Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

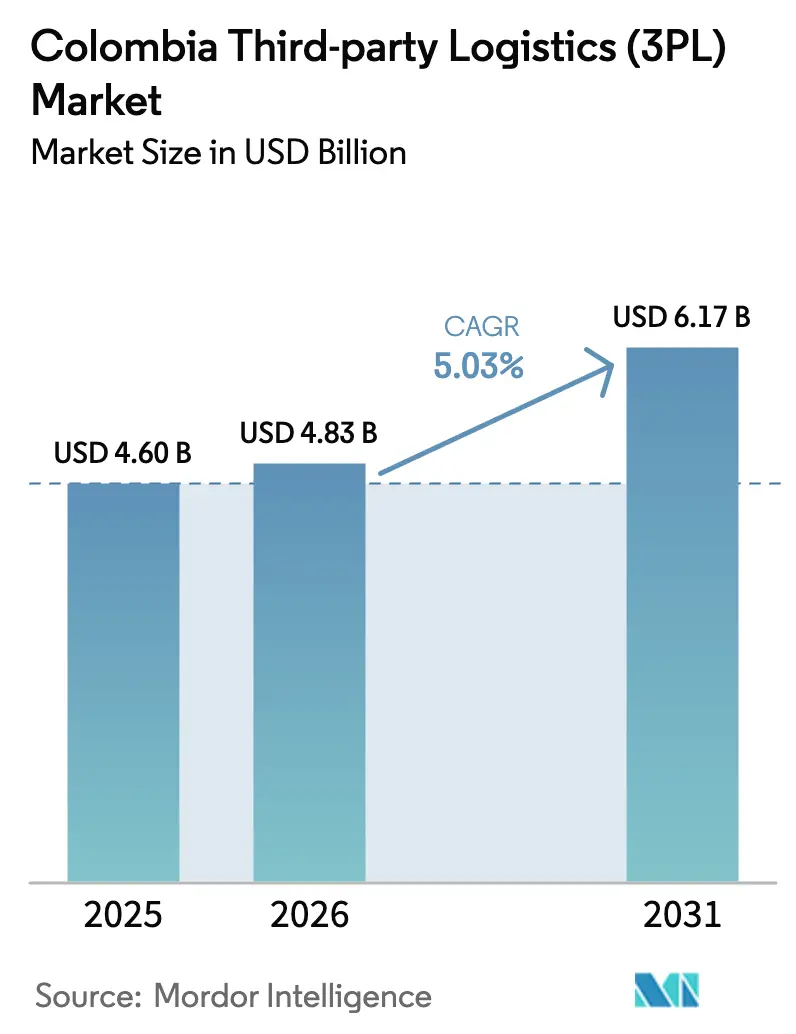

| Base Year Market Size (2025) | USD 4.60 Billion |

| Market Size (2026) | USD 4.83 Billion |

| Market Size (2031) | USD 6.17 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Third-party Logistics (3PL) Market Analysis by Mordor Intelligence

The Colombia Third-party Logistics Market size is estimated at USD 4.83 billion in 2026, and is expected to reach USD 6.17 billion by 2031, at a CAGR of 5.03% during the forecast period (2026-2031).

Demand is accelerating as nearshoring, port modernization, and end-to-end digitization reshape shipment patterns. E-commerce platforms are expanding beyond Bogota into secondary cities, stimulating parcel volumes and prompting 3PLs to roll out micro-fulfillment sites. Port upgrades at Buenaventura and the forthcoming Puerto Antioquia are re-routing exports toward coastal corridors, while Magdalena River and rail investments promise new inland options that ease reliance on mountain roads. Digital transportation and warehouse management systems are lowering entry barriers for small carriers, yet cargo-security expenses and currency volatility continue to squeeze margins. Competition now hinges less on fleet size and more on visibility platforms that integrate trucking, rail, river, and ocean legs into a single control tower.

Key Report Takeaways

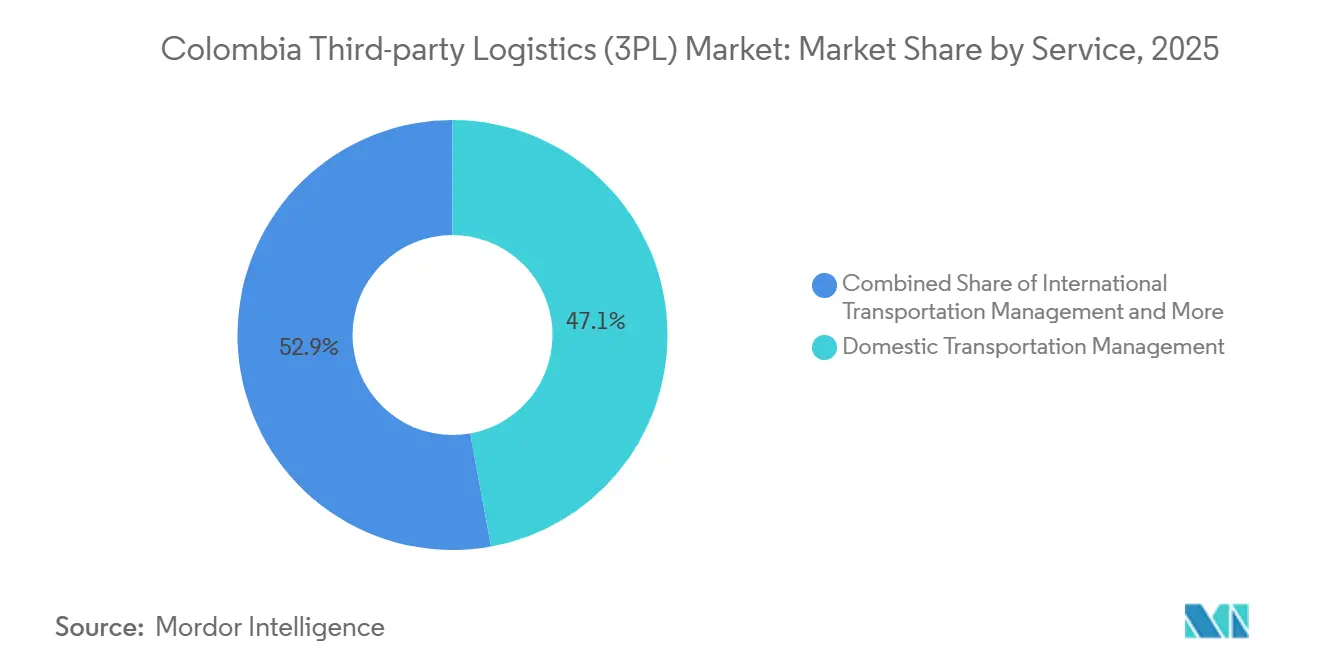

- By service type, domestic transportation commanded 47.14% of revenues in 2025; Value-Added Warehousing & Distribution is set to expand at a 6.09% CAGR to 2031.

- By logistics model, asset-light providers controlled 45.23% of the Colombia third-party logistics (3PL) market size in 2025, yet Hybrid models are advancing at a 5.73% CAGR.

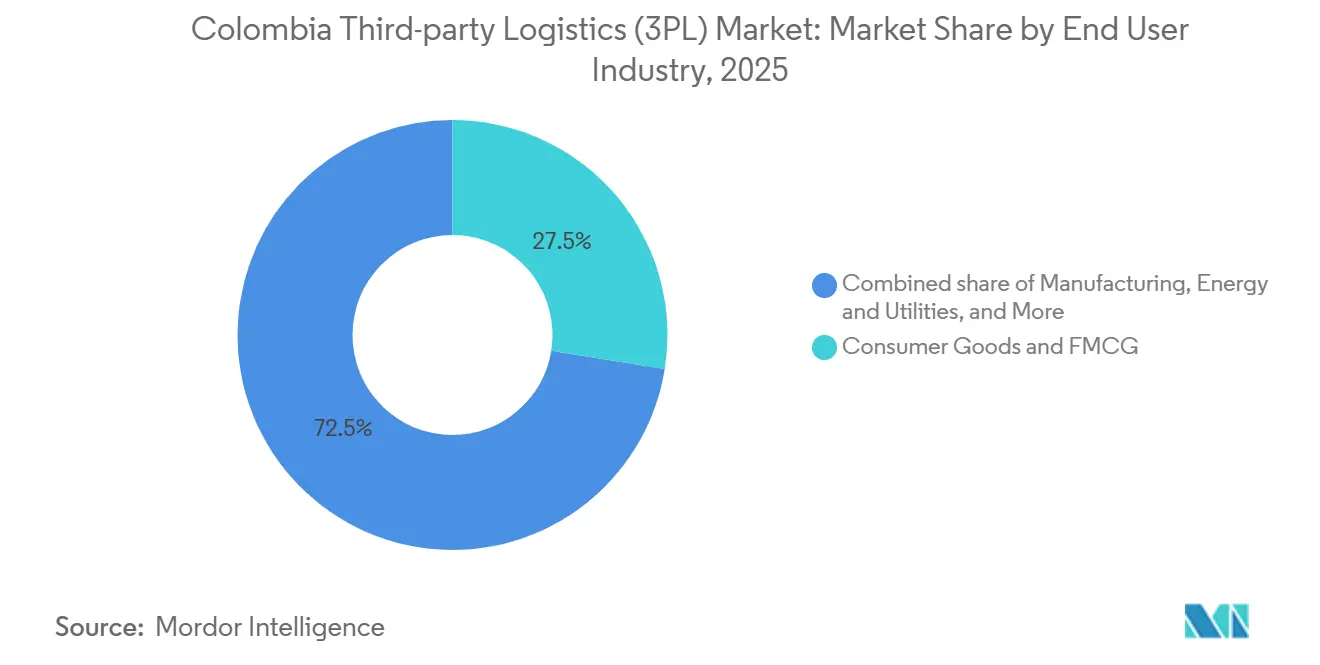

- By end-user industry, consumer goods and FMCG held 27.53% of the Colombia Third Party Logistics (3PL) market share in 2025. The Colombia Third Party Logistics (3PL) market for Retail and E-commerce is set to grow at a 7.12% CAGR between 2026-2031.

- By geography, the Andean region held 58.02% in 2025, while Colombia third-party logistics market size for the Pacific Corridor is projected to record the fastest 6.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Third-party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of domestic e-commerce | +1.3% | Andean Region (Bogotá, Medellín, Cali) | Short term (≤2 years) |

| Nearshoring of the US and LATAM supply chains into Colombia | +1.6% | National, with a concentration in Free Trade Zones | Medium term (2-4 years) |

| Expansion of special Free-Trade Zones (FTZs) & multimodal parks | +0.8% | Andean, Pacific Corridor, Caribbean Coast | Medium term (2-4 years) |

| Investments in cold-chain capacity for floriculture & pharma exports | +0.6% | Andean (flower farms), Pacific Corridor (ports) | Short term (≤2 years) |

| Digitization, TMS/WMS SaaS adoption among SMEs | +0.5% | National, early gains in urban centers | Medium term (2-4 years) |

| Magdalena River & rail corridor upgrades, unlocking inland freight | +0.7% | Magdalena River basin, La Dorada-Chiriguaná corridor | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth Of Domestic E-Commerce

Online sales reached COP 12 trillion (USD 2.97 billion) in 2025, rising 23.9% year-on-year, and pushed 3PLs to cut urban delivery windows from 48 hours to same-day. Parcel growth of 30-35% in Cali and Barranquilla is widening the customer base beyond Bogotá. The surge is strongest in grocery and pharmacy categories, which require temperature control and real-time inventory visibility. Providers are setting up micro-fulfillment hubs inside populous districts, matching inventory to neighborhood demand profiles. Regional specialists who master local traffic restrictions and zoning rules are gaining contracts from national retailers.

Nearshoring Of Regional Supply Chains

Tariff relief under free-trade agreements and dual-ocean access are attracting textile, auto-parts, and medical-device producers that target the US and intra-LATAM markets. Lead-times have fallen by up to 50% versus Asia-based sourcing, justifying labor-cost premiums. 3PLs are responding with bonded warehouses and cross-dock sites inside zones such as Tocancipá, where duties are deferred until goods exit to the local market. Increased southbound traffic from Brazilian plants and northbound exports to Central America are raising demand for cross-border compliance expertise[1].A.P. Moller-Maersk, “Maersk Inaugurates New Container Logistics Centre in Bogotá,” maersk.com

Digitization Via TMS/WMS SaaS Adoption

More than 70% of Colombian logistics firms launched digital projects in 2024 to manage routing, invoicing, and customs data on cloud platforms. SaaS models eliminate high up-front license fees, allowing small carriers to access optimization algorithms once reserved for multinationals. Digital freight marketplaces have begun matching independent truckers to spot loads in real time, lowering empty-mile ratios. Sector associations and government grants now fund training for data analytics skills, addressing a labor shortage that could erode 23% of sector cash flow by 2030 if left unresolved[2].Food Logistics Staff, “The Urgent Need for Digital Transformation in LatAm Food Logistics,” foodlogistics.com

Magdalena River & Rail Corridor Upgrades

USD 800 million of public-private investment is modernizing the La Dorada-Chiriguaná rail line and dredging the Magdalena River to cut bulk-freight costs by 26% by 2030. Higher axle loads and faster train speeds will divert cement, grain, and coal away from congested mountain roads. 3PLs capable of integrating barge, rail, and truck services can now offer shippers mode-mix options that align with cost or speed priorities, widening their service portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic road-infrastructure bottlenecks & mountain terrain | -0.8% | National, acute in the Andean highlands | Medium term (2-4 years) |

| Cargo-theft & security costs on key corridors | -0.5% | Ruta del Sol, Norte de Santander, La Guajira | Short term (≤2 years) |

| Customs bureaucracy & port dwell times | -0.4% | Buenaventura, Cartagena ports | Short term (≤2 years) |

| Exchange-rate volatility affecting contract pricing | -0.3% | National, particularly import-dependent sectors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Customs Bureaucracy & Port Dwell Times

Despite Cartagena ranking among the world’s most efficient terminals, paperwork checks still prolong container release times. Time-sensitive cargo such as fresh mangoes and just-in-time auto parts suffers the most. Electronic declarations and risk-based inspections are rolling out, but cross-agency coordination issues persist. 3PLs with in-house brokerage arms are monetizing pre-clearance services, helping shippers cut detention fees and improve inventory turns.

Exchange-Rate Volatility Affecting Contract Pricing

Peso swings against the US dollar directly impact diesel costs, which account for up to 40% of haulage expenses. Fixed-price contracts denominated in pesos expose carriers to fuel spikes, while dollar contracts expose shippers to local inflation. Some 3PLs are adopting rolling fuel surcharges and currency-adjustment clauses, yet smaller firms lack hedging tools, prompting consolidation as they seek balance-sheet strength to withstand FX shocks[3].International Trade Administration, “Colombia - Infrastructure,” trade.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Warehousing and Distribution Gains Momentum

Domestic Transportation holds 47.14% of Colombia Third-party (3PL) Logistics market share in 2025, while Value-Added Warehousing & Distribution is expanding the fastest at a 6.09% CAGR through 2031. Warehousing is narrowing the performance gap with trucking as omnichannel retailers integrate store and online inventories, driving demand for kitting, labeling, and reverse-logistics services. Maersk’s new Tocancipá campus illustrates how integrated cold rooms and cross-docks create single-site logistics solutions that compress lead times and minimize double handling. Despite its scale advantage, Domestic Transportation faces tightening labor dynamics, with driver shortages expected to double by 2028, according to the International Road Transport Union.

Infrastructure bottlenecks and security-related costs are also encouraging modal diversification, supporting projected growth in multimodal contracts as river and rail corridors reopen. Asset-heavy haulers are investing in AI-powered dispatch tools to increase trip utilization, while warehouse operators deploy goods-to-person robots to meet same-day e-commerce cut-offs. Cross-dock hubs near Bogotá airport now trans-load perishables from trucks to wide-body freighters in under two hours, sustaining Colombia’s high-value florist exports. Meanwhile, ocean forwarding margins remain constrained by liner overcapacity, prompting forwarders to differentiate through bundled customs consulting and trade-finance services.

By End-User Industry: E-Commerce Upsets Legacy Hierarchies

Consumer Goods & FMCG held the largest share of Colombia 3PL market in 2025 at 27.53%, while Colombia Third-party (3PL) Logistics market size for Retail & E-Commerce is projected to grow the fastest at a 7.12% CAGR as smartphone adoption and digital payments penetrate secondary cities. E-commerce expansion is reshaping logistics models as large brands seek unified stock pools that fulfill both store replenishment and direct-to-consumer orders. This shift is compelling 3PLs to implement inventory platforms with real-time, order-level visibility. Life-sciences shipments are also gaining market share as pharmaceutical fill-finish plants ramp up production near Cali, supported by validated cold rooms built to meet international Good Distribution Practice requirements.

Automotive parts and textiles moving into Colombia’s free-trade zones sustain consistent manufacturing volumes but require cross-dock operations and vendor-managed inventory programs to control multi-tier stock levels. Pharmaceutical exports depend heavily on compliant logistics chains featuring validated lanes and temperature-mapping audits. DHL’s acquisition of CRYOPDP strengthens Colombia’s integration into global clinical-trial logistics, enhancing credibility among drug manufacturers. Meanwhile, technology hardware and energy components, although representing smaller volumes, offer premium returns for logistics operators capable of maintaining strict handling and compliance standards.

By Logistics Model: Hybrid Configurations Scale Up

Asset-light firms captured the largest share of Colombia Third-party (3PL) market in 2025 at 45.23%, while hybrid logistics models are expanding the fastest at a 5.73% CAGR. Asset-light players scale quickly through subcontracted fleets, but the pandemic exposed their fragility when spot-market capacity disappeared, prompting shippers to favor providers guaranteeing peak-season equipment. Hybrid operators combining owned fulfillment centers and dedicated last-mile trucks with outsourced line-haul are gaining traction in new bids. Many now invest in automated small-parcel sorters within urban depots while continuing to rely on partner carriers for long-haul dry-van transport.

The share of fully asset-heavy fleets continues to contract, except in hazardous goods and validated cold-chain logistics, where direct control mitigates compliance risk. Small owner-operators increasingly depend on digital freight boards for utilization, yet performance rating systems reveal quality inconsistencies, steering multinational shippers toward hybrid 3PLs that maintain standardized service levels. Investors also view these hybrid firms favorably, considering their balanced asset portfolios more resilient to fuel-cost volatility and capacity market swings.

Geography Analysis

The Andean highlands, home to Bogota, Medellin, and Cali, captured 58.02% of 2025 revenue thanks to population density and manufacturing clusters. Congestion in mountain corridors, however, pushes logistics costs above coastal benchmarks. The Colombia third-party logistics market size allocated to the Pacific Corridor is forecast to grow fastest at a 6.62% CAGR through 2031 as Buenaventura’s berth deepening and the USD 4 billion Tren de Cercanías rail system shorten door-to-port transit times[4].Redacción El País, “Los Pasos que se Están Dando para Avanzar en el Tren de Cercanías de Cali,” elpais.com.co

Caribbean ports at Cartagena and Santa Marta benefit from efficiency scores that attract transshipment traffic, offering shippers schedule reliability and lower demurrage risks. The National Dredging Plan will further improve channel depths, easing access for neo-Panamax vessels. Inland departments along the Magdalena River stand to gain as barge services restart, enabling grain and cement exporters to bypass mountain passes. Orinoquía and Amazonia remain underserved, yet oil, gas, and timber projects create niche volumes that reward operators willing to invest in rugged equipment and community engagement.

Nearshoring is relocating assembly plants to coastal free-trade zones to avoid mountain trucking, creating a two-tier network: export-oriented corridors aligned with ports and consumption-driven routes feeding interior cities. 3PLs must design separate asset footprints for each, balancing the speed demands of consumer parcels with the cost efficiency required for bulk commodities.

Competitive Landscape

Top Companies in Colombia Third Party Logistics (3PL) Market

The sector shows moderate concentration. Global integrators such as DHL, DSV, and Maersk manage end-to-end visibility platforms, while national champions like Servientrega excel at last-mile parcels. Niche players specialize in cold chain for flowers and biopharma, or in dangerous-goods handling. Digital capabilities, rather than fleet size, now drive contract awards; shippers expect real-time ETA and exception alerts across modes.

DHL leads express shipping, underpinned by its Bogotá Gateway. DSV’s 2025 acquisition of Schenker roughly doubled network scale and will enhance cross-border capacity into Colombia once integration is completed. CEVA Logistics added three RORO vessels on Far East-South America lanes in 2025, offering finished-vehicle exporters new sailings that call at Colombian ports. Emergent Cold Latin America’s 157 million ft³ regional footprint positions it as the leader in temperature-controlled storage, appealing to both floriculture and pharmaceutical shippers.

Domestic consolidation is underway as family-owned trucking firms seek capital to install telematics and comply with security mandates. Venture investors back digital brokers that connect owner-operators to e-commerce traffic, challenging traditional forwarders. Yet premium contract wins increasingly go to 3PLs able to certify GDP logistics or provide multimodal river-rail solutions, barriers that loosely organized marketplaces cannot yet clear.

Colombia Third-party Logistics (3PL) Industry Leaders

DHL Supply Chain

Kuehne + Nagel

Blu Logistics

Coordinadora Mercantil

Servientrega

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CEVA Logistics deployed three additional RORO vessels linking the Far East to Colombian ports, enhancing finished-vehicle export options.

- April 2025: DSV completed its purchase of Schenker, expanding global reach and technology investment capacity that benefits Colombian lanes.

- March 2025: DHL acquired CRYOPDP to strengthen clinical-trial and biopharma logistics offerings in Colombia.

- February 2025: The Ministry of Transport imposed an eight-hour minimum trip time, raising tariffs up to 51% on short routes and altering cost structures for domestic carriers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Colombia third-party logistics market as all revenue earned by specialized providers that, on contract, manage domestic or international freight movement, customs brokerage, and value-added warehousing or distribution for shippers. Activities captured include road, air, sea, and multimodal transport management alongside outsourced storage and order-fulfillment services.

Scope Exclusion: Postal parcel networks and any in-house logistics operations run by manufacturers or retailers are not counted.

Segmentation Overview

- By Service

- Domestic Transportation Management

- International Transportation Management

- Freight Forwarding & Customs Brokerage

- Value-Added Warehousing & Distribution

- Reverse & After-sales Logistics

- By Mode of Transport

- Road Freight

- Rail Freight

- Air Freight

- Sea Freight

- Multimodal / Intermodal

- By End-user Industry

- FMCG (incl. Beauty & Home Care)

- Retail & E-commerce (Hyper/Super/Convenience)

- Automotive & Spare Parts

- Technology (Consumer Electronics & Appliances)

- Fashion & Lifestyle (Apparel & Footwear)

- Cold-Chain (Fruits, Vegetables, Pharma, Meat, Seafood)

- Industrial & Chemicals

Detailed Research Methodology and Data Validation

Primary Research

Phone interviews and short surveys with freight forwarders, FMCG shippers, e-commerce sellers, fleet financiers, and regional warehouse developers helped us validate tariff assumptions, contract churn rates, and typical storage yields across Bogotá, Medellín, and the coastal corridors.

Desk Research

We extracted baseline indicators from open public sources such as the National Department of Statistics traffic surveys, DIAN customs dashboards, Ministry of Transport trucking bulletins, Civil Aviation freight ton-kilometer logs, Port of Cartagena throughput sheets, and releases from ANDI's logistics committee. Company filings, investor decks, and reputable press enriched operator benchmarks, while paid datasets like D&B Hoovers (financial splits) and Dow Jones Factiva (deal flow) sharpened the competitive map. These sources are illustrative; many additional references were screened to confirm consistency.

Market-Sizing & Forecasting

We began with a top-down reconstruction of Colombia's freight bill, applied a 54 percent outsourcing ratio, and then separated spend across domestic transport, international forwarding, and warehousing. Selective bottom-up checks sampled 3PL revenue disclosures, warehouse stock surveys, and channel checks tempered totals before finalization. Key model drivers include e-commerce parcel volumes, free-trade-zone export tonnage, diesel price index, warehouse vacancy, peso-USD exchange swings, and port dredging milestones. Multivariate regression coupled with ARIMA overlays produced forecasts, with expert panels adjusting scenario ranges wherever data gaps appeared.

Data Validation & Update Cycle

Mordor analysts run variance screens against historical series, peer benchmarks, and fresh trade data, then escalate anomalies for review before sign-off. The model updates annually, with interim refreshes if fuel tax shifts, port strikes, or currency shocks materially alter demand patterns.

Why Mordor's Colombia Third party Logistics Baseline Is Dependable

Published estimates often diverge because analysts apply dissimilar service scopes, outsourcing ratios, currency bases, or refresh cadences. Some studies fold courier volumes into 3PL totals, others track only asset-heavy warehousing, and several lock forecasts to a single-year exchange rate without later reconciliation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.60 B (2025) | Mordor Intelligence | - |

| USD 5.00 B (2023) | Regional Consultancy A | Includes freight forwarding and CEP, relies solely on macro spend shares |

| USD 0.48 B (2024) | Trade Journal B | Tracks contract warehousing only, omits transport management |

These contrasts show that our disciplined variable selection, rolling-currency normalization, and balanced top-down and bottom-up checks deliver a transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

How large is the Colombia third-party logistics market in 2026?

The Colombia third-party logistics market size reached USD 4.83 billion in 2026 and is forecast to climb to USD 6.17 billion by 2031.

Which service type is growing fastest?

Value-Added Warehousing & Distribution is projected to expand at a 6.09% CAGR as omnichannel retail and nearshoring drive demand for sophisticated inventory services.

What region is expected to gain share by 2031?

The Pacific Corridor is set to post a 6.62% CAGR, outpacing the Andean highlands due to port deepening and new rail links that shorten export transit times.

How are 3PLs addressing road congestion?

Providers are integrating barge and rail legs, adopting AI route optimization and shifting inventory closer to consumption points to limit exposure to mountain bottlenecks.

Which industries are driving cold-chain investment?

Floriculture exports and the rapidly growing pharmaceutical manufacturing sector require validated temperature-controlled logistics, spurring expansion of cold-chain capacity across airports and seaports.

Page last updated on: