Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

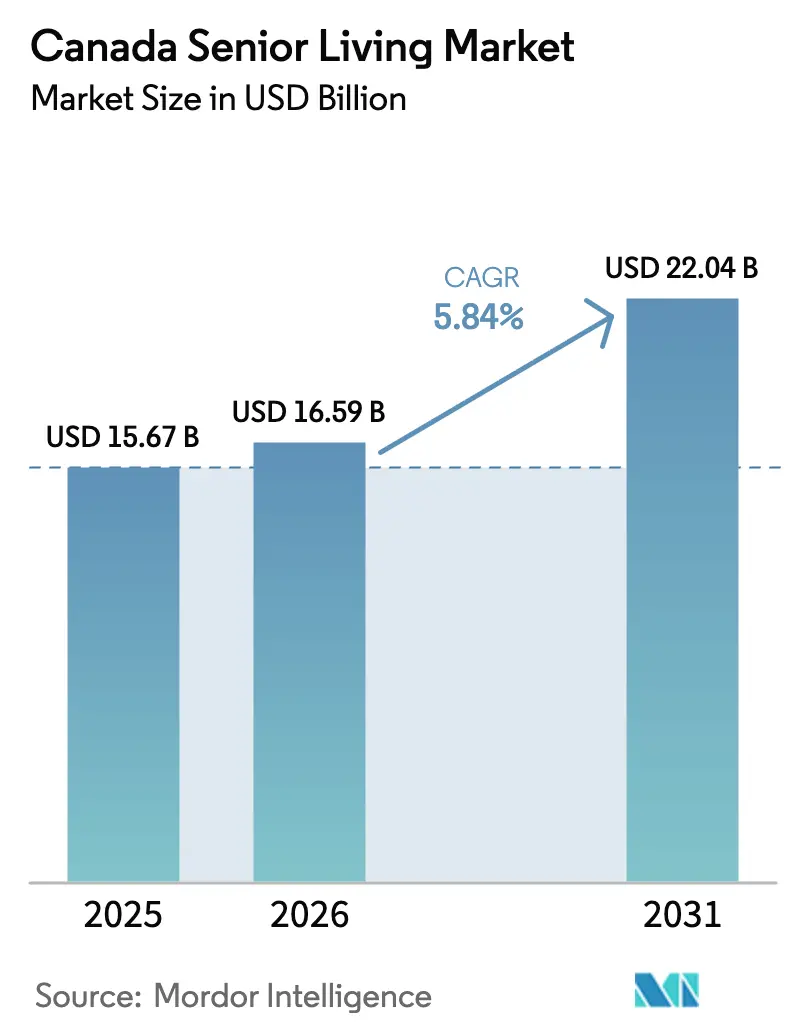

| Base Year Market Size (2025) | USD 15.67 Billion |

| Market Size (2026) | USD 16.59 Billion |

| Market Size (2031) | USD 22.04 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

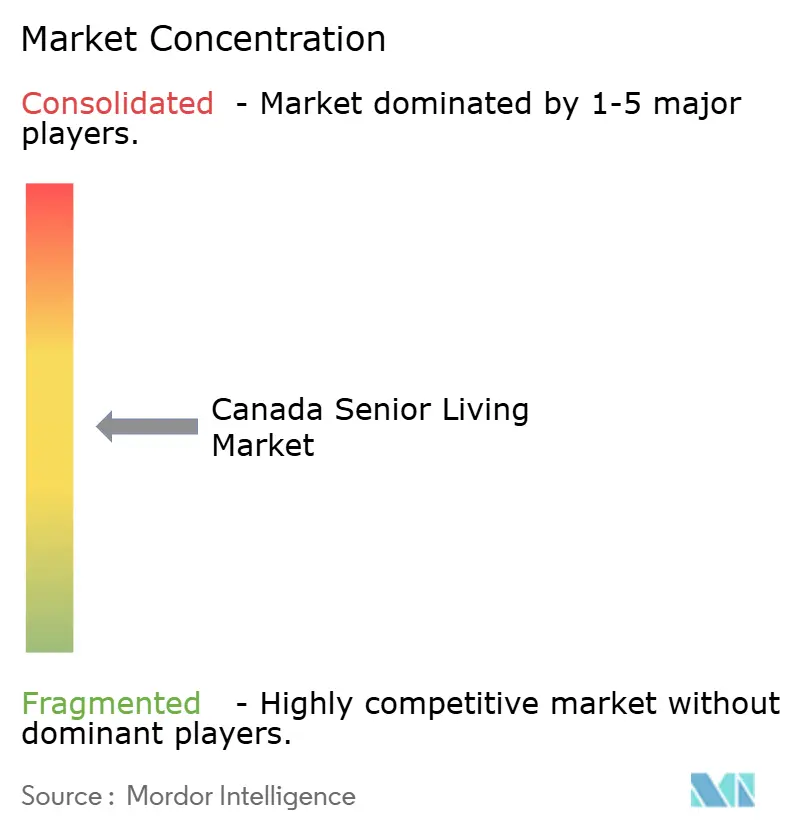

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Senior Living Market Analysis by Mordor Intelligence

The Canada Senior Living Market size was valued at USD 15.67 billion in 2025 and estimated to grow from USD 16.59 billion in 2026 to reach USD 22.04 billion by 2031, at a CAGR of 5.84% during the forecast period (2026-2031). Demand is propelled by the rapid expansion of the 85-plus cohort, growing hospital discharge backlogs, and the preference of affluent baby boomers for purpose-built communities that integrate health care, hospitality, and social programming. The accelerating shift away from single-family homes toward service-rich, age-in-place residences is deepening penetration rates in urban cores. Meanwhile, operators are grappling with an acute labor shortage—35,000 nursing vacancies nationwide—and rising wage pressure even as occupancy recovers to pre-pandemic levels. Capital continues to flow into the Canada senior living market from REITs and infrastructure funds, with technology-enabled care models and sustainability retrofits emerging as critical differentiators.

Key Report Takeaways

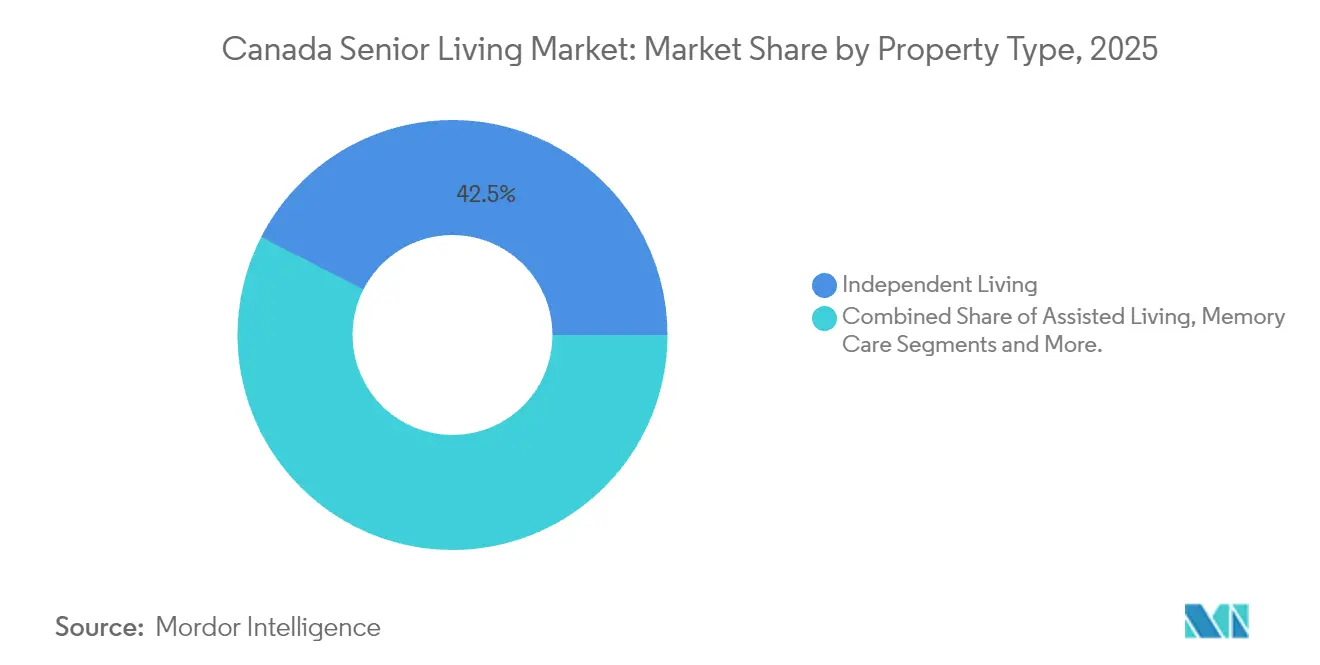

- By property type, Independent Living led with 42.46% of Canada's senior living market share in 2025, while Memory Care is advancing at a 6.33% CAGR through 2031.

- By business model, Long-Lease/Rental commanded 79.28% share of the Canada senior living market size in 2025; Hybrid (Sale + Lease) is growing fastest at 6.55% CAGR.

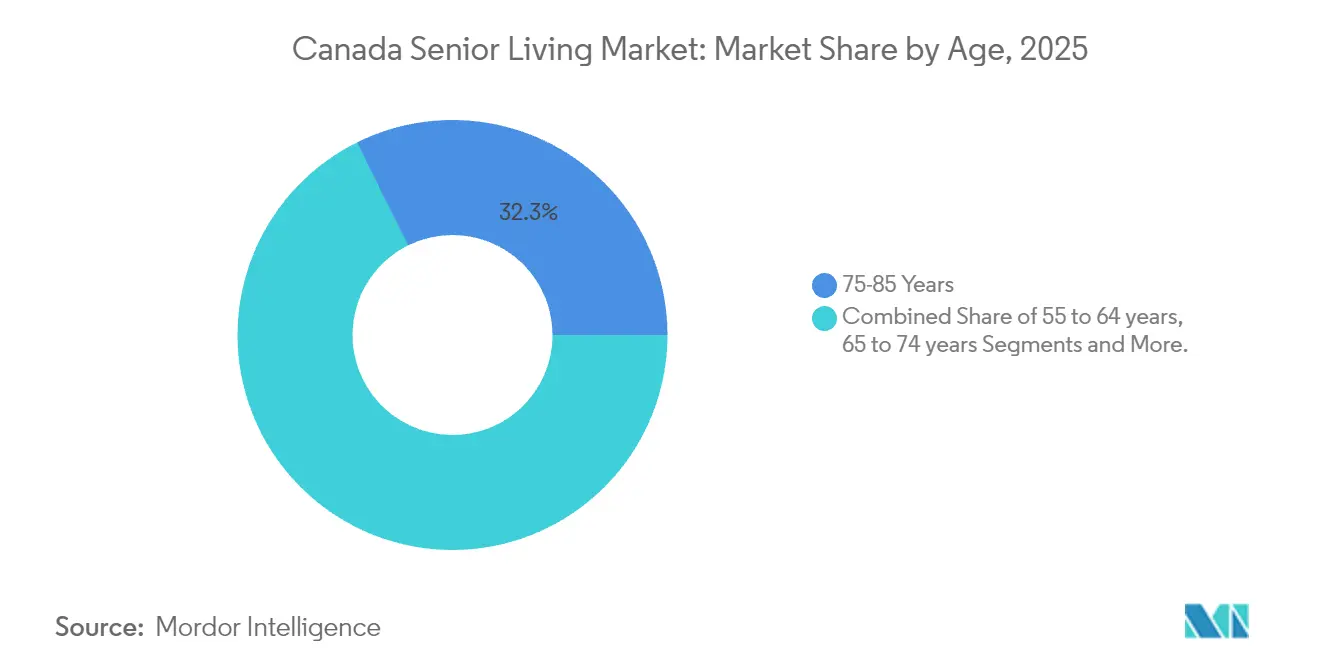

- By age, the 75-85 cohort accounted for 32.32% of demand in 2025, whereas the above-85 bracket is expanding at a 6.74% CAGR.

- By province, Ontario held a 45.02% share in 2025, yet British Columbia is the fastest-growing geography at 6.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Senior Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid aging of the 75–85+ cohort boosting demand for independent, assisted, and memory care | +1.8% | National; strongest in Ontario and British Columbia | Long term (≥ 4 years) |

| High household wealth among Boomers enabling private-pay options and premium amenities | +1.2% | National; peaks in Vancouver and GTA | Medium term (2–4 years) |

| Shift from single-family homes to service-rich, age-in-place communities near healthcare and transit | +0.9% | Toronto, Vancouver, Montreal, Calgary | Medium term (2–4 years) |

| Hospital and home-care capacity pressure driving referrals toward seniors housing | +0.7% | National; acute in Ontario and Quebec | Short term (≤ 2 years) |

| Technology-enabled care improving outcomes and operating efficiency | +0.5% | National; early adoption in British Columbia and Ontario | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Aging of the 75–85+ Cohort Boosting Demand for Independent, Assisted, and Memory Care

The 85-plus population is set to triple by 2073, creating a long runway of need for housing that can scale care intensity. Residents over 80 present higher rates of chronic disease, mobility limits, and dementia, shifting demand toward assisted living and memory care. Operators have responded by allocating more capital to high-acuity suites and by embedding nursing partnerships to manage complex clinical profiles. Sustained demographic momentum shields the Canada senior living market from cyclical swings and underpins development pipelines. Staffing strategy now centers on building nurse pipelines before rising acuity outpaces available labor.

High Household Wealth Among Boomers Enabling Private-Pay Options and Premium Amenities

Seniors control 61% of national household wealth, with a median senior family net worth of USD 806,000, supporting a willingness to pay for upscale communities. Luxury operators such as Amica achieve occupancy above 90% by bundling chef-driven dining, wellness clinics, and concierge services. The wealth effect is most pronounced in Greater Vancouver and the GTA, where home equity unlocks liquidity to fund entry fees. Regional disparities persist, leaving Atlantic markets underserved. Investors view high-net-worth segments as insulated from pricing pushback, reinforcing a two-tier supply pattern across the Canada senior living market.

Shift from Single-Family Homes to Service-Rich, Age-in-Place Communities Near Healthcare and Transit

Urban land shortages and escalating home upkeep costs are persuading retirees to trade detached houses for purpose-built towers situated near hospitals and transit nodes. Verve’s Don Mills Residence in Toronto, featuring integrated medical suites and smart-building systems, reached stabilized occupancy in record time. Co-located health services lower emergency readmissions and reduce caregiver burden, bolstering public-sector referrals. CMHC-insured 50-year debt at sub-4% rates further encourages rental formats that promise long-term tenure. The locational premium has become a decisive factor in lease-up velocity across the Canada senior living market.

Hospital and Home-Care Capacity Pressure Driving Referrals Toward Seniors Housing and Transitional Care Models

Emergency rooms are running at 120-140% capacity, with 92% of alternate-level-of-care patients aged 55 plus[1]Canadian Institute for Health Information, “Alternate Level of Care in Canada,” cihi.ca. Provinces now fund transitional beds inside private retirement residences to alleviate hospital gridlock. Extendicare opened 448 long-term care beds through such partnerships in 2024-25. Discharge planners are embedded in hospitals to route patients directly to licensed communities, creating a predictable referral funnel. Operators that integrate electronic medical records and 24/7 nursing capture higher per diems and strengthen payer relationships, enhancing the resilience of the Canada senior living market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordability gaps and limited middle-market product in high-cost provinces | −0.5% | British Columbia, Ontario urban cores, Alberta | Medium term (2–4 years) |

| Acute staffing shortages and rising wages for nurses/PSWs squeezing margins and service levels | −0.6% | National; most severe in Quebec and Atlantic provinces | Short term (≤ 2 years) |

| Complex, province-by-province regulations and licensing slowing approvals and expansion | −0.4% | National; acute in Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Affordability Gaps and Limited Middle-Market Product in High-Cost Provinces

Monthly assisted-living fees range from USD 2,565 to USD 4,030, a level 40% of older Canadians cannot meet without selling assets or leaning on relatives[2]Canada Mortgage and Housing Corporation, “Housing Market Insights,” cmhc-schl.gc.ca. Land prices, construction inflation, and municipal charges push new rents even higher in Vancouver and Toronto, widening the divide between luxury towers and subsidized nursing beds. Households earning USD 36,650 to USD 58,640 fall into an underserved “middle” that finds few purpose-built options. Quebec’s private RPA model proves that scale can trim costs—average rates sit near USD 2,418—yet even this level excludes the two lowest income quintiles. Operators must cut unit sizes, share amenities, or partner with provinces on rent supplements to unlock this latent demand.

Acute Staffing Shortages and Rising Wages for Nurses/PSWs Squeezing Margins and Service Levels

Canada is short 35,000 nurses, and one in five plans to leave the profession, driving heavy reliance on agency labor at a 30–50% markup. Personal support workers earn only USD 13.20-16.10 an hour, making it hard to compete with retail and hospitality wages. Staffing gaps curb service quality and force some homes to cap new admissions despite healthy demand. Rural and Atlantic markets struggle most as caregivers migrate to higher-pay urban centers. Operators are trying wage bumps, retention bonuses, and college partnerships, but results will take up to two years to materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Independent Living Dominates, Memory Care Accelerates

Independent Living captured 42.46% of Canada's senior living market share in 2025, underscoring its role as the entry point for the young-old segment. Suites emphasize social engagement, dining choice, and wellness, allowing operators to run lean clinical staffing. Memory Care, however, is the growth engine, advancing at a 6.33% CAGR through 2031 as dementia prevalence climbs and families pursue specialized settings. Sienna’s USD 880 million purchase of Aspira’s portfolio signaled the premium investors assign to higher-acuity models. Average monthly fees in dedicated memory wings reach USD 4,398–5,864, out-earning independent units by 40-60%.

Developers now favor continuum-of-care sites that combine independent, assisted, and memory options under one roof, boosting lifetime value and retention. Verve’s Don Mills community exemplifies this vertical integration, housing 94 independent suites, 23 assisted units, and 17 secure memory beds. By 2031, multi-level campuses are expected to supply more than half of the new beds in the Canada senior living market. Nursing Care, while heavily regulated, benefits from provincial capacity mandates; Extendicare’s pipeline illustrates the public-private alignment needed to expand long-term care inventory.

By Business Model: Rental Remains Pre-eminent, Hybrid Gains Momentum

Long-Lease/Rental communities controlled 79.28% of the Canada senior living market size in 2025, reflecting consistent CMHC financing and resident preference for liquidity. The structure permits operators to refresh service packages and adjust rents without resale complications. Hybrid Sale + Lease formats, though smaller, are advancing at a 6.55% CAGR as wealthy downsizers seek to preserve equity while accessing care. Fengate’s acquisition of Arbutus Walk and Wesbrook Village, totaling 88 condo and 295 rental suites, illustrates investor belief in mixed-tenure yield stacking.

Hybrid contracts commonly offer residents a 50–70% refundable life-lease stake, balancing estate planning with monthly fee flexibility. Regulatory complexity is higher—life-lease deals can fall under securities law—limiting adoption to sophisticated developers. Outright sale remains niche at under 5% share due to illiquidity concerns. Over the forecast horizon, the hybrid model is expected to widen geographic reach, particularly in Greater Vancouver, where average home sale proceeds exceed USD 732,600, supplying capital for entry fees.

By Age: 75-85 Holds the Crown, Above 85 Explodes

The 75-85 cohort represented 32.32% of residents in 2025, confirming its status as the largest customer block. Individuals in this bracket often transition from independent to assisted living as mobility declines, supplying a pipeline to higher-acuity units. The above-85 segment is the fastest-growing, charting a 6.74% CAGR through 2031 on the back of longer life expectancy and increased frailty. Lease-up velocity in memory wings mirrors this demographic surge, with some Vancouver and Toronto communities posting six-month wait lists.

Operators now craft marketing aimed at adult children, who typically drive decisions for parents over 85. Lifetime value is substantial: an early-seventies entrant who ages in place across care levels may generate USD 1–2 million in cumulative revenue. The 65-74 band remains an emerging niche, generally attracted to lifestyle-led campuses with preventive health programming. Active-adult villages targeting the 55-64 group continue to supply a feeder channel into the broader Canada senior living market, but volume remains comparatively small.

Geography Analysis

Ontario retained the lion’s share at 45.02% in 2025, reflecting its 14.8 million residents and a mature licensing regime under the Retirement Homes Act 2010. Leading chains locate flagship campuses near Toronto teaching hospitals, benefiting from deep nurse pools and transit links. Nevertheless, land scarcity and development fees are moderating growth, pushing developers toward secondary markets such as London and Kingston, where Extendicare recently added 448 long-term care beds through public-private partnerships.

British Columbia is the pacesetter, expanding at a 6.98% CAGR as Vancouver’s USD 732,600 median home value frees equity for entry fees and REIT capital targets limited high-density supply. Welltower’s USD 3.4 billion acquisition of Amica emphasized coastal luxury, while Fengate’s hybrid projects underscore investor appetite for mixed tenure. The province’s Green Buildings mandate accelerates heat-pump retrofits, raising capex but unlocking CMHC-backed debt at favorable terms.

Quebec’s 1,449 private RPAs deliver more affordable monthly rates of USD 2,418 but impose bilingual staffing and MSSS certification, deterring some anglophone entrants. Incumbents such as Cogir achieve economies of scale via standardized 300-plus suite towers outside Montreal’s core. Alberta benefits from lower land costs and energy wealth, yet trails British Columbia in growth due to its smaller population base. Atlantic provinces and the Prairies remain underserved; operators prepared to settle for slimmer margins and partner with provincial authorities can tap latent demand in these regions of the Canada senior living market.

Competitive Landscape

Competition is moderate, with the top three operators—Chartwell, Sienna, and Revera—controlling roughly one-third of national beds. Scale enables preferred lender terms, centralized procurement, and national staffing pipelines. Nonetheless, the field remains open: more than half of properties are owned by regional chains, nonprofits, or single-site operators, creating room for roll-ups. Technology investment is a key separator; chains deploying EMR and remote monitoring gain operating leverage and stronger payer relations.

Institutional capital is reshaping ownership. Welltower’s USD 3.4 billion Amica takeover positions the REIT as the premium urban landlord, layering in management fees while securing luxury exposure. Sienna’s USD 880 million Aspira purchase highlights a strategic focus on dementia care that commands higher per diems and exhibits lower turnover. Extendicare’s revenue rose 11.8% in Q4 2024 as newly built public-funded beds came online, illustrating how clinical expertise and government partnerships can offset exposure to private-pay volatility.

Smaller independents compete by targeting cultural niches—Mandarin-speaking or South Asian communities—and by planting flags in secondary cities where conglomerates lack local knowledge. Sustainability retrofits and modular construction are emerging as cost-control levers, especially for mid-market entrants. Consolidation momentum is expected to quicken as succession-ready owners exit and REIT cost of capital stays low, reinforcing a gradual uptick in concentration across the Canada senior living market.

Canada Senior Living Industry Leaders

Chartwell Retirement Residences

Sienna Senior Living

Revera Inc.

Extendicare Inc.

Atria Senior Living

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Welltower Inc. agreed to acquire Amica Senior Lifestyles from Ontario Teachers' Pension Plan for CAD 4.6 billion (USD 3.4 billion), including 38 operating luxury senior residences and 9 development parcels across British Columbia and Ontario. As part of the transaction, Welltower will acquire a minority interest in Amica's management company, with Amica's management team retaining majority ownership of the manager. The deal, expected to close in Q4 2025, positions Welltower to capitalize on rapidly growing demand and limited new supply in Canada's premium senior housing segment.

- February 2025: Fengate Asset Management acquired two British Columbia senior living properties, Arbutus Walk and Wesbrook Village, from Seasons Retirement Communities, totaling 295 rental suites and 88 condominium suites. The transaction reflects continued investor appetite for purpose-built rental and hybrid ownership models in high-wealth, land-constrained markets.

- June 2024: Revera Inc. sold its 15% interest in 25 long-term care homes to Extendicare Inc., marking Revera's strategic exit from long-term care ownership to focus on retirement living and assisted living. The transaction underscores the sector's bifurcation, with operators choosing to specialize in either hospitality-driven retirement living or clinically intensive long-term care.

- April 2024: Chartwell Retirement Residences closed Heritage Glen in Mississauga, Ontario, displacing approximately 200 residents due to persistently low occupancy and operating losses. The closure highlights the sector's vulnerability to oversupply in specific micro-markets and the challenges of maintaining service levels amid staffing shortages.

Canada Senior Living Market Report Scope

Senior living is a concept that refers to a variety of housing and lifestyle options for senior citizens that are adapted to the challenges of aging, such as limited mobility and susceptibility to illness. The Canada Senior Living Market is Segmented by Province (Alberta, Nova Scotia, Quebec, British Columbia, Ontario, and the Rest of Canada). The report also covers the impact of COVID-19 on the market. The report offers the market size in value terms in USD for all the abovementioned segments.

By Property Type

| Assisted Living |

| Independent Living |

| Memory Care |

| Nursing Care |

By Business Model

| Outright Sale (Freehold) |

| Long-Lease / Rental |

| Hybrid (Sale + Lease) |

By Age

| 55 to 64 years |

| 65 to 74 years |

| 75 to 85 years |

| Above 85 years |

By Province

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Property Type | Assisted Living |

| Independent Living | |

| Memory Care | |

| Nursing Care | |

| By Business Model | Outright Sale (Freehold) |

| Long-Lease / Rental | |

| Hybrid (Sale + Lease) | |

| By Age | 55 to 64 years |

| 65 to 74 years | |

| 75 to 85 years | |

| Above 85 years | |

| By Province | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

How large is the Canada senior living market in 2026?

The Canada senior living market size is USD 16.59 billion in 2026, with a projected value of USD 22.04 billion by 2031.

What is driving the fastest growth in Canada’s senior living property types?

Memory Care is leading growth at a 6.33% CAGR as dementia prevalence rises and operators seek higher-margin, high-acuity offerings.

Which province shows the strongest growth prospects?

British Columbia is advancing at a 6.98% CAGR to 2031, buoyed by high household wealth and aggressive REIT investment.

How are staffing shortages affecting operators?

Nursing and PSW vacancies inflate agency labor costs by up to 50%, squeezing margins and compelling greater use of technology-enabled care.

What strategic moves are reshaping market ownership?

Welltower’s USD 3.4 billion acquisition of Amica and Sienna’s USD 880 million memory-care purchase highlight REIT-driven consolidation toward premium and high-acuity assets.

Page last updated on: