Biomimetic Medical Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

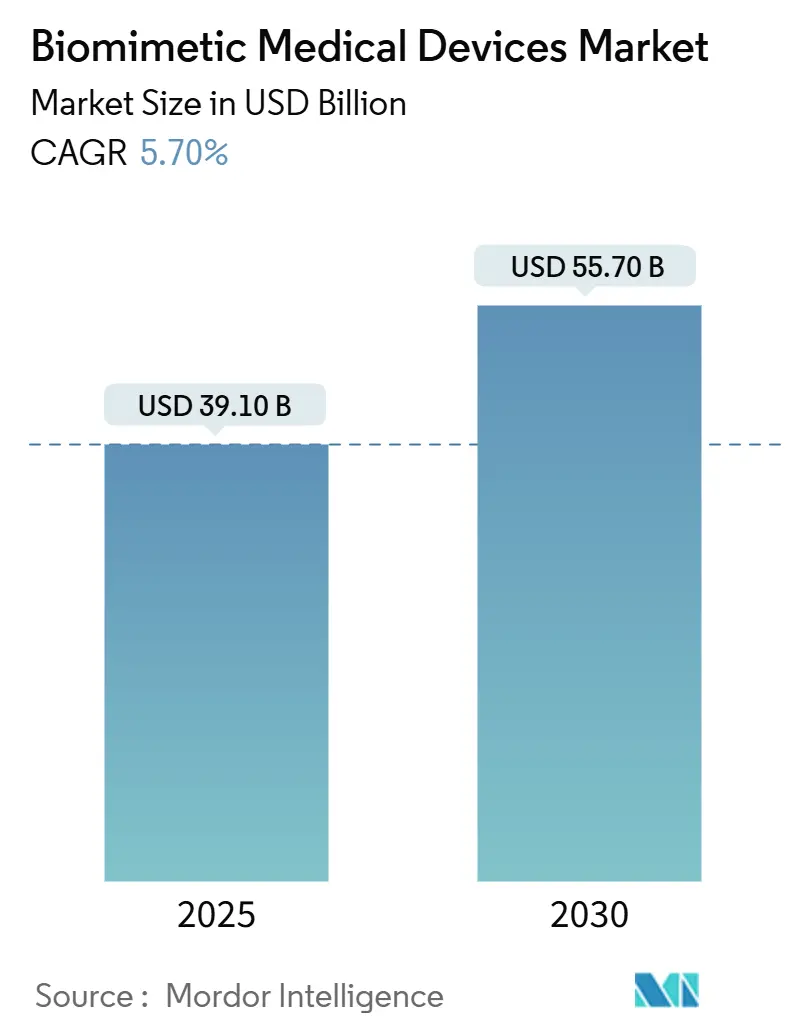

| Market Size (2025) | USD 39.10 Billion |

| Market Size (2030) | USD 55.70 Billion |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomimetic Medical Devices Market Analysis by Mordor Intelligence

The biomimetic medical devices market size stood at USD 39.1 billion in 2025 and is projected to reach USD 55.7 billion by 2030, registering a 7.6% CAGR. Strong demand for implants that replicate natural biomechanics, rapid advances in nanotechnology-enabled surfaces, and wider adoption of 3D bioprinting collectively underpin this expansion of the biomimetic medical devices market. Graphene oxide coatings that improve osseointegration, the clinical arrival of AI-guided smart implants, and favorable reimbursement for bone and dental replacements are all reinforcing the commercial runway ahead for the biomimetic medical devices market. The surge in tissue-engineering procedures, especially those reliant on patient-specific scaffolds, is widening clinical indications and broadening hospital procurement patterns across the biomimetic medical devices market. Meanwhile, rising procedure volumes for orthopedic and dental implants, coupled with robust venture funding for biohybrid sensor platforms, continue to attract new entrants and intensify competition in the biomimetic medical devices market.

Key Report Takeaways

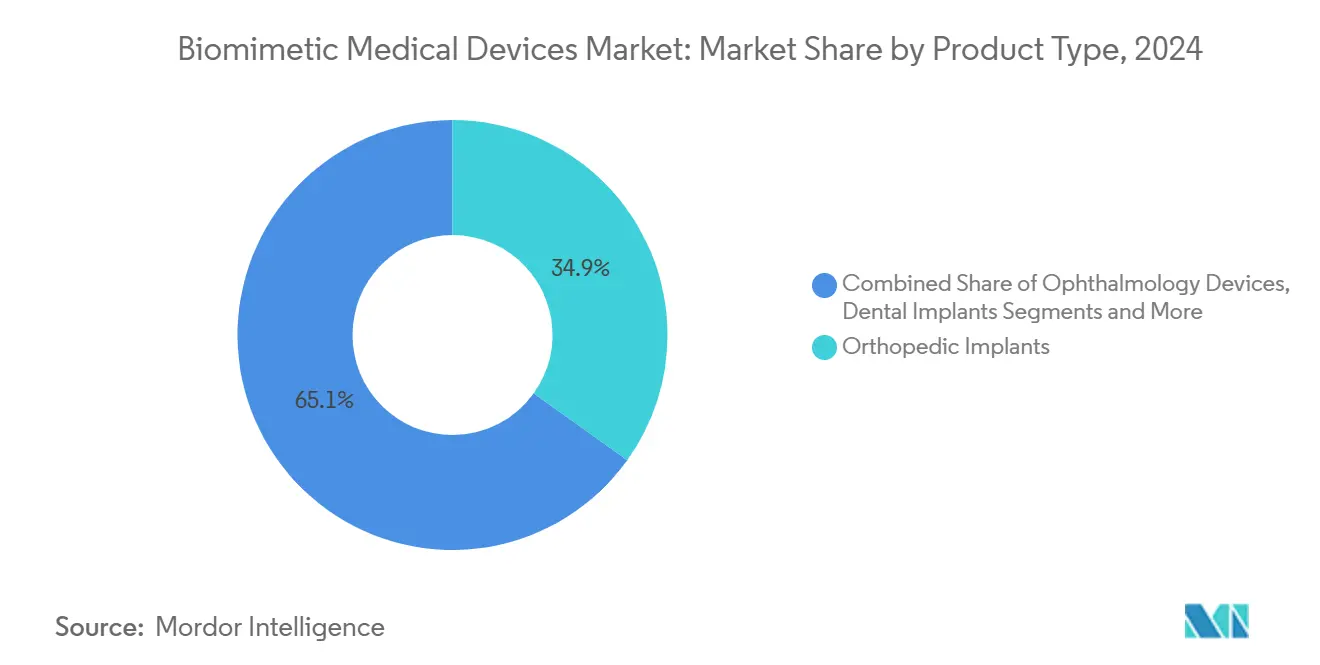

- By product type, orthopedic implants led with 34.9% biomimetic medical devices market share in 2024, while tissue-engineering scaffolds are forecast to expand at an 11.6% CAGR through 2030.

- By application, tissue engineering accounted for 24.0% of the biomimetic medical devices market size in 2024, and neurology applications are advancing at an 11.9% CAGR to 2030.

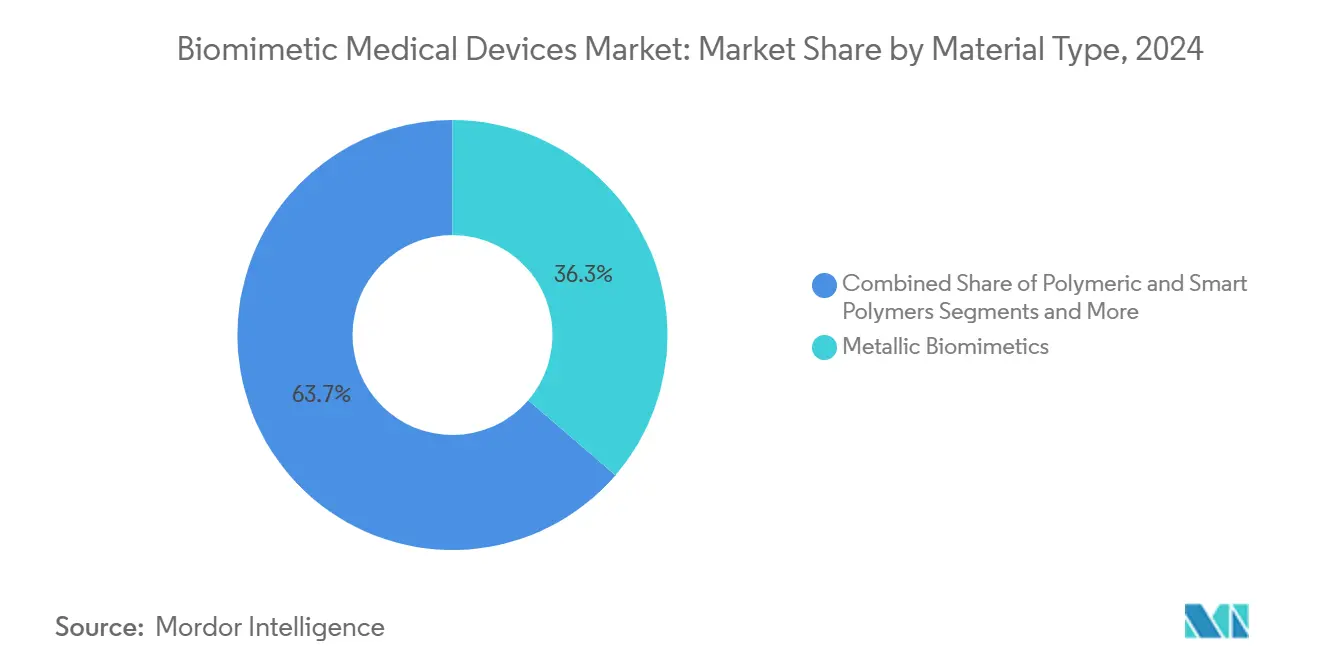

- By material type, metallic biomimetics held 36.3% revenue share in 2024, whereas natural biomaterials are projected to grow at a 12.0% CAGR through 2030.

- By end user, hospitals commanded 49.4% share of the biomimetic medical devices market size in 2024; research institutes represent the fastest-growing channel at 9.9% CAGR.

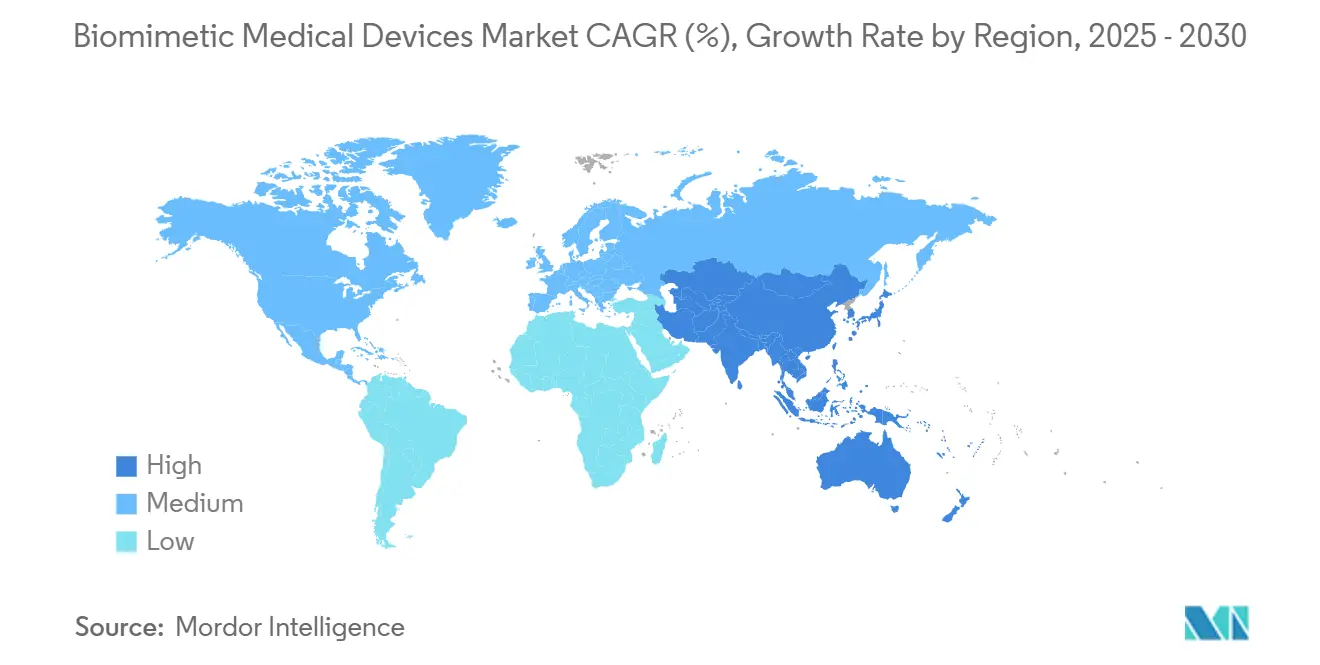

- By geography, North America maintaineda 43.3% share in 2024, while Asia Pacific is forecast to record a 9.0% CAGR to 2030.

Global Biomimetic Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nanotechnology-Enabled Precision Surfaces | +1.80% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Expansion Of Tissue-Engineering Procedures | +2.10% | Global, led by Asia Pacific & North America | Long term (≥ 4 years) |

| Rising Orthopedic And Dental Implant Volumes | +1.50% | Global, aging populations in developed markets | Short term (≤ 2 years) |

| Adoption Of Biomimetic Drug-Delivery Microfluidics | +1.20% | North America & EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Plant-Derived Decellularized Scaffolds | +0.70% | Global, with research concentration in EU & North America | Long term (≥ 4 years) |

| AI And IoT-Linked Smart Biomimetic Implants | +0.90% | North America & Asia Pacific core markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nanotechnology-Enabled Precision Surfaces Drive Bio Integration Excellence

Nanoscale surface engineering has moved beyond laboratory trials into routine clinical deployment, with graphene derivatives demonstrating superior mechanical strength and antibacterial performance in dental implants[1]MDPI Editorial, “Emerging Trends in Biomimetic Medical Devices,” mdpi.com . By replicating natural bone nano topography, these coatings reduce implant failure by 40% versus conventional surfaces, while nanoparticle layers enable controlled release of angiogenic factors that accelerate osseointegration. The US FDA recently cleared a nanoparticle-enhanced tissue-engineered vascular graft, underscoring regulators' confidence in nanoscale biomimicry for intravascular use.

Tissue-engineering Procedures Reshape the Regenerative Medicine Landscape

Three-dimensional bioprinting now creates patient-specific constructs that mimic complex tissue architecture, with silk-fibroin scaffolds demonstrating rapid wound closure and successful skin grafting in ongoing clinical trials[2]Christopher Murphy, “Cyclodextrin-Hydrogel Smart Drug Carriers,” frontiersin.org . Electrospinning techniques allow precise pore-size control, with 20–120 µm ideal for dermal regeneration and up to 700 µm for cancellous bone repair. Coral-inspired calcium phosphate grafts have achieved complete bone defect healing within six months, eliminating the need for autografts.

AI Integration Transforms Smart Implant Functionality

Artificial intelligence now tailors real-time device behavior: neural interfaces enable direct cortical control of robotic limbs. Machine-learning algorithms developed at Harvard doubled the propulsion efficiency of biohybrid swimming rays compared with static biomimetic designs. Neuromorphic processors embedded within prostheses deliver adaptive stimulation with sub-millisecond latency, improving functional recovery in stroke rehabilitation scenarios.

Plant-derived Materials Unlock Sustainable Biomimetic Solutions

Dragline silk produced through recombinant fermentation provides strength-to-density ratios comparable to high-grade titanium, yet remains fully biodegradable. Decellularized plant scaffolds have shown favorable hemodynamics in cardiovascular patches[3]Shengjie Ling, “Silk Fibroin for Biomimetic Vascular Scaffolds,” Nature, nature.com. Multifunctional nanohybrids synthesized from lignin and silk proteins are pushing biosensor sensitivity into femtomolar ranges while reducing environmental footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Region Regulatory Approvals | -1.40% | Global, particularly severe in EU under MDR | Short term (≤ 2 years) |

| High Production And Customization Costs | -0.90% | Global, affecting SMEs disproportionately | Medium term (2-4 years) |

| Nanotoxicity And Long-Term Safety Unknowns | -0.60% | Global, with stricter oversight in North America & EU | Long term (≥ 4 years) |

| Limited Reimbursement Frameworks For Novel Implants | -0.80% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity Constrains Market Access

The European Union’s Medical Device Regulation has lengthened certification cycles, prompting many companies to reduce product portfolios while prioritizing higher-margin implants. Concurrently, workforce reductions at major regulators are elongating FDA review queues, delaying first-in-class biomimetic submissions, and raising developers' holding costs. These dynamics collectively shave growth from the biomimetic medical devices market by restricting the timely commercialization of innovative designs.

Manufacturing Cost Pressures Challenge Scalability

Device makers currently spend 20% of revenue on logistics and raw materials, a figure amplified by elevated metal powder prices and specialized clean-room requirements. Powder-bed fusion and directed energy deposition remain central to personalized implant fabrication, yet post-processing and validation can double production time. Nevertheless, cost-optimized 3D-printing protocols and IoT-enabled supply-chain monitoring are beginning to offset price headwinds, pointing to medium-term relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Orthopedic Implants Anchor Demand, Scaffolds Accelerate Growth

Orthopedic implants generated the most significant contribution to the biomimetic medical devices market size, reflecting 34.9% revenue share in 2024 and underpinned by hip and knee replacements in aging populations. Neural-network design frameworks now reduce femoral stem stress shielding by 50%, extending implant longevity. Dental implant uptake is expanding with graphene-oxide surfaces that cut peri-implantitis risk, aligning with the broader digitization of the biomimetic medical devices market.

Tissue-engineering scaffolds hold the strongest momentum, posting an 11.6% CAGR through 2030 as 3D-printed constructs transition into commercial wound-healing and bone-void fillers. Cardiovascular patches and bioresorbable stents are likewise advancing, supported by the recent FDA clearance of a peripheral artery bioresorbable scaffold. Drug-delivery devices built on cyclodextrin-hydrogel hybrids now respond to pH and enzymatic cues, while bionic prosthetics using agonist-antagonist myoneural interfaces restore near-natural gait patterns.

By Application: Tissue Engineering Dominates, Neurology Surges

Tissue-engineering and regenerative medicine applications held 24.0% of the biomimetic medical devices market share in 2024, driven by hospital adoption of patient-specific skin, bone, and vascular constructs. Nanozyme-embedded wound dressings that actively modulate the healing microenvironment are pushing clinical outcomes beyond traditional care standards.

Neurology devices register the fastest growth at 11.9% CAGR, reflecting breakthroughs in closed-loop deep-brain stimulators and multipoint neural probes that sense and modulate cortical activity simultaneously. Plastic and reconstructive surgery further leverages coral-inspired bone substitutes for craniofacial defects, while sports medicine adopts 3D-printed talus replacements that recorded 96.3% device survivorship at two-year follow-up.

By Material Type: Metals Retain Volume Leadership, Natural Biomaterials Gain Ground

Metallic implants remain the backbone of the biomimetic medical devices market, commanding 36.3% share due to established supply chains and high fatigue strength. Titanium dioxide nanocoatings and hydroxyapatite layers continue to lift osseointegration metrics in dental restoration studies.

Natural biomaterials represent the fastest-growing class with a 12.0% CAGR, propelled by sustainability mandates and strong patient acceptance. Recombinant spider silk and collagen-elastin composites match synthetic polymer toughness while enabling full degradation, lowering long-term foreign-body risks. Smart polymers integrating cyclodextrin and chitosan support targeted oncology drug release, further widening the product palette available within the biomimetic medical devices market.

By End User: Hospitals Dominate, Research Institutes Expand Pipeline

Hospitals accounted for 49.4% of the biomimetic medical devices market size in 2024, reflecting their role as primary implantation sites and recipients of bundled reimbursement payments. Robotic-assisted arthroplasty and image-guided cardiac interventions are embedding biomimetic components at scale, accelerating replacement cycles.

Research and academic institutes deliver the highest growth at 9.9% CAGR to 2030, fueling innovation via neuroprosthetic trials and organ-on-chip platforms. Collaborative hubs at institutions such as Carnegie Mellon University and the Auckland Bioengineering Institute integrate computational models with bioprinting, producing rapid prototyping advantages that ripple across the biomimetic medical devices industry.

Geography Analysis

North America led the biomimetic medical devices market with 43.3% revenue share in 2024, supported by a mature reimbursement structure, extensive surgeon training programs, and early regulatory clearances for advanced implants. Abbott’s Tendyne transcatheter mitral valve replacement system illustrates the region’s commitment to minimally invasive biomimetic solutions, enabling valve replacement without open-heart surgery. Robust venture funding and strategic partnerships between hospitals and device manufacturers further consolidate North American leadership, reinforcing the regional stake in the biomimetic medical devices market.

Asia Pacific recorded the fastest trajectory at a 9.0% CAGR, driven by rising healthcare expenditure, expanding middle-class demand, and national strategies that prioritize advanced manufacturing of medical hardware. China’s dominance in graphene dental implant patent filings, Japan’s precision machining expertise, and South Korea’s aggressive AI adoption are reshaping competitive dynamics. India couples cost-effective 3D-printing infrastructure with a large orthopedic procedure base, positioning the country as a growing exporter of personalized implants.

Europe navigates a complex regulatory transition but remains an R&D powerhouse. Germany, France, and the United Kingdom host public-funded projects such as bird-inspired flow-control heart valves that reduce thrombogenesis. Backlogs under the EU Medical Device Regulation have slowed product launches, yet consortiums targeting harmonized testing pathways aim to shorten approval timelines. Scandinavian countries pioneer sustainable biomaterials and circular-economy device recovery schemes, reinforcing Europe’s role in eco-centric growth themes within the biomimetic medical devices market.

Competitive Landscape

The competitive environment balances consolidation with vibrant niche innovation. Large diversified firms use scale to fund multiyear R&D pipelines and secure global distribution, while specialist start-ups concentrate on breakthrough materials and neuroelectronic interfaces. Stryker’s USD 4.9 billion acquisition of Inari Medical granted immediate entry into mechanical thrombectomy for venous thromboembolism, reflecting opportunistic expansion strategies. Johnson & Johnson’s purchase of Abiomed similarly strengthened its cardiovascular franchise, indicating high-value targets remain central to portfolio renewal across the biomimetic medical devices industry.

Technology integration remains the primary differentiator. Abbott commercially deployed the first dual-chamber leadless pacemaker and secured pivotal trials for conduction-system pacing ICD leads, unlocking new physics for cardiac rhythm management. Zimmer Biomet invested in data-driven orthopedics, merging sensor-equipped implants with cloud analytics to guide post-operative rehabilitation. Competitive pressure now centers on delivering validated clinical superiority alongside digital-health ecosystems, an area where start-ups armed with AI algorithms and flexible architecture sensors pose meaningful disruption.

White-space segments such as closed-loop organ neuroprosthetics and fully bioresorbable vascular grafts offer room for outsized gains. Academic spin-offs, including Columbia University’s python-teeth inspired rotator cuff anchor and MIT’s neural prosthetic interface, showcase a pipeline of high-impact devices moving toward regulatory submission. Strategic alliances between component suppliers, software firms, and contract manufacturing partners are expected to accelerate time-to-market and broaden intervention portfolios.

Biomimetic Medical Devices Industry Leaders

Johnson & Johnson (DePuy Synthes)

Medtronic Plc

Johnson & Johnson (DePuy Synthes Medtronic Stryker Corporation

Abbott Laboratories

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Abbott received FDA approval for the Tendyne transcatheter mitral valve replacement system, the first device enabling mitral valve replacement without open-heart surgery. This system addresses patients with severe mitral annular calcification who are not surgical candidates.

- May 2025: Zimmer Biomet reported Q1 2025 revenue growth of 1.1%, driven by innovations in hip and knee product lines, including the Z1 Triple-Taper Femoral Hip System and Oxford Cementless Partial Knee, with updated guidance reflecting the Paragon 28 acquisition impact

- April 2025: Abbott initiated the ASCEND CSP pivotal clinical trial for its investigational Conduction System Pacing ICD lead, following successful first-in-world leadless left bundle branch area pacing procedures that received FDA Breakthrough Device Designation.

- March 2025: Abbott announced two-year TRILUMINATE Pivotal trial data showing that the TriClip transcatheter edge-to-edge repair system reduced heart failure hospitalizations by 27% and that 84% of patients reached moderate or less tricuspid regurgitation grade.

Global Biomimetic Medical Devices Market Report Scope

As per scope, biomimetic medical devices are healthcare technologies designed to mimic natural biological structures or functions. They include implants, prosthetics, stents, lenses, and neural interfaces that replicate the body’s tissues or organs.

The Biomimetic Medical Devices Market is Segmented by Product Type (Orthopedic Implants, Ophthalmology Devices, and More), Application (Plastic & Reconstructive Surgery, Wound Healing, and More), Material Type (Metallic Biomimetics, Polymeric, and More), End User (Hospitals, Specialty Clinics, and More), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Orthopedic Implants |

| Ophthalmology Devices |

| Dental Implants |

| Cardiovascular Stents & Patches |

| Tissue-Engineering Scaffolds |

| Drug-Delivery Systems |

| Prosthetics & Bionics |

| Other Product Types |

| Plastic & Reconstructive Surgery |

| Wound Healing |

| Tissue Engineering & Regenerative Medicine |

| Orthopedic & Sports Medicine |

| Cardiovascular Repair |

| Dental Restoration |

| Neurology & Sensorimotor |

| Other Applications |

| Metallic Biomimetics |

| Polymeric & Smart Polymers |

| Ceramic / Bioactive Glasses |

| Natural / Bio-Derived (e.g., Silk, Plant) |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Orthopedic Implants | |

| Ophthalmology Devices | ||

| Dental Implants | ||

| Cardiovascular Stents & Patches | ||

| Tissue-Engineering Scaffolds | ||

| Drug-Delivery Systems | ||

| Prosthetics & Bionics | ||

| Other Product Types | ||

| By Application | Plastic & Reconstructive Surgery | |

| Wound Healing | ||

| Tissue Engineering & Regenerative Medicine | ||

| Orthopedic & Sports Medicine | ||

| Cardiovascular Repair | ||

| Dental Restoration | ||

| Neurology & Sensorimotor | ||

| Other Applications | ||

| By Material Type | Metallic Biomimetics | |

| Polymeric & Smart Polymers | ||

| Ceramic / Bioactive Glasses | ||

| Natural / Bio-Derived (e.g., Silk, Plant) | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Research & Academic Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the biomimetic medical devices market?

The biomimetic medical devices market size reached USD 39.1 billion in 2025 and is forecast to hit USD 55.7 billion by 2030.

Which product category holds the largest share of the biomimetic medical devices market?

Orthopedic implants lead the market, accounting for 34.9% revenue share in 2024.

Which region is growing fastest in the biomimetic medical devices industry?

Asia Pacific is the fastest-growing region, expected to record a 9.0% CAGR through 2030.

What material segment is expanding most rapidly?

AI optimizes implant design in real time, doubles biohybrid propulsion efficiency, and enables closed-loop neural prostheses, elevating clinical performance and patient outcomes.

Page last updated on: