Cloud Security In Retail Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

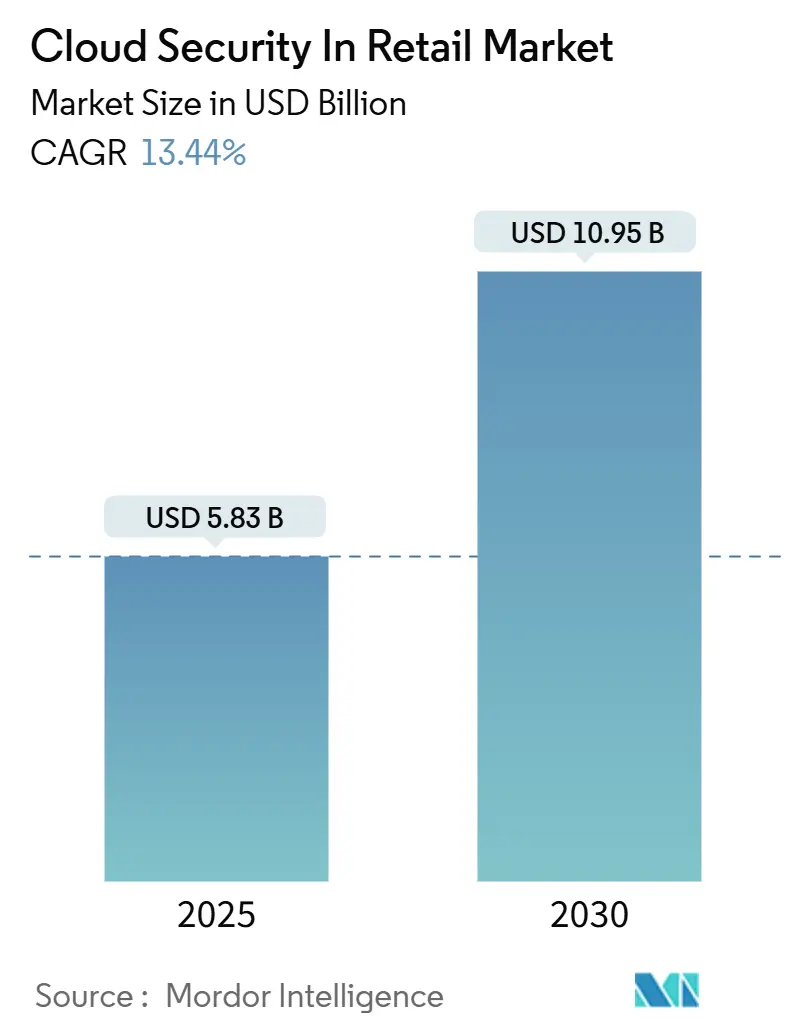

| Market Size (2025) | USD 5.83 Billion |

| Market Size (2030) | USD 10.95 Billion |

| Growth Rate (2025 - 2030) | 13.44% CAGR |

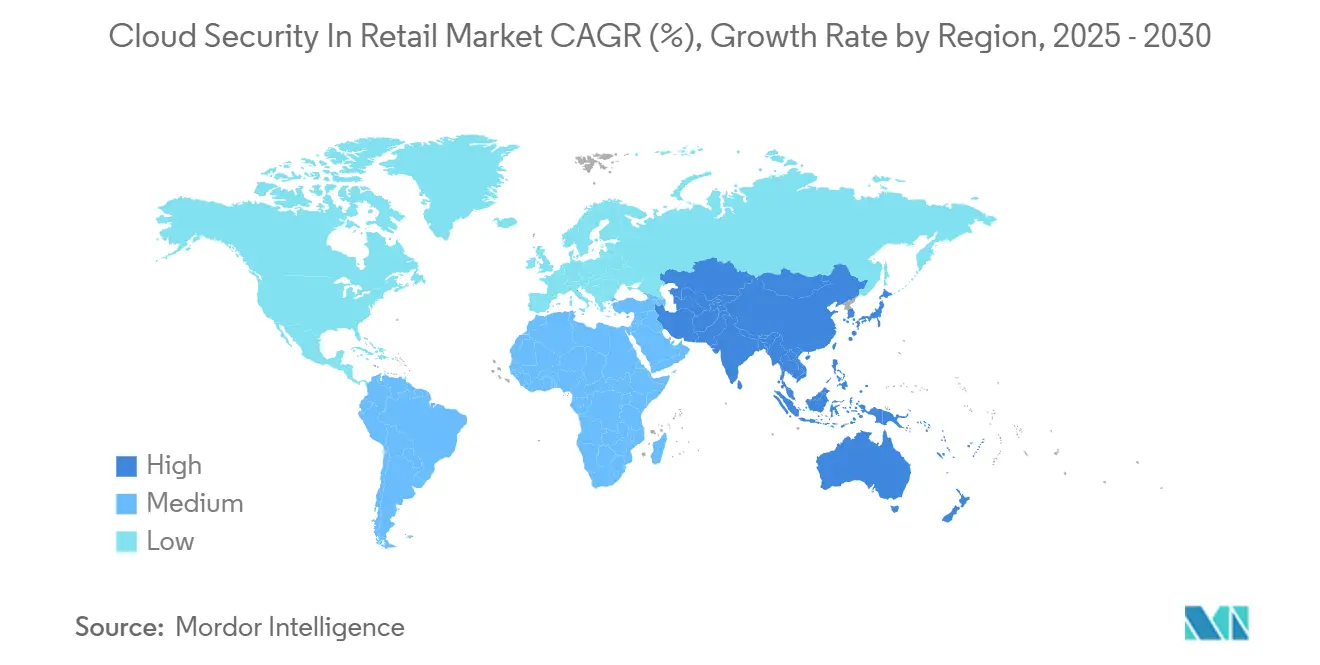

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

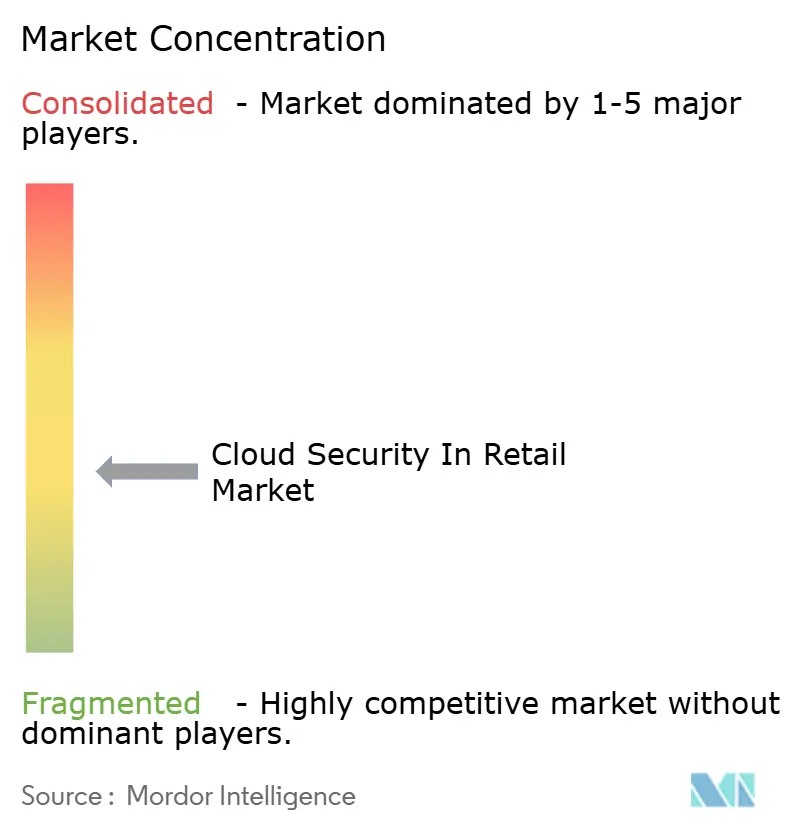

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Security In Retail Market Analysis by Mordor Intelligence

The cloud security in retail market size stood at USD 5.83 billion in 2025 and is projected to reach USD 10.95 billion in 2030, translating into a 13.44% CAGR across the forecast horizon. Retailers are accelerating investments as omnichannel models enlarge the attack surface, zero-trust frameworks mature, and compliance deadlines tighten. Heightened ransomware activity during peak shopping periods has shifted budget toward immutable backups, micro-segmentation, and threat-hunting services. The mandatory adoption of PCI DSS 4.0 and India’s Digital Personal Data Protection Act is expanding the demand for multi-factor authentication and data-residency controls. Hybrid cloud designs that keep latency-sensitive inventory systems on-premises while moving customer-facing workloads to hyperscaler regions are gaining traction. Vendors that embed security into retail-specific APIs hold a differentiation edge.

Key Report Takeaways

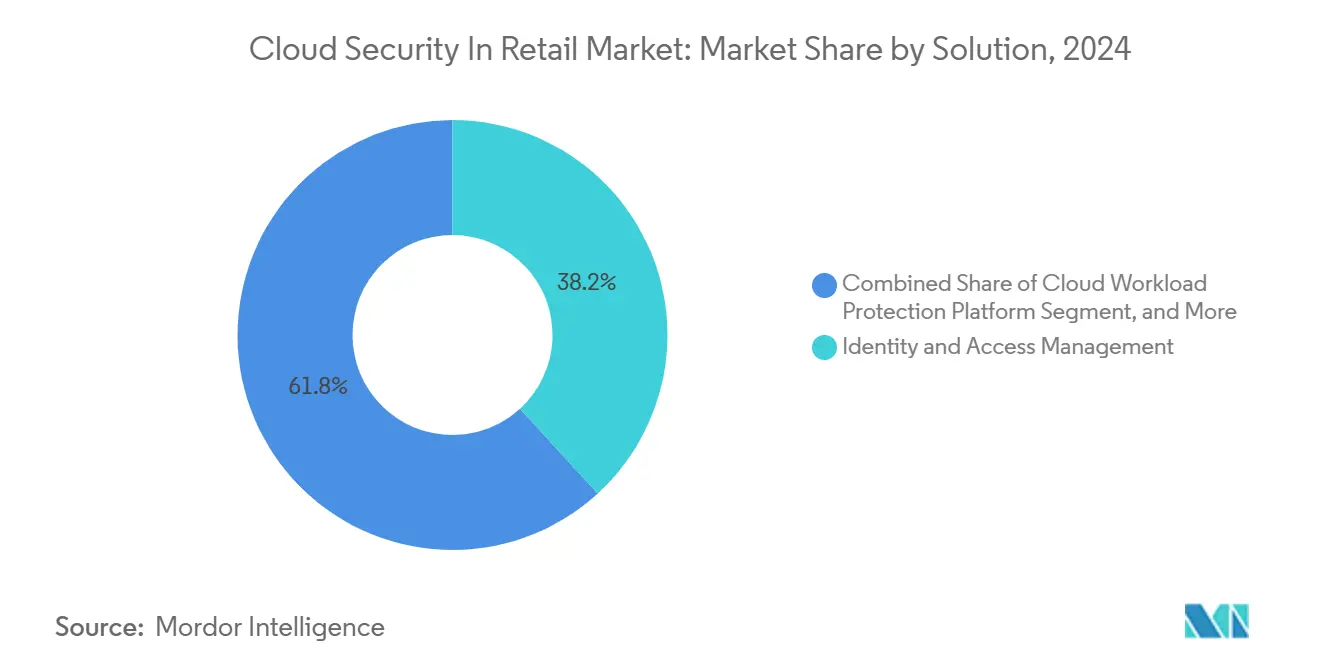

- By solution, identity and access management led with 38.20% of the cloud security in retail market share in 2024, while cloud workload protection platforms are forecast to grow at a 15.80% CAGR through 2030.

- By security type, network security accounted for 31.50% of 2024 spending, while application security is poised to advance at a 16.70% CAGR through 2030.

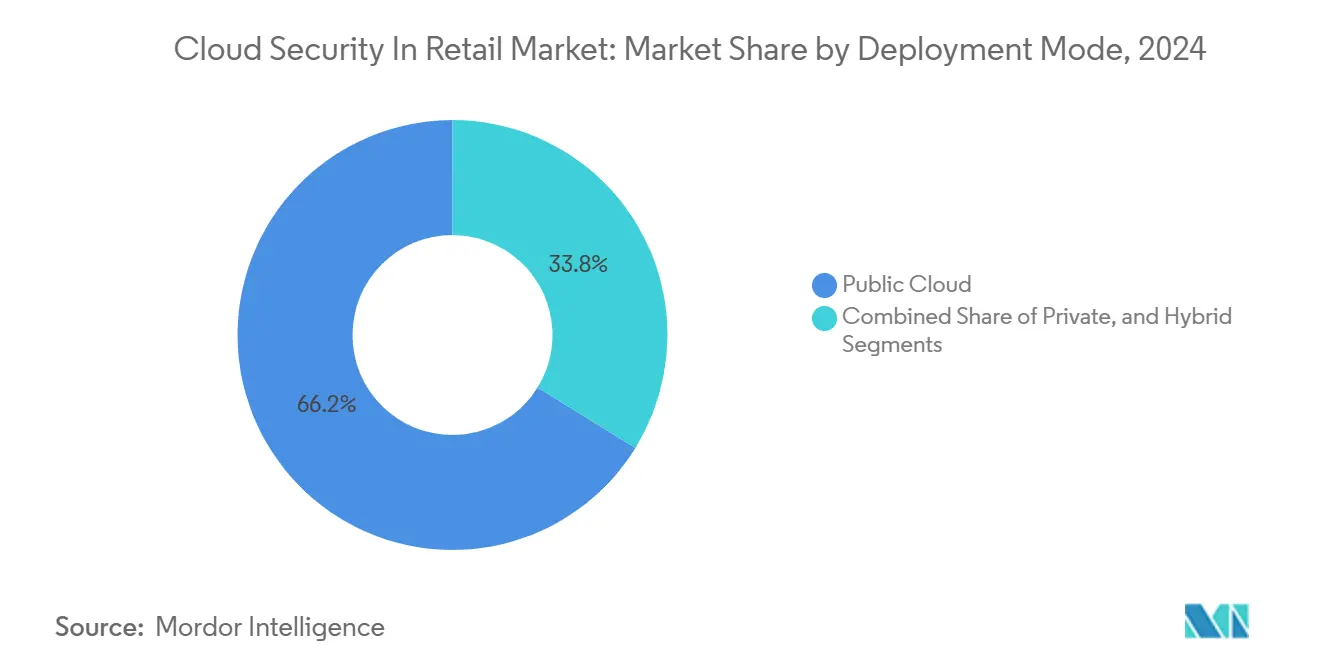

- By deployment mode, public cloud deployments accounted for a 66.20% share in 2024, whereas hybrid cloud is projected to expand at a 17.10% CAGR across the forecast period.

- By service model, software-as-a-service tools represented a 58.40% share in 2024, and platform-as-a-service security is projected to climb at an 18.20% CAGR toward 2030.

- By geography, North America held a 38.40% share in 2024, while the Asia Pacific is expected to grow at a 15.20% CAGR during the forecast period.

Global Cloud Security In Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing threat of sophisticated retail-focused ransomware | +3.2% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Surge in compliance-driven security spending (PCI DSS 4.0, DPDP Act) | +2.8% | North America, Europe, Asia Pacific (India core) | Medium term (2-4 years) |

| Expansion of omnichannel and click-and-collect workflows | +2.1% | Global, led by North America and the Asia Pacific urban centers | Medium term (2-4 years) |

| Rise of AI-enabled fraud detection platforms requiring secure cloud APIs | +1.9% | North America, Europe, Asia Pacific (China, Japan) | Long term (≥ 4 years) |

| Edge-enabled smart store roll-outs are increasing the attack surface | +1.6% | North America, Europe, Asia Pacific (pilot deployments) | Long term (≥ 4 years) |

| Tokenization of loyalty and gift-card ecosystems | +1.2% | Global, early traction in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Threat of Sophisticated Retail-Focused Ransomware

Ransomware syndicates refined their targeting during 2024, timing attacks around major shopping events when downtime costs are multiplied. Incidents such as the Clop group’s file-transfer exploits and the Blue Yonder outage exposed gaps in backup hygiene and incident-response coordination. Sophos reported that 69% of retailers experienced at least one ransomware attack in 2024, with median recovery expenses exceeding USD 2 million when business interruption and fines are counted.[1]Sophos Labs, “The State of Ransomware 2024,” sophos.com Retailers now prioritize immutable storage, micro-segmentation that isolates point-of-sale systems, and SOC platforms that correlate endpoint and network telemetry for faster detection of lateral movement.

Surge in Compliance-Driven Security Spending (PCI DSS 4.0, DPDP Act)

PCI DSS 4.0 introduced 53 new or evolved requirements effective March 2025, including phishing-resistant authenticators and expanded MFA coverage. Retailers with legacy terminals are upgrading gateways and deploying FIDO2 tokens to avoid non-compliance penalties.[2]Payment Card Industry Security Standards Council, “PCI DSS v4.0 Summary of Changes,” pcisecuritystandards.org India’s DPDP Act imposes fines up to INR 2.5 billion (USD 30 million) for mishandling sensitive personal data, compelling multinational chains to deploy consent-management tools and data-localization controls within Indian cloud regions.

Expansion of Omnichannel and Click-and-Collect Workflows

Headless commerce architectures blend mobile apps, web storefronts, and in-store kiosks, exposing APIs that coordinate inventory, payments, and logistics. API traffic surges magnify the risk of injection attacks when rate limits and schema validation are weak. The National Retail Federation found 58% of surveyed retailers rank API security among their top three investment areas for 2024.[3]National Retail Federation, “2024 Retail Cybersecurity Survey,” nrf.com To contain sprawl, CISOs adopt cloud-access security brokers for shadow IT governance and deploy zero-trust gateways that verify each request across distributed touchpoints.

Rise of AI-Enabled Fraud Detection Platforms Requiring Secure Cloud APIs

Real-time fraud models parse behavioral signals across cloud data lakes, necessitating encrypted channels and auditable calls to inference endpoints. Adversarial machine-learning attacks that nudge models toward false negatives have led retailers to implement secure boot and signed-model distribution. Federal Trade Commission guidance released in January 2025 mandates transparency for AI decisioning, prompting adoption of lineage tracking and model-card generation.[4]Federal Trade Commission, “Guidance on AI Transparency and Accountability,” ftc.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy POS integration complexity | -1.8% | Global, acute in North America and Europe, with aging infrastructure | Short term (≤ 2 years) |

| Perceived higher TCO of best-practice cloud security architectures | -1.4% | Global, pronounced in small and mid-sized retailers | Medium term (2-4 years) |

| Vendor lock-in concerns for retailers moving to a single cloud | -0.9% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Shortage of retail-savvy cybersecurity talent | -1.1% | Global, severe in the Asia Pacific, and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy POS Integration Complexity

Terminals deployed before 2015 often run proprietary OS builds that cannot authenticate to cloud identity providers or emit structured logs. Firmware support has lapsed for many models, forcing retailers to choose between costly refreshes or accepting the risk of blind spots. On-premises gateways that cleanse POS telemetry before forwarding it to cloud SIEM tools introduce latency and create new failure points, hindering the broader adoption of cloud security in the retail market.

Perceived Higher TCO of Best-Practice Cloud Security Architectures

Subscription pricing, log-egress fees, and premium support tiers elevate operating costs for smaller merchants. A full zero-trust stack can consume 8%-12% of a mature retailer’s IT budget, and few standardized calculators factor in breach-avoidance savings. CFO skepticism delays funding cycles even as threat intelligence validates exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Identity Governance Anchors Spending as Workload Protection Accelerates

Identity and access management accounted for 38.20% of 2024 spending, the highest share within the cloud security market in the retail sector. Cloud workload protection platforms are on track for a 15.80% CAGR through 2030, reflecting rapid container adoption. Data-loss prevention, intrusion detection, encryption, SIEM, and cloud-access security broker tools round out spending as retailers harden every control layer.

IAM strength stems from PCI DSS 4.0 multi-factor authentication mandates and the shift to passwordless FIDO2 authentication, which reduces phishing risk. The growth of cloud workload protection reflects retailers’ migration from monolithic systems to Kubernetes clusters, where runtime scanning and lateral movement detection are paramount. Vendors such as Palo Alto Networks added agent-less scanning for serverless functions in 2025, closing blind spots in short-lived compute tasks. Unified platforms that correlate IAM events with workload telemetry support faster response and are shaping future roadmap convergence.

By Security Type: Application Defenses Outpace Network Controls

Network controls held 31.50% of total spending in 2024. Application security, however, is forecast to expand at a 16.70% CAGR, surpassing network growth as API traffic outpaces traditional web flows in retail. Database, endpoint, and web or email defenses remain essential but grow more slowly.

Headless commerce and microservices drive retailers to prioritize the protection of API gateways, parameter validation, and schema enforcement. OWASP updated its API Security Top 10 in 2024, with broken object-level authorization as the most common flaw. Cloudflare’s retail WAF ruleset, released January 2025, includes signatures that distinguish legitimate comparison crawlers from credential-stuffing bots, reducing false positives for flash sales.

By Deployment Mode: Hybrid Configurations Gain as Latency Demands Persist

Public cloud maintained a 66.20% share in 2024, reflecting hyperscalers’ elasticity during traffic spikes. Hybrid designs will expand at a 17.10% CAGR as grocers and department stores keep latency-sensitive inventory databases on-premises while pushing customer-facing workloads to multiregion clusters.

AWS Outposts reference architectures launched in January 2025 enable stores to process transactions locally during connectivity loss and later sync data to regional zones. Retailers deploy Zscaler Private Access to secure on-premises inventory systems without extending the attack surface to the public internet. Such hybrid blueprints illustrate why the cloud security in retail market continues to diversify across public and local nodes.

By Service Model: SaaS Dominates While PaaS Security Surges

SaaS tools accounted for 58.40% of spending in 2024, underscoring retailers’ preference for turnkey solutions. Platform-as-a-service defenses will post an 18.20% CAGR as merchants build custom fraud models on managed AI platforms. Infrastructure-layer security focuses on misconfiguration detection for virtual networks and storage buckets.

Google Cloud added data-lineage tracking and model-card generation to Vertex AI in February 2025, enabling retailers to document the provenance of fraud models for FTC audits. CrowdStrike’s runtime container protection, introduced the same month, extends endpoint telemetry across PaaS workloads. These enhancements highlight how the cloud security market size for PaaS-focused controls in the retail sector is scaling alongside machine-learning deployments.

Geography Analysis

North America accounted for 38.40% of the 2024 global spending, driven by state-level breach notification statutes and the early adoption of tokenization. The expanded enforcement of California’s Consumer Privacy Act and Virginia’s Consumer Data Protection Act in 2024 led to increased penalties, prompting investments in discovery and encryption platforms. The FTC AI transparency rules, published in January 2025, require model validation logs, which are expected to accelerate the adoption of governance platforms.

The Asia Pacific is projected to record a 15.20% CAGR through 2030, driven by China’s data-localization rules, Japan’s stricter amendments to personal information, and India’s DPDP Act consent mandates. The rapid growth of super-apps and cross-border marketplaces intensifies the need for API governance. Japan’s Ministry of Economy, Trade, and Industry issued cloud-security guidelines in March 2025 that echo global standards, reducing regulatory ambiguity for retailers.

Europe remains shaped by GDPR, spurring pseudonymization and DLP spending, while the Digital Operational Resilience Act obliges payment processors and, by extension, retail payment partners to audit cloud vendors. Middle Eastern sovereign-cloud mandates and African mobile-money ecosystems are forging regional demand for cloud-access security brokers that enforce per-country data limits. Together, these regional nuances sustain multi-speed growth across the cloud security in the retail market.

Competitive Landscape

The cloud security in retail market is moderately fragmented. Hyperscalers bundle entry-level security features into infrastructure contracts, then upsell managed detection and response, steering customers toward single-provider ecosystems. Specialized vendors carve out niches through pre-integrations with Shopify, SAP Commerce Cloud, and Oracle Retail, which reduce deployment friction. Smaller entrants focus on edge analytics in smart stores, processing telemetry from computer-vision cameras and RFID readers at the perimeter.

Cisco’s adaptive micro-segmentation patent, filed in 2024, outlines algorithms that dynamically tighten firewall rules around anomalous payment flows. CrowdStrike’s fiscal 2024 10-K cited a 35% rise in retail annual recurring revenue, highlighting momentum for unified endpoint and workload protection. Vendor roadmaps emphasize automated compliance dashboards that map controls to PCI DSS and regional privacy laws, reducing reporting burdens for overstretched retail security teams.

Strategic moves underscore consolidation: Microsoft integrated Entra ID risk signals with Azure Sentinel in March 2025 to blend identity context into SIEM analytics, and Palo Alto Networks’ Prisma Cloud expanded serverless scanning in February 2025. These developments position full-stack platforms to capture spend as retailers rationalize their use of point solutions.

Cloud Security In Retail Industry Leaders

Trend Micro Incorporated

Imperva Inc.

Broadcom Inc.

International Business Machines Corporation

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Japan’s METI published cloud-security guidelines for critical infrastructure, recommending MFA and stringent key management.

- March 2025: Zscaler reported a 40% increase in retail deployments of Private Access during 2024, evidencing hybrid-security momentum.

- March 2025: Microsoft made Entra ID retail risk signals generally available, enabling adaptive authentication tied to anomalous transaction volumes.

- February 2025: Google Cloud introduced Vertex AI data-lineage tracking and model-card generation, easing FTC transparency compliance.

Global Cloud Security In Retail Market Report Scope

The Cloud Security in Retail Market Report is Segmented by Solution (Identity and Access Management, Data Loss Prevention, Intrusion Detection and Prevention, Security Information and Event Management, Encryption, Cloud Workload Protection Platform, Cloud Access Security Broker), Security Type (Application Security, Database Security, Endpoint Security, Network Security, Web and Email Security), Deployment Mode (Public, Private, Hybrid), Service Model (SaaS, PaaS, IaaS), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Identity and Access Management |

| Data Loss Prevention |

| Intrusion Detection and Prevention |

| Security Information and Event Management |

| Encryption |

| Cloud Workload Protection Platform |

| Cloud Access Security Broker |

| Application Security |

| Database Security |

| Endpoint Security |

| Network Security |

| Web and Email Security |

| Public |

| Private |

| Hybrid |

| Software as a Service (SaaS) |

| Platform as a Service (PaaS) |

| Infrastructure as a Service (IaaS) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Solution | Identity and Access Management | |

| Data Loss Prevention | ||

| Intrusion Detection and Prevention | ||

| Security Information and Event Management | ||

| Encryption | ||

| Cloud Workload Protection Platform | ||

| Cloud Access Security Broker | ||

| By Security | Application Security | |

| Database Security | ||

| Endpoint Security | ||

| Network Security | ||

| Web and Email Security | ||

| By Deployment Mode | Public | |

| Private | ||

| Hybrid | ||

| By Service Model | Software as a Service (SaaS) | |

| Platform as a Service (PaaS) | ||

| Infrastructure as a Service (IaaS) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What was the value of the cloud security in retail market in 2025?

The market was valued at USD 5.83 billion in 2025.

Which solution area holds the largest cloud security in retail market share?

Identity and access management led with a 38.20% share in 2024.

Which region is growing fastest?

Asia Pacific is forecast to register a 15.20% CAGR through 2030.

Why are hybrid cloud architectures gaining popularity?

Retailers require local processing for latency-sensitive inventory queries while scaling customer-facing workloads in the public cloud, driving hybrid cloud adoption.

How does PCI DSS 4.0 influence spending?

The standard’s expanded MFA and encryption mandates compel retailers to upgrade legacy systems and invest in key management.

Which driver contributes most to market growth?

Rising ransomware threats, estimated to contribute 3.2% to the market's CAGR, are the most significant growth factor.

Page last updated on: