Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | |

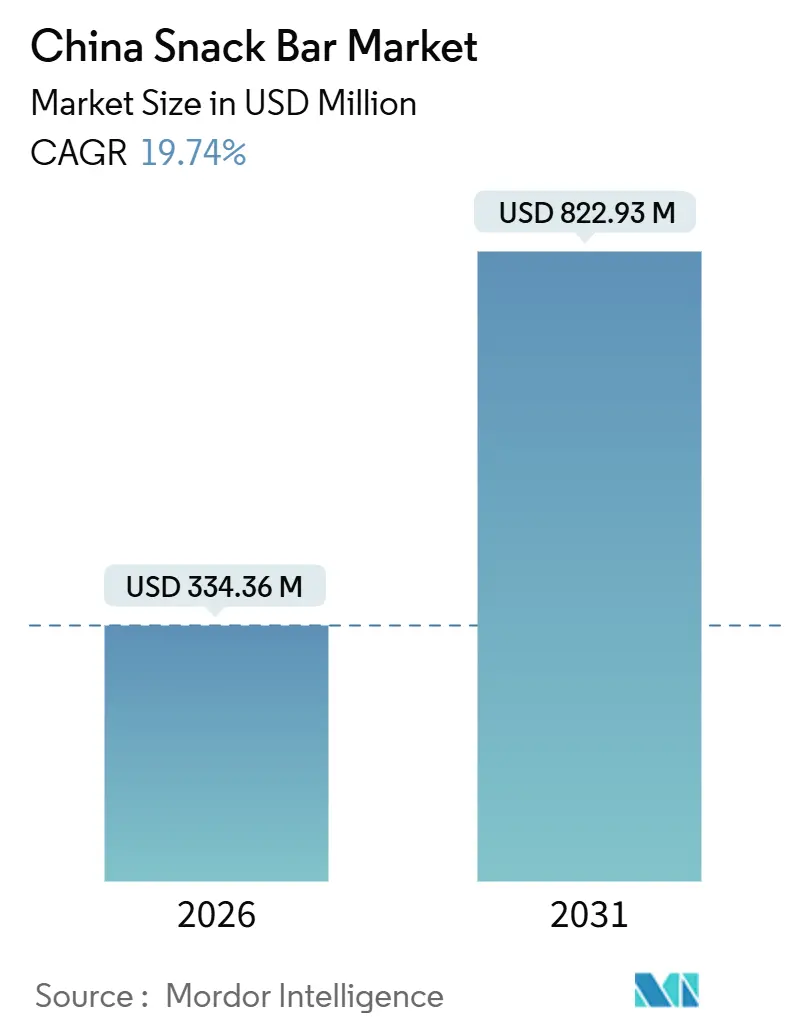

| Market Size (2026) | USD 334.36 Million |

| Market Size (2031) | USD 822.93 Million |

| Growth Rate (2026 - 2031) | 19.74% CAGR |

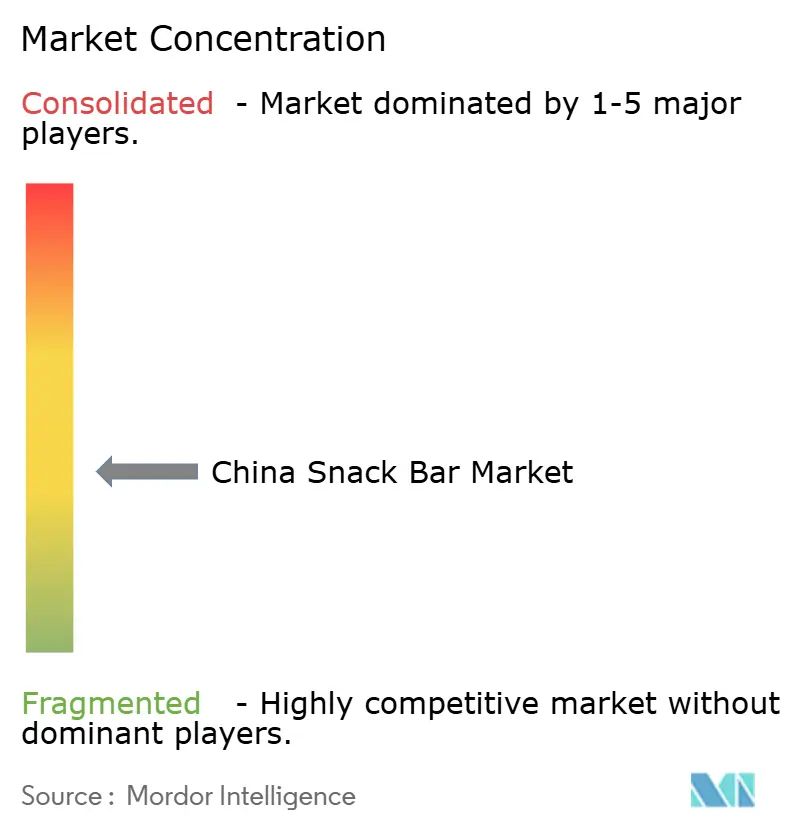

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Snack Bar Market Analysis by Mordor Intelligence

The China snack bar market size reached USD 334.36 million in 2026 and is projected to climb to USD 822.93 million by 2031, advancing at a 19.74% CAGR. Escalating fitness participation, government emphasis on balanced protein intake, and rapid penetration of short-video commerce are expanding category reach beyond traditional post-workout occasions. Domestic dairy majors and global confectionery brands are investing in functional-ingredient innovation that lifts average protein content while improving taste, a historic adoption barrier. Automated bar-forming lines, livestreaming sales models, and provincial sports-nutrition subsidies are lowering entry costs and raising consumer trial, especially in tier-2 cities. Heightened regulatory scrutiny and ingredient price swings continue to pressure gross margins, yet brands that comply with GB 28050-2025 labeling and diversify sourcing remain positioned to outgrow the category.

Key Report Takeaways

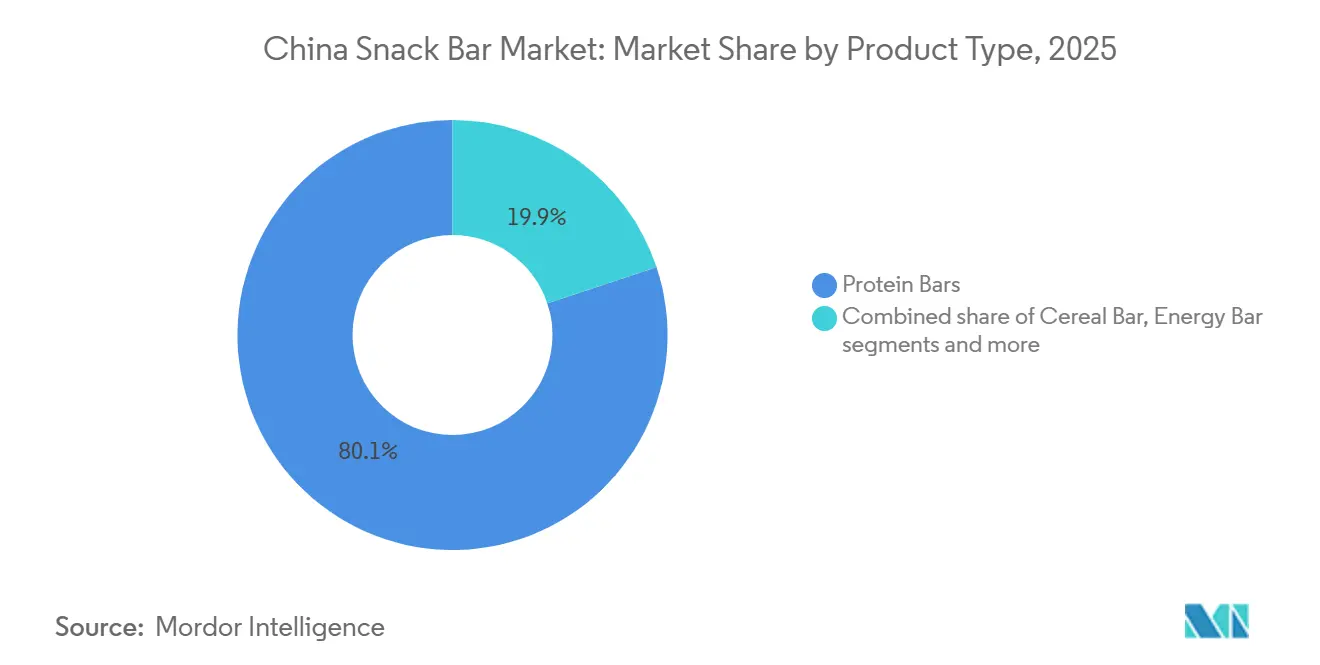

- By product type, protein bars led with 80.12% of the China snack bar market share in 2025, while energy bars posted the fastest 21.45% CAGR through 2031.

- By ingredient base, dairy or mixed-protein variants captured 64.07% of the China snack bar market in 2025 and are expanding at a 20.94% CAGR through 2031.

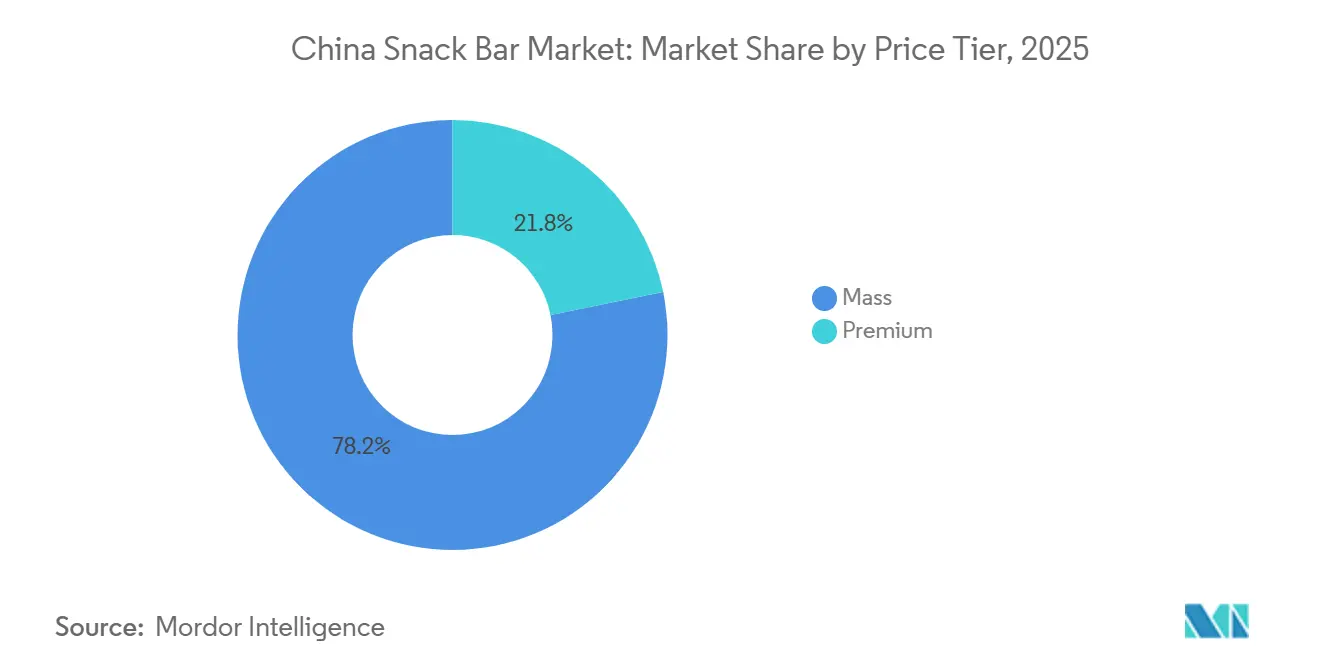

- By price tier, mass offerings held 78.15% of the China snack bar market in 2025, whereas premium bars are forecast to grow at a 21.74% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets commanded 41.47% China snack bar market share in 2025 while online retail is projected to rise at a 23.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fitness-centric lifestyles among Gen Z and millennials | +4.2% | Tier-1 and tier-2 cities | Medium term (2-4 years) |

| Premiumization through functional ingredients | +3.8% | Nationwide, led by tier-1 | Medium term (2-4 years) |

| Automated bar-forming capacity upgrades | +2.5% | Manufacturing hubs east and west | Long term (≥4 years) |

| Provincial sports-nutrition subsidies | +1.8% | Zhejiang, Jiangsu, Guangdong, Sichuan | Medium term (2-4 years) |

| Busy urban on-the-go lifestyles | +3.5% | Major metros | Short term (≤2 years) |

| Government nutrition improvement focus | +2.9% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fitness-centric lifestyles among Gen Z and Millennials

China’s fitness market has expanded rapidly, adding nearly 50 million participants and extending the sports nutrition consumer base beyond traditional bodybuilders to include casual gym-goers and home workout enthusiasts. Paid gym memberships reached 69.75 million in 2023, yet penetration remains low at 2.8% compared with 19.9% in the United States, highlighting significant growth potential as the government aims to develop a CNY 7 trillion (USD 965 billion) sports industry by 2030, according to the State Council of China[1]Source: State Council of China, “China Food and Nutrition Development Plan (2025-2030),” GOV.CN. Protein bars have become a key product for this demographic, offering convenient, portion-controlled nutrition; a 2024 Glanbia Nutritionals study found that 52% consume them before or after exercise, while 33% use them during leisure activities such as gaming or streaming, and 31% as desk snacks. This multi-occasion usage differentiates China from Western markets, where protein bars remain largely tied to athletic performance, and is particularly pronounced among Gen Z and Millennial consumers, who are driving wellness spending and show a willingness to pay a premium for clean-label, low-sugar, or plant-based formulations.

Premiumisation Through Functional-Ingredient Innovation

Innovation in functional ingredients is transforming product design, with a growing emphasis on high-protein claims supported by whey protein isolates, plant-based combinations, and dairy protein concentrates, according to the USDA Foreign Agricultural Service. Yili Group, which recorded FY2024 revenue of CNY 115.8 billion (USD 16.0 billion), has invested in human milk oligosaccharides (HMOs) and collaborated with Alibaba to introduce AI-powered personalization for protein bar formulas aimed at digestive health and immune support. In January 2024, Mars China introduced a low-glycemic-index version of Snickers featuring functional fibers and a 40% reduction in sugar while preserving flavor, addressing a key challenge as taste remains the primary obstacle to protein bar adoption in Glanbia’s research[2]Source: Glanbia Nutritionals, “Protein Bar Consumer Study 2024,” GLANBIANUTRITIONALSUSA.COM. Mengniu Dairy has pushed forward with mycoprotein and dairy protein innovations, and PepsiCo’s CNY 500 million (USD 68.6 million) oat processing plant in Jiangsu, with an annual capacity of 160,000 tons, is expected to support the production of oat-based protein bars by late 2025, according to PepsiCo. Meanwhile, premium product segments are projected to expand at a 21.74% CAGR through 2031, surpassing mass-market growth as consumers increasingly opt for enhanced functional benefits such as longer-lasting energy, improved muscle recovery, and greater satiety.

Domestic Capacity Upgrades in Automated Bar-Forming Lines

Chinese equipment producers are increasingly supplying automated bar-forming systems with capacities between 150 and 1,200 kilograms per hour, incorporating AI-based quality inspection and IoT-powered predictive maintenance that cut downtime by 15–20% and lower unit costs by 18–22%, according to the China Food Machinery Manufacturers. PepsiCo’s CNY 1.3 billion (USD 179 million) plant in Shaanxi completed in 2024, along with its 25,000-ton potato chip expansion in Shandong, illustrates the scale of investment flowing into snack automation, while Mondelez International’s CNY 53 million (USD 7.34 million) smart warehousing hub in Beijing launched in February 2024 forms part of more than CNY 1 billion invested in China over the past decade, reflecting strong confidence in local supply-chain efficiency. Three Squirrels also committed CNY 200 million (USD 27.5 million) in 2024 toward manufacturing upgrades to support its move into 33 sub-brands across snack bars, instant foods, and drinks. Together, these developments are reducing barriers for mid-range brands and allowing contract manufacturers to run private-label programs for platforms such as Tmall and JD.com, which are testing in-house protein bars priced 20–30% below branded products, while also aligning with provincial initiatives in regions like Jiangsu, Guangdong, and Sichuan that use tax breaks and land incentives to build emerging snack-food clusters.

Provincial Sports-Nutrition Subsidies and Events Pipeline

Provincial authorities in Zhejiang, Jiangsu, Guangdong, and Sichuan have introduced sports nutrition subsidy schemes linked to large-scale participation events such as marathons, cycling competitions, and fitness exhibitions, providing vouchers redeemable for protein bars and recovery snacks at partner retailers, according to the State Council of China. Under Zhejiang’s 2024 Healthy Living Initiative, CNY 120 million (USD 16.5 million) was set aside to support sports nutrition purchases for registered gym users and event attendees, while Jiangsu’s Sports Bureau worked with convenience store chains to roll out 20% discounts on functional snacks during provincial sporting events, as reported by the Zhejiang Provincial Government. These initiatives are boosting brand exposure and encouraging product trials, especially in tier-2 and tier-3 cities, where awareness of protein bars is still below 15%, compared with 35–40% in tier-1 cities, according to USDA Foreign Agricultural Service data[3]Source: USDA Foreign Agricultural Service, “China Food Processing Ingredients Report 2024,” FAS.USDA.GOV. Meanwhile, the number of organized endurance events continues to rise, with more than 1,800 marathons and similar races held across China in 2024, up from 1,200 in 2022. Organizers now require nutrition stations stocked with protein bars and energy gels, according to the China Athletics Association. This growing event infrastructure is helping generate repeat demand and educate consumers about functional benefits, speeding adoption in lower-tier markets where offline retail accounts for over 70% of sales but e-commerce distribution is still limited.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory constraints on health and functional claims | -1.5% | National, with stricter enforcement in tier-1 cities | Medium term (2-4 years) |

| Ingredient cost volatility (nuts, whey, plant proteins) | -2.1% | National, with higher impact on import-dependent manufacturers | Short term (≤ 2 years) |

| Limited consumer familiarity beyond tier-1 cities | -1.8% | Tier-3 and tier-4 cities, rural areas | Long term (≥ 4 years) |

| Counterfeit/grey-import bars eroding brand equity | -1.2% | National, concentrated in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Constraints on Health and Functional Claims

China’s regulatory framework for sports nutrition is structured around a dual-track approach led by the State Administration for Market Regulation (SAMR), which requires pre-market approval for new ingredients and restricts protein-content claims to products that meet the GB 28050-2025 nutrition labeling standards set to take effect in March 2027[4]Source: State Administration for Market Regulation, “GB 28050-2025 Nutrition Labeling Standards,” SAMR.GOV.CN. At the same time, GB 7718-2025 enforces full ingredient transparency and limits health-related statements to an approved list, prohibiting claims such as “muscle-building” or “fat-burning” unless supported by clinical evidence submitted to the National Medical Products Administration (NMPA). While soy protein isolate and whey protein were included in the raw materials catalog in 2023, easing the approval process for dairy-based protein bars, plant-derived proteins like pea and rice isolates are still reviewed individually, often delaying product introductions by six to twelve months. In addition, the General Administration of Customs (GACC) Decree 248 requires registration of overseas manufacturing facilities for imported protein bars, extending supply-chain lead times by 3 to 6 months and giving domestic producers with established NMPA ties an advantage. Collectively, these regulations tend to squeeze profit margins by roughly 8–12% for brands facing reformulation or launch delays, while also allowing compliant companies to gain market share from competitors that fail to meet the standards.

Ingredient Cost Volatility (Nuts, Whey, Plant Proteins)

In September 2025, whey protein concentrate traded between USD 1.35 and 1.80 per pound, while dry whey prices fell from USD 0.435 per pound in 2024 to USD 0.400 in 2025, reflecting a global dairy oversupply, according to the USDA Agricultural Marketing Service. Despite this, domestic whey prices in China climbed in late 2024 due to strong demand from infant formula and sports nutrition, creating a 15–20% premium over import parity and compressing margins for dairy-based protein bars. Nut-based bars, which accounted for 35.93% of the market in 2025, face 5-8% margin pressure when almond prices exceed USD 3.50 per pound, prompting brands to substitute peanuts or cashews, risking altered taste. Meanwhile, plant-based proteins like pea and rice isolates remain 20-30% more expensive per gram than whey, limiting their use largely to premium products even as consumer demand grows for sustainably sourced ingredients, according to the OECD-FAO Agricultural Outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Bars Dominate Through Functional Differentiation

Protein bars dominated 80.12% of the market in 2025 and are projected to grow at a 21.45% CAGR through 2031, fueled by their ability to deliver 15–20 grams of protein per serving while overcoming taste barriers with flavors like chocolate, yogurt, and hazelnut favored by Chinese consumers. In contrast, energy bars, cereal bars, and fruit-and-nut bars occupy the remaining share but expand more slowly, lacking the functional-ingredient innovation and multi-occasion versatility of protein bars. Mars China’s low-glycemic-index Snickers, launched in January 2024, illustrates this trend, reducing sugar by 40% and adding functional fibers to support sustained energy for work-break or pre-workout consumption rather than traditional confectionery occasions.

Energy bars remain popular among endurance athletes and marathon participants, supported by provincial sports-nutrition subsidies in Zhejiang and Jiangsu redeemable at retail outlets. Cereal bars face challenges from premiumization, being perceived as lower-protein, higher-carb options suited to children or casual snacking, while fruit-and-nut bars cater to the organic and clean-label segment, commanding 20–30% price premiums but constrained by shorter shelf life (6–9 months versus 12–18 months for protein bars) and higher ingredient costs during almond or hazelnut price spikes. Glanbia’s 2024 study found that 52% of protein-bar consumers eat them before or after workouts, 33% during TV or gaming, and 31% as work-break snacks, creating a broader use-case than energy bars (pre-workout) or cereal bars (breakfast or children’s snacks). The segment’s dominance is reinforced by e-commerce platforms such as Douyin and Pinduoduo, which drove the majority of Three Squirrels’ online sales in 2024 and prioritize high-margin, high-engagement products like protein bars in livestream campaigns, boosting visibility and trial rates.

By Ingredient Base: Dairy Innovation Outpaces Nut-Based Incumbents

Nut-based bars accounted for 35.93% of the market in 2025, but dairy- and protein-based variants are set to grow at a 20.94% CAGR through 2031, driven by consumer demand for higher protein content (18–22 grams per serving versus 8–12 grams for nut-based bars) and smoother textures that overcome taste barriers. Yili Group’s focus on whey-protein isolation and human milk oligosaccharide (HMO) development positions it to launch gut-health-oriented protein bars in 2026 for consumers emphasizing immunity, digestive wellness, and muscle recovery, while Mengniu Dairy advances mycoprotein and dairy-protein innovations. PepsiCo’s CNY 500 million (USD 68.6 million) oat facility in Jiangsu, with a 160,000-ton annual capacity, will supply oat-based protein bars by late 2025, blending plant and dairy proteins to appeal to flexitarian diets. Granola- and oat-based bars are expanding alongside the hot-cereals market, supported by PepsiCo’s segment presence, according to the USDA Foreign Agricultural Service.

Date-based bars remain niche, concentrated in tier-1 cities influenced by Middle Eastern and Mediterranean culinary trends, while hybrid bars combining nuts, dairy proteins, oats, and dates are among the fastest-growing sub-segments due to their flavor complexity and functional benefits. Tree-nut consumption in China is projected to rise, supporting long-term demand for nut-based bars, but price volatility in almonds and hazelnuts is prompting manufacturers to substitute peanuts or cashews, risking consumer dissatisfaction over taste changes. The “Other” category, including seed-based (chia, flax) and legume-based (chickpea, lentil) bars, captures a smaller share but is attracting startup R&D focused on vegan and allergen-free products.

By Price Tier: Premium Gains Despite Mass Dominance

Mass-tier protein bars held 78.15% of the market in 2025, but premium offerings are growing faster, at a 21.74% CAGR through 2031, as Gen Z and Millennials are willing to pay 30–50% more for clean-label, low-glycemic-index, or plant-based products. Premium bars, typically priced at CNY 8-15 (USD 1.10-2.07) per unit versus CNY 3-6 (USD 0.41-0.83) for mass-tier equivalents, justify the higher cost with 18-22 grams of protein per serving, functional ingredients like probiotics, collagen, and adaptogens, and sustainable packaging for wellness-focused consumers. Three Squirrels’ expansion into 33 sub-brands, including premium coffee and instant foods, illustrates this strategy, with the company achieving CNY 10.62 billion (USD 1.46 billion) revenue in 2024, a 49.3% year-on-year increase, driven by higher average selling prices and diversified channels. Mars China’s low-GI Snickers, positioned at the premium end of the mass tier, captured 12% of protein-bar sales within six months of its January 2024 launch, showing that functional innovation can command pricing power even among price-sensitive consumers.

Mass-tier products leverage scale through supermarkets and hypermarkets, which held 41.47% of the 2025 channel share, using high-traffic placement and multi-pack promotions to drive trials, while bulk-snack stores, 25,000 at end-2023 and expected to exceed 30,000 by 2025, offer single-serve mass-tier bars at CNY 2-4 (USD 0.28–0.55), lowering barriers in tier-2 and tier-3 cities where awareness remains under 15%, according to the USDA Foreign Agricultural Service. Premium-tier growth is concentrated in tier-1 cities and online platforms: Douyin’s livestreaming e-commerce, which reached CNY 807 billion (USD 111 billion) in 2024, highlights functional benefits and offers limited-time discounts, while private-label initiatives by Tmall and JD.com enter the premium space with 20-30% discounted own-brand protein bars, using consumer data to optimize flavors and packaging.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Online retail is set to grow at a 23.03% CAGR through 2031, outpacing supermarkets, hypermarkets, convenience stores, and other channels, driven by Douyin’s 49% urban household penetration and its overtaking of JD.com in health-product sales, according to the USDA Foreign Agricultural Service. Supermarkets and hypermarkets still held 41.47% of the market in 2025. Three Squirrels’ channel strategy shifted from 60% online/40% offline in 2022 to 70% offline/30% online in 2024, aiming to capture impulse purchases at bulk-snack stores and convenience outlets where protein bars are prominently placed near checkouts and beverage coolers. Convenience stores leverage extended hours, often operating 24/7, and proximity to offices and residential areas to serve work-break and late-night snacking occasions that supermarkets cannot address. Douyin and Pinduoduo accounted for 24.8% of Three Squirrels’ online sales in 2024, as livestreaming e-commerce offers lower commission rates (2-5% versus 5-8% on traditional platforms), allowing brands to invest more in influencer collaborations and product sampling.

Livestreaming campaigns generate over 2 billion annual views for protein-bar content, demonstrating usage occasions (pre-workout, work-break, post-dinner) and offering limited-time discounts of 30-40% that drive 8-12% conversion rates, compared with 2–4% for static listings. Instant retail and same-city delivery services via Meituan and Ele.me reduce purchase-to-consumption times to under 30 minutes in tier-1 cities, boosting impulse buys at convenience stores and bulk-snack outlets. Meanwhile, “Other Distribution Channels”, including gyms, fitness clubs, vending machines, and direct-to-consumer subscriptions, represent a smaller share but are growing as gyms partner with protein-bar brands to place vending machines in locker rooms and reception areas, capturing high post-workout purchase intent.

Geography Analysis

China’s snack bar market shows significant regional variation, with tier-1 cities, Beijing, Shanghai, Guangzhou, and Shenzhen, capturing a disproportionate share of revenue in 2025 despite comprising less than 10% of the population, driven by higher disposable incomes, fitness penetration of 35–40%, and protein-bar familiarity above 40%, according to the USDA Foreign Agricultural Service. Tier-2 cities like Chengdu, Hangzhou, Nanjing, and Wuhan are expanding rapidly, supported by provincial sports-nutrition subsidies in Zhejiang, Jiangsu, and Sichuan that provide vouchers redeemable at retail partners and mass-participation events such as marathons and cycling races. Zhejiang’s 2024 Healthy Living Initiative allocated CNY 120 million (USD 16.5 million) for sports-nutrition subsidies, while Jiangsu’s Sports Bureau partnered with convenience stores to offer 20% discounts during provincial games. Tier-3 and tier-4 cities experience slower adoption due to low consumer awareness, underdeveloped e-commerce logistics, and the prevalence of counterfeit or grey-market imports that erode brand equity.

Manufacturing hubs in Jiangsu, Guangdong, Shandong, and Shaanxi are attracting investment in automated bar-forming lines and smart warehousing: PepsiCo’s CNY 1.3 billion (USD 179 million) Shaanxi facility and CNY 500 million (USD 68.6 million) oat plant in Jiangsu will supply protein and oat-based bars across eastern and central China by late 2025, while Mondelez International’s CNY 53 million (USD 7.34 million) intelligent warehouse in Beijing supports same-city delivery under two hours. Three Squirrels’ CNY 200 million (USD 27.5 million) production upgrades in 2024 enable distribution to bulk-snack stores and convenience chains in tier-2 and tier-3 cities, where offline retail exceeds 70% but e-commerce logistics remain limited. These developments align with the China Food and Nutrition Development Plan (2025–2030), which emphasizes protein intake and functional nutrition, and provincial incentives targeting a CNY 7 trillion (USD 965 billion) sports industry by 2030, according to the State Council of China.

E-commerce penetration varies regionally: Douyin reaches 49% of urban households in tier-1 and tier-2 cities but only 20–25% in tier-3 and tier-4 markets, where platforms like Tmall and JD.com maintain stronger logistics and consumer trust. Bulk-snack stores, projected to exceed 30,000 by 2025, are concentrated in tier-2 and tier-3 cities, offering single-serve protein bars at CNY 2–4 (USD 0.28–0.55) to encourage trial among new consumers. Discount retailers such as Miniso and Yonghui have expanded snack-bar assortments, capturing market share in price-sensitive tier-2 cities dominated by mass-tier products. Meanwhile, counterfeit and grey-import bars remain prevalent in tier-3 and tier-4 cities, creating opportunities for compliant domestic manufacturers to gain share through education campaigns and retail partnerships emphasizing NMPA-approved labeling and GB 28050-2025 compliance.

Competitive Landscape

The Chinese snack bar market continues to be moderately fragmented, with the top five players, Beijing Happy Energy Health Technology, Mars, General Mills, PepsiCo (through Be & Cheery), and Nestlé—collectively accounting for less than a dominant share, leaving considerable room for regional specialists and e-commerce-native challengers to grow through provincial subsidies, automation, and livestreaming partnerships. Competitive strategies are increasingly split, as multinationals such as Mars and Nestlé emphasize functional-ingredient innovation and premium positioning, exemplified by Mars’ low-GI Snickers and Nestlé’s Harvest Gourmet plant-based facility in Tianjin, while domestic brands like Three Squirrels and Bestore focus on channel diversification and aggressive sub-brand expansion, with Three Squirrels moving into 33 sub-brands across categories including beverages, coffee, pet food, and instant meals and reporting CNY 10.62 billion (USD 1.46 billion) in 2024 revenue, up 49.3% year-on-year according to Reuters.

Yili Group and Mengniu Dairy are also entering the protein bar space by leveraging dairy-protein innovation, whey-isolation technology, and expansive distribution networks spanning more than one million retail points to cross-sell functional snacks within China’s CNY 115.8 billion (USD 16.0 billion) dairy market. Significant white-space opportunities remain in tier-3 and tier-4 cities where penetration is low, as well as in niche segments such as vegan, allergen-free, and keto-friendly bars catering to consumers focused on dietary needs and sustainability. Technology is reshaping competition, with Douyin’s 49% urban household reach and leadership in health-product sales enabling smaller brands to bypass traditional retail through influencer-led livestreaming that delivers 8-12% conversion rates versus 2-4% for static listings, according to the USDA Foreign Agricultural Service.

PepsiCo’s 2022 partnership with the Chinese Nutrition Society further strengthens its science-backed product development for Be & Cheery within SAMR’s regulatory framework, while advances in automated bar-forming equipment with AI quality control and IoT maintenance, offered by Chinese manufacturers with capacities of 150 to 1,200 kilograms per hour, are cutting unit costs by 18-22% and lowering barriers for mid-tier brands and private-label producers serving Tmall and JD.com. At the same time, e-commerce-native startups are disrupting traditional cycles by launching limited-edition local flavors such as salted egg yolk, matcha, and black sesame on platforms like Douyin and Xiaohongshu, gauging demand within weeks and scaling only after validation, significantly reducing inventory risk compared with conventional 12–18 month development timelines.

China Snack Bar Industry Leaders

Beijing Happy Energy Health Technology Co. Ltd

General Mills Inc.

Mars Incorporated

PepsiCo Inc.

Nestlé SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nestlé acquired Hsu Fu Chi (Fenghua Food) for an undisclosed sum, gaining access to the confectionery and snack-bar manufacturer's distribution network across tier-2 and tier-3 cities and its portfolio of date-based and nut-based bars popular in southern China.

- March 2025: Three Squirrels announced plans for an initial public offering in Hong Kong and launched its coffee brand, "Second Brain," expanding into beverages with 60 stock-keeping units and targeting CNY 2 billion (USD 275 million) in coffee revenue by 2027.

- January 2025: PepsiCo's CNY 500 million (USD 68.6 million) oat production facility in Jiangsu, capable of 160,000 tons annually, commenced production of oat-based protein bars, blending plant and dairy proteins to appeal to flexitarian consumers, with initial distribution through Be & Cheery's retail network

- June 2024: PepsiCo completed its CNY 1.3 billion (USD 179 million) facility in Shaanxi and expanded potato-chip capacity by 25,000 tons in Shandong, demonstrating capital commitment to snack-food automation and regional supply-chain optimization

China Snack Bar Market Report Scope

Snack bars are convenient, ready-to-eat food products in bar form designed to provide quick energy, nutrition, or satiety between meals. This report defines the China Snack Bar Market as the commercial landscape for ready-to-eat nutritional and functional snack bars and analyzes its scope across product types (cereal bars, energy bars, protein bars, fruit and nut bars), ingredient bases (nut-based, granola/oat-based, date-based, dairy/protein-based, hybrid blends, and others), price tiers (mass and premium), and distribution channels (supermarkets/hypermarkets, convenience stores, online retail stores, and other channels).

By Product Type

| Cereal Bar |

| Energy Bar |

| Protein Bar |

| Fruit and Nut Bar |

By Ingredient Base

| Nut-based bars |

| Granola/Oat-based |

| Date-based |

| Dairy/Protein-based |

| Hybrid blends |

| Other |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarket/Hypermarket |

| Convenience Store |

| Online Retail Store |

| Other Distribution Channels |

| By Product Type | Cereal Bar |

| Energy Bar | |

| Protein Bar | |

| Fruit and Nut Bar | |

| By Ingredient Base | Nut-based bars |

| Granola/Oat-based | |

| Date-based | |

| Dairy/Protein-based | |

| Hybrid blends | |

| Other | |

| By Price Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarket/Hypermarket |

| Convenience Store | |

| Online Retail Store | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms