Blood Gas And Electrolyte Analyzer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 3.62 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

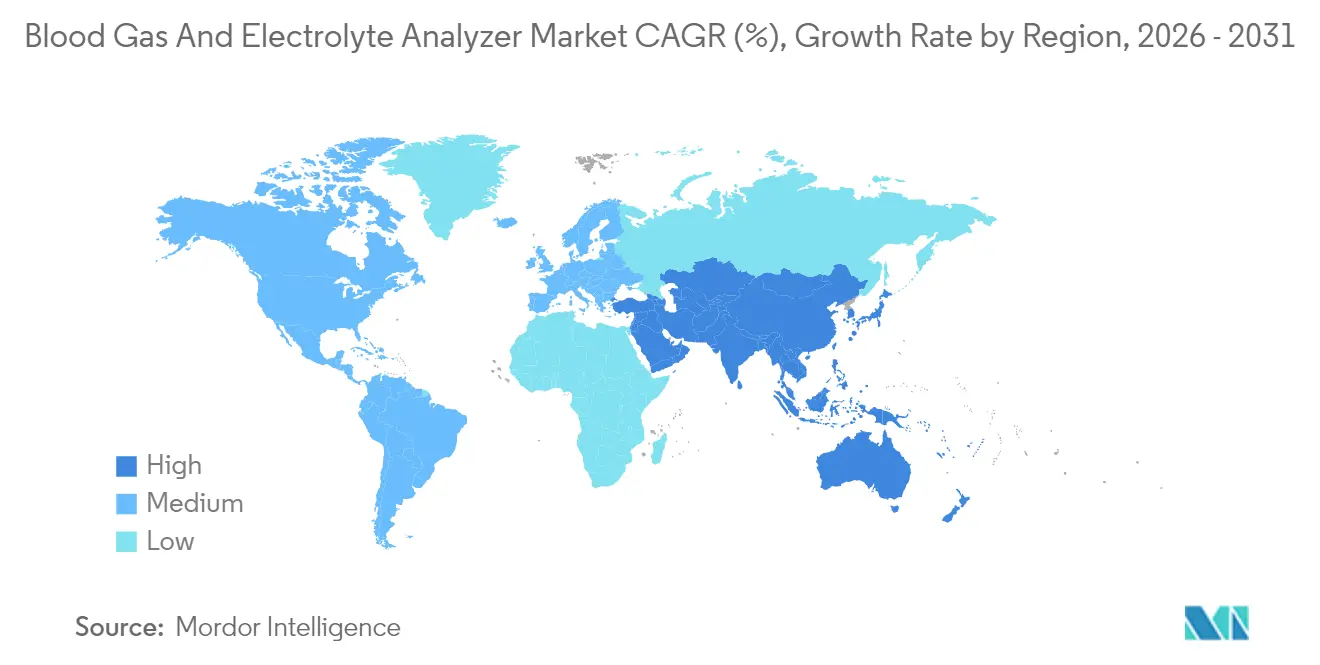

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Gas And Electrolyte Analyzer Market Analysis by Mordor Intelligence

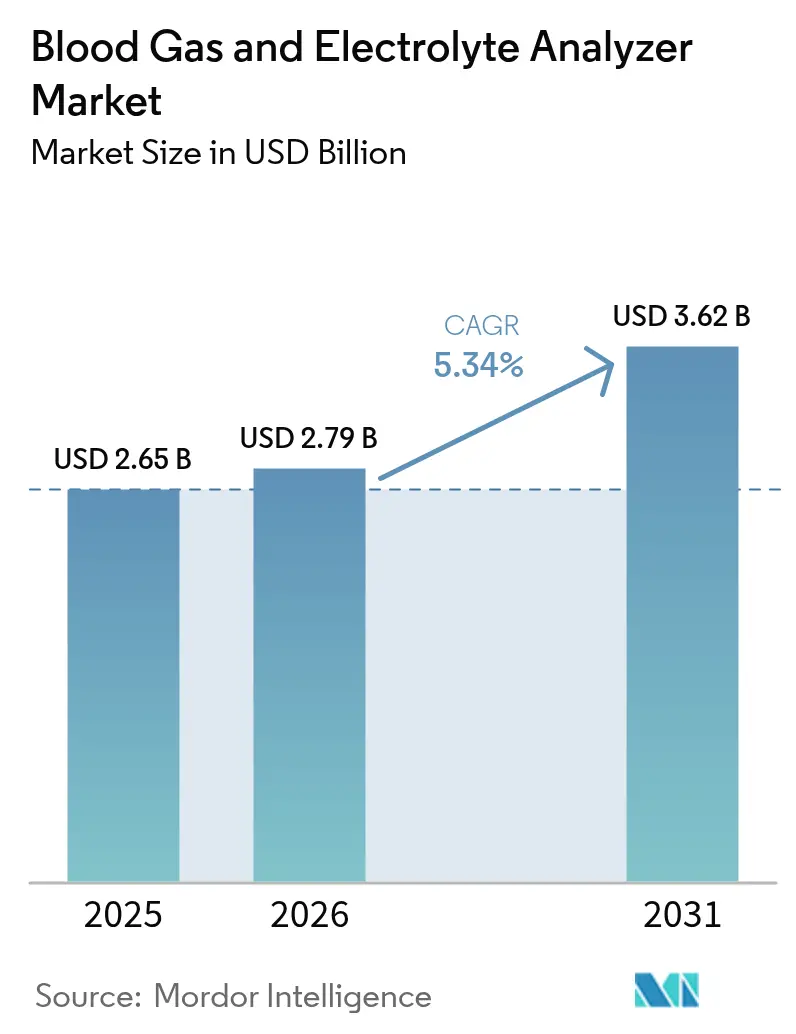

The Global Blood Gas And Electrolyte Analyzer Market size was valued at USD 2.65 billion in 2025 and estimated to grow from USD 2.79 billion in 2026 to reach USD 3.62 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031).

Growth rests on the indispensable role of rapid arterial blood-gas and electrolyte testing in critical-care, emergency, and peri-operative settings, especially as respiratory disease, neonatal intensive-care admissions, and complex metabolic emergencies rise. Demand is reinforced by health-system moves toward point-of-care workflows that compress result turnaround from hours to minutes, plus hospital automation initiatives that link analyzers to laboratory information systems for continuous quality oversight. Portable devices with wireless connectivity are scaling fastest because ambulance crews, operating theatres, and bedside teams value immediate decision support. Asia-Pacific is closing the gap on North America’s volume dominance as public and private investment channels modernize acute-care infrastructure and widen access to acute diagnostics.

Key Report Takeaways

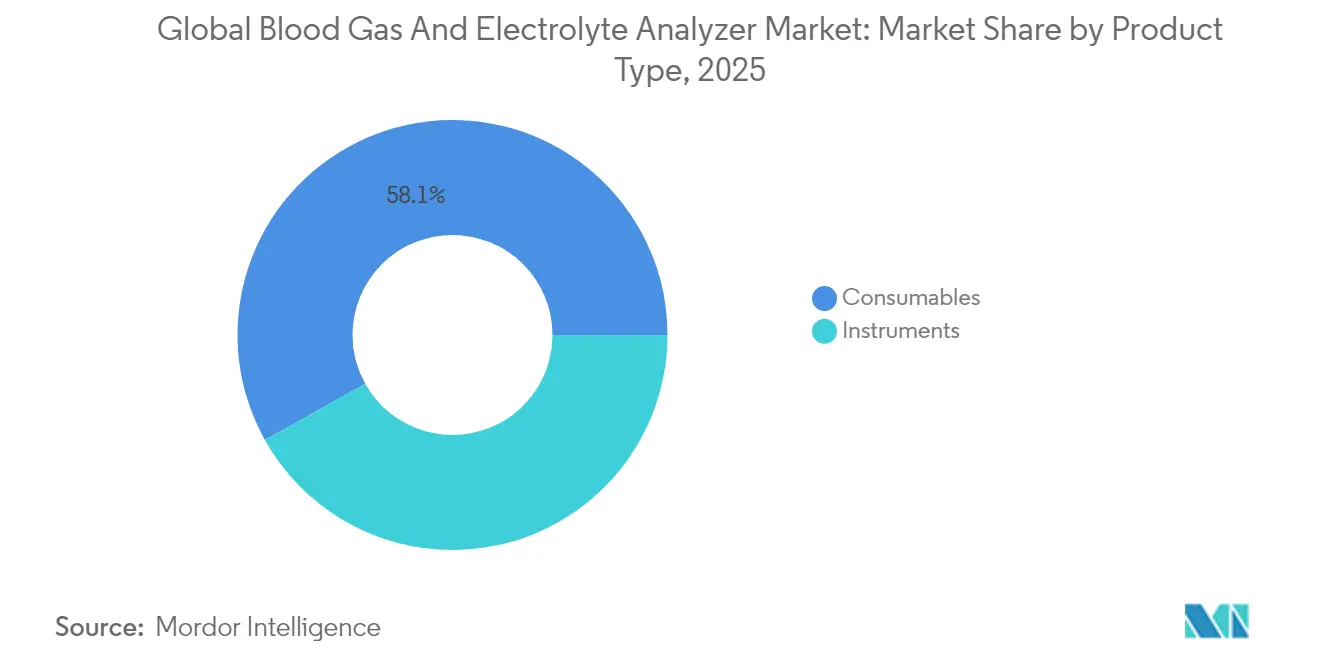

- By product type, consumables contributed 58.12% of the blood gas and electrolyte analyzer market share in 2025, while electrolyte analyzers are projected to post the fastest 5.82% CAGR through 2031.

- By modality, benchtop systems retained 50.35% revenue share in 2025, yet portable/handheld units are set to grow at a 7.12% CAGR to 2031.

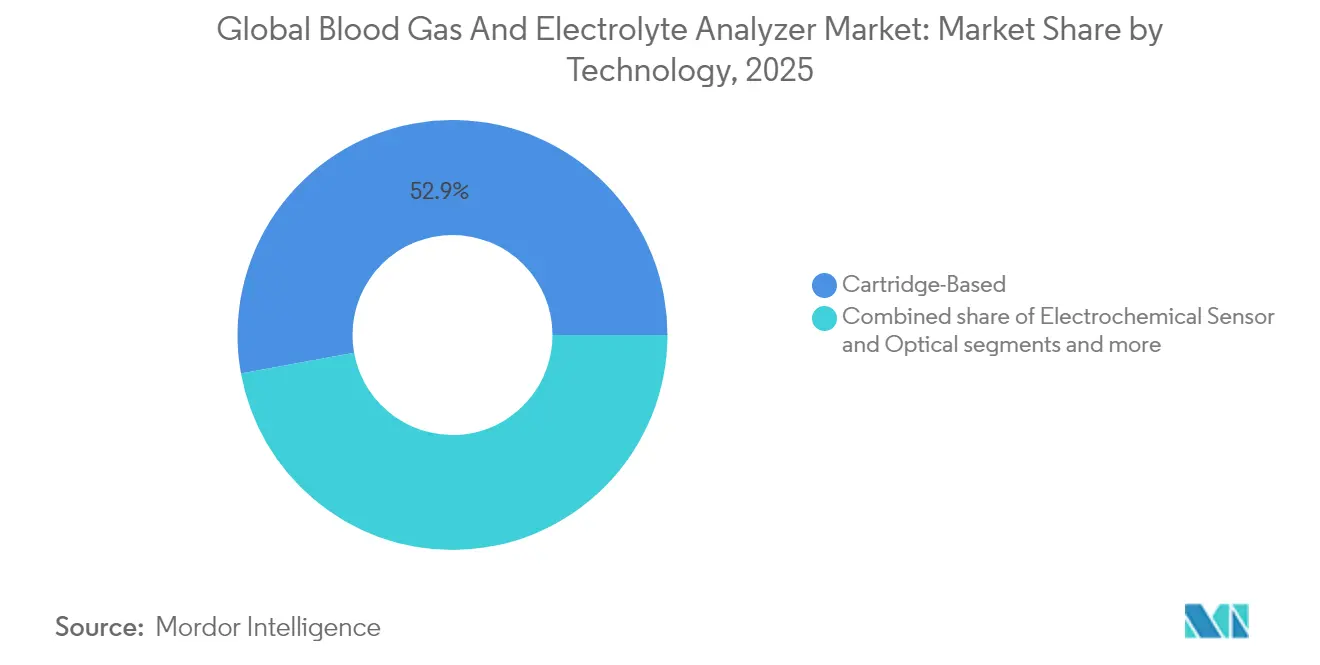

- By technology, cartridge-based platforms held 52.86% of the blood gas and electrolyte analyzer market size in 2025; optical/optode sensing is on track for a 6.78% CAGR between 2026-2031.

- By end-user, hospital central laboratories commanded 45.05% of 2025 sales, whereas ambulance and emergency services will record the highest 6.12% CAGR over the forecast horizon.

- By geography, North America generated 38.12% of global revenue in 2025; Asia-Pacific will register the fastest 7.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Gas And Electrolyte Analyzer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-care point-of-care testing uptake | +1.20% | Global, strong in North America & Europe | Short term (≤ 2 years) |

| COPD & asthma admissions in megacities | +1.00% | Asia-Pacific, Middle East, global urban hubs | Medium term (2-4 years) |

| Neonatal ICU micro-sampling demand | +0.70% | Global, higher in advanced health systems | Medium term (2-4 years) |

| IoT-enabled lab automation | +1.10% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Technology advances in analyzers | +0.80% | Early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Critical-Care Point-of-Care Testing

Bedside analyzers now deliver arterial pH, PaO₂, PaCO₂, electrolytes, and lactate results in under a minute, compressing decision cycles for sepsis bundles, ventilator adjustments, and trauma resuscitation. Systems such as the epoc Blood Analysis System integrate Wi-Fi modules so data flows directly into electronic medical records, eliminating manual transcription errors and cutting laboratory workload.Lower turnaround times translate into documented cost avoidance: a pediatric ICU reduced daily test frequency by 53% and saved USD 19,068 annually after deploying stewardship protocols around point-of-care blood-gas devices journals. Emergency departments also benefit, where 60-second results support prompt stroke differentiation before radiology confirmation.

Rapid Rise in COPD & Asthma Admissions in Megacities

Ambient air pollution, aging populations, and high smoking prevalence are driving COPD burdens toward low- and middle-income economies; 90% of COPD deaths now arise in those settings [1]Global Initiative for Chronic Obstructive Lung Disease, “GOLD 2025 Report,” goldcopd.org. Metropolitan hospitals facing surges of acute exacerbations require on-site blood-gas capacity to titrate oxygen therapy and non-invasive ventilation. Manufacturers are releasing ruggedized analyzers with battery backup and climate-tolerant sensors for secondary-level facilities lacking stable power. Expanded access improves triage accuracy, shortens emergency room dwell time, and can curb readmission penalties tied to respiratory care pathways.

Integration of IoT-Enabled Benchtop Analyzers Accelerating Lab Automation

Next-generation benchtop systems act as networked nodes inside fully automated “Dark Labs,” exchanging QC flags, maintenance alerts, and patient results with laboratory middleware in real time mlo-online.com. Automated substrate loading, on-board calibration, and machine-vision robotics slash manual touches by 75%, allowing overstretched technologists to manage more tests per shift siemens-healthineers.com. Remote dashboards let vendors push firmware updates and provide predictive maintenance, reducing downtime and aligning with hospitals’ smart-connected-care blueprints.

Technological Advancements in Blood Gas and Electrolyte Analyzers

Optical optode sensors that use luminescence quenching for dissolved gases deliver stable baselines with fewer recalibrations, supporting a 7.20% CAGR leadership within the technology segment diagnostics. Simultaneously, cartridge-based analyzers continue to evolve through embedded intelligence modules that spot hemolysis or air bubbles before results release, as seen in GEM Premier 7000 with iQM3. AI algorithms trained on patient-based real-time QC data sets outperform rule-based systems in detecting systematic drift, mitigating error propagation and lowering repeat test costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-budget constraints | -0.90% | Global, amplified in emerging markets | Short term (≤ 2 years) |

| Regulation & reimbursement hurdles | -0.60% | North America & Europe | Medium term (2-4 years) |

| Skilled-operator shortage | -0.80% | Worldwide, variable intensity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Budget Constraints

Capital scarcity after pandemic procurement spikes forces hospitals to defer analyzer refresh cycles. The U.S. Department of Health and Human Services documented sharp price surges for critical devices, squeezing budgets and shifting preference to reagent-rental or pay-per-test contracts that lift upfront cost barriers. Vendors respond by bundling service, QC cartridges, and analytics dashboards under operating-expense models, aligning with finance teams that favor predictable monthly cash flows.

Issues Regarding Regulation and Reimbursement of ABG Tests

Regulatory hurdles and reimbursement issues tied to arterial blood gas (ABG) tests are stifling the market's growth. Manufacturers face delays in launching new devices due to stringent regulatory approvals, which also inflate compliance costs and pose challenges for those looking to innovate or broaden their product offerings. Furthermore, varying or sparse reimbursement policies in diverse healthcare systems diminish the financial allure for providers to embrace cutting-edge blood gas analyzers, further curbing the market's growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumable Dominance and Electrolyte Analyzer Momentum

Consumables contributed 58.12% to the blood gas and electrolyte analyzer market in 2025, underlining the razor-razorblade model that anchors vendor revenue stability. Each arterial or venous sample draws a single-use cartridge, electrode pack, or reagent ampoule, turning high test frequency in critical-care beds into recurring cash flow. Masimo demonstrates the model: 89% of its healthcare revenue comes from consumables and services, financing R&D cycles that feed next-generation platforms. Integrated reagent-QC pouches also reduce inventory complexity and environmental exposure, lifting shelf life—an attractive feature for resource-limited facilities.

Electrolyte analyzers display a 5.82% CAGR through 2031 as outpatient chronic-disease clinics, dialysis centers, and sports-medicine programs seek compact devices that report sodium, potassium, chloride, ionized calcium, and glucose within two minutes. The segment overlays growth of combined analyzers that merge gases, metabolites, CO-oximetry, and electrolytes in one platform, shrinking blood draw volumes—a decisive point for neonatal wards. Nova Biomedical’s micro-sample mode demonstrates how microfluidics and intelligent fluidics engineering can fit an 11-test panel into 90 µL, linking clinical benefit to lower total cost of ownership news-medical.net. As a result, the blood gas and electrolyte analyzer market size for electrolyte-focused devices is forecast to command material share gains over the decade.

By Modality: Portable Systems Outpace Benchtop Installations

Benchtop analyzers retained 50.35% of global revenue in 2025 thanks to throughput, extended menus, and middleware hooks that central labs require. Dark-lab architecture integrates these analyzers with track systems and robotic arms, pushing unattended overnight operation to new levels mlo-online.com. Hospitals value long-term reagent contracts and consolidated QC regimes that stabilize per-test economics.

Portable and handheld platforms, however, are increasing at a 7.12% CAGR. Ambulance crews deploy battery-powered analyzers alongside defibrillators, capturing pH and lactate en-route to trauma centers, enabling physicians to pre-activate massive transfusion protocols. In operating rooms, anesthesiologists place palm-sized devices on the instrument table to fine-tune ventilation during thoracic surgery. Because these handhelds upload results via Bluetooth or hospital Wi-Fi, they integrate into lab reports without extra clerical work, making them pivotal to the decentralization wave sweeping the blood gas and electrolyte analyzer market.

By Technology: Cartridge Systems Hold Lead, Optode Sensors Accelerate

Disposable-cartridge systems held 52.86% market share in 2025 by packaging sensors, calibrants, and QC fluids into sealed units that technicians swap in seconds. Automated detection of hemolysis and micro-clots in the pathway, as embedded in GEM Premier 7000, mitigates the 70% error contribution attributed to pre-analytical factors, protecting clinical confidence.

Optode technology is rising fastest on a 6.78% CAGR as photoluminescence quenching and NDIR modules bring drift-free sensing across wider temperature ranges, cutting recalibration downtime. Hospitals in tropical climates appreciate the resilience when air-conditioning falters. Electrochemical sensors are trending toward miniaturization with nanostructured electrodes that maintain linearity at low currents, extending usable life. Collectively these advances preserve the blood gas and electrolyte analyzer market size advantage of established modalities while opening incremental niches.

By End-User: Hospital Labs in Front, Emergency Services Scaling Fast

Hospital central laboratories contributed 45.05% of 2025 revenue by virtue of volume concentration and broad test menus. However, automation means a single technologist can monitor multiple instruments through dashboards, mitigating labor shortages. Atellica integrated lines illustrate this shift, trimming manual tasks by up to 75%.

Ambulance and emergency services, expanding at 6.12% CAGR, create new front-line demand. Point-of-care devices placed in helicopters offer altitude-adjusted calibration curves, delivering uncompromised accuracy for aeromedical teams. Diagnostic clinics treating COPD outpatients and veterinary ICUs monitoring equine colic cases also broaden reach. These divergent settings ensure the blood gas and electrolyte analyzer market retains a balanced mix of centralized and distributed testing channels, cushioning vendors against single-site demand shocks.

Geography Analysis

North America generated 38.12% of global revenue in 2025, anchored by dense ICU bed stock, reimbursement for respiratory diagnostics, and extensive provider networks. The blood gas and electrolyte analyzer market size for the region stays buoyant as consolidation, exemplified by BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care Unit, adds connected-care capabilities to corporate portfolios. Nevertheless, laboratory retirement waves threaten capacity; 18.9% vacancy in blood-bank brethren spills over to critical-care labs, prompting health systems to favor analyzers with walk-away operation.

Asia-Pacific is forecast to post a 7.14% CAGR to 2031, narrowing the gap through public hospital expansion, private sector build-out, and government programs that subsidize diagnostic equipment for lower-tier cities. Urban smog adds to COPD caseloads, swelling arterial blood-gas demand. Domestic manufacturing initiatives encourage localization of cartridges and sensors, trimming import duties and strengthening supply resilience. As a result, the blood gas and electrolyte analyzer market in Asia-Pacific is transitioning from import-dependent to hybrid supply chains, accelerating price-point convergence with Western markets.

Europe retains a solid revenue base thanks to early technology uptake, stringent QC standards, and centralized procurement that negotiates large reagent volumes. Growth is steadier than in emerging regions but benefits from rising adoption of handheld analyzers in ambulance fleets aligned with pan-European emergency-medical-services guidelines.

Latin America and the Middle East & Africa together represent modest but accelerating slices of the blood gas and electrolyte analyzer market. Gulf countries channel oil surpluses into tertiary-care complexes that specify analyzers with Arabic user interfaces, while Brazilian private chains upgrade labs to manage a growing cardiovascular burden. Vendor differentiation increasingly depends on training hubs, local-language software, and heat-tolerant cartridges that sustain performance above 35 °C.

Competitive Landscape

The blood gas and electrolyte analyzer market exhibits moderate concentration around Radiometer Medical (Danaher), Siemens Healthineers, Abbott, Werfen, Nova Biomedical, Masimo, and bioMérieux. Abbott maintains a robust footprint through i-STAT handhelds, leveraging its global rapid-diagnostics channel globalpointofcare.abbott. Siemens continues to marry hardware to the Atellica informatics stack, fostering lock-in around consumables and middleware.

Acquisitions fuel portfolio enhancement. bioMérieux spent EUR 138 million on SpinChip Diagnostics in January 2025 to obtain 10-minute immunoassay capability from whole blood, complementing its respiratory panel offering. Werfen’s earlier buyout of Accriva Diagnostics added coagulation and ACT cartridges to its GEM line, bundling broader peri-operative coverage. Competitive axes now center on workflow simplification, cartridge shelf life, integrated QC, and cybersecurity credentials for IoT connectivity.

Technology differentiation remains key. Werfen’s iQM3 self-monitoring detects hemolysis in seconds, lowering repeat-draw incidence. Siemens offers dual-channel connectivity to hospital Wi-Fi and LTE fallback, ensuring uptime in disaster scenarios. Nova Biomedical emphasizes microsampling strength, while Masimo leverages signal-processing expertise to add continuous SpO₂ trend lines to intermittent blood-gas results. White-space opportunities persist in microsample neonatal suites, field-deployable rugged analyzers, and platforms that embed AI-driven interpretive commentary for non-specialist users. Smaller innovators such as Sphere Medical and Brolis target those niches with near-real-time spectroscopic sensing and swept-wavelength infrared lasers, respectively.

Blood Gas And Electrolyte Analyzer Industry Leaders

Abbott Laboratories

Medica Corporation

Danaher Corporation (Radiometer)

Siemens Healthcare GmbH

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: bioMérieux acquired SpinChip Diagnostics for EUR 138 million to expand point-of-care immunoassay capabilities.

- May 2024: Nova Biomedical received FDA clearance for micro-capillary sampling on Stat Profile Prime Plus, enabling 11-test panels from 90 µL news-medical..

Global Blood Gas And Electrolyte Analyzer Market Report Scope

As per the scope of the report, blood gas and electrolyte analyzers are useful medical devices for detecting metabolic imbalances and measuring renal and cardiac functions. It is traditionally performed in the clinical chemistry laboratory, but it is now becoming popular and common in point-of-care testing. The Blood Gas and Electrolyte Analyzer Market is segmented by Modality (Benchtop and Portable), Product (Blood Gas Analyzer, Electrolyte Analyzer, and Combined Analyzer), End-User (Centralized Laboratories, Point of Care, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Instruments | Blood Gas Analyzer |

| Electrolyte Analyzer | |

| Combined Blood Gas & Electrolyte Analyzer | |

| Consumables (Cartridges, Reagents & Sensor Strips) |

| Benchtop Systems |

| Portable / Hand-Held Systems |

| Cartridge-Based |

| Electrochemical Sensor |

| Optical / Optode |

| Others (Ion-Selective Electrode, Fluorescent) |

| Hospital Central Laboratories |

| Point-of-Care Testing within Hospitals |

| Ambulance & Emergency Medical Services |

| Diagnostic Laboratories & Clinics |

| Home Healthcare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia- Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type (Value) | Instruments | Blood Gas Analyzer |

| Electrolyte Analyzer | ||

| Combined Blood Gas & Electrolyte Analyzer | ||

| Consumables (Cartridges, Reagents & Sensor Strips) | ||

| By Modality (Value) | Benchtop Systems | |

| Portable / Hand-Held Systems | ||

| By Technology (Value) | Cartridge-Based | |

| Electrochemical Sensor | ||

| Optical / Optode | ||

| Others (Ion-Selective Electrode, Fluorescent) | ||

| By End-User (Value) | Hospital Central Laboratories | |

| Point-of-Care Testing within Hospitals | ||

| Ambulance & Emergency Medical Services | ||

| Diagnostic Laboratories & Clinics | ||

| Home Healthcare Settings | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia- Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Global Blood Gas And Electrolyte Analyzer Market?

The Global Blood Gas And Electrolyte Analyzer Market size is expected to reach USD 2.79 billion in 2026 and grow at a CAGR of 5.34% to reach USD 3.62 billion by 2031.

What is the current Global Blood Gas And Electrolyte Analyzer Market size?

In 2026, the Global Blood Gas And Electrolyte Analyzer Market size is expected to reach USD 2.79 billion.

Who are the key players in Global Blood Gas And Electrolyte Analyzer Market?

Abbott Laboratories, Medica Corporation, Danaher Corporation (Radiometer), Siemens Healthcare GmbH and F. Hoffmann-La Roche Ltd are the major companies operating in the Global Blood Gas And Electrolyte Analyzer Market.

Which is the fastest growing region in Global Blood Gas And Electrolyte Analyzer Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Blood Gas And Electrolyte Analyzer Market?

In 2025, the North America accounts for the largest market share in Global Blood Gas And Electrolyte Analyzer Market.

Page last updated on: