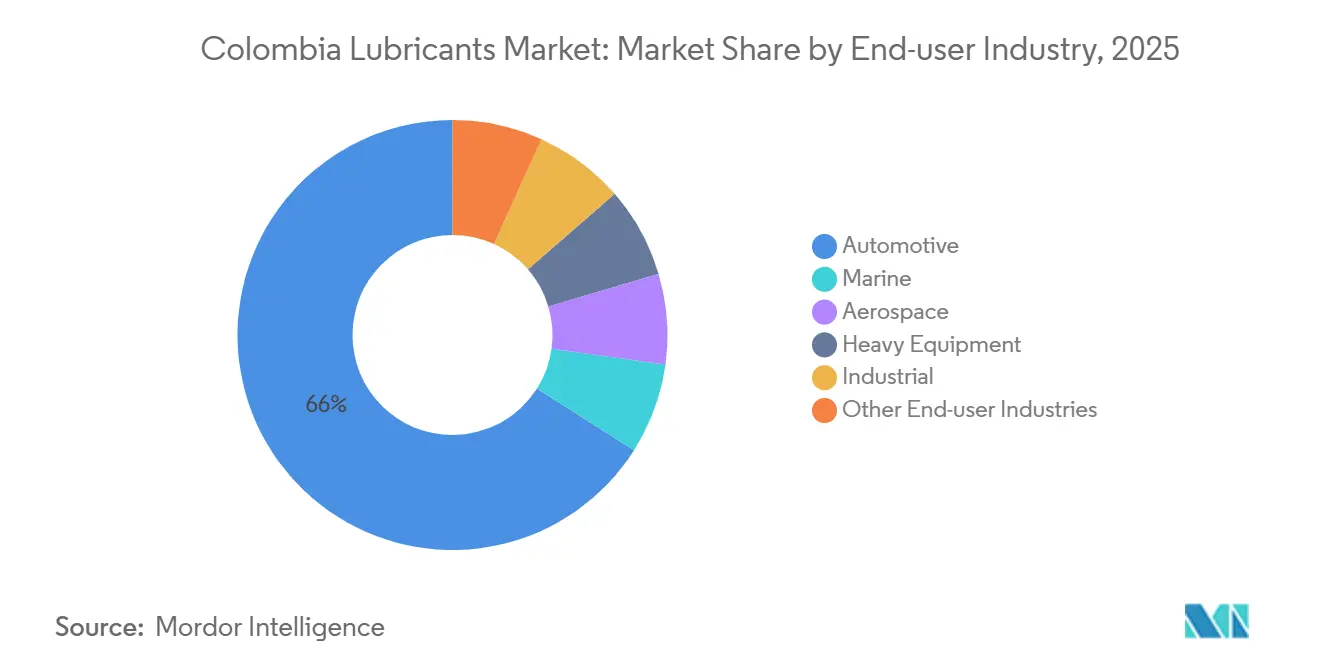

- By end-user industry, automotive captured 66.00% of the Colombia lubricants market share in 2025, while the industrial is set to grow at a 4.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovering Vehicle and Motorcycle Parc | +1.2% | National, with early gains in Bogotá, Medellín, Cali | Short term (≤ 2 years) |

| Industrial CAPEX Rebound in Mining and Power | +0.9% | Andean corridor, Caribbean coast (Cerrejón, Cartagena) | Medium term (2-4 years) |

| OEM-Backed Warranty Programs for Premium Synthetics | +0.7% | Urban centers, commercial-fleet hubs | Medium term (2-4 years) |

| Palm-Oil Tax Incentive Driving Bio-Lubricants | +0.3% | Eastern plains (Meta, Casanare), Magdalena Medio | Long term (≥ 4 years) |

| Predictive-Maintenance Adoption Requiring High-Performance Fluids | +0.5% | Industrial corridors, mining operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovering Vehicle and Motorcycle Parc

Passenger vehicle sales rose by 26.5% year-on-year to 254,205 units in 2025, reversing three years of consecutive declines and increasing lubricant demand in Bogotá, Medellín, Cali, and secondary cities. Hybrid and battery-electric models contributed 34.5% of the additional volume, resulting in a divided aftermarket where internal-combustion vehicles require API SP oils, while EVs need specialty greases and dielectric fluids. Motorcycle registrations, which have historically exceeded passenger car registrations, continue to support demand for two-stroke and four-stroke oils in cost-sensitive workshops. Stop-and-go traffic congestion is reducing effective drain intervals despite the use of synthetic oils. Dealerships are now offering OEM-approved oils bundled with prepaid service packages, leading to higher per-liter value even as synthetic oil adoption moderates overall volume growth.

Industrial CAPEX Rebound in Mining and Power

Ecopetrol’s 2026 capital program, valued between USD 5.7 billion and USD 7.0 billion, focuses on refinery upgrades and new combined-cycle gas turbines, increasing demand for ISO VG 32 and 46 turbine oils, transformer oils, and hydraulic fluids. Mining activities outside the coal sector, including gold, nickel, and copper in Antioquia and Chocó, are expanding, driving the need for heavy-duty gear oils and greases capable of withstanding high shock loads. ExxonMobil documented a Colombian mine that extended gear-oil drain intervals fivefold and achieved annual savings of USD 200,000 using Mobil SHC 632 synthetic gear oil. Power-generation operators are piloting real-time oil-analysis systems for predictive maintenance, further encouraging the use of high-performance synthetic oils.

OEM-Backed Warranty Programs for Premium Synthetics

Renault, Kia, Mazda, and Toyota now mandate the use of fully synthetic or semi-synthetic engine oils in Colombia to protect turbochargers and after-treatment systems. Products such as Terpel’s Oiltec and Ultrek lines, Shell Helix Ultra, and Mobil 1, which hold multiple OEM approvals, are sold at premiums of up to 50% over mineral oils. Fleet operators are adopting 15W-40 and 10W-30 synthetic oils, which extend service intervals from 10,000 km to 25,000 km, reducing downtime and labor costs. A freight operator reported a sixfold increase in bearing life and annual savings of USD 85,000 by using Mobilith SHC 007 synthetic grease. Larger blending plants with ISO 9001 certification benefit from warranty requirements that direct volumes toward approved brands.

Palm-Oil Tax Incentive Driving Bio-Lubricants

Colombia produced 1.89 million metric tons of palm oil in 2024 and offers tax credits for bio-lubricant blending, though current production remains limited to pilot volumes in Meta and Casanare. Smallholder cooperatives lack esterification capacity, and public procurement regulations do not mandate bio-content. Fedepalma estimates that bio-lubricants could utilize 50,000 metric tons of palm oil annually by 2030 if policy support is implemented. However, fiscal constraints delayed relevant legislation in 2025. At present, bio-based hydraulic fluids and chainsaw oils remain niche products, primarily marketed to environmentally conscious forestry operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural Shortage of Group II/III Base Oils and Additives | -0.8% | National, acute in Bogotá and Medellín blending hubs | Short term (≤ 2 years) |

| Government Price Caps Squeezing Distributor Margins | -0.5% | National, most severe in regulated fuel-station networks | Medium term (2-4 years) |

| Grey-Channel Imports Undermining Quality Standards | -0.3% | Border regions (Cúcuta, Ipiales), informal retail channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Price Caps Squeezing Distributor Margins

Retail fuel prices are regulated by the Ministry of Mines and Energy, and station operators combine lubricants with gasoline to attract customers[1]Ministerio de Minas y Energía, “Resolución de Precios de Combustibles 2025,” minenergia.gov.co. In 2025, the peso depreciated by 8% against the dollar, increasing landed lubricant costs. However, service-station distributors could not fully transfer these cost increases to customers without risking a shift to grey-market sellers. This pressure on margins is driving market consolidation, as seen in Uno Corp’s ongoing deal to acquire Primax.

Grey-Channel Imports Undermining Quality Standards

Counterfeit oils entering through informal crossings at Cúcuta, Ipiales, and Leticia accounted for 10%-15% of national volume in 2024, according to trade groups. These products frequently fail to meet NTC viscosity and flash-point standards, leading to premature engine damage. Although the Superintendencia de Industria y Comercio has proposed QR-code traceability to address this issue, it faces challenges due to limited inspection resources[2]Superintendencia de Industria y Comercio, “Proyecto de Código QR para Lubricantes,” sic.gov.co. Authentic lubricant manufacturers need to prioritize consumer education and channel audits to safeguard their brand reputation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transmission Fluids Outpace Engine Oils

Automotive engine oil accounted for 48.45% of the Colombia lubricants market share in 2025, driven by the nation’s 3.2 million-unit passenger car parc. However, transmission fluids are expected to grow at a 4.68% CAGR through 2031, supported by increasing sales of CVT, DCT, and eight-speed automatic transmissions that require Dexron VI or Mercon LV-approved ATFs. As a result, the market size for transmission fluids is expanding faster than that of engine oils, although longer ATF drain intervals partially offset volume growth. Specialty gear oils and hydraulic fluids cater to the growing needs of mining and construction fleets. For example, ExxonMobil’s Mobil SHC 632 reduced lubricant costs by USD 200,000 at a mining site, emphasizing the value of synthetic durability. Niche categories such as brake fluids and metalworking fluids remain essential for ISO and ASTM compliance, while transformer and turbine oils are becoming more relevant as power infrastructure modernizes.

Second-order effects are influencing the product mix. EV adoption reduces demand for engine oils but increases the need for high-performance greases and dielectric coolants to stabilize battery temperatures. Calcium sulfonate complex greases address high-load applications in agriculture and mining, where contamination risks are significant. Process oils for rubber and plastics benefit from Colombia’s growing petrochemical investments, but remain a minor segment in terms of overall volume.

By Base Stock Type: Synthetics Gain on Warranty Mandates

Mineral oils held 63.50% of the Colombia lubricants market share in 2025, as two-wheelers, agricultural equipment, and rural workshops prioritize cost-effectiveness. However, synthetic lubricants are projected to grow at a 4.38% CAGR through 2031, driven by OEM warranty requirements for API SP-rated full synthetics in turbocharged gasoline and common-rail diesel engines. Semi-synthetics bridge affordability gaps by blending Group II base oils with polyalphaolefins. Structural shortages in Group III base oils limit supply, forcing blenders to prioritize high-margin OEM channels. Bio-based lubricants remain in the experimental phase, with pilot programs in Meta and Casanare validating palm-ester hydraulic oils. However, the lack of large-scale esterification capacity hinders commercialization despite tax incentives.

By End-user Industry: Industrial Segment Accelerates

The automotive segment accounted for 66.00% of the Colombia lubricants market size in 2025. However, industrial applications are projected to grow at a 4.44% CAGR through 2031, supported by Ecopetrol’s USD 5.7 billion to USD 7.0 billion refinery and power-generation investments. Commercial vehicle fleets consume significant volumes of 15W-40 and 10W-30 diesel synthetics, while two-wheelers in secondary cities sustain demand for low-viscosity mineral oils. Heavy equipment in mining and construction drives demand for ISO 100-320 gear oils and NLGI 2 greases. Marine and aerospace applications remain niche, while digital-platform volumes are still emerging, offering potential for direct-to-consumer services.

Geography Analysis

Bogotá, Medellín, Cali, Barranquilla, and Bucaramanga collectively account for the majority of the Colombia lubricants market size, reflecting dense vehicle parcs and concentrated industrial activity. Bogotá leads in synthetic lubricant adoption due to dealership-enforced OEM warranties. Medellín’s textile and food-processing industries consume significant volumes of hydraulic and metalworking fluids, while Cali’s logistics role near the Pacific port drives demand for ATFs and diesel engine oils among commercial fleets. Cartagena’s refinery produces Group I and limited Group II base stocks, meeting coastal demand and reducing import lead times for certain products.

Secondary cities such as Pereira, Manizales, and Villavicencio are outpacing national growth due to infrastructure development and increased farm mechanization. Villavicencio serves as a hub for lubricants in the Llanos Orientales oil and cattle regions, including pilot bio-lubricant projects utilizing local palm oil. Border towns like Cúcuta and Ipiales face higher grey-market penetration, which undermines brand-name sales as smugglers exploit price differences with Venezuela and Ecuador. The Andean corridor, spanning Pasto, Bogotá, and Bucaramanga, remains an industrial hub with significant demand for high-film-strength synthetics in mining, cement, and metallurgy.

Coastal power plants and petrochemical hubs in Barranquilla and Cartagena sustain steady demand for turbine and transformer oils. Renewable energy integration is driving demand for dielectric fluids capable of handling higher voltage fluctuations, representing a niche but rapidly growing segment. Regional disparities in synthetic lubricant adoption persist, with urban centers exceeding 30% synthetic share, while rural areas remain below 10%. This presents long-term opportunities for premiumization as warranty enforcement and fleet economics evolve.

Competitive Landscape

Terpel’s acquisition of ExxonMobil’s Colombian lubricants factory and distribution arm for COP 271.2 billion (USD 59.6 million) in late 2025, followed by a 2026 port-terminal deal, consolidates market share under a unified platform. Shell, Chevron, and TotalEnergies import finished products or operate blending partnerships, maintaining their positions in premium segments through strong OEM endorsements. Primax Colombia, with 1,024 stations and a blending plant, is awaiting regulatory approval for its acquisition by Uno Corp. The asset previously changed ownership when Saudi Aramco acquired Grupo Romero’s Primax group for USD 3.5 billion in March 2025.

Local players such as COÉXITO and Petromil cater to niche industrial and agricultural markets with competitive pricing and regional logistics. Grey-market competition pressures formal blenders to differentiate through warranty-approved synthetics, loyalty programs, and predictive maintenance analytics. Emerging opportunities include EV-specific greases and dielectric coolants, where no dominant brand has yet emerged despite the sale of 19,724 BEVs in 2025. Digital distribution remains under 5% of total lubricant sales, offering potential for disruption through direct-to-consumer subscription models.

International investments highlight the strategic importance of the Colombian market. Repsol aims to double its global lubricants EBITDA to EUR 126 million by 2030, identifying Colombia as a key target in Latin America. Gulf Oil is leveraging REFAX’s station network to explore market entry, while Brazilian independent Moove’s regional acquisitions suggest potential future bids in Colombia. While consolidation may enhance blending scale and logistics, regulatory scrutiny could necessitate divestitures to maintain competitive balance.

Colombia Lubricants Industry Leaders

Chevron Corporation

Shell plc

BP p.l.c.

Exxon Mobil Corporation

Organización Terpel S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Colombia announced that it would no longer approve new oil or large-scale mining projects within its Amazon biome, which constituted 42% of the country's territory. This is expected to impact the lubricant market by potentially reducing the availability of raw materials derived from oil production in the region.

- August 2025: Honduran conglomerate UNO Corp, a subsidiary of Terra Group, acquired an 80% stake in Primax Colombia S.A. This acquisition, which included over 880 service stations and associated fuel distribution infrastructure such as a blending plant, is expected to strengthen the lubricant market by expanding distribution capabilities.

Colombia Lubricants Market Report Scope

Lubricants are substances that, when applied as a coating between solid surfaces, reduce friction, heat, and wear. Lubricant products are made from a combination of base oils and additives. Lubricants are utilized to adjust the friction and wear of surfaces in contact with bodies that are moving relative to one another, lowering the heat released when the surfaces move. The composition of base oil in the formulation of lubricants is primarily between 75% and 90%.

The Colombia lubricants market is segmented by product type, base stock type, and end-user industry. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

How large is the Colombia lubricants market?

The Colombia lubricants market stands at 313.80 million liters in 2026 and is expected to reach 378.67 million liters by 2031.

Which product type is forecast to grow fastest through 2031?

Transmission fluids lead with a projected 4.68% CAGR through 2031 as CVT and DCT gearboxes proliferate.

Which base stock type is forecast to grow fastest through 2031?

Synthetic lubricants are rising at a 4.38% CAGR through 2031.

What role will bio-lubricants play?

Palm-based bio-lubricants remain at pilot scale; without mandatory blends or procurement rules, commercial volumes should stay minor until at least 2030.

Page last updated on: