Brazil Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

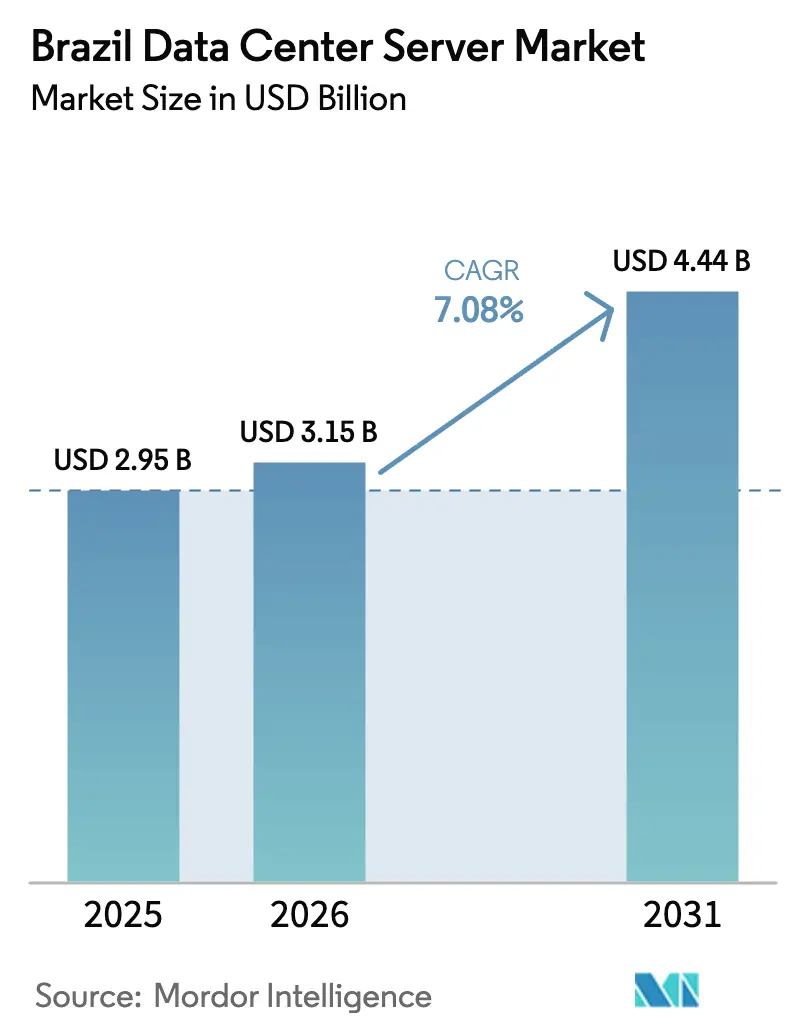

| Base Year Market Size (2025) | USD 2.95 Billion |

| Market Size (2026) | USD 3.15 Billion |

| Market Size (2031) | USD 4.44 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

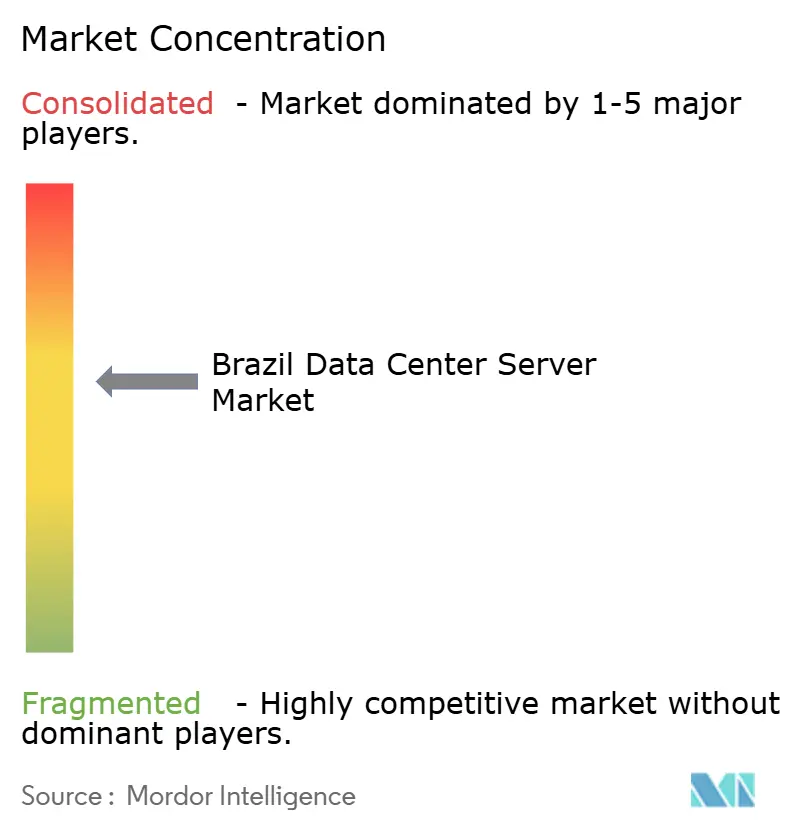

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Data Center Server Market Analysis by Mordor Intelligence

The Brazil data center server market size is projected to be USD 2.95 billion in 2025, USD 3.15 billion in 2026, and reach USD 4.44 billion by 2031, growing at a CAGR of 7.08% from 2026 to 2031. Strong federal incentives, an acceleration in artificial-intelligence adoption, and hyperscalers’ search for sovereign compute capacity anchor the current expansion of the Brazil data center server market. Investment clusters around São Paulo, Rio de Janeiro, and the Campinas corridor, where renewable-energy substations, fiber backbones, and skilled labor enable rapid capacity additions. Operators are retrofitting facilities with liquid cooling to handle tropical thermals and GPU power densities that exceed legacy design limits. Currency volatility and elevated import tariffs raise delivered hardware costs, yet local assembly in the Manaus Free Trade Zone and proposed ReData tariff relief are buffering some of the inflationary pressure. Competitive dynamics are intensifying as domestic integrators leverage duty exemptions to win public-sector tenders while global OEMs secure large hyperscale contracts that underpin long-term demand visibility.

Key Report Takeaways

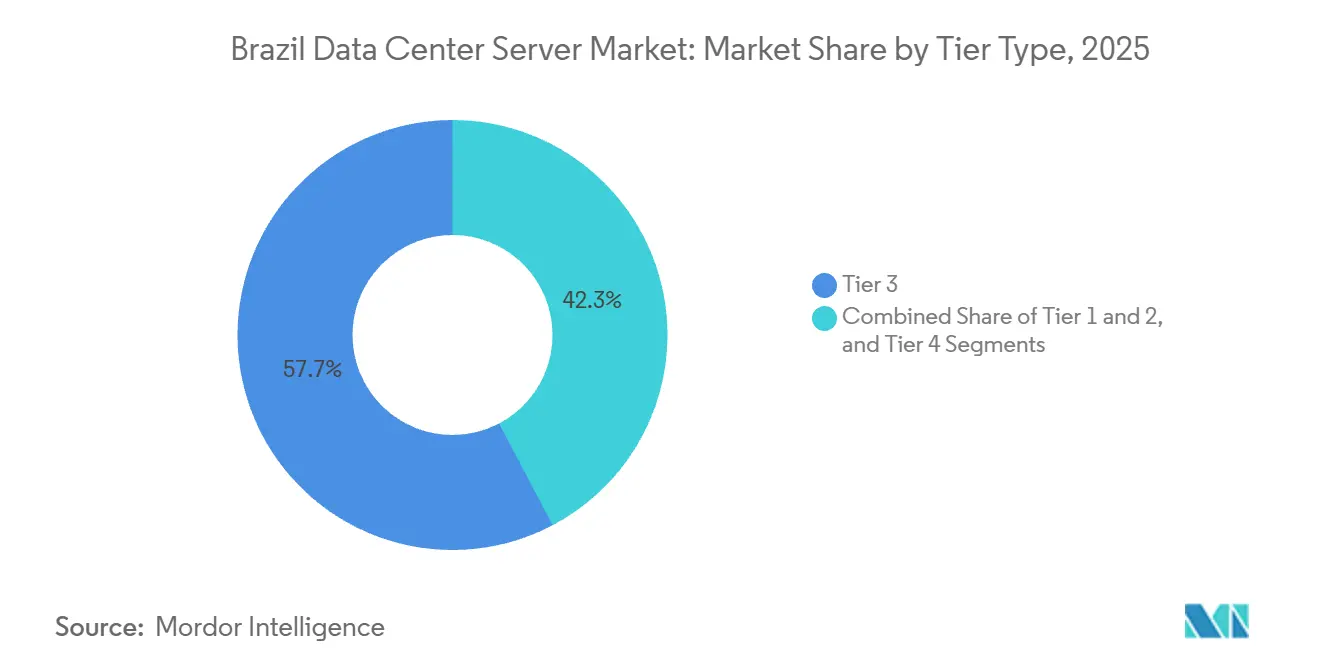

- By tier classification, Tier 3 facilities held 57.72% of Brazil data center server market share in 2025 while Tier 4 deployments are advancing at a 6.15% CAGR through 2031.

- By size, hyperscale campuses accounted for 59.94% of the Brazil data center server market size in 2025 and are forecast to grow at a 6.35% CAGR to 2031.

- By ownership model, colocation sites led with 54.87% of share in 2025, yet hyperscaler self-builds are expanding the fastest at 6.67% CAGR to 2031.

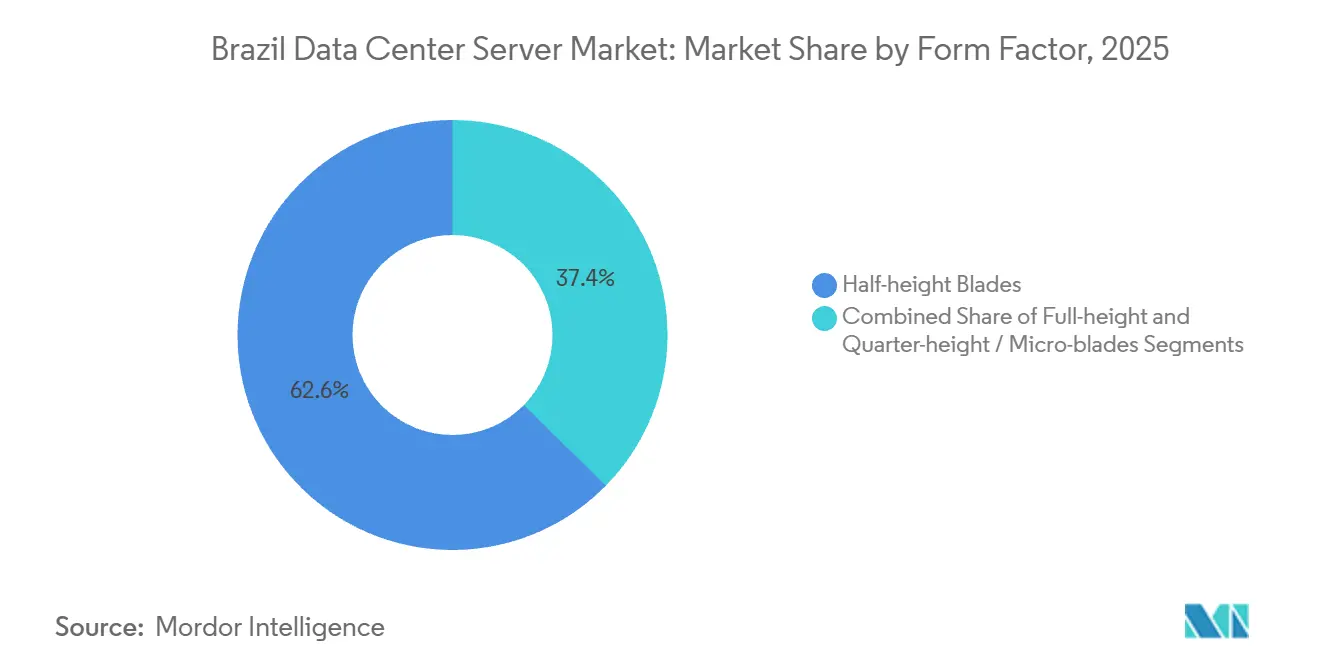

- By form factor, half-height blades dominated with 62.64% share in 2025, while quarter-height and micro-blades are projected to expand at 6.72% CAGR through 2031.

- By workload, AI and advanced analytics captured 37.76% share share in 2025, reflecting the pivot toward GPU-dense configurations.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The data center server market size of Mordor Intelligence integrates these into one global valuation.

Brazil Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Significant Investments in Hyperscale and Colocation Build-Outs | +1.8% | National, concentrated in São Paulo, Rio de Janeiro, Campinas | Medium term (2-4 years) |

| AI / ML Workload Surge Demanding GPU-Dense Servers | +1.5% | São Paulo, Rio de Janeiro, academic hubs | Short term (≤ 2 years) |

| 5G Roll-Out Pushing Regional Edge Nodes | +1.0% | State capitals, 1 000+ municipalities | Medium term (2-4 years) |

| Corporate Shift to Hybrid Cloud and SaaS | +0.9% | Financial services, retail, telecom | Long term (≥ 4 years) |

| Federal Data Center Incentive Package Unlocking USD 377 billion Capex | +1.2% | Nationwide | Long term (≥ 4 years) |

| Adoption of Liquid Cooling to Meet Tropical Thermal Challenges | +0.5% | GPU clusters in hot-weather zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Significant Investments in Hyperscale and Colocation Build-Outs

Hyperscale and colocation operators announced more than USD 5 billion in new Brazilian capacity during 2025, led by projects such as Elea’s Rio AI City and Ascenty’s partnership with Aligned Data Centers.[1]Bruno Rovai, “Microsoft activates its first two AI data halls in Brazil,” BNamericas, bnamericas.com Microsoft activated its first AI-dedicated halls in early 2026, reinforcing sovereign-cloud positioning. Institutional investors, including the USD 1.4 billion Patria–GIC joint venture, are accelerating green-field builds, signaling confidence despite currency risk. Investment remains concentrated in the Southeast, yet edge-oriented projects are emerging in Fortaleza and Curitiba to serve 5G-enabled low-latency workloads.

AI/ML Workload Surge Demanding GPU-Dense Servers

Public-sector entities and enterprises increased orders for NVIDIA Hopper and Blackwell GPUs throughout 2025, driving record demand for liquid-cooled, high-density racks.[2]Daniela Braun, “Nvidia urges government support for AI in Brazil,” Valor International, valorinternational.globo.com The University of São Paulo’s Jairu cluster, deployed in 2026, underscores domestic integration capabilities. GPU-as-a-service offerings from Claro and Axia Energia monetize idle capacity and help enterprises bypass import-tariff constraints.

5G Roll-Out Pushing Regional Edge Nodes

TIM Brasil extended 5G to 1,000 municipalities by late 2025, installing 8,400 gNodeBs that enable low-latency edge compute. ANATEL’s February 2026 approval of a 700 megahertz auction prioritizes rural precision-agriculture use cases. Edge servers in quarter-height or micro-blade formats are therefore poised for rapid uptake at cell-site aggregation points.

Corporate Shift to Hybrid Cloud and SaaS

ANPD Resolution 19/2024 tightens cross-border data transfers, prompting enterprises to repatriate sensitive workloads onto hybrid multicloud platforms. IBM research shows a 2.5× value uplift from hybrid architectures relative to single-cloud deployments. Telecom operators are bundling sovereign AI services that blend private-cloud GPU pools with public-cloud elasticity, widening the addressable base for Brazil data center server market offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cyber-Attacks and LGPD Compliance Costs | -0.7% | Major metros with strict enforcement | Short term (≤ 2 years) |

| BRL Volatility and Import Tariffs on IT Hardware | -0.9% | Nationwide importers | Short term (≤ 2 years) |

| São Paulo Power-Grid Congestion Delaying Rack Energization | -0.4% | São Paulo metro | Medium term (2-4 years) |

| Limited Domestic Silicon Packaging and Test Capacity | -0.3% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Attacks and LGPD Compliance Costs

ANPD’s elevation to independent-agency status in 2024 ushered in stricter breach-notification timelines and higher penalties, raising the total cost of ownership for colocation tenants. Resolution 18/2024 formalized data-protection-officer mandates, compelling small and mid-sized firms to hire specialized staff. Operators must now certify resilience and sustainability under ANATEL Resolution 780/2025, extending project lead times and capital requirements.

BRL Volatility and Import Tariffs on IT Hardware

The Brazilian real fell more than 15% against the U.S. dollar in 2025, magnifying landed costs for imported servers and GPUs. Combined federal and state duties can exceed 52% on AI accelerators, postponing enterprise refresh cycles.[3]Daniela Braun, “Brazilian public sector boosts AI investment, Nvidia says,” Valor International, valorinternational.globo.com Provisional Measure 1 318/2025, which would grant tariff relief under the ReData program, faces legislative uncertainty, injecting procurement risk for hyperscalers planning multibillion-dollar campuses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Mission-Critical Workloads Drive Tier 4 Momentum

Tier 3 facilities held the largest slice of the Brazil data center server market in 2025, supported by colocation providers that balance uptime with cost. Tier 4 facilities are gaining ground at a 6.15% CAGR as banks and government agencies insist on 99.995% availability, pushing the Brazil data center server market size for Tier 4 toward double-digit share by 2031. Campinas and Fortaleza offer land and renewable-energy advantages that attract new Tier 4 builds. Consolidation into higher tiers satisfies ANPD’s 24-hour incident-notification rule and mitigates financial losses from interrupted AI training runs. Meanwhile, Tier 1 and Tier 2 sites remain relevant for edge content-delivery networks and disaster-recovery nodes, yet their relative share continues to erode as enterprises migrate to higher resilience footprints.

Tier 3 deployments cluster in São Paulo, Rio de Janeiro, and Brasília, where fiber density and skilled labor justify the incremental redundancy. Tier 4 projects such as Local DC’s USD 20 million Campinas build add megawatt-scale blocks optimized for GPU racks, aligning with ReData’s renewable-energy provisions. Power-and-cooling fault tolerance is now viewed as strategic insurance rather than overhead, especially for sovereign AI models that cannot be easily restarted in another region. Lower-tier facilities target niche uses, including IoT gateways and regional backups, but face margin compression as capital gravitates toward Tier 3 and Tier 4 expansions.

By Data Center Size: Hyperscale Dominance Reflects Cloud and AI Concentration

Hyperscale campuses accounted for 59.94% of the Brazil data center server market share in 2025 and are projected to grow at a 6.35% CAGR during the forecast period, as Microsoft, Oracle, and Ascenty build multi-gigawatt footprints. Hyperscale operators bundle renewable power purchase agreements and subsea-cable connectivity, lowering the total cost of ownership for GPU tenants. Large-scale facilities follow in secondary tech hubs such as Campinas, delivering mid-scale capacity to regional service providers.

Medium-sized data centers serve verticals that require sovereign data without hyperscale scale economies, while small edge sites support latency-sensitive 5G and IoT workloads. Embratel’s program to build 15 micro-data centers underscores the commercial viability of distributed footprints. As the Brazil data center server market matures, size-based segmentation increasingly correlates with workload type: AI training gravitating toward hyperscale GPU clusters, and content caching or industrial IoT favoring small-footprint edge nodes.

By Data Center Type: Colocation Leads, Hyperscalers Accelerate

Colocation Data Center accounted for 54.87% of the market share in 2025. Enterprises favored colocation in 2025 to diffuse LGPD compliance and cybersecurity spending across tenants. However, hyperscalers internalize rack capacity faster, posting a 6.67% CAGR that narrows the gap within the Brazil data center server market. Oracle and NVIDIA’s memorandum to equip Elea’s Rio AI City with Blackwell GPUs exemplifies self-build momentum, although final commitments hinge on tariff relief.

Enterprise and edge facilities retain niches where on-premises control or ultra-low latency is mandatory, yet hybrid-cloud orchestration increasingly lets firms flex between private racks and public regions. Colocation providers counter hyperscaler gains by launching GPU-as-a-service and managed AI stacks that deliver pay-per-use access to scarce H100 and B200 inventory, reinforcing their relevance for mid-market adopters.

By Form Factor: Blades Dominate, Micro-Blades Gain Edge Traction

Half-height blades constituted 62.64% of share in 2025, supported by mature supply chains and dense virtualization needs. Full-height blades cater to 2-kilowatt-plus GPU nodes for AI training, while quarter-height and micro-blades grow fastest at 6.72% CAGR as operators place inference clusters at 5G edge nodes. As 5G coverage extends to 1 000 municipalities, compact servers suited to constrained cell-site cabinets gain relevance. Although micro-blades still face ecosystem limitations, falling per-core costs and telecom partnerships are expected to widen adoption within the Brazil data center server market.

Quarter-height designs power smart-city cameras and precision-agriculture gateways running on ruggedized hardware. Half-height blades remain the default for virtualized private clouds, where density and management homogeneity trump form-factor miniaturization. Full-height chassis capture share in academic clusters such as Jairu, whose NVLink-interconnected B200 nodes illustrate the thermal and power demands addressed by liquid cooling.

By Application and Workload: AI Leads, Virtualization Rebounds

AI, machine learning, and advanced analytics contributed 37.76% of share in 2025, fueled by sovereign AI projects and GPU-as-a-service offerings. Virtualization and private cloud workloads are set for a 6.49% CAGR through 2031 as Resolution 19/2024 encourages on-premises repatriation. High-performance computing supports oil-and-gas simulation and academic research, while media rendering and genomics drive storage-centric demand for NVMe arrays.

Edge inference workloads expand alongside 5G, yet hardware tariffs slow mass deployment. Telecom operators localize large-language-model processing to respect data-sovereignty mandates, blending small language models with Portuguese-specific datasets. Hybrid-cloud control planes orchestrate workloads across colocation, hyperscale, and edge facilities, enhancing the Brazil data center server market’s resilience to currency and tariff shocks.

Geography Analysis

São Paulo retains the largest installed base, leveraging fiber convergence and proximity to enterprise headquarters. Rio de Janeiro ranks second, buoyed by subsea-cable landings and energy availability that underpin hyperscale expansions. The Campinas corridor emerges as an alternative hyperscale hub, offering lower land costs and shorter timelines for grid interconnection.

In the Northeast, Fortaleza attracts edge deployments due to its strategic subsea connectivity to Africa and Europe. This positions it as a hub for content delivery and gaming latency. Southern states such as Paraná and Rio Grande do Sul witness medium-scale builds tailored to manufacturing and agritech workloads, leveraging cooler climates that ease cooling loads.

Central-West regions are seeing growing interest from mining and precision agriculture verticals that rely on AI inference at regional edge nodes. Federal investments in satellite backhaul and 5G rural coverage extend server demand into previously underserved municipalities. As geographic dispersion increases, the Brazil data center server market remains heavily weighted toward the Southeast through 2026.

Mordor Intelligence tracks the data center server market across other major regions such as Americas, Africa, and North America, with additional country-level coverage spanning Canada, United States, Nigeria, South Africa, Italy, and Norway, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Brazil data center server market is moderately concentrated. Huawei and Inspur capture budget-sensitive public-sector contracts with financing flexibility, while Supermicro-licensed assemblies from Positivo and Scherm Brasil benefit from Manaus duty exemptions. NVIDIA dominates AI accelerator sockets with Hopper and Blackwell GPUs, despite AMD’s inroads in virtualization-heavy environments.

Colocation providers differentiate by locking in renewable power purchase agreements and integrating liquid cooling, meeting ReData’s sustainability thresholds. Hyperscalers secure exclusive GPU allocations through direct supplier partnerships, mitigating export-control bottlenecks. Emerging disruptors include energy firms like Axia Energia, which monetize spare GPU capacity, and telecom operators like Claro Brasil, leveraging NVIDIA Cloud Partner status to deliver sovereign AI services.

Network-fabric innovation accelerates as Arrcus and OpenGlobe deploy programmable routers supporting SRv6 for Brazil’s education network. This deployment showcases open-networking alternatives that may spill into commercial edge designs. Competitive intensity is expected to rise through 2031, but first-mover builders of sovereign AI capacity and renewable-powered campuses are positioned to capture above-market growth.

Brazil Data Center Server Industry Leaders

Hewlett Packard Enterprise (HPE)

Super Micro Computer Inc.

Cisco Systems Inc.

IBM Corporation

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft activated two AI-dedicated halls in Hortolândia and Sumaré, São Paulo, the first stage of a BRL 14.7 billion (USD 2.7 billion) program scheduled through 2027.

- February 2026: The University of São Paulo unveiled Jairu, South America’s largest AI cluster, with 96 NVIDIA Blackwell B200 GPUs assembled domestically at a cost of BRL 40 million (USD 7.4 million).

- February 2026: Brazil’s Federal Court of Accounts cleared ANATEL’s 700 MHz auction, expanding rural 5G and enabling precision-agriculture edge deployments.

- February 2026: Local DC committed USD 20 million to a 6 MW Campinas data center designed for GPU-heavy sovereign workloads.

- December 2025: Arrcus and OpenGlobe delivered programmable SRv6 routers for the national research network, enabling OpenRAN experimentation.

Brazil Data Center Server Market Report Scope

A data center server is basically a high-capacity computer without peripherals like monitors and keyboards. It is a hardware unit installed inside a rack, having a central processing unit (CPU), storage, and other electrical and networking equipment, making them powerful computers that deliver applications, services, and data to end-user devices.

The Brazil Data Center Server Market Report is Segmented by Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge), Form Factor (Half-height Blades, Full-height Blades, and Quarter-height/Micro-blades), and Application/Workload (Virtualization and Private Cloud, High-Performance Computing (HPC), Artificial Intelligence/Machine Learning and Data Analytics, Storage-centric, and Edge/IoT Gateways). The Market Forecasts are Provided in Terms of Value (USD).

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| Half-height Blades |

| Full-height Blades |

| Quarter-height / Micro-blades |

| Virtualisation and Private Cloud |

| High-Performance Computing (HPC) |

| Artificial Intelligence/Machine Learning and Data Analytics |

| Storage-centric |

| Edge / IoT Gateways |

| By Tier Type | Tier 1 and 2 |

| Tier 3 | |

| Tier 4 | |

| By Data Center Size | Small Data Center |

| Medium Data Center | |

| Large Data Center | |

| Hyperscale Data Center | |

| By Data Center Type | Colocation Data Center |

| Hyperscalers Data Center/CSPs | |

| Enterprise and Edge Data Center | |

| By Form Factor | Half-height Blades |

| Full-height Blades | |

| Quarter-height / Micro-blades | |

| By Application / Workload | Virtualisation and Private Cloud |

| High-Performance Computing (HPC) | |

| Artificial Intelligence/Machine Learning and Data Analytics | |

| Storage-centric | |

| Edge / IoT Gateways |

Key Questions Answered in the Report

What is the forecast value of the Brazil data center server market in 2031?

The sector is projected to reach USD 4.44 billion by 2031.

Which tier classification is growing fastest?

Tier 4 facilities are advancing at a 6.15% CAGR through 2031 on rising mission-critical AI workloads.

How dominant are hyperscale campuses today?

Hyperscale sites captured 59.94% of 2025 revenue and are expanding at 6.35% CAGR on sovereign-cloud and AI demand.

Why are GPU-as-a-service models emerging?

High import tariffs and currency swings make pay-per-use GPU access attractive for enterprises that cannot absorb large capital outlays.

Which server form factor will gain most from 5G rollouts?

Quarter-height and micro-blade servers will see the fastest uptake as edge nodes proliferate at cell-site aggregation points.

How strict are Brazil’s data-protection rules?

ANPD mandates 24-hour breach notification and tight cross-border transfer controls, driving hybrid-cloud and sovereign-compute adoption.

Page last updated on: