Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.84 Billion |

| Market Size (2026) | USD 20.7 Billion |

| Market Size (2031) | USD 25.59 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

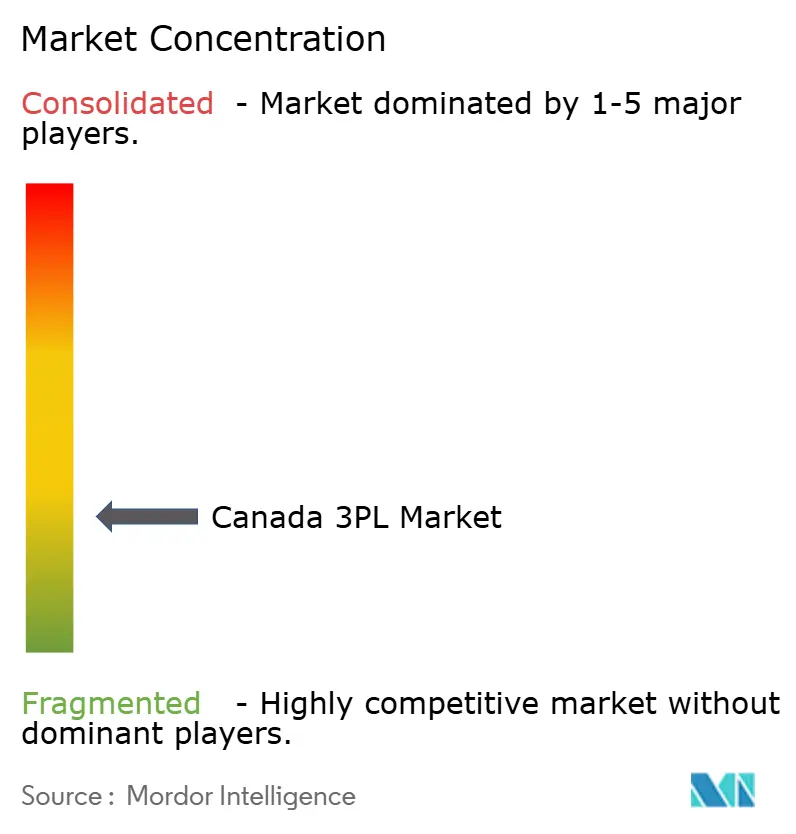

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada 3PL Market Analysis by Mordor Intelligence

The Canada 3PL Market size was valued at USD 19.84 billion in 2025 and estimated to grow from USD 20.7 billion in 2026 to reach USD 25.59 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031).

Robust cross-border trade under the Canada-United States-Mexico Agreement (CUSMA), fast-growing e-commerce fulfillment volumes, and technology-enabled capacity optimization are the strongest forces shaping the Canada Third-Party Logistics market. Regulatory reforms such as the Canada Border Services Agency’s CARM program and the federal elimination of fuel charges are lowering compliance complexity and transport costs, encouraging small and midsize shippers to outsource logistics functions. Meanwhile, specialized requirements around cold-chain distribution for pharmaceuticals, temperature-controlled battery components, and reverse logistics for recycling are steering providers toward higher-margin value-added services. Strategic mergers—including UPS’s USD 1.6 billion purchase of Andlauer Healthcare Group—signal that logistics operators capable of marrying domain expertise with digital execution are positioned to expand their share in the Canada Third-Party Logistics market.

Key Report Takeaways

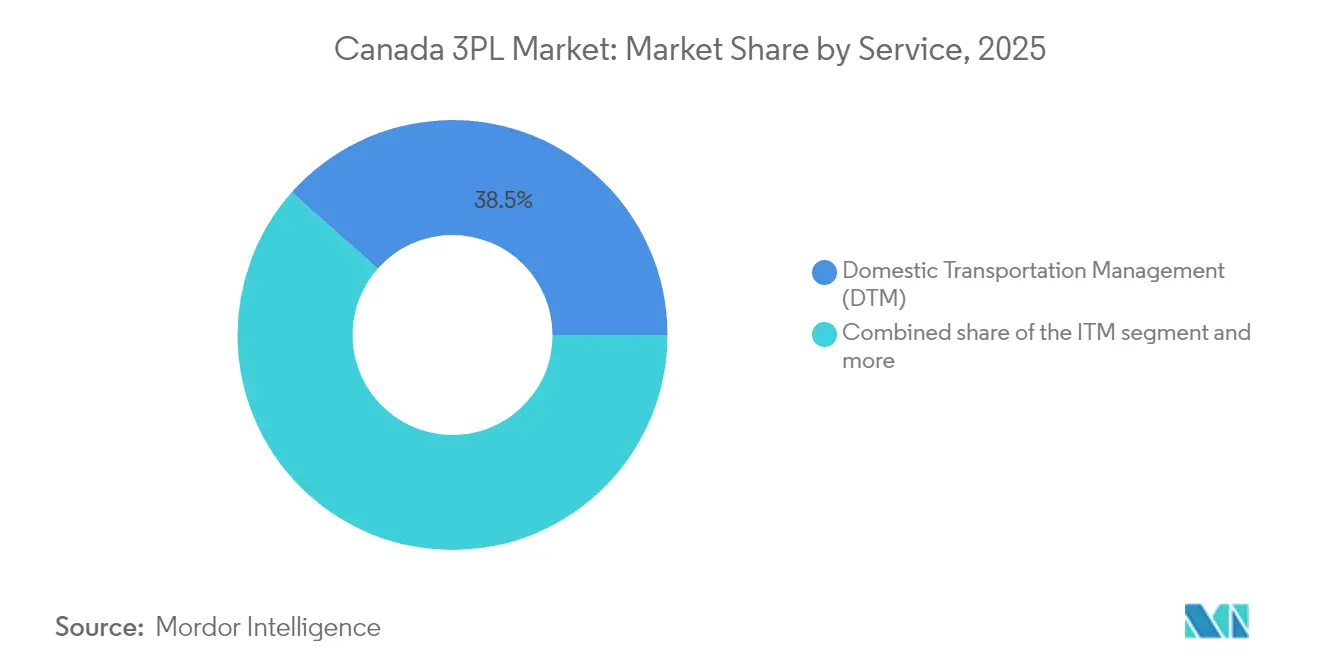

- By service, Domestic Transportation Management led with a 38.45% revenue share in 2025; Value-Added Warehousing & Distribution is projected to expand at a 7.06% CAGR through 2031.

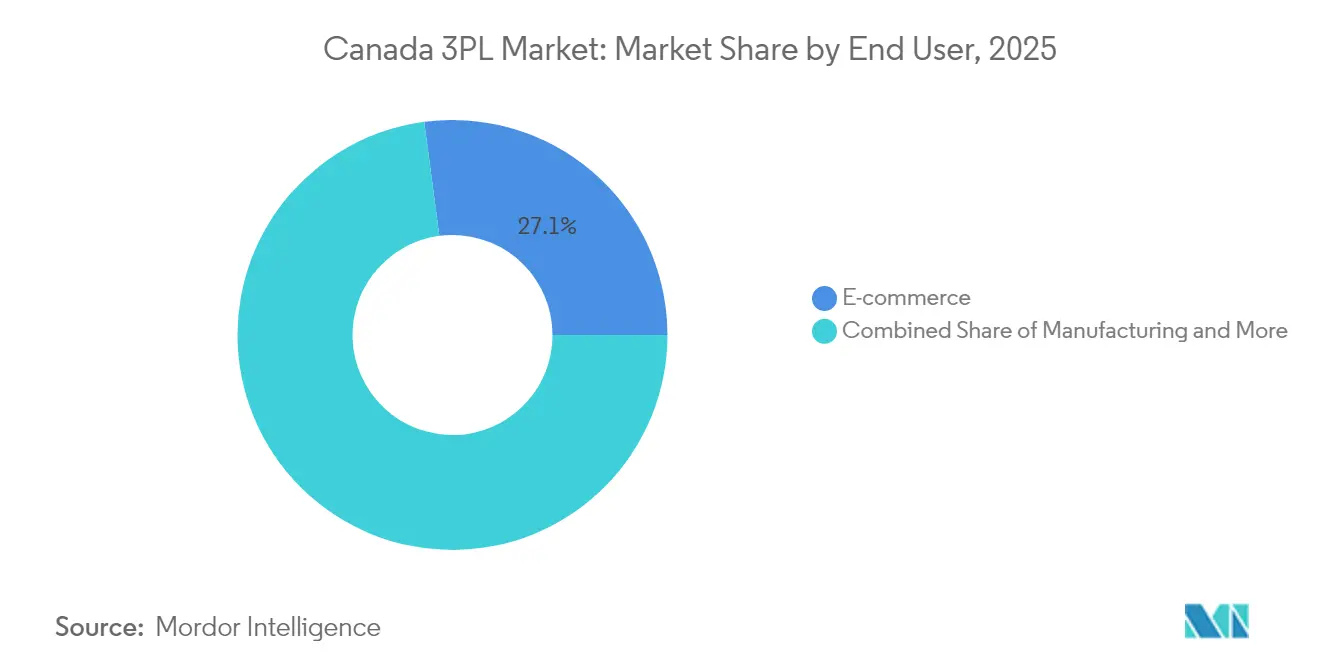

- By end user, E-commerce captured 27.10% of the Canada Third-Party Logistics market share in 2025 and is advancing at a 6.67% CAGR to 2031.

- By logistics model, Asset-Light operators held 50.55% share in 2025, whereas Hybrid providers are on track for a 6.76% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment boom post-Bill C-244 | +1.2% | National; Greater Toronto Area & Vancouver corridors | Medium term (2-4 years) |

| EV battery supply-chain localization push | +0.8% | Ontario & Quebec manufacturing hubs | Long term (≥4 years) |

| CUSMA-driven cross-border near-shoring | +0.9% | Ontario-Michigan border region | Medium term (2-4 years) |

| Inflation-linked distribution-center contracting (DCC) surge | +0.6% | National, cost-sensitive sectors | Short term (≤2 years) |

| AI-enabled freight-matching platforms | +0.4% | Large urban freight nodes | Long term (≥4 years) |

| Canada-wide carbon-pricing incentives | +0.3% | National, province-specific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

E-commerce Fulfillment Boom Post-Bill C-244

New carbon-pricing rules removed federal fuel surcharges on April 1, 2025, immediately easing last-mile delivery costs. During the Canada Post strike of December 2024, private 3PLs absorbed diverted parcel flows, proving their network agility. Warehouse vacancies climbed to 4.5% in 2024, supplying much-needed space near major cities. Federal grants totaling USD 75.8 million now subsidize electric trucks, encouraging sustainable urban deliveries. Collectively, these developments reinforce the Canada Third-Party Logistics market growth path by accelerating fulfillment outsourcing among merchants.

EV Battery Supply-Chain Localization Push

BloombergNEF ranked Canada the world leader in EV battery supply chains in 2024, spurring large investments. Siemens earmarked USD 150 million for Ontario R&D centers, while Volkswagen broke ground on a USD 7 billion gigafactory in St. Thomas. Rail speed improvements of 30% around Chicago facilitate U.S. component inflows. Handling lithium, cobalt, and nickel under strict safety rules calls for specialized 3PL expertise. The Canada Third-Party Logistics market thus benefits from high-value freight, tight delivery schedules, and reverse-logistics demand for battery recycling.

CUSMA-Driven Cross-Border Near-Shoring

Cross-border shipments averaged 6,000 per month in 2024 as manufacturers relocated production nearer to U.S. buyers. The October 2024 launch of CARM shifted customs security from brokers to importers, making compliance knowledge a critical differentiator. U.S.–Canada trade reached USD 782.4 billion in 2024, with imports rising 4.23%. 3PLs that can bundle brokerage, bonded warehousing, and just-in-time transport are winning new contracts. The Canada Third-Party Logistics market consequently gains depth by anchoring North American supply chains in Ontario and Quebec[1]Canada Border Services Agency, “CARM Release 2 Overview,” Canada Border Services Agency, cbsa-asfc.gc.ca.

Inflation-Linked DCC Outsourcing Surge

Persistent wage inflation—driver pay rose to USD 27.10 per hour by Q2 2024—erodes in-house fleet margins. Many manufacturers responded by converting private fleets into dedicated contracts with 3PLs. Providers secure multi-year agreements pegged to consumer-price index escalators, locking in revenue visibility. Shippers, in turn, shift asset-ownership risk while tapping network optimization technologies. As costs find equilibrium, the Canadian third-party Logistics market strengthens its annuity base.

Restraint Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver-shortage wage spiral | −0.7% | National; long-haul routes | Short term (≤2 years) |

| Rail-network congestion in Prairie provinces | −0.5% | Western grain & resource corridors | Medium term (2-4 years) |

| Warehousing land-use restrictions in the GTA | −0.3% | Greater Toronto Area | Long term (≥4 years) |

| Fragmented customs-brokerage IT standards | −0.4% | Major ports & border crossings | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Driver-Shortage Wage Spiral

Vacant trucking positions fell to 15,350 by Q2 2024, yet pay kept climbing. Safety legislation in British Columbia imposes penalties of up to USD 100,000 for overpass strikes, ratcheting carrier liability. Rising wages squeeze small haulers that feed larger 3PL networks. When operators exit, capacity tightens, raising spot rates and slowing the Canada Third-Party Logistics market expansion[2]Statistics Canada, “Job Vacancy and Wage Survey, Second Quarter 2024,” Statistics Canada, statcan.gc.ca.

Rail-Network Congestion in Prairie Provinces

An August 2024 shutdown of two national railways stalled USD 1 billion of daily trade. Winter grain exports have already dropped to 525,000 metric tons weekly during port ice closures. Shippers re-route to trucks, paying higher freight bills and lengthening lead times. Multimodal 3PLs capture emergency volumes, but persistent congestion tempers aggregate growth in the Canada Third-Party Logistics market[3]Canadian Pacific Kansas City, “2024-25 Winter Contingency Plan,” Canadian Pacific Kansas City, cpkcr.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Warehousing Innovation Drives Growth

Domestic Transportation Management commanded 38.45% of 2025 revenue, underlining Canada’s vast geography and interprovincial freight dependence. Value-Added Warehousing & Distribution, however, is growing the quickest at 7.06% CAGR. The Canada Third-Party Logistics market size tied to smarter warehousing will therefore expand faster than legacy line-haul services. CARM-driven compliance needs and Siemens’ battery R&D sites elevate demand for bonded, temperature-controlled buildings. Operators deploying robotics, RFID, and micro-fulfillment pods shrink pick times and improve cubic utilization, cushioning rent inflation.

Over the forecast, growth hinges on integrating real-time inventory visibility across e-commerce, healthcare, and EV supply chains. International Transportation Management advances on the back of CUSMA freight, yet congestion-prone rail corridors highlight the importance of multimodal resilience. Continued cold-chain investment after UPS-Andlauer and tighter food-safety audits further widen margins in specialty warehousing. Through 2031, the Canadian third-party Logistics market will reward providers that treat distribution centers as tech-enabled nodes rather than static cost centers.

By End User: Retail Dominance Amid Sector Diversification

E-commerce held 27.10% in 2025, the single biggest slice of the Canada Third-Party Logistics market. Dropship expectations for two-day delivery and seasonal demand spikes lift warehouse automation ROI. Automotive manufacturing, supercharged by EV battery localization, creates backhaul synergies: components flow north, finished vehicles move south. Life Sciences demand intensifies in parallel, as stricter Health Canada GDP guidelines raise cold-chain compliance thresholds. The Canada Third-Party Logistics market share tied to healthcare is therefore set to widen, even if absolute volumes trail retail.

Energy & Utilities customers adopt green corridors for ammonia, hydrogen, and carbon capture equipment. Food & Beverages diversify suppliers amid climate-related crop volatility, expanding regional freight loops. Such cross-sector dynamics smooth revenue volatility for large 3PLs. As each vertical adds specialized KPIs-from stock-keeping-unit accuracy to chain-of-custody traceability-the competitive moat around diversified service portfolios strengthens across the Canada Third-Party Logistics market.

By Logistics Model: Hybrid Strategies Gain Momentum

Asset-Light firms still dominate at 50.55% but Hybrid operators notch the fastest 6.76% CAGR. Pure brokers excel at flexibility, yet customers needing temperature-controlled capacity or electric trucks favor asset control. Ryder’s shift toward contractual logistics shows how selective fleet ownership can lock in sticky revenue at scale. Achieving this balance is central to sustained gains in the Canada Third-Party Logistics market. Ongoing real-estate shortages in the GTA make full asset-heavy plays risky, but provincial Special Economic Zones promise fast-track permits that recalibrate risk-reward equations.

Hybrid 3PLs also capitalize on lower borrowing costs when coupling green bonds with zero-emission equipment. Meanwhile, asset-light specialists invest in software, using AI to pool capacity and replicate network effects previously reserved for carriers with thousands of trailers. The Canada Third-Party Logistics market ultimately converges toward platforms that stitch together internal fleets, contracted owner-operators, and marketplace capacity under one visibility layer.

Geography Analysis

Ontario and Quebec form the economic core, hosting most automotive and consumer-goods production. Availability in GTA warehouses hit 4.5% in 2024, easing somewhat from record lows, while average rents softened to USD 18.17 per ft². Yet land constraints persist; zoning appeals delay modern distribution centers, nudging the Canada Third-Party Logistics market toward suburban micro-fulfillment. Montreal saw negative absorption of 1.3 million ft², with vacancy edging up to 3.9%, though lower rents there attract importers needing bilingual customer support.

The Prairie provinces rely heavily on rail to move grain, potash, and energy products. Recurrent congestion and winter port closures cut weekly grain railings to 525,000 tons, steering shippers toward blended rail-truck routings. Value-added transloading yards in Winnipeg and Regina now anchor west-to-east logistics flows, further linking the Canada Third-Party Logistics market to agricultural export cycles. British Columbia’s overpass-strike fines raise insurance premiums, but its Pacific ports remain vital for Asia-bound forestry exports, underpinning steady container demand.

Atlantic Canada emerges as a niche energy corridor. USD 22.5 million in federal grants fund green-ammonia infrastructure, positioning Halifax and Point Tupper as gateways for renewable fuels into Europe. Polar routing limitations after the 2024 heavy-fuel-oil ban will redirect Arctic resupply cargo through Atlantic terminals. Though smaller in absolute terms, the region’s specialized handling needs create outsize margin potential within the Canada Third-Party Logistics market. Overall, regional diversification stabilizes national volumes amid localized disruptions.

Competitive Landscape

The Canadian 3PL arena is fragmented. Consolidation accelerated when UPS agreed to buy Andlauer Healthcare Group for USD 1.6 billion, adding 34 temperature-controlled sites. TFI International followed by purchasing Hercules Forwarding for over USD 100 million, reinforcing cross-border less-than-truckload (LTL) reach. Both deals underscore a strategic shift away from scale alone toward domain specialization—cold chain and cross-border compliance, respectively.

Technology is the primary differentiator. Canadian National Railway’s 30% velocity gain around Chicago stems from advanced dispatch analytics, while AI freight-matching startups cut empty-mile ratios by double digits. Labor relations also reshape market share: DHL Express Canada narrowly avoided a prolonged lockout with 2,100 unionized staff, prompting shippers to hedge volumes. Hybrid operators that blend owned fleets with marketplace capacity absorb diverted freight, inching up their stake in the Canada Third-Party Logistics market.

Future competitive intensity will hinge on CARM readiness and zero-emission fleet rollouts. Smaller brokers lacking the financial capacity to post importer security bonds risk disintermediation. Conversely, providers issuing green bonds to fund electric truck acquisitions gain preferential access to ESG-minded shippers. Taken together, the forces of regulation, technology, and sustainability are recasting rivalry contours across the Canada Third-Party Logistics market.

Canada 3PL Industry Leaders

DHL Supply Chain

Purolator Logistics

Kuehne + Nagel

DSV

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kenco purchased the 3PL arm of Drexel Industries, adding four Toronto-area warehouses and 100 employees to strengthen cross-border distribution.

- April 2025: UPS agreed to acquire Andlauer Healthcare Group for USD 1.6 billion, expanding global cold-chain reach in anticipation of H2 2025 closure.

- March 2025: Canadian National Railway merged operations with Iowa Northern Railway, linking Prairie grain origins to Gulf export terminals.

- January 2025: CN secured U.S. Surface Transportation Board approval to absorb Iowa Northern Railway, integrating 175 route miles into its 20,000-mile network.

Canada 3PL Market Report Scope

A comprehensive background analysis of the Canada 3PL Market, covering the current market trends, restraints, technological updates and detailed information on the market concentration through the various segments and competitive landscape of the industry.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

How large is the Canada Third-Party Logistics market in 2026?

The Canada Third-Party Logistics market size is valued at USD 20.7 billion in 2026.

What is the projected growth rate for Canadian 3PL services through 2031?

The market is forecast to grow at a 4.33% CAGR, reaching USD 25.59 billion by 2031.

Which service category is expanding the fastest?

Value-Added Warehousing & Distribution is set to grow at a 7.06% CAGR as shippers demand specialized storage and fulfillment.

Why are hybrid logistics models gaining popularity in Canada?

Hybrid models blend asset ownership with brokered capacity, giving providers both operational control and flexibility amid compliance and sustainability pressures.

Page last updated on: