Cloud-Based English Language Learning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

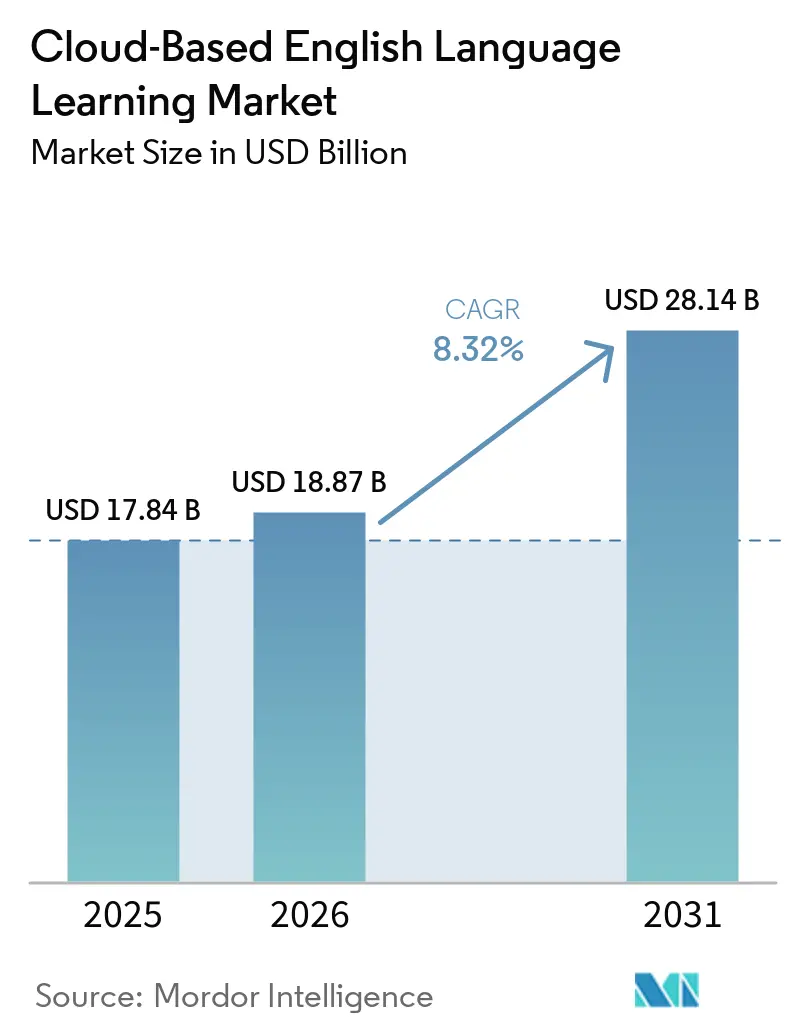

| Market Size (2026) | USD 18.87 Billion |

| Market Size (2031) | USD 28.14 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-Based English Language Learning Market Analysis by Mordor Intelligence

The Cloud-Based English Language Learning Market size is expected to grow from USD 17.84 billion in 2025 to USD 18.87 billion in 2026 and is forecast to reach USD 28.14 billion by 2031 at 8.32% CAGR over 2026-2031.

Enterprise demand is shifting from emergency remote tools to structured, outcome-verified programs as globalization and visa-linked proficiency policies normalize digital English learning. Generative AI is widening access to speaking practice, which is the most persistent skills gap, and is reshaping willingness-to-pay as premium features migrate into mainstream tiers for scale. Adoption patterns signal a durable channel mix in which self-paced apps drive frequency while live and blended formats carry credibility for promotions, mobility, and compliance. Competitive strategies emphasize platform distribution, content-assessment integration, and privacy-ready architectures that can withstand evolving data and AI regulation. The Cloud-based English language learning market is also seeing deeper ties with productivity ecosystems and HR tech, which support continuous use and measurable progress within daily workflows.

Key Report Takeaways

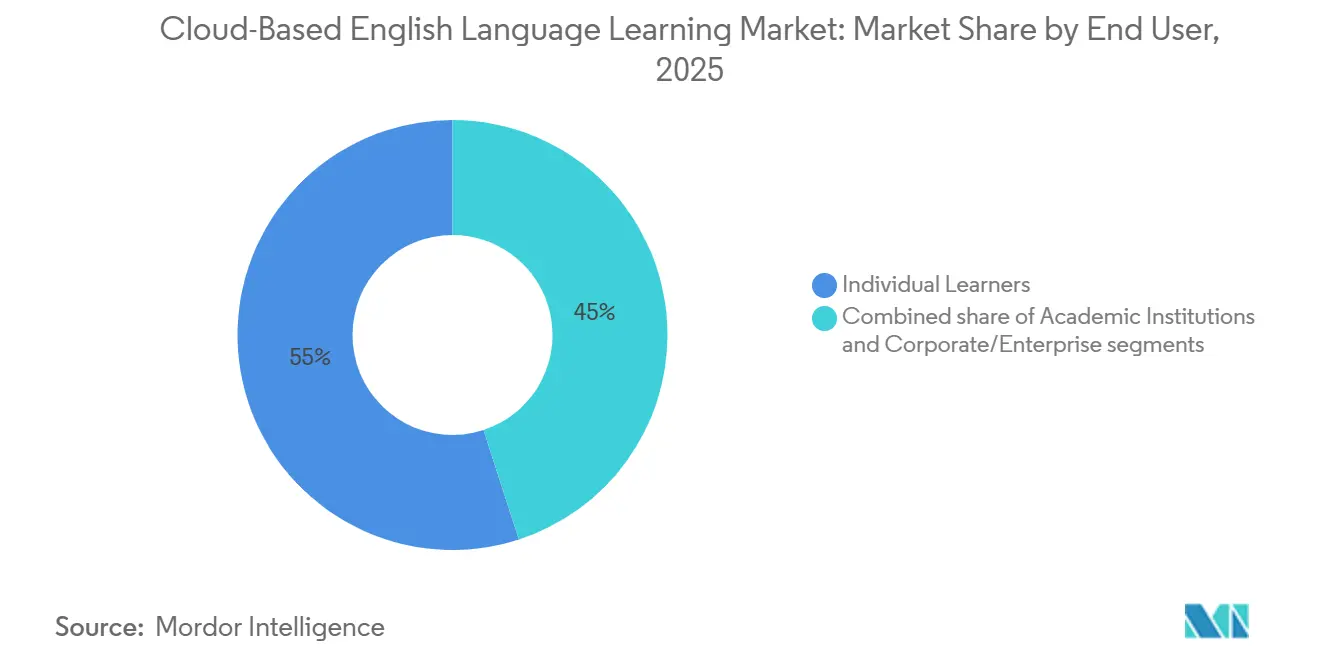

- By end user, individual learners led with 55% of the Cloud-based English language learning market share in 2025, while corporate and enterprise is projected to expand at a 17% CAGR through 2031.

- By learning mode, self-paced app-based courses accounted for 60% of the Cloud-based English language learning market share in 2025, and live online classes are forecast to grow at a 17.8% CAGR through 2031.

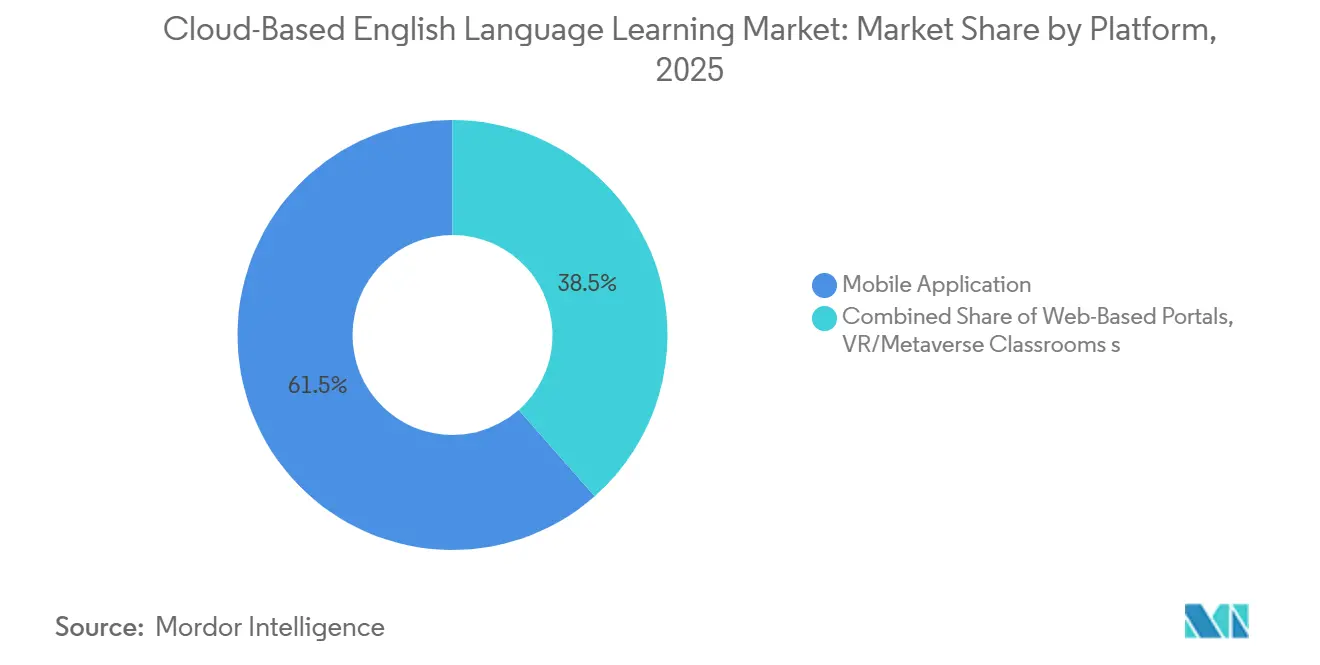

- By platform, mobile applications captured 61.5% of the Cloud-based English language learning market share in 2025, while virtual-reality and metaverse classrooms, are projected to rise at a 27% CAGR.

- By age group, the K–12 segment held 34.5% of the Cloud-based English language learning market share in 2025, while adults aged 25+ are the fastest-growing cohort at an 18.3% CAGR through 2031.

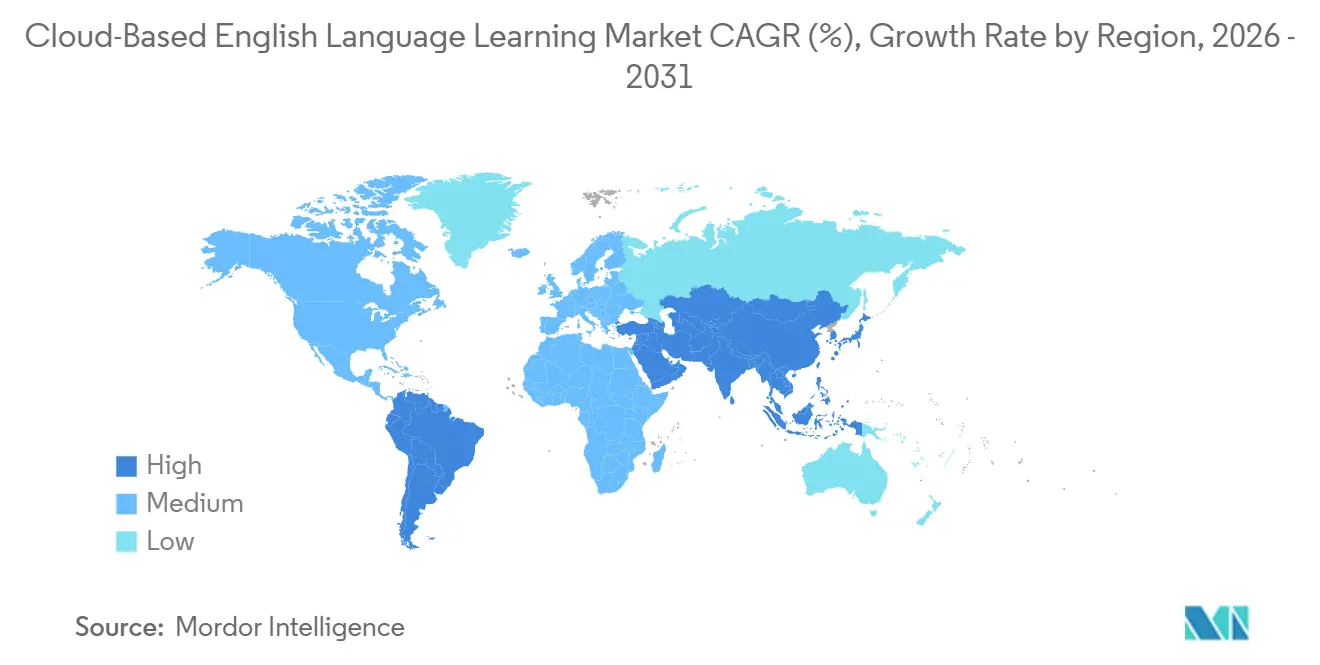

- By geography, Asia-Pacific maintained 43% of the Cloud-based English language learning market share in 2025 and is projected to lead growth at a 22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud-Based English Language Learning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Visa-linked PTE/IELTS prep digitization | +1.8% | Global, concentrated in Australia, UK, Canada, US migration corridors | Medium term (2-4 years) |

| Corporate English upskilling mandates | +2.1% | Global, strongest in APAC (China, India), MENA, Latin America | Long term (≥ 4 years) |

| GenAI tutors enable scalable speaking practice | +1.9% | Global, early adopters in North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Telco/device bundling boosts subscriptions | +0.9% | Emerging markets: India, Southeast Asia, Sub-Saharan Africa | Medium term (2-4 years) |

| Mobile-first uptake in emerging markets | +1.3% | APAC (India, Indonesia, Vietnam), Africa (Nigeria, Kenya, Egypt), Latin America (Brazil, Mexico) | Long term (≥ 4 years) |

| CEFR micro-credentials embedded in hiring | +0.9% | Global, with concentration in EU, North America corporate HR | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Visa-Linked PTE/IELTS Prep Digitization: Test-Taker Volumes Stabilize Despite Migration Policy Flux

Pearson reported that PTE Academic volumes declined 5% in 2025 as policy tightening in certain destinations affected visa-linked demand, while sales held steady through price adjustments and renewals, indicating more resilient monetization even with lower throughput. PTE acceptance covers 97% of Canadian universities and 95% of colleges, all Australian, New Zealand, and Irish universities, and 99% of United Kingdom universities, which anchors digital-first preparation for academic and migration pathways in major corridors. Pearson extended the product set with PTE Core and launched PTE Express targeted at United States-bound learners, aligning test design with destination-specific policy criteria to deepen addressability[1]Pearson plc, “PTE Express and Product Portfolio Update,” Pearson plc, pearsonplc.com. The Duolingo English Test processed results within 72 hours for hundreds of thousands of candidates at accessible price points and expanded its global acceptance base, increasing competitive pressure on incumbents to match its turnaround speed and transparency while preserving integrity[2]Duolingo English Test, “Test Overview and Acceptance,” Duolingo, englishtest.duolingo.com. ETS modernized TOEFL iBT for January 2026 with adaptive sections, faster score reporting, and embedded AI-driven preparation, underscoring how test providers now integrate instruction to capture value upstream of exam day[3]ETS, “Enhanced TOEFL iBT Launch and Features,” ETS, ets.org. As test delivery and proctoring shift to the cloud, providers are reworking assurance controls to manage identity verification and security at scale, supporting the Cloud-based English language learning market with more flexible, at-home journeys that still meet institutional and immigration standards.

Corporate English Upskilling Mandates: High-Maturity Programs Yield 2× Net Profit, 10× AI Deployment

EF’s 2026 Maturity Report found that organizations with highly mature language programs achieved twice the net profit and deployed AI at ten times the rate of less mature peers, converting language learning from a discretionary line item to a structural driver of operational effectiveness. The business case centers on workforce readiness and market access, where certified English proficiency correlates with smoother cross-border execution, a higher rate of successful new-market entry, and more reliable assignment mobility. EF’s proficiency mapping identified persistent gaps in speaking and listening, even in high-scoring countries, which steers budgets toward targeted speaking practice and role-based curriculum aligned with work tasks rather than broad, generic coverage. The projected incremental spend in Business English through the late 2020s reflects executives’ preference for platforms that align content with the CEFR, issue verifiable credentials, and provide cohort analytics that link training inputs to performance outcomes. Pearson’s Communications Coach integrates with Microsoft 365, so employees receive feedback within familiar tools, improving adoption by reducing the friction between intent and action at work. This enterprise orientation benefits the Cloud-based English language learning market by reinforcing demand for compliance-ready assessments, HRIS integration, and clear ROI reporting that withstands procurement and audit scrutiny.

GenAI Tutors Enable Scalable Speaking Practice: Duolingo’s “Video Call” Migration Prioritizes Growth Over Yield

Duolingo’s 2026 decision to move its flagship AI conversation feature from its top-tier to a mid-tier subscription increases access by an order of magnitude, signaling a deliberate trade-off of near-term average revenue for user growth and frequency, and positioning AI tutors as mass-market retention tools. The shift supports the most acute global skill gap, as speaking remains the hardest competency to build in self-paced formats, and it lowers intimidation barriers by allowing real-time practice without human judgment. Pearson deployed AI-powered tutoring for institutional clients to scale coaching without hiring in proportion to demand. This model blends content, analytics, and assessment credibility to create sticky enterprise relationships. Speak’s funding and user milestones underscored that conversational AI can unlock high-frequency practice at consumer-friendly price points, expanding the top of the funnel for learners who postpone live tutoring until later in their journey. Novakid’s launch of an AI-native conversational app for teens shows how life-stage design can extend a provider’s reach beyond its legacy segment while preserving CEFR alignment and adaptive pathways. At the same time, third-party studies on classroom-style tutoring reported faster CEFR-level progress, pushing the Cloud-based English language learning market toward hybrid models that pair AI practice with structured human coaching at critical milestones.

CEFR Micro-Credentials Embedded in Hiring: B2 Baselines and Verifiable Certificates Shape HR Workflows

Pearson’s research across key countries found that a strong majority of respondents consider English important for work today and expect its relevance to grow, which aligns hiring practices with CEFR-based thresholds for roles across functions. Employers are tightening verification requirements by requiring QR-verifiable certificates and secure identity checks, favoring platforms that issue traceable credentials and produce transparent analytical reports for human review. CEFRhub highlights the emergence of privacy-by-design assessment that aligns with GDPR and North American data regimes, reducing the risk that automated scoring will be used as the sole basis for consequential decisions. Pearson’s Global Scale of English maps job roles to forward-looking ability descriptors, enabling HR teams to specify level targets for hiring and promotions with greater precision. As micro-credentials fold into promotion and mobility frameworks, employee and employer incentives align, which supports recurring investment and sustained engagement in the Cloud-based English language learning market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low self-paced course completion | -1.4% | Global, most acute in self-study segments without community features | Short term (≤ 2 years) |

| Data privacy and consent regimes | -0.8% | EU, California, emerging in APAC and LATAM | Long term (≥ 4 years) |

| App-store commissions reduce ARPU | -0.9% | Global, concentrated in iOS and Google Play ecosystems | Medium term (2-4 years) |

| AI hallucinations undermine trust | -0.7% | Global, early-stage concern in generative-AI tutoring and assessment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Self-Paced Course Completion: Median MOOC Retention Compresses Lifetime Value, Cohort Models Counter With 70%+ Rates

Completion rates in self-paced formats remain low, forcing platforms to spend more on acquisition to maintain active learner bases and delaying monetization. Providers that combine scheduled cohorts, community discussion, and live touchpoints report higher completion rates, making blended models more attractive for enterprise training where verification matters. Duolingo and other high-scale apps improve daily engagement through micro-lessons and gamification loops, but many learners still need structured coaching to translate practice into rapid CEFR advancement. Marketplace tutoring models document faster level gains within short windows, which supports business cases for higher-priced, outcome-tied offers when paired with AI tools that prepare and reinforce between sessions. Live class ecosystems, including large volumes of virtual sessions each month, offer accountability that self-paced content alone struggles to deliver, especially for speaking and writing. The net effect pushes the Cloud-based English language learning market toward hybrid architectures that raise completion and outcome credibility while preserving the scale benefits of digital delivery.

Data Privacy and Consent Regimes: Transparency Obligations Raise Compliance Costs and Favor Mature Operators

European and North American data laws require explicit consent, subject-access controls, and human oversight when automated processing could significantly affect a user, thereby increasing the fixed compliance costs for AI-heavy language platforms. Providers are adopting privacy-by-design approaches that restrict the repurposing of user data and prioritize explainability in automated judgments to satisfy internal legal review and external audits. Multi-cloud and regional data storage help institutions comply with localization rules, which is one reason vendors formalize partnerships with hyperscalers to segment workloads while scaling capacity. As rules evolve in the EU and other jurisdictions, enterprise buyers lean toward vendors with track records in regulated markets and visible governance artifacts, creating a barrier for smaller entrants. These requirements shape product roadmaps and sales cycles and influence how the Cloud-based English language learning market approaches assessment, identity, and analytics in enterprise deals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Corporate Mandates Propel Enterprise Segment to 17% CAGR, Overtaking Retail Growth as ROI Visibility Sharpens

Individual learners held a 55% share in 2025, while the enterprise segment is projected to grow at a 17% CAGR through 2031, reflecting budget shifts toward accountable, verifiable outcomes in the Cloud-based English language learning market. EF’s 2026 findings that high-maturity language programs correlate with stronger profit and faster AI deployment support executive sponsorship of scaled training tied to CEFR levels and job performance. Employers secure measurable benefits from targeted English upskilling, including more reliable international assignment mobility and fewer execution risks in cross-border roles. Pearson’s Communications Coach shows how embedding learning prompts into everyday tools like Microsoft 365 raises usage and simplifies compliance proof points for HR and audit teams. Preply’s enterprise offering aligns dashboards and CEFR tracking with L&D reporting needs, linking training hours to performance management and procurement standards. The Cloud-based English language learning market size associated with enterprise contracts benefits from multi-seat agreements that aggregate demand. At the same time, retail monetization still depends on freemium conversion and app-store dynamics.

Academic institutions remain a sizable institutional buyer cohort and continue to expand as English proficiency becomes a career prerequisite for university placement and international study tracks. Consumer platforms continue to serve the largest volume of learners but face lower average revenue per user than business accounts, which deepens strategic emphasis on cohort-based experiences and add-on services. Enterprise buyers gravitate to solutions that blend AI practice with instructor interventions and auditable assessment, a combination that strengthens the Cloud-based English language learning industry’s positioning in procurement-heavy categories. Over time, end-user mix will depend on how well vendors align outcome reporting with promotion criteria and mobility frameworks, which could broaden the enterprise slice of the Cloud-based English language learning market as CFOs see predictable returns.

By Learning Mode: Self-Paced Apps Dominate With 60% Share, Live Classes Surge at 17.8% CAGR as Employers Demand Verifiable Skill Transfer

Self-paced app-based courses held 60% share in 2025, confirming that flexible, micro-learning formats anchor daily practice frequency across the Cloud-based English language learning market. At the same time, live online classes are projected to grow at 17.8% CAGR as companies favor synchronous, accessible instruction to verify real-world speaking and writing performance. Duolingo’s large active user base illustrates the power of bite-sized content loops that create daily habits. At the same time, enterprise cohorts still require certified progress and instructor sign-off at defined milestones. Babbel Live conducts a large volume of virtual classes each month, meeting demand for curated groups and guided sessions that keep learners on track toward promotion or migration goals. MOOCs remain a smaller slice due to lower completion rates, which reduces their attractiveness for employers requiring proof of transfer from knowledge to performance. Blended formats combine AI-driven preparation and recap with scheduled human interventions and community reinforcement, lifting completion compared with pure self-study and strengthening program credibility in audits.

For institutions and corporations, blended delivery supports data collection and reporting aligned with CEFR or in-house role frameworks, making it easier to justify spend and renewals. The Cloud-based English language learning market size linked to live and blended modes reflects premium pricing that attaches to verified outcomes and compliance needs. At the same time, self-paced apps prioritize scale economics and engagement. Providers are introducing workflow features such as automated lesson summaries and reinforcement exercises to bridge gaps between live sessions, thereby improving skill retention and perceived value. As these models converge, the Cloud-based English language learning industry continues to differentiate on verified impact, teacher quality, and integration depth with institutional systems.

By Platform: Mobile Apps Capture 61.5% Share, VR/Metaverse Classrooms Accelerate From a 2.1% Base at 27% CAGR

Mobile applications captured 61.5% of platform share in 2025, supported by smartphone ubiquity and the convenience of short practice bursts that fit busy schedules across the Cloud-based English language learning market. Web portals remain essential for enterprise customers that require SSO, LMS compatibility, and cohort analytics, enabling administrators to orchestrate programs and verify outcomes. Virtual reality classrooms account for 2.1% of deployments and are projected to grow at 27% CAGR as immersive speaking practice gains traction and early pilots document measurable improvements. GoStudent VR’s data showing broad speaking-skill gains has attracted interest from secondary students and educators seeking confidence-building environments for conversation and role-play. EON Reality expanded its XR-based language solutions to align with CEFR and ACTFL, reinforcing an institutional pathway for immersive practice.

Mobile-first design continues to focus on 3–5-minute modules, streak mechanics, and intelligent notifications to sustain frequency, supporting steady user growth and broad top-of-funnel exposure. The Cloud-based English language learning market size tied to immersive formats will depend on hardware accessibility and content libraries, which are improving as vendors seed free or low-cost experiences and align to familiar curricula. For now, platform strategies converge on hybrid experiences that let learners switch between mobile, web, and VR while preserving progress and assessment integrity. This design fits both consumer convenience and enterprise governance needs.

By Age Group: K–12 Holds 34.5% Share, Adults 25+ Grow Fastest at 18.3% CAGR as Upskilling and Mobility Expand Addressable Demand

K–12 accounted for a 34.5% share in 2025, supported by parental priorities for university access and early skill formation that align with CEFR progression. Novakid’s 2026 product for teens extends personalized conversation into a bridge category for learners aging out of children’s apps but not yet ready for adult curricula. Higher-education learners continue to prepare for global study and early-career roles, with a heavy emphasis on test readiness and academic English, which stabilizes demand for preparatory content tied to PTE, TOEFL, and other recognized credentials. Adults 25+ are projected to expand at 18.3% CAGR through 2031 as companies formalize language expectations in hiring, promotion, and mobility programs, and as more pathways tie economic opportunity to certified proficiency. Enterprise packages for employee cohorts in service, operations, and client-facing roles lead to higher willingness to pay for verified progress.

In adult cohorts, AI tutors remove friction for speaking practice between live sessions and support flexible schedules, a pattern that encourages sustained engagement across months rather than weeks. Corporate solutions from major vendors add role-based scenarios and analytics that integrate with performance reviews, reinforcing the link between proficiency and career trajectory in the Cloud-based English language learning market. Over time, age-segmented product fit and verifiable outcomes are likely to be the differentiators that matter most for retention and lifetime value, particularly in adult segments where the stakes include migration, promotions, and cross-border assignments.

Geography Analysis

Asia-Pacific held 43% share in 2025 and is projected to lead growth at a 22% CAGR through 2031, reflecting mobile-first study patterns, government workforce mandates, and large student cohorts entering higher education and global mobility pipelines. This profile positions APAC as the primary engine of the cloud-based English-language learning market, with public-private partnerships and institutional contracts expanding program reach. Pearson reported strong institutional momentum across Latin America and the Middle East in recent results, and noted short-term PTE volume softness tied to policy changes in specific corridors, underscoring the sensitivity of visa-linked categories to geopolitical shifts. Providers that balance academic credentials, at-home test delivery, and enterprise offerings are best placed to capture APAC’s multi-channel growth while managing policy risk in migration-exposed subsegments.

North America’s adoption is reinforced by corporate training budgets and strong subscription elasticity, with enterprise solutions that integrate into productivity suites gaining preference for their low-friction user experience. Duolingo’s 2025 performance milestones and guidance highlighted a scale-first posture that supports ongoing engagement and broadening of the product portfolio, which often sets pricing references for consumer tiers. Europe benefits from CEFR standardization and regulatory clarity, which plays to the strengths of providers with mature compliance and privacy infrastructure and may influence procurement criteria across borders. University and visa pathways in the United Kingdom and other European destinations continue to underpin steady demand for PTE and TOEFL preparation. At the same time, institutions seek cloud-native administration and faster score reporting to manage cohorts.

The cloud-based English-language learning market in emerging regions of the Middle East and Africa, as well as Latin America, is set to grow from a smaller base as mobile-first adoption and youth demographics expand the learner pool. Vendors partnering with ministries, universities, and large employers can accelerate access and address localized compliance, identity, and assessment needs. Across regions, platform availability in mobile, web, and VR modes allows providers to tailor delivery to infrastructure realities. At the same time, assessment credibility and data governance principles act as common denominators in large-scale deployments.

Competitive Landscape

The cloud-based English-language learning market remains moderately fragmented, with leading players spanning AI-native applications, human-tutor marketplaces, and assessment-centric platforms. Duolingo surpassed USD 1 billion in 2025 bookings and prioritized scale by expanding access to AI conversation features. This move can compress near-term average revenue per user but widen the funnel of engaged learners. Pearson’s English Language Learning division reported steady sales and margin improvement and launched new products and cloud partnerships that link instruction to recognized credentials and enterprise workflows. Babbel combined large subscription bases with live classes and business solutions, strengthening defensibility with EU-ready compliance practices that resonate with enterprise buyers.

Strategic initiatives cluster in three areas. First, capital formation for AI acceleration and global expansion, as seen in Preply’s Series D and Speak’s Series C, signals investor conviction in scalable conversational AI and hybrid tutoring. Second, product launches that embed generative AI to automate practice, feedback, and teacher assistance, with vendors reporting high activation rates for tools that save time and personalize learning. Third, regulatory positioning through privacy-by-design credentials and verifiable certificates to meet HR and institutional due diligence, where CEFRhub and similar providers promote auditable outputs rather than opaque scores. These vectors reinforce a landscape where distribution, workflow integration, and verifiable outcomes now differentiate more than content volume alone.

Immersive learning and cohort-based architectures offer white space as completion and confidence rise with social accountability and experiential simulations. GoStudent’s VR programs and EON Reality’s XR language platforms offer institutional routes for speaking-practice immersion aligned with CEFR and school standards. Over time, providers that integrate AI practice, human coaching, assessment credibility, and secure data governance into seamless user journeys are positioned to gain share in the Cloud-based English language learning market, especially where buyers demand measurable transfer to workplace performance.

Cloud-Based English Language Learning Industry Leaders

Duolingo Inc.

Babbel GmbH

EF Education First

Pearson ELT

Open English

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Duolingo expanded access to AI learning by moving “Video Call with Lily” from Max to Super, scaling AI conversational learning, and shifting its strategy toward user growth over monetization.

- January 2026: ETS and Study.com launched an official TOEFL iBT prep program aligned with the redesigned adaptive TOEFL exam, featuring AI tutoring, CEFR scoring, and new test formats

- January 2026: Preply raised USD 150 million Series D led by WestCap to scale the AI-powered tutoring platform, expand engineering teams, and enhance AI learning co-pilot capabilities.

- November 2025: EON Reality launched an XR–based K–12 language learning platform with AI conversational practice aligned to CEFR/ACTFL standards for immersive education delivery.

Global Cloud-Based English Language Learning Market Report Scope

Cloud-based English language learning market refers to the segment of the education industry where English learning services are delivered through online, cloud-hosted platforms (apps or websites), allowing users to learn speaking, writing, listening, and reading skills anytime and anywhere via the internet.

The Cloud-Based English Language Learning Market Report is segmented by End User (Individual Learners, Academic Institutions, Corporate / Enterprise), Learning Mode (Self-paced App-based Courses, Live Online Classes, Massive Open Online Courses (MOOCs), Blended/Hybrid Programs), Platform (Mobile Apps, Web-based Portals, Virtual-Reality/Metaverse Classrooms), Age Group (K-12, Higher-Education (18-24), Adults (25+)), and Geography (North America (Canada, United States, Mexico), South America (Brazil, Peru, Chile, Argentina, Rest of South America), Europe (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe), Asia-Pacific (India, China, Japan, Australia, South Korea, South-East Asia, Rest of Asia-Pacific), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, Nigeria, Rest of Middle East and Africa)). The Market Forecasts are Provided in Terms of Value (USD), Based on Availability.

| Individual Learners |

| Academic Institutions |

| Corporate / Enterprise |

| Self-paced App-based Courses |

| Live Online Classes |

| Massive Open Online Courses (MOOCs) |

| Blended/Hybrid Programs |

| Mobile Apps |

| Web-based Portals |

| Virtual-Reality/Metaverse Classrooms |

| K-12 |

| Higher-Education (18-24) |

| Adults (25+) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By End User | Individual Learners | |

| Academic Institutions | ||

| Corporate / Enterprise | ||

| By Learning Mode | Self-paced App-based Courses | |

| Live Online Classes | ||

| Massive Open Online Courses (MOOCs) | ||

| Blended/Hybrid Programs | ||

| By Platform | Mobile Apps | |

| Web-based Portals | ||

| Virtual-Reality/Metaverse Classrooms | ||

| By Age Group | K-12 | |

| Higher-Education (18-24) | ||

| Adults (25+) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and 2031 outlook for the Cloud-based English language learning market?

The Cloud-based English language learning market is USD 18.87 billion in 2026 and is projected to reach USD 28.14 billion by 2031 at an 8.32% CAGR.

Which end user contributes most and which grows fastest?

Individual learners hold 55% in 2025, while corporate and enterprise is the fastest-growing at 17% CAGR through 2031, reflecting outcome and compliance priorities for employers.

How are generative AI features changing product strategies?

Providers are moving AI conversation tools into broader tiers to drive engagement at scale, then pairing AI practice with structured coaching for verified progress and higher completion.

Which platforms are gaining traction across regions?

Mobile apps lead with 61.5% share for daily practice, web portals support enterprise governance and analytics, and VR classrooms are the fastest-growing from a small base at 27% CAGR.

What regions lead demand and why?

Asia-Pacific holds 43% share and leads growth at 22% CAGR as mobile-first learning, government mandates, and higher-education pipelines expand usage.

What compliance themes matter most for enterprise buyers?

Buyers prioritize CEFR-aligned assessment credibility, data governance aligned with GDPR-like regimes, and verifiable certificates, which influence vendor selection and renewals.

Page last updated on: