Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

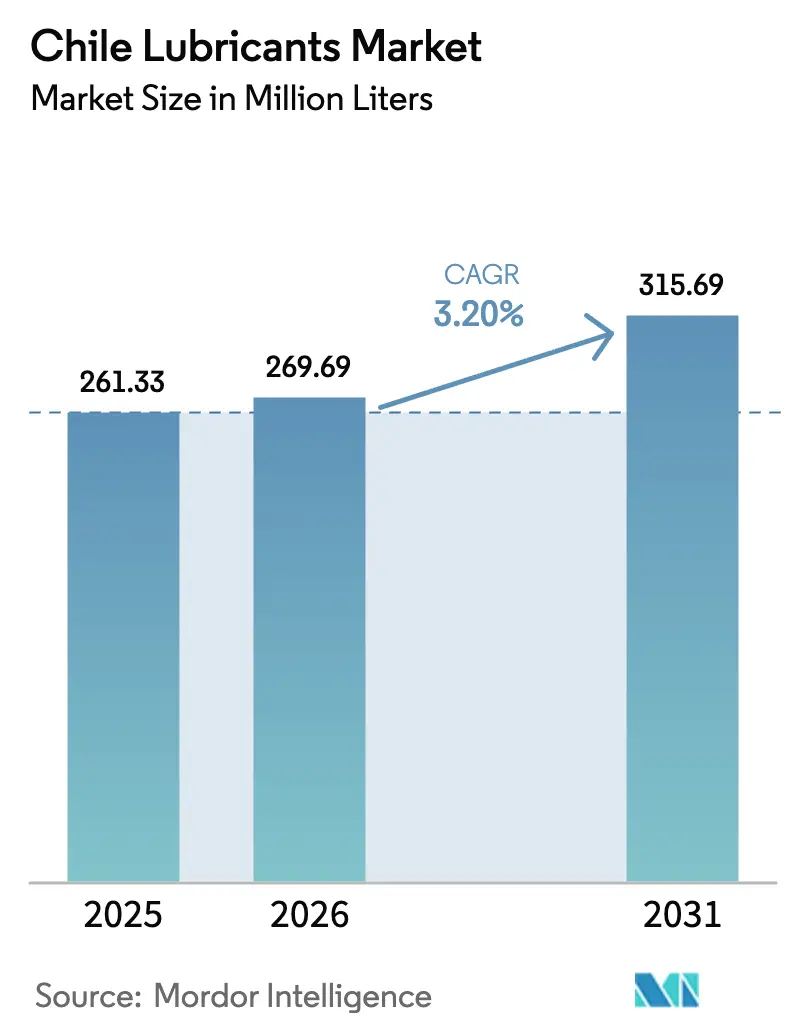

| Base Year Market Size (2025) | 261.33 Million liters |

| Market Volume (2026) | 269.69 Million liters |

| Market Volume (2031) | 315.69 Million liters |

| Growth Rate (2026 - 2031) | 3.20% CAGR |

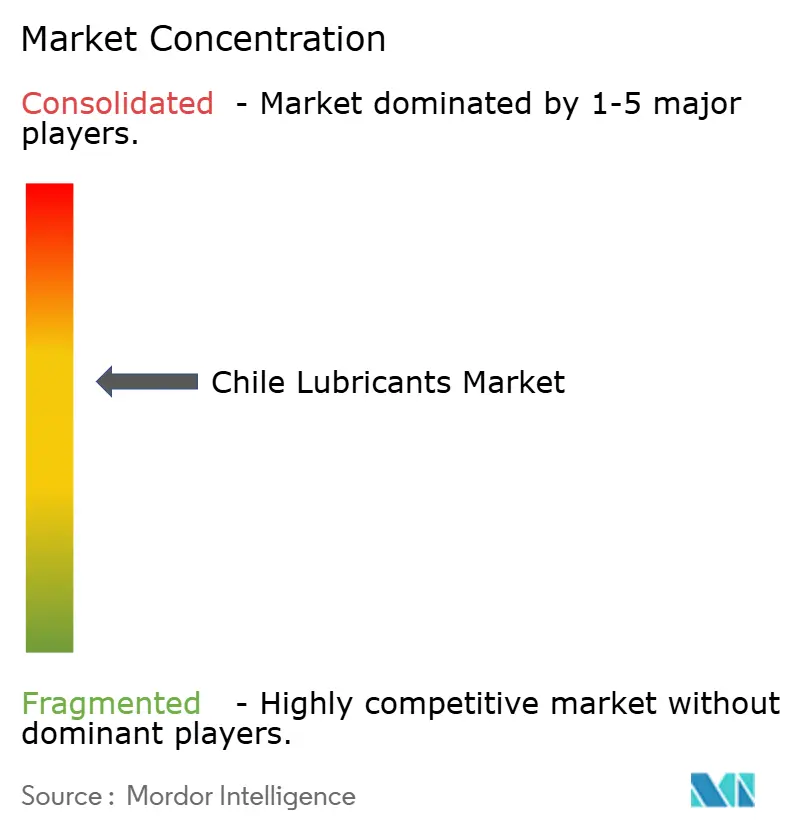

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Lubricants Market Analysis by Mordor Intelligence

The Chile Lubricants Market size was valued at 261.33 million liters in 2025 and is estimated to grow from 269.69 million liters in 2026 to reach 315.69 million liters by 2031, at a CAGR of 3.20% during the forecast period (2026-2031). This tempered headline growth conceals a deeper transition. Electrification across copper mining and public transport, tighter sulfur caps in fuel, and Law 20.920’s extended-producer-responsibility (EPR) rules are reshaping formulations, pushing demand toward premium synthetics and bio-based blends even as longer drain intervals curb volume turnover. With imported base oils constituting nearly all of the supply, fluctuations in the peso and shifts in freight rates can significantly impact landed-cost spreads and influence stocking choices. Engine oil remains the dominant segment. However, this supremacy is being tempered by the rapid rise of niche segments, including specialty greases tailored for battery-electric haul-truck drivetrains and biodegradable hydraulic fluids designed for underground mining. The competitive landscape is fierce: Empresas Copec, harnessing Mobil-branded products and its Quintero blending plant, commands a notable market share. Meanwhile, Enex is expanding its footprint with service stations and Shell Oil Change centers, bolstering its national presence.

Key Report Takeaways

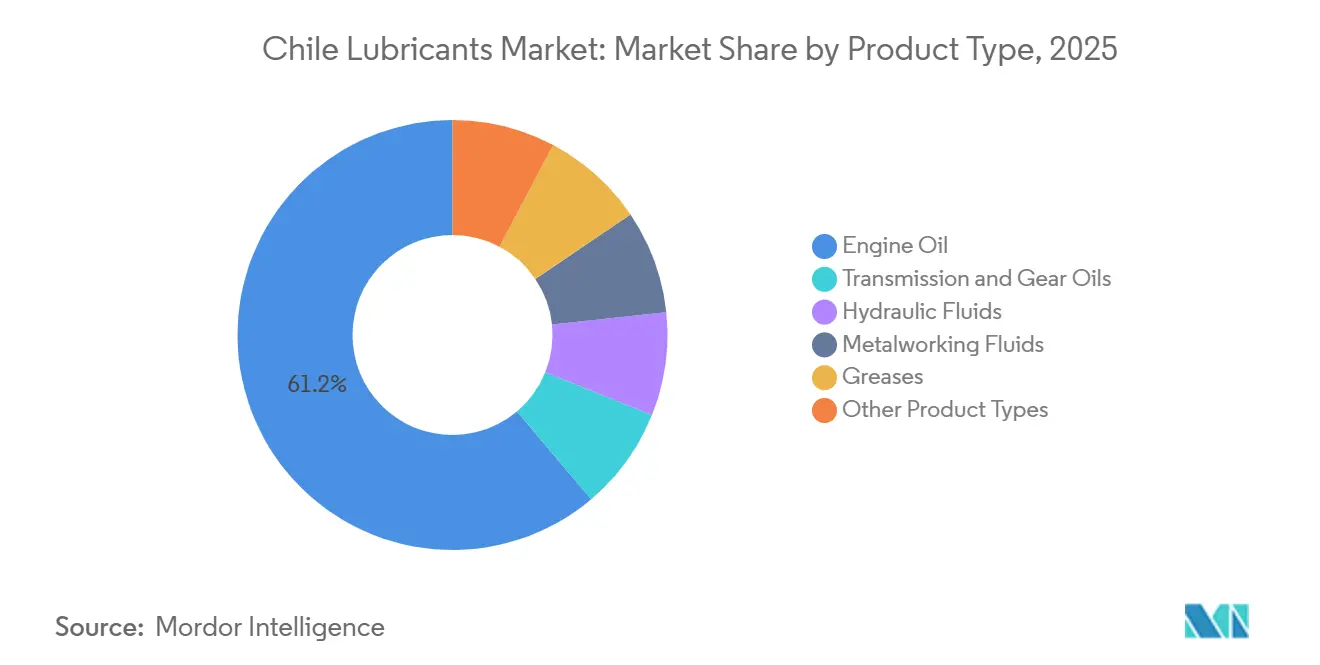

- By product type, engine oil accounted for a 61.16% share of the Chile lubricants market in 2025 and is expected to expand at a 4.80% CAGR through 2031.

- By end-user, the automotive sector held 82.08% of the Chile lubricants market share in 2025, while power generation is projected to post the fastest CAGR at 5.10% through 2031.

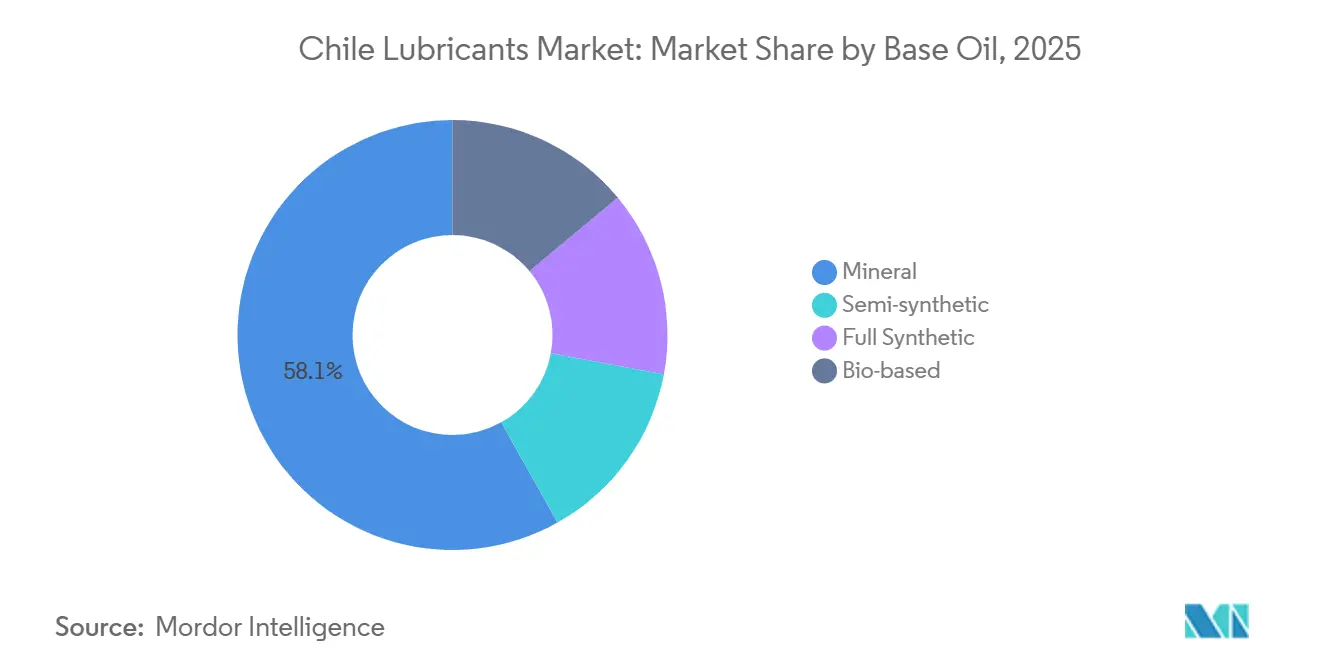

- By base oil, mineral grades captured 58.12% of the Chile lubricants market size in 2025, whereas bio-based formulations are forecast to advance at a 6.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mining-equipment lubricant demand | +1.2% | Antofagasta, Atacama, Coquimbo | Long term (≥ 4 years) |

| Growing automotive-aftermarket volumes | +0.8% | Santiago, Valparaíso, Concepción | Medium term (2–4 years) |

| Expansion of copper-processing capacity | +0.6% | Antofagasta, O’Higgins | Long term (≥ 4 years) |

| OEM-approved low-viscosity synthetics | +0.5% | Atacama Desert mining corridors | Medium term (2–4 years) |

| Maritime fuel-efficiency mandates | +0.3% | Valparaíso, San Antonio, Antofagasta, Iquique | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Mining-Equipment Lubricant Demand

Cochilco’s investment pipeline through 2028 keeps demand robust for hydraulic fluids, greases, and engine oils used in haul trucks, excavators, and crushers[1]Comisión Chilena del Cobre, “Cartera de Proyectos de Inversión Minera 2025-2035,” Cochilco.cl. TotalEnergies field trials report diesel savings when optimized lubricants reduce friction and heat in large mining fleets, directly supporting cost-of-ownership targets. Codelco’s November 2025 five-year multi-vendor contracts confirm a preference for supply security and performance differentiation, spreading volumes across Copec, Enex, Klüber Lubrication Chile, Mining Lube Engineering, and Esmax. Water scarcity drives up-time priorities; a significant portion of Antofagasta’s water now comes from desalination, increasing dust exposure and heightening the need for high-film-strength lubricants. The IEA projects global copper extraction must rise significantly over three decades to meet the energy-transition metals demand, locking in Chile’s position as a lubricant-intensive supplier.

Growing Automotive-Aftermarket Volumes

Chile's expanding vehicle parc fuels a robust aftermarket for engine oils, coolants, and transmission fluids. Enex, with its Shell Oil Change centers and service stations, anchors convenience, catering to both DIY motorists and commercial fleets. In December 2025, distributor Andes Motor standardized product approvals, integrating Shell Helix and Shell Rimula lubricants across its network, covering brands from Maxus to Iveco. The market sees a swift shift to ultra-low-viscosity grades, with SAE 0W-20, 0W-16, and 0W-12 oils, featuring low-SAPS chemistries, safeguarding modern after-treatment systems. Chevron's March 2025 roll-out of GF-7 underscores the industry's pivot towards OEM-certified synthetics.

Expansion of Copper-Processing Capacity

In 2024, Chile focused heavily on exploration, with a primary emphasis on copper. This move indicates a rise in demand for metalworking fluids and hydraulic oils, thanks to the introduction of new concentrators. Meanwhile, battery-electric and hydrogen-hybrid haul trucks are turning to high-performance greases for their wheel bearings and gear sets, which are designed to endure higher torque cycles. This demand for greases is helping to counterbalance a dip in engine oil consumption. Highlighting the industry's shift, TotalEnergies introduced HYDRANSAFE HFC-E, a fire-resistant and biodegradable hydraulic fluid, showcasing a commitment to underground safety and eco-toxicity standards.

OEM-Approved Low-Viscosity Synthetics for Chile’s Cold-Desert Nights

In the Atacama Desert, where day-night temperature swings are extreme, lubricants must have pour points below –40 °C and high viscosity indices. Detroit Diesel’s DT12 Latin America bulletin endorses MB 235.16 75W-85 fluids, permitting extended drain intervals. This not only compresses lubricant turnover but also elevates the per-liter value. The API introduced its SQ specification in 2025, targeting hybrid vehicles. This new standard tightens volatility and oxidation thresholds, steering formulators towards Group III+ and PAO base stocks. ExxonMobil’s Mobil Delvac 1 Transmission Fluid V30, boasting certifications from Volvo 97307/97318, showcases a low pour point and a high viscosity index, highlighting the industry's shift towards premium synthetics.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV adoption in Santiago’s taxi fleet | –0.6% | Santiago Metropolitan Region | Medium term (2–4 years) |

| Stricter used-oil disposal norms (DS148 revision) | –0.3% | Urban centers nationwide | Short term (≤ 2 years) |

| Base-oil import cost volatility | –0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Adoption in Santiago’s Taxi Fleet

In 2024, Santiago's all-electric bus fleet expanded significantly, accounting for a notable portion of the city's total buses. Projections indicate further growth by the close of 2025, signaling a shift away from heavy-duty engine oil demand. Passenger battery electric vehicle (BEV) sales have also boosted market penetration. With policy roadmaps in place, there's a strong indication that national BEV uptake could surpass a significant threshold in the next decade. This shift threatens to diminish engine oil volumes, a staple in the automotive industry. In response, suppliers are increasingly diversifying, focusing on high-performance greases tailored for electric drivetrains and exploring non-automotive sectors like power generation and mining.

Stricter Used-Oil Disposal Norms (DS148 Revision)

Law 20.920 lists used lubricating oil as priority waste under EPR rules, assigning collection and recycling obligations to producers and importers[2]Ministerio de Medio Ambiente, “Ley 20.920 Reglamento REP Aceites Lubricantes,” Medioambiente.gob.cl. Decree DS148 classifies used oil as hazardous, mandating certified storage, transport, and treatment—raising compliance costs especially for small workshops. Enex joined the ReSimple and ProREP collective systems and became the first lubricant brand with a HuellaChile product-footprint verification, signaling a move toward lifecycle transparency that may favor incumbents with logistics scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor Volume, Greases Gain in Mining

Engine oil held a 61.16% slice of the Chile lubricants market in 2025 and is expected to expand at a 4.80% CAGR through 2031 on the back of a large legacy internal-combustion fleet. Even with extended drain intervals, the shift towards API SP and SQ synthetic grades continues to drive revenue growth, outpacing volume increases. While transmission and gear oils constitute a smaller yet vital segment, Detroit's DT12 gearboxes now recommend MB 235.16 75W-85 oils. These oils, with drain intervals extending significantly, elevate their value based on specifications, even as overall turnover sees a decline.

Hydraulic fluids play a crucial role in mining operations. Biodegradable, fire-resistant HFC-E products are now meeting the heightened safety standards mandated for underground operations. Mining investments are fueling concentrator expansions, which in turn require lubricants for cutting, grinding, and forming. Specialty greases are witnessing the fastest growth in this landscape, driven by electrified haul-truck drivetrains that demand higher torque loads and operate on continuous duty cycles. Lithium-complex chemistry is at the forefront, bolstered by domestic lithium extraction, ensuring a steady supply of raw materials.

By End-User Industry: Automotive Dominates, Power Generation Accelerates

Automotive retained 82.08% of Chile's lubricants market share in 2025 but faces a structural slide as EV penetration climbs, especially in urban fleets. While engine-oil volumes taper, ultra-low-viscosity synthetics and service bundles cushion revenue decline. Power generation, although smaller, posts the fastest CAGR at 5.10% through 2031 as wind, solar, and battery storage projects demand turbine oils, transformer oils, and hydraulic fluids for pitch systems. Codelco’s multi-vendor contracts underscore steady diesel-engine demand for mine fleets, while new LNG-powered maritime assets pull in dual-fuel marine-engine lubricants.

By Base Oil: Mineral Leads, Bio-Based Surges on Regulatory Tailwinds

Mineral grades held a 58.12% share in 2025 courtesy of cost advantage, yet bio-based formulations exhibit the highest growth trajectory at 6.41% CAGR to 2031, underpinned by EPR incentives and eco-labeling requirements. Semi-synthetic blends bridge cost-performance gaps, while Group III and PAO full synthetics gain share as OEM drain specifications tighten. Shell’s Panolin range and TotalEnergies’ HYDRANSAFE offerings illustrate how suppliers leverage biodegradable credentials to win contracts in environmentally sensitive operations.

Geography Analysis

The regions of Antofagasta, Atacama, and Coquimbo, rich in copper, accounted for a significant portion of Chile's national copper output in 2024. In Antofagasta, where a significant percentage of water extractions now depend on desalination, water scarcity exacerbates dust and heat challenges. As a result, miners are increasingly turning to high-film-strength synthetics and biodegradable hydraulic fluids, tailored for the region's harsh desert conditions.

Passenger cars and light commercial vehicles dominate the central-valley regions of Santiago, Valparaíso, and O’Higgins. However, with Santiago rapidly electrifying its public transport and ride-hailing fleets, traditional engine oil consumption is poised to decline. This shift heightens competition for premium synthetics and services at quick-service centers.

Marine-lubricant demand is anchored in coastal hubs like Valparaíso, San Antonio, Antofagasta, and Iquique. These hubs cater especially to fishing and coastal cargo vessels, which are now adopting LNG or biofuel blends to comply with IMO carbon-intensity regulations. Meanwhile, the southern macro-zones, stretching from Biobío to Magallanes, may have a smaller lubricant demand, but it's growing. This uptick is fueled by the needs of forestry machinery, aquaculture facilities, and onshore wind turbines, all of which require specialized greases and turbine oils.

Competitive Landscape

The Chile lubricants market is moderately consolidated. Niche specialists such as Klüber Lubrication Chile win share in high-performance greases through technical differentiation, while Mining Lube Engineering leverages site-based service contracts to entrench product lines in remote mining districts. White-space opportunities cluster around bio-lubricants, turbine oils for renewable projects, and digital oil-analysis platforms that shift engagements from product supply to condition-based maintenance.

Chile Lubricants Industry Leaders

Shell Plc

Chevron Corporation

BP PLC

TotalEnergies

YPF SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP PLC began exploring a divestiture of its Castrol lubricants unit, valued near USD 10 billion, as part of a plan to raise USD 20 billion by 2027. The sale could reshape Castrol’s sizable Chilean footprint.

- May 2025: TotalEnergies released next-generation Quartz oils meeting API SQ and ILSAC GF-7 performance bars and designed for turbocharged gasoline direct-injection engines.

Chile Lubricants Market Report Scope

Any substance physically integrated to reduce friction between two or more moving surfaces is called a lubricant. On metallic surfaces, lubricants aid in preventing material degradation, erosion, corrosion, and rust development. Lubricants are typically made up of 90% petroleum-based oil and various additives to give them desirable properties specific to a given purpose.

The Chile lubricants market is segmented by product type, end-user industry, and base oil. By product type, the market is segmented into engine oil, transmission and gear oils, hydraulic fluids, metalworking fluids, greases, and other product types (e.g., industrial heat transfer fluid). By end-user industry, the market is segmented into automotive, power generation, heavy equipment, metallurgy and metalworking, and other end-user industries (e.g., marine and rail). By base oil, the market is segmented into mineral, semi-synthetic, full synthetic, and bio-based. For each segment, the market sizing and forecasts have been done based on volume (Litres).

By Product Type

| Engine Oil |

| Transmission and Gear Oils |

| Hydraulic Fluids |

| Metalworking Fluids |

| Greases |

| Other Product Types (Industrial Heat Transfer Fluid, etc.) |

By End-user Industry

| Automotive |

| Power Generation |

| Heavy Equipment |

| Metallurgy and Metalworking |

| Other End-user Industries (Marine and Rail, etc.) |

By Base Oil

| Mineral |

| Semi-synthetic |

| Full Synthetic |

| Bio-based |

| By Product Type | Engine Oil |

| Transmission and Gear Oils | |

| Hydraulic Fluids | |

| Metalworking Fluids | |

| Greases | |

| Other Product Types (Industrial Heat Transfer Fluid, etc.) | |

| By End-user Industry | Automotive |

| Power Generation | |

| Heavy Equipment | |

| Metallurgy and Metalworking | |

| Other End-user Industries (Marine and Rail, etc.) | |

| By Base Oil | Mineral |

| Semi-synthetic | |

| Full Synthetic | |

| Bio-based |

Key Questions Answered in the Report

What is the current size and forecast growth of the Chile lubricants market?

The Chile lubricants market size is 269.69 million liters in 2026 and is projected to reach 315.69 million liters by 2031, reflecting a 3.20% CAGR.

Which product category leads consumption?

Engine oil remains dominant with a 61.16% share in 2025, supported by a large internal-combustion fleet and premium migration to synthetics.

How will electric-vehicle adoption affect lubricant demand?

Electric buses and passenger BEVs reduce engine oil volumes, especially in Santiago, but create opportunities for specialty greases and thermal-management fluids for electric drivetrains.

Which regions account for the highest lubricant consumption?

Antofagasta, Atacama, and Coquimbo regions lead industrial volumes due to copper mining, while Santiago and Valparaíso dominate automotive demand.

Page last updated on: