Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

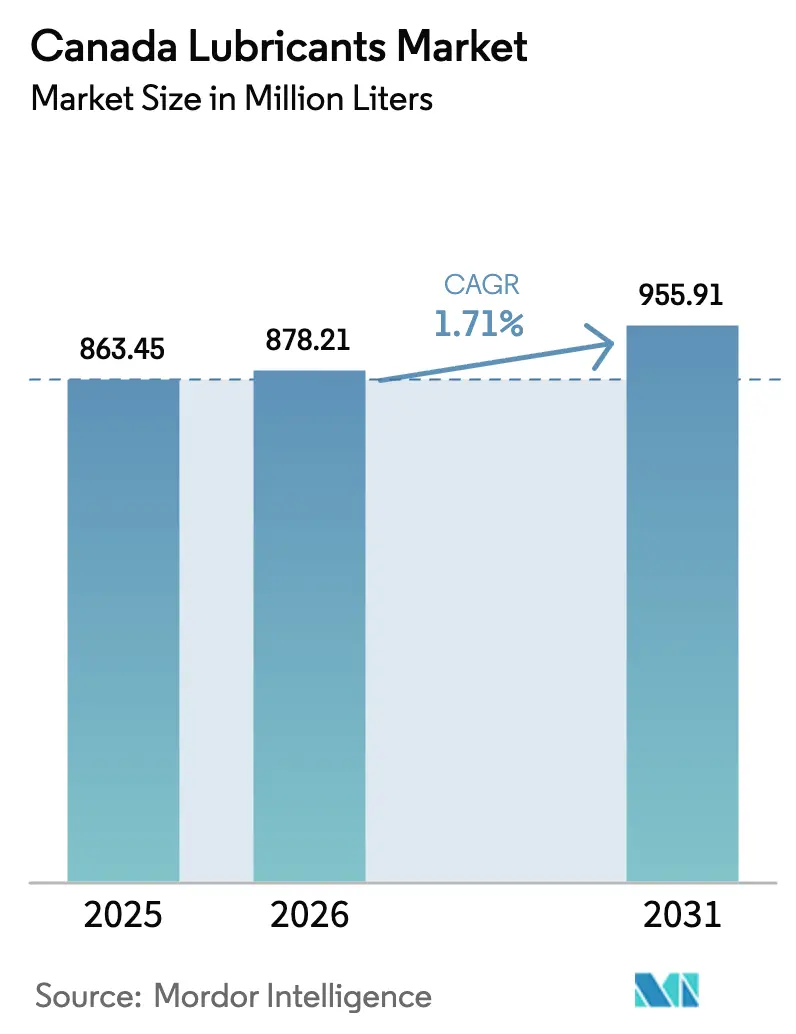

| Base Year Market Size (2025) | 863.45 Million liters |

| Market Volume (2026) | 878.21 Million liters |

| Market Volume (2031) | 955.91 Million liters |

| Growth Rate (2026 - 2031) | 1.71% CAGR |

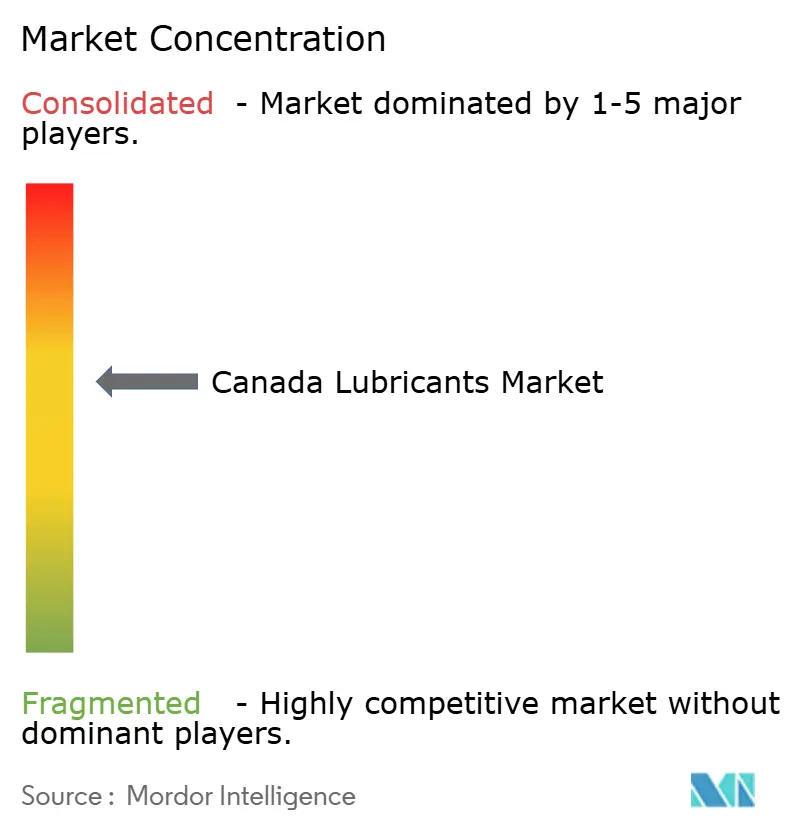

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Lubricants Market Analysis by Mordor Intelligence

The Canada Lubricants Market size is expected to increase from 863.45 Million liters in 2025 to 878.21 Million liters in 2026 and reach 955.91 Million liters by 2031, growing at a CAGR of 1.71% over 2026-2031. Extended drain intervals and the increasing penetration of electric vehicles are moderating volume growth in the Canada lubricants market. However, demand remains supported by high-performance synthetic lubricants, oil-sands maintenance activities, and bio-based policy incentives. Projects such as Cenovus Energy’s Foster Creek expansion and Canadian Natural Resources Limited’s multi-year capacity additions are driving the consumption of hydraulic fluids and gear oils. Additionally, Ontario’s automotive assembly plants and Quebec’s stricter emissions regulations are fostering a shift toward ultra-low-viscosity formulations, which offer higher profit margins. While Alberta’s energy corridor continues to serve as the primary volume driver, emerging opportunities in Northwest Passage shipping and federal green-procurement initiatives are creating niche growth areas, contributing to a gradual upward trend in the Canada lubricants market.

Key Report Takeaways

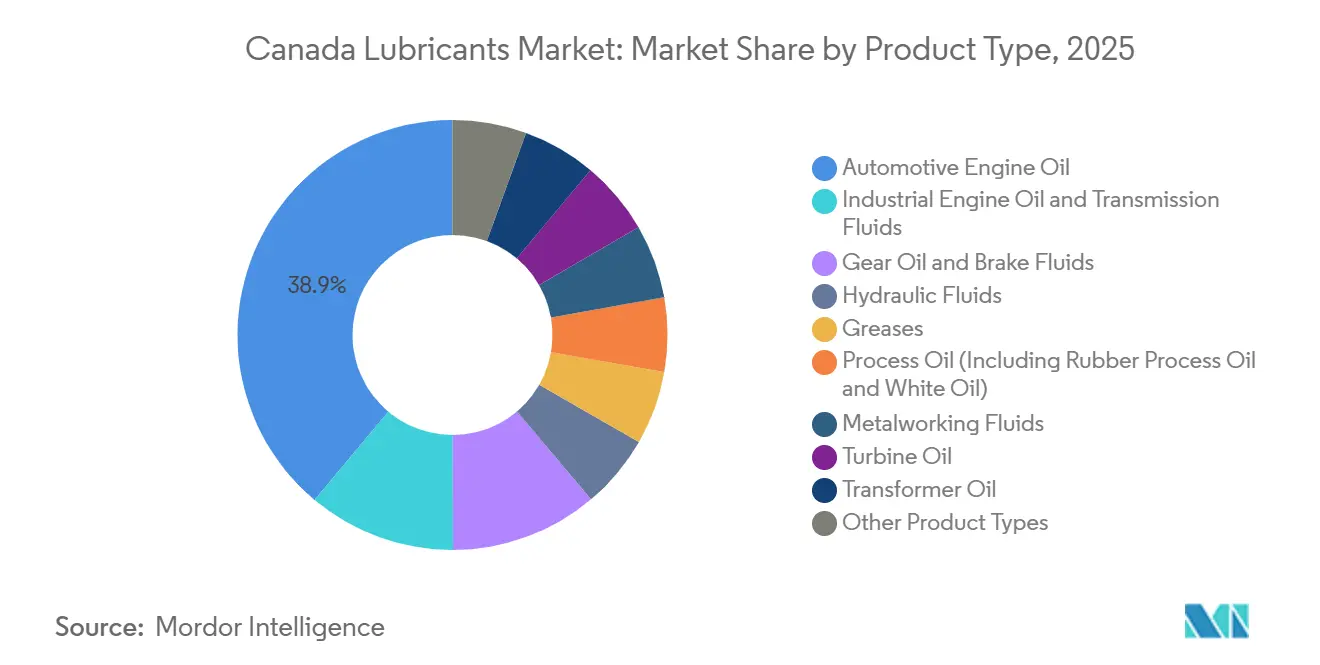

- By product type, automotive engine oil led with 38.92% of the Canada lubricants market share in 2025, while industrial engine oil is forecast to expand at a 2.21% CAGR through 2031.

- By base stock type, mineral oil-based lubricants accounted for 58.32% of the Canada lubricants market share in 2025, while bio-based lubricants are projected to advance at a 5.11% CAGR through 2031.

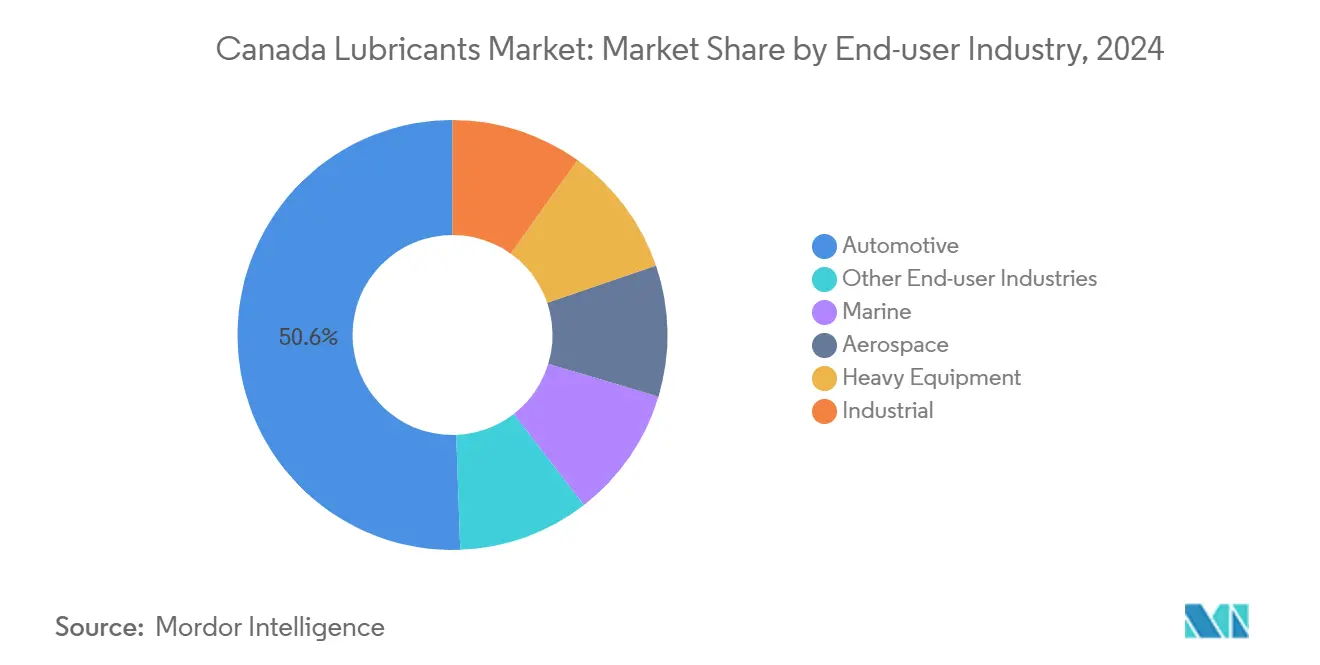

- By end-user industry, automotive retained 50.58% of the Canada lubricants market share in 2025; Marine is set to record a 3.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM-mandated ultra-low-viscosity oils | +0.4% | National, concentrated in Ontario and Quebec automotive hubs | Medium term (2-4 years) |

| Growing sales of motor vehicles | +0.3% | National, with strength in Alberta and British Columbia | Short term (≤ 2 years) |

| Expansion of mining and oil-sands operations | +0.5% | Alberta and Saskatchewan, spillover to British Columbia | Long term (≥ 4 years) |

| Shift toward high-performance synthetic lubricants | +0.3% | National, early adoption in premium automotive and industrial segments | Medium term (2-4 years) |

| Government clean-tech procurement incentives | +0.2% | National, with concentration in Ontario and Quebec manufacturing corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM-Mandated Ultra-Low-Viscosity Oils

Automakers have shifted to 0W-16 and 0W-8 grades to adhere to stricter CAFE regulations, increasing the demand for Group III and PAO in the Canada lubricants market. Toyota and Honda have adopted 0W-16 for most 2024-2026 models sold domestically. Furthermore, ILSAC’s draft GF-8A standard, introduced in 2025, sets oxidation-stability and wear-protection requirements that mineral blends find challenging to meet. Imperial Oil’s 2026 Strathcona turnaround has boosted Group III output, offering integrated majors a cost advantage as local blenders adjust to these changes. The shift in viscosity grades has reduced product life cycles, favoring suppliers with flexible R&D teams capable of quickly recertifying formulations in the Canada lubricants market.

Growing Sales of Motor Vehicles

Light-vehicle registrations recovered to 1.92 million units in 2024, although the 2026 SAAR has stabilized around 1.69 million as interest rates have leveled off. EV penetration fell below 9% in early 2026 after federal rebates expired, preceding the relaunch of the EV Affordability Program. Each battery electric vehicle (BEV) reduces annual engine oil consumption by approximately 4-5 liters. However, increasing fleet and commercial vehicle registrations have helped sustain overall lubricant demand, maintaining baseline volumes in the Canada lubricants market.

Expansion of Mining and Oil-Sands Operations

Cenovus Energy’s 30,000 bpd Foster Creek expansion and Canadian Natural Resources Limited’s 340,000 bpd growth roadmap are driving ongoing demand for Arctic-grade hydraulic fluids and high-temperature SAGD gear oils. Suncor has forecasted refinery throughput of 460,000-475,000 bpd at over 99% utilization for 2026, supporting consistent demand for process oils and greases. Long lead times and capital expenditure commitments ensure stable multi-year demand, providing industrial suppliers with a reliable outlook in the Canada lubricants market.

Shift Toward High-Performance Synthetic Lubricants

TotalEnergies announced in May 2025 its commitment to transition its Canadian product range to 100% synthetic within three years, reflecting a broader industry trend toward longer-lasting, low-volatility fluids. Chevron’s introduction of NEXBASE 4 XP Group III+ in March 2025 has provided domestic feedstock, reducing dependency on imports and improving margins for local blenders[1]Chevron, “NEXBASE 4 XP Product Launch,” chevron.ca. Extended drain intervals have effectively doubled service life for heavy-duty fleets, mitigating higher per-liter costs and increasing the adoption of synthetic lubricants in the Canada lubricants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening PFAS and ZDDP regulations | -0.3% | National, with Quebec enforcing stricter provincial standards | Medium term (2-4 years) |

| OEM long-drain service intervals | -0.2% | National, concentrated in commercial vehicle and fleet segments | Short term (≤ 2 years) |

| Rapid rise of sealed-for-life EV drivetrains | -0.5% | National, concentrated in urban centers (Toronto, Vancouver, Montreal) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening PFAS and ZDDP Regulations

Environment and Climate Change Canada’s Prohibition of Certain Toxic Substances Regulations 2025 will prohibit PFAS-containing lubricants starting June 30, 2026, requiring the reformulation of greases and hydraulic fluids[2]Environment and Climate Change Canada, “Prohibition of Certain Toxic Substances Regulations 2025,” canada.ca. At the same time, API PC-12 introduces stricter phosphorus limits, impacting ZDDP usage and increasing costs for redesigning additive packages. Compliance is expected to raise raw material costs by 10-15%, squeezing profit margins for smaller blenders in the Canada lubricants market.

Rapid Rise of Sealed-for-Life EV Drivetrains

Battery-electric vehicles are replacing multi-fluid internal combustion engine (ICE) systems with 1-2 liters of long-life EDU coolant. Petro-Canada’s EVR line and TotalEnergies’ Quartz EV-Drive R 3.1 cater to this niche, but revenue per vehicle is anticipated to drop by 40-50%. Federal goals for 100% zero-emission vehicle sales by 2035 could reduce the Canada lubricants market by 60-80 million liters by the early 2030s, particularly in urban areas where adoption is advancing most rapidly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Oils Outpace Automotive

Automotive engine oil held 38.92% of the Canada lubricants market share in 2025, reflecting its established dominance in passenger and light-commercial vehicles. Industrial engine oil, however, is expected to grow at a CAGR of 2.21% through 2031, supported by the addition of natural-gas turbines and remote mining gensets requiring stationary-engine lubrication. Transmission and Gear Oils face challenges due to CVTs using lower fill volumes and extended drain intervals. Hydraulic Fluids and Greases benefit from maintenance cycles in oil sands and infrastructure investments, while PFAS bans are driving innovation in additives. Metalworking Fluids support Ontario’s machining industry, and Turbine Oils cater to grid-stability upgrades across the country.

Conversely, margin compression in ultra-low-viscosity Automotive Engine Oils is likely to continue as OEMs demand stricter specifications. Suppliers with broad portfolios can shift their focus to industrial and specialty niches to sustain profitability across the Canada lubricants market.

By Base Stock Type: Bio-Based Surge Amid Mineral Dominance

Mineral Oil-Based Lubricants accounted for 58.32% of the Canada lubricants market share in 2025, driven by cost advantages in high-volume segments. Bio-based lubricants are projected to grow at a CAGR of 5.11% through 2031, supported by federal clean-tech procurement initiatives and the availability of canola-oil feedstock. Synthetic grades are gaining traction due to OEM viscosity requirements and extended drain intervals.

Semi-synthetic, which bridge the gap between cost and performance, saw reduced demand as full synthetics become more competitively priced. TotalEnergies’ transition strategy reflects confidence that premium positioning will offset volume declines. Technical challenges such as oxidative stability and cold-flow properties continue to limit bio-based penetration in heavy-duty applications, but policy incentives under the Strategic Innovation Fund are gradually reducing the dominance of mineral oil-based lubricants in the Canada market.

By End-user Industry: Marine Leads, Automotive Holds

Automotive retained 50.58% of the Canada lubricants market share in 2025, supported by 26 million registered vehicles. Commercial trucks, which consume three to four times more lubricant per unit than passenger cars, help sustain volumes despite a slowdown in retail sales. Marine, however, is expected to grow at a CAGR of 3.12% through 2031 as Northwest Passage shipping lanes and IMO sulfur regulations drive demand for low-temperature cylinder oils and sterntube greases.

Heavy Equipment, including construction, mining, and agriculture, relies on hydraulic oils capable of functioning in temperatures ranging from -40°C winters to +35°C summers. Industrial users in power generation and metalworking continue to purchase process oils and turbine lubricants. Aerospace remains a high-margin niche where certification barriers support premium pricing. The Canada lubricants market thus splits between high-volume, mature automotive sales and faster-growing, lower-volume marine and industrial segments.

Geography Analysis

Regional disparities define the Canada lubricants market. Alberta accounts for 35-40% of industrial lubricant demand due to oil-sands operations, while Ontario and Quebec together drive nearly half of automotive lubricant consumption. Cenovus and Canadian Natural Resources projects sustain demand for hydraulic fluid and gear oil in Alberta, while Ontario’s manufacturing sector and Quebec’s aerospace industry consume metalworking and turbine oils.

British Columbia’s forestry and mining sectors favor biodegradable hydraulic formulations to comply with provincial environmental regulations. Saskatchewan and Manitoba rely on tractor hydraulic and gear lubricants designed to withstand prairie temperature extremes, while Atlantic Canada’s fishing fleets and offshore rigs maintain a modest but specialized demand for marine lubricants.

The northern territories require Arctic-grade synthetic lubricants for mining and transportation, as mineral oils solidify at temperatures below -30°C. Cross-border logistics expose the market to currency fluctuations, but proximity to U.S. Gulf Coast base-oil imports helps stabilize feedstock supply. Provincial policy variations compel distributors to customize inventories, increasing working capital requirements and favoring larger players in the Canada lubricants market.

Competitive Landscape

Exxon Mobil, Petro-Canada Lubricants, Shell, Chevron, and BP collectively hold 66% of the Canada lubricants market in 2025 through integrated refinery, blending, and retail operations. Imperial Oil’s 23% retail share and 50,000 bpd lubricant sales highlight the leverage of captive refining. Petro-Canada’s Mississauga facility blends 15,600 bpd but experienced a decline in segment income in 2025 due to base-oil price pressures.

Regional players such as Boss and KLONDIKE, along with specialty formulators like FUCHS and Valvoline, share the remaining 35-40% of the market by focusing on technical services and rapid delivery. TotalEnergies expanded its footprint through five distribution agreements in 2024-2025, while Catalys’ nationwide rebranding in May 2025 highlights the competitive advantage of agile logistics. Chevron’s domestic production of Group III+ base oils challenges import-dependent competitors by reducing feedstock costs.

Strategic divergence is evident: major players are streamlining product portfolios and emphasizing synthetic lubricants, while mid-sized companies target bio-based and EV fluid niches supported by federal incentives. Channel partnerships continue to redefine market reach, indicating that logistical flexibility will play a critical role in shaping future competition in the Canada lubricants market.

Canada Lubricants Industry Leaders

Exxon Mobil Corporation

Chevron Corporation

BP p.l.c.

Shell plc

Petro‐Canada Lubricants Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Petro‐Canada Lubricants Inc. assumed global management of the Suniso refrigeration lubricants brand, including overseeing global supply and stewardship for Suniso’s mineral and synthetic HVAC-R products. This development is expected to strengthen Petro-Canada's position in the lubricant market by expanding its product portfolio and global reach.

- March 2025: Petro‐Canada Lubricants Inc. updated its SUPREM line of engine oils with new formulations designed to meet the ILSAC GF-7 and API SQ (successor to API SP/SN Plus) specifications. These improved lubricants are tailored to meet the stringent requirements of modern passenger cars, SUVs, and light-duty trucks.

Canada Lubricants Market Report Scope

Lubricants are substances that, when applied as a coating between solid surfaces, reduce friction, heat, and wear. Lubricant products are made from a combination of base oils and additives. Lubricants are utilized to adjust the friction and wear of surfaces in contact with bodies that are moving relative to one another, lowering the heat released when the surfaces move. The composition of base oil in the formulation of lubricants is primarily between 75% and 90%.

The Canada lubricants market is segmented by product type, base stock type, and end-user industry. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the volume of the Canada lubricants market?

The Canada lubricants market stands at 878.21 million liters in 2026 and is forecast to reach 955.91 million liters by 2031.

How fast is demand growing in industrial engine oils through 2031?

Industrial engine oil is expected to post a 2.21% CAGR through 2031, the fastest among product types.

Which base-stock type is expanding the quickest through 2031?

Bio-based lubricants are forecast to grow at a 5.11% CAGR through 2031.

Why are ultra-low-viscosity oils important for suppliers?

0W-16 and 0W-8 grades mandated by OEMs require Group III or PAO base stocks, boosting synthetic penetration and margins.

Page last updated on: