Bullous Pemphigoid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

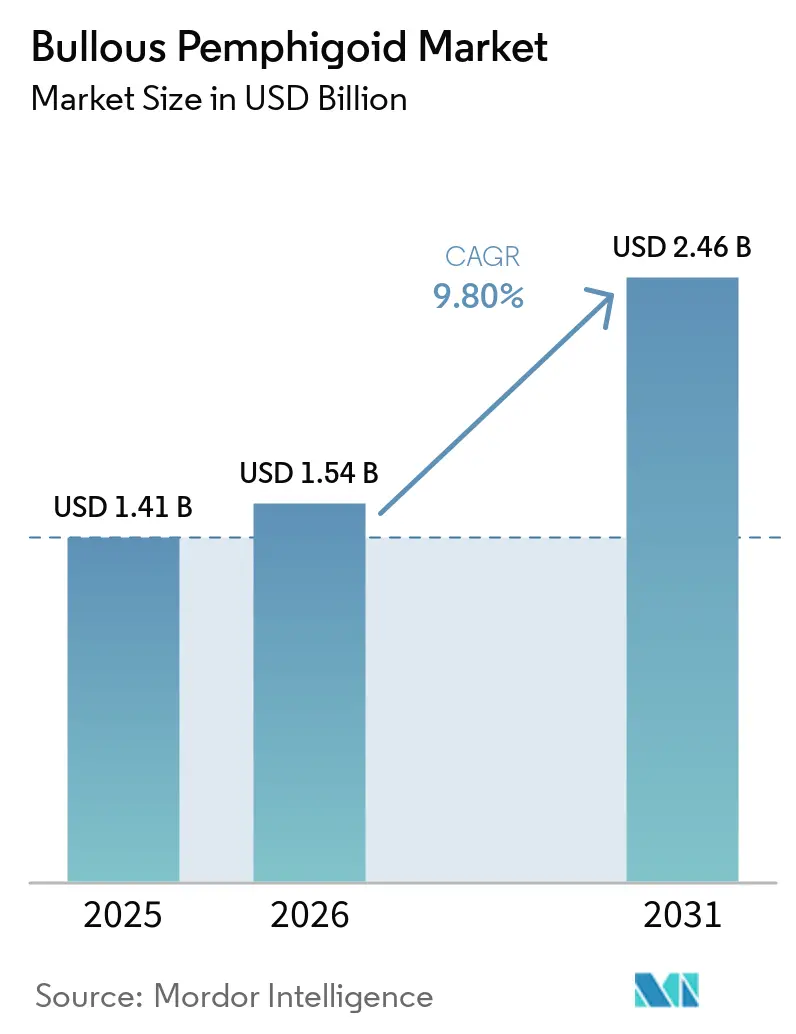

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 9.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bullous Pemphigoid Market Analysis by Mordor Intelligence

The Bullous Pemphigoid Market size is projected to expand from USD 1.41 billion in 2025 and USD 1.54 billion in 2026 to USD 2.46 billion by 2031, registering a CAGR of 9.80% between 2026 to 2031.

Dupilumab’s first-in-class approval for adults with bullous pemphigoid in the United States in June 2025 set a new treatment baseline that supports premium pricing and earlier biologic use in refractory cases, which lifted the bullous pemphigoid market above its prior growth trend. Regulatory momentum extended to Japan in March 2026, creating synchronized access for a super-aged population where safety concerns with systemic steroids are pronounced. Pending European authorization keeps clinician interest high, and the risk management plan disclosures reinforce the consistency of trial endpoints and safety monitoring parameters for broader market introduction, which together underpin positive sentiment across the bullous pemphigoid market. The disease’s concentration in older adults sustains a durable treatment need, and evidence supporting steroid-sparing strategies continues to shape real-world care choices in the bullous pemphigoid market, which helps narrow unwarranted variation and reduces corticosteroid-related harm in routine practice. Clinical data demonstrating sustained disease control with a targeted pathway agent expanded payer willingness to reimburse in steroid-refractory cases, improving access for the estimated 27,000 adults in the United States who did not respond to conventional therapy, and strengthening the forward trajectory of the bullous pemphigoid market.

Key Report Takeaways

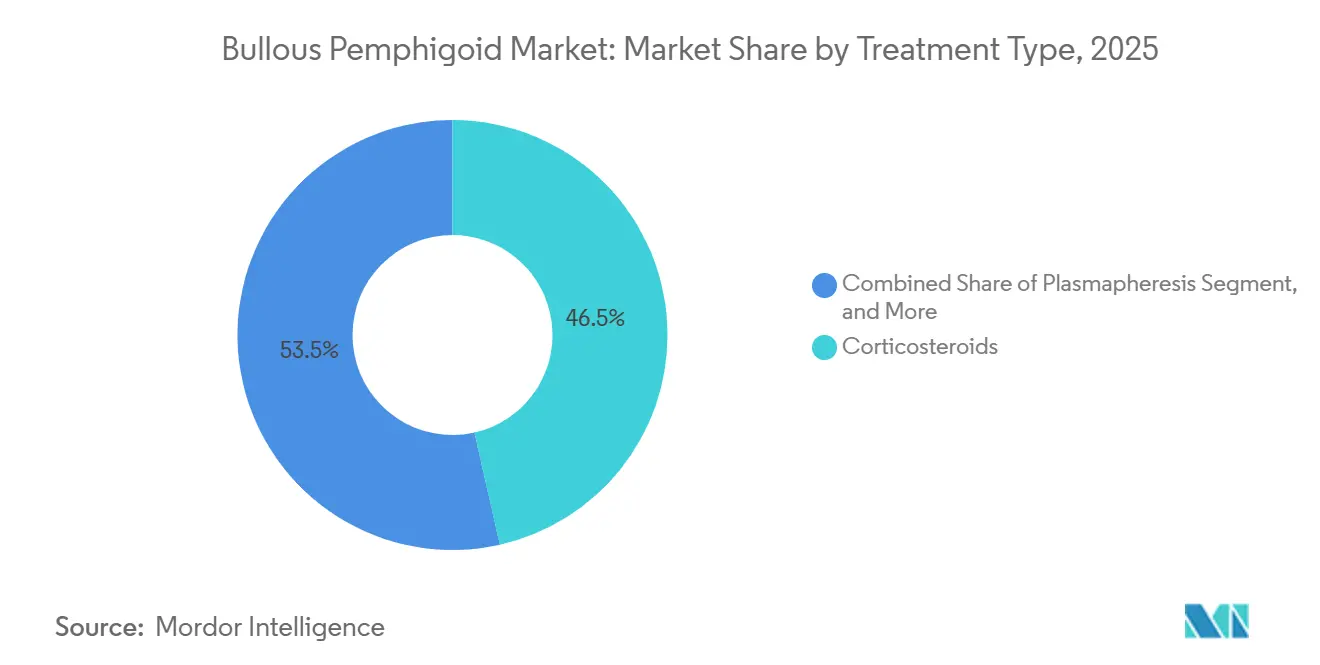

- By treatment type, corticosteroids led with 46.48% revenue share in 2025. Immunosuppressants are projected to expand at a 10.13% CAGR to 2031 in the bullous pemphigoid market.

- By route of administration, oral therapies held 48.31% share in 2025. Topical therapies are advancing at an 11.21% CAGR through 2031 in the bullous pemphigoid market.

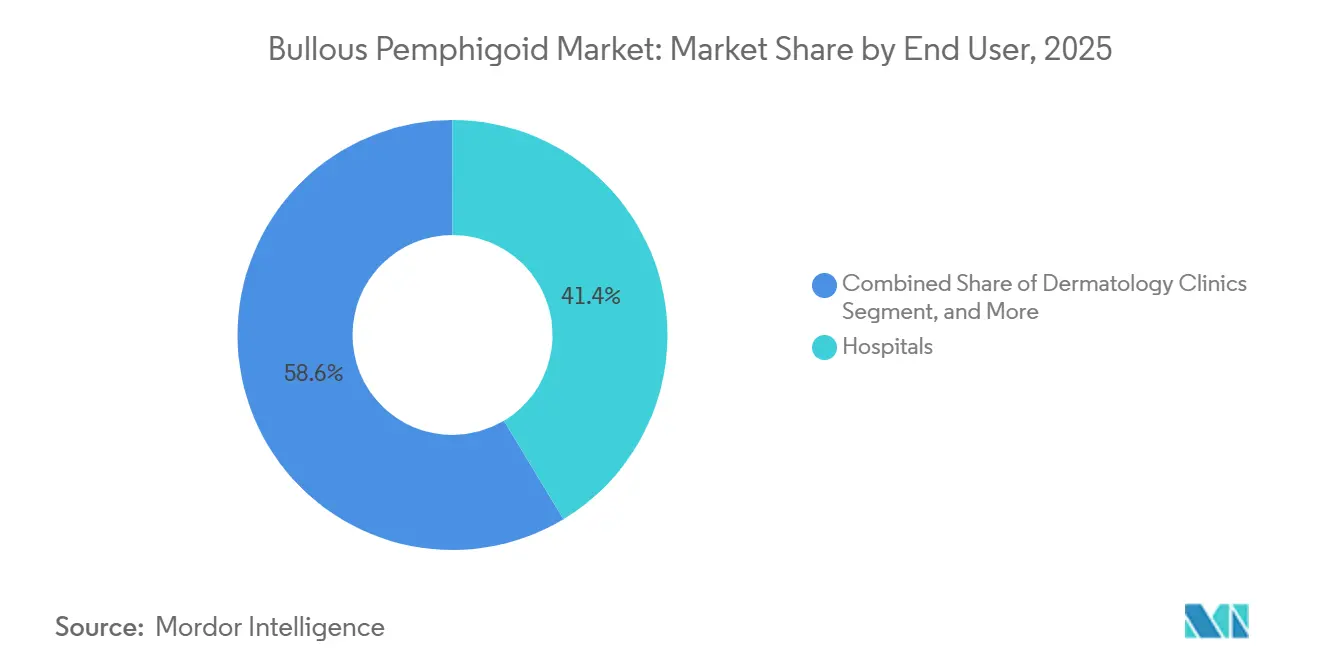

- By end user, hospitals accounted for 41.37% share in 2025. Dermatology clinics record the fastest growth at a 12.75% CAGR to 2031 in the bullous pemphigoid market.

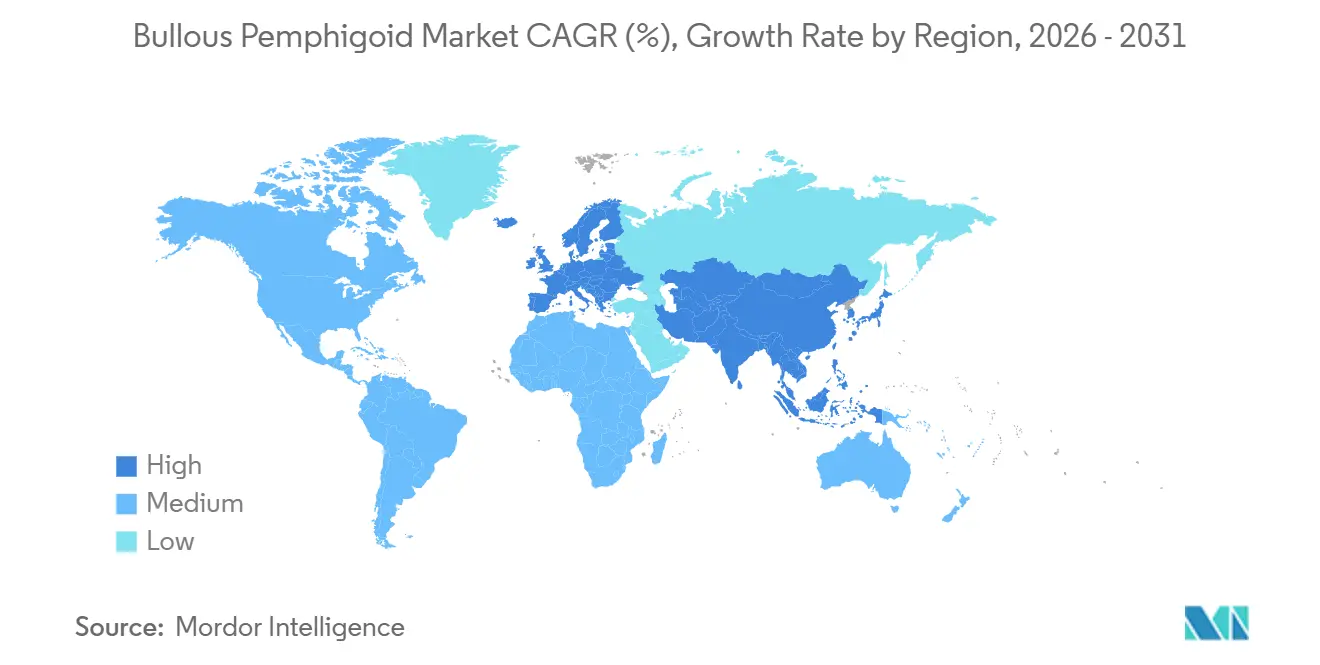

- By geography, North America commanded 43.12% share in 2025. Asia-Pacific is the fastest-growing region at a 13.67% CAGR through 2031 in the bullous pemphigoid market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bullous Pemphigoid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Expansion Driving Higher Incidence | +2.3% | Global, with peak impact in Japan, Germany, Italy where median ages exceed 45 years | Medium term (2-4 years) |

| Rising Diagnosed Incidence and Awareness From Improved ELISA Testing and Dermatologist Training | +1.8% | North America and EU core, spill-over to urban APAC centers | Short term (≤ 2 years) |

| Evidence-Backed Steroid-Sparing Regimens Adoption Reducing Long-Term Corticosteroid Toxicity | +1.5% | North America and Western Europe, with lag in price-sensitive emerging markets | Medium term (2-4 years) |

| First Targeted Biologic Approvals and Regulatory Tailwinds | +2.4% | Global, led by US in 2025 and Japan in 2026, with Europe anticipated next | Short term (≤ 2 years) |

| Drug-Induced BP From DPP-4 Inhibitors and Immune Checkpoint Inhibitors Expanding Patient Pool | +1.2% | Global, concentrated in regions with high diabetes and advanced oncology use | Long term (≥ 4 years) |

| Hospital and Payer Shift to Reduce Steroid-Related Adverse Events Lowering Total Cost of Care | +0.8% | National, with early gains in integrated systems in the US and public payers in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population Expansion Driving Higher BP Incidence

The bullous pemphigoid market benefits from a structural demographic tailwind as the disease disproportionately affects older adults who face higher risks of severe disease and recurrent flares. Evidence from European and Asian cohorts confirms that typical patients are in their late seventies or older, and age correlates with more erosions and greater clinical severity, which creates sustained demand for therapies that avoid the complications of long-term systemic steroids. Public health tracking in England indicated growth in burden over time and supports the need for access pathways that address hospitalization risk and extended recovery windows in elderly patients, reinforcing durable volume across the bullous pemphigoid market. Japan’s March 2026 approval for dupilumab underscores the importance of age-aware benefit-risk assessments and formulary decisions in super-aged societies, where steroid toxicity and polypharmacy complicate care. As longevity rises, the clinical reality of frailty, comorbidities, and fracture risk elevates the value proposition of steroid-sparing options, which encourages guideline-aligned care in the bullous pemphigoid market. These dynamics provide a multi-year underpinning for demand, lessen cyclical volatility, and favor products that deliver remission while limiting systemic adverse events in older adults.

Rising Diagnosed Incidence and Awareness from Improved Diagnostic Tools

Better adherence to standardized diagnostic workflows is lifting case capture and compressing time to diagnosis, which expands the near-term treated population in the bullous pemphigoid market. Direct immunofluorescence is positive in a high proportion of suspected cases, and validated serologic tests for BP180 and BP230 improve sensitivity and specificity, supporting earlier treatment initiation at specialty centers. European practice recommendations and widespread clinician education have promoted the combined use of biopsy and serology, which is important for distinguishing BP from other autoimmune blistering diseases and eczematous mimickers. As diagnostic infrastructure improves in urban Asia, detection is normalizing toward European rates, which raises the number of patients eligible for guideline-concordant management within the bullous pemphigoid market. These trends drive a one-time elevation in prevalent treated cases as latent patients are identified, followed by steady alignment with age-adjusted incidence and improved referral pathway. The net effect is faster triage to therapy and more consistent follow-up in community and academic settings over the next two to four years.

Evidence-Backed Steroid-Sparing Regimens Adoption

Randomized and comparative evidence has shifted first-line care toward potent topical corticosteroids for extensive skin involvement and toward using steroid-sparing agents when systemic therapy is needed, which improves outcomes in routine practice and stabilizes quality of care across the bullous pemphigoid market.[1]S. Singh et al., “Interventions for bullous pemphigoid,” Cochrane Database of Systematic ReviewsThe mortality and complication profiles associated with chronic systemic corticosteroids are increasingly recognized, reinforcing dose minimization with topicals or steroid-sparing agents in most cases.[2]American Academy of Dermatology, “Bullous pemphigoid, diagnosis and treatment,”As formularies update step-therapy protocols to reflect topical-first approaches for localized disease and cautious systemic escalation, payers shape standardized access pathways that align with improved safety profiles. Clinics and hospitals that operationalize these protocols are seeing fewer steroid-related complications and more consistent skin healing endpoints over time, which reduces utilization variability and supports better patient experience within the bullous pemphigoid market. These changes reward products and care models that speed resolution while limiting systemic exposure, especially in older adults with multiple comorbidities.

First Targeted Biologic Approvals and Regulatory Tailwinds

Dupilumab’s June 2025 approval in the United States for adults with bullous pemphigoid marked the first targeted pathway therapy for the disease and delivered statistically significant gains in sustained remission compared with placebo in the pivotal program, which reset clinical expectations and lifted the bullous pemphigoid market outlook.[3]Sanofi, “Dupixent approved in the US as the only targeted medicine to treat patients with bullous pemphigoid,” Priority review designations and global regulatory sequencing compressed timelines for both the United States and Japan, which limited time-to-access for elderly patients, most at risk from chronic steroids.[4]Sanofi, “Dupixent approved in Japan as the first targeted medicine to treat adults with bullous pemphigoid,” Japan’s March 2026 approval extended availability to a super-aged population and reinforced confidence in the trial data’s external validity across regions. EMA risk management disclosures indicate an advanced review state and a consistent benefit-risk framework, which supports near-term European decisions and a coordinated launch footprint for the bullous pemphigoid market. Together, these steps tighten global launch lags relative to historical dermatology therapies and promote rapid physician adoption in steroid-refractory cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost and Long Duration of Biologics/IVIG Limiting Payer Authorization And Patient Adherence | -1.4% | Global, acute in non-reimbursed emerging markets in Latin America, Southeast Asia, and sub-Saharan Africa | Long term (≥ 4 years) |

| Early Misdiagnosis and Diagnostic Latency Delaying Appropriate Therapy Initiation | -0.9% | APAC core and parts of Latin America and MEA with limited dermatopathology capacity | Medium term (2-4 years) |

| Safety Constraints in Frail Elderly Limit Aggressive Immunosuppression due To Infection Risk and Polypharmacy Interactions | -0.6% | Global, most pronounced in patients aged 85 years and older and in nursing homes | Short term (≤ 2 years) |

| Off-Label Reimbursement and Access Variability Creating Treatment Disparities | -1.1% | National, with variance between U.S. public and private payers and public systems in Europe and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Long Duration of Biologics/IVIG Limiting Access

The high acquisition cost and chronic dosing requirements for targeted biologics and IVIG create access hurdles that slow equitable adoption across the bullous pemphigoid market. Payers frequently require evidence of prior steroid use and clinical failure for IVIG authorization, which lengthens time to treatment for refractory patients and increases administrative burden on prescribers and institutions. In systems with constrained specialty budgets, the need for infusion capacity and ongoing monitoring adds resource stress that prefers topical-first and lower-cost options, especially for elderly patients with limited mobility. Even where reimbursement is available, out-of-pocket costs and co-insurance can reduce adherence or lead to treatment interruptions that diminish real-world effectiveness. These economic pressures moderate penetration of advanced agents outside tertiary centers and better-resourced health plans, which shapes the near-term mix within the bullous pemphigoid market. As clinical experience and outcomes data accumulate, health technology assessment pathways can evolve to recognize steroid-sparing benefits, but near-term affordability limits remain material in many geographies.

Early Misdiagnosis and Diagnostic Latency Delaying Therapy

Delays from symptom onset to confirmed diagnosis remain a key restraint because initial presentations can mimic eczema or drug reactions, and many patients first present outside dermatology, which postpones definitive testing and therapy in the bullous pemphigoid market. Access to dermatopathology with direct immunofluorescence and to validated serology is uneven across regions, and limited capacity in rural and resource-constrained settings extends diagnostic timelines. Patients diagnosed later often have higher disease activity and more extensive skin involvement, which complicates steroid minimization strategies and elevates hospitalization risk. Standardizing referral protocols and expanding access to serologic testing can reduce time to treatment and improve patient outcomes, but this infrastructure build-out takes sustained investment. In the interim, diagnostic latency will continue to limit early optimization of therapy for a portion of patients in the bullous pemphigoid market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Corticosteroids Anchor Market Despite Biologics’ Incursion

Corticosteroids captured 46.48% of the bullous pemphigoid market share in 2025, reflecting their entrenched first-line status in clinical guidance for both oral and high-potency topical use in patients with variable disease extent. Immunosuppressants are projected to grow at a 10.13% CAGR as clinicians seek to reduce cumulative steroid exposure in prolonged disease courses, which favors azathioprine, mycophenolate mofetil, or methotrexate under careful monitoring. Biologics and targeted therapies were nascent in 2025, and momentum accelerated after June 2025 as dupilumab demonstrated superior sustained remission versus placebo in controlled studies, which materially strengthens uptake in steroid-refractory adults. IVIG remains a late-line option for refractory cases and typically requires prior authorization that documents lack of response or intolerance to steroids and other immunosuppressants, which constrains use to patients with significant disease burden. Comparative evidence supports potent topical corticosteroids for many patients with extensive skin involvement due to efficacy and safety advantages over high-dose oral regimens, especially in older and frail patients.

Across the bullous pemphigoid market, biologics are poised to expand addressable use in patients who do not achieve durable control with steroids or who face safety risks from systemic exposure, while corticosteroid volume remains high but gradually tilts toward topical-first strategies The bullous pemphigoid industry is also seeing broader institutional alignment with steroid-sparing protocols and more consistent referral to specialty centers for severe or relapsing cases, which supports both outcomes and cost management. Over the forecast period, premium-priced targeted options will lift category value even with conservative utilization criteria, while immunosuppressants benefit from their role in step-therapy algorithms. The bullous pemphigoid market will continue to depend on high-potency topical steroids for first-line care due to strong efficacy and accessibility, while systemic options are reserved for broader or refractory disease.

By Route of Administration: Oral Dominance Faces Topical Resurgence

Oral therapies held 48.31% share in 2025 due to long-standing reliance on systemic steroids for rapid disease control, but this leadership is increasingly challenged by topical strategies that now demonstrate strong outcomes and a better safety balance in many patients. Topical therapies are advancing at an 11.21% CAGR as evidence and clinical guidance promote high-potency regimens for extensive disease, which can reduce systemic risks while achieving robust skin healing endpoints in the bullous pemphigoid market. Subcutaneous administration gained new relevance with dupilumab’s 2025 approval, since labeled dosing enables patients to self-inject after training and reduces dependence on infusion centers for eligible adults. Intravenous routes remain important for agents like rituximab and for IVIG when indicated in refractory disease, although payer criteria and facility capacity shape utilization patterns.

In the bullous pemphigoid market, this shift in route preference reflects both evolving clinical evidence and the practicalities of caring for older adults with comorbidities and mobility limitations. The bullous pemphigoid industry continues to refine when to escalate beyond topical therapy to systemic or targeted options, and subcutaneous self-administration offers a path to maintain disease control with fewer clinic visits for appropriate patients. Over time, the mix should keep tilting toward routes that minimize treatment burden while preserving sustained remission, and this favors topical regimens in early lines and subcutaneous biologics in refractory adults. Intravenous therapies retain a defined role in complex cases and in settings where payer policy or clinical history support their use.

By End User: Dermatology Clinics Capture Share from Hospitals

Hospitals accounted for 41.37% share in 2025 due to their central role in acute presentations, severe erosions, and the need for inpatient observation or intravenous treatments in complicated cases. Dermatology clinics are growing at a 12.75% CAGR as outpatient diagnosis, topical-first protocols, and follow-up for subcutaneous therapies align with clinic workflows, which shifts maintenance care outside hospital settings in the bullous pemphigoid market. The subcutaneous route for dupilumab enables initiation in clinics for eligible adults and supports continuity of care with structured follow-up, reducing the need for infusion infrastructure in appropriate cases. Infusion services remain essential for patients who receive IVIG or intravenous rituximab, but payer and institutional policies encourage outpatient delivery whenever possible.

Over the forecast period, the bullous pemphigoid market should continue to decentralize routine care into dermatology clinics and integrated outpatient centers, while hospitals focus on severe or unstable cases that need close monitoring. The bullous pemphigoid industry is also benefiting from teledermatology and structured nurse education that improves adherence to topical regimens in older adults, which supports outpatient management and reduces readmissions. Payers reinforce these shifts with step-therapy criteria that require topical trials and careful documentation before systemic escalation, aligning financial incentives with clinical guidance. Hospitals will retain a stable role due to case complexity, infection risk, and comorbidity burden in the oldest cohorts.

Geography Analysis

North America commanded 43.12% of the bullous pemphigoid market share in 2025 due to early access to targeted therapy, established specialty referral networks, and payer frameworks that support steroid-sparing strategies in appropriate adults. The United States approval in June 2025 for dupilumab created a clear treatment path for adults who failed or could not tolerate standard therapies, and the sponsor highlighted an estimated 27,000 adults as a near-term addressable pool in the country, which supported a step-change in demand. Specialty guidelines and payer protocols that prioritize high-potency topical steroids for many cases create a consistent standard that then branches to targeted options for refractory disease, stabilizing utilization growth across the region. Over time, alignment between public and private payers should reduce variation in authorization and improve continuity of dosing for eligible adults. North America remains a reference market for clinical adoption of steroid-sparing approaches that other regions evaluate as targeted therapies become available.

Asia-Pacific is growing at a 13.67% CAGR in the bullous pemphigoid market, led by Japan’s March 2026 approval, which brings targeted therapy into a super-aged society with high clinical need and broad dermatology capacity. As urban diagnostic capacity increases, detection is expected to converge toward Western rates, closing historical gaps in underdiagnosis across large city centers. The pace of adoption varies by health system design and reimbursement policy, but the region benefits from clinician familiarity with pathway-targeted agents across other dermatologic and immunologic diseases, which eases integration once approvals are secured. Academic and referral centers shape early diffusion patterns and set standards for follow-up in older adults with complex comorbidities, and their protocols tend to propagate into community practice within a few years. This combination of regulatory progress, aging demographics, and infrastructure maturation supports sustained regional expansion of the bullous pemphigoid market.

Europe had a large base in 2025 and awaits final regulatory action, with EMA review supported by published risk management documentation that tracks clinical outcomes, safety, and mitigation plans for wider market introduction. Public payers frame cost effectiveness in terms of steroid-sparing benefits and hospitalization avoidance, which interact with formulary scope and criteria at launch. European clinical practice aligns with standardized diagnosis and advancing dermatopathology capacity that will continue to reduce missed or delayed cases, improving earlier intervention in the bullous pemphigoid market. National health technology assessments and negotiated access agreements will shape pace of uptake across member states. As approvals finalize and reimbursement decisions mature, Europe will likely see consistent adoption among steroid-refractory adults with continued reliance on high-potency topical therapy as the early-line standard.

Competitive Landscape

Companies such as Sanofi and Regeneron have a significant targeted segment in the bullous pemphigoid market following the June 2025 U.S. approval and March 2026 Japan authorization, which together created the first labeled pathway therapy with controlled trial evidence for sustained remission in adults. The launch strategy has emphasized sterile technique education, self-injection readiness, and clinic-based initiation for eligible adults, which lowers dependence on infusion centers for targeted therapy. In parallel, generics and established immunosuppressants remain important given their step-therapy roles and broad availability. This bifurcation leaves the targeted category concentrated while the overall bullous pemphigoid market remains diversified across steroids, topicals, and systemic agents in routine care.

Biosimilar rituximab products add competitive tension in systemic lines of therapy because they are familiar to providers managing autoimmune diseases, even though bullous pemphigoid use often involves off-label considerations and payer criteria. Intravenous immunoglobulin suppliers compete on contracting and access in refractory presentations, supported by payer policies that define place-of-service and authorization requirements. Companies active across immunology continue to generate adjacent data in inflammatory skin diseases that can inform future bullous pemphigoid trial designs and patient selection. This ecosystem encourages pragmatic comparisons on safety and sustained control that will shape physician preference in the bullous pemphigoid market.

Recent innovations in dermatology and immunology signal potential future competition that could target type 2 inflammation or other relevant pathways, though near-term impact depends on investment in dedicated bullous pemphigoid programs. For example, positive phase 2 results with Biogen’s litifilimab in cutaneous lupus highlight the strength of targeted approaches in autoantibody-driven conditions, which could influence future R&D decisions around blistering disorders if sponsors pursue label expansion. Broader pipeline momentum across IL-17, TYK2, and BTK targets in other dermatologic indications keeps physician focus on mechanism-informed care and could set the stage for additional entrants if companies commit to bullous pemphigoid trials. These dynamics maintain strategic pressure on leaders to sustain clinical differentiation and real-world value in the bullous pemphigoid market.

Bullous Pemphigoid Industry Leaders

AbbVie, Inc.

Bristol Myers Squibb Company

Regeneron Pharmaceuticals, Inc.

Sanofi S.A.

UCB S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sanofi and Regeneron announced Japan’s Ministry of Health, Labor and Welfare approved Dupixent for adults with moderate-to-severe bullous pemphigoid, the first targeted medicine for BP in Japan, and the product’s seventh indication in the country.

- March 2026: Biogen presented positive Phase 2 AMETHYST data for litifilimab in cutaneous lupus erythematosus at the American Academy of Dermatology Annual Meeting, showing a significant reduction in skin disease activity at Week 16 versus placebo and more participants achieving clear or almost clear skin .

- March 2026: AbbVie highlighted clinical and real-world immunology evidence at the 2026 AAD Annual Meeting, including long-term safety data for upadacitinib in atopic dermatitis and Phase 3 data for upadacitinib in non-segmental vitiligo, which underscores ongoing innovation in inflammatory skin diseases

Global Bullous Pemphigoid Market Report Scope

As per the scope of the report, bullous pemphigoid is a rare autoimmune skin disorder characterized by the formation of large, fluid-filled blisters (bullae) on the skin. It occurs when the immune system mistakenly attacks proteins in the skin’s basement membrane, leading to inflammation and separation of skin layers. The condition primarily affects older adults, especially those above 60 years of age. It is typically chronic and requires long-term immunosuppressive or biologic therapy for management.

The bullous pemphigoid market is segmented by treatment type, route of administration, end user, and geography. By treatment type, the market is segmented into corticosteroids, plasmapheresis, immunosuppressants, biologics / targeted therapies, and others. By route of administration, the market is segmented into oral, topical, subcutaneous, and intravenous. By end user, the market is segmented into hospitals, dermatology clinics, infusion centers/day care centers, and home care / long-term care facilities. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Corticosteroids |

| Plasmapheresis |

| Immunosuppressants |

| Biologics / Targeted therapies |

| Others |

| Oral |

| Topical |

| Subcutaneous |

| Intravenous |

| Hospitals |

| Dermatology Clinics |

| Infusion Centers / Day Care Centers |

| Home Care / Long-term Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Corticosteroids | |

| Plasmapheresis | ||

| Immunosuppressants | ||

| Biologics / Targeted therapies | ||

| Others | ||

| By Route of Administration | Oral | |

| Topical | ||

| Subcutaneous | ||

| Intravenous | ||

| By End User | Hospitals | |

| Dermatology Clinics | ||

| Infusion Centers / Day Care Centers | ||

| Home Care / Long-term Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size and growth outlook for the bullous pemphigoid market through 2031?

The bullous pemphigoid market size was USD 1.41 billion in 2025 and is projected to reach USD 2.46 billion by 2031 at a 9.8% CAGR over 2026-2031.

Which treatment types will drive the bullous pemphigoid market over the forecast period?

Corticosteroids remain the value anchor due to first-line use, while immunosuppressants and the first targeted biologic expand premium segments as steroid-sparing demand grows.

How will routes of administration evolve in the bullous pemphigoid market?

Oral therapies remain prominent, topical regimens continue to gain based on safety and efficacy support, and subcutaneous self-injection expands for eligible adults using labeled biologics.

Which regions are positioned for the fastest growth in the bullous pemphigoid market?

Asia-Pacific shows the highest growth trajectory due to Japan’s 2026 approval and improving diagnostic infrastructure in major urban centers.

What are the main barriers to broad biologic adoption in the bullous pemphigoid market?

High acquisition cost, payer step edits, and infusion capacity for some late-line therapies limit rapid scale beyond tertiary centers, especially in budget-constrained systems.

How will competitive dynamics change in the bullous pemphigoid market through 2031?

The targeted segment remains concentrated around the first approved biologic, while biosimilars, IVIG suppliers, and systemic agents compete on access and contracting, with potential future entrants from adjacent immunology pipelines.

Page last updated on: