Bag Filter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.29 Billion |

| Market Size (2031) | USD 21.98 Billion |

| Growth Rate (2026 - 2031) | 8.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

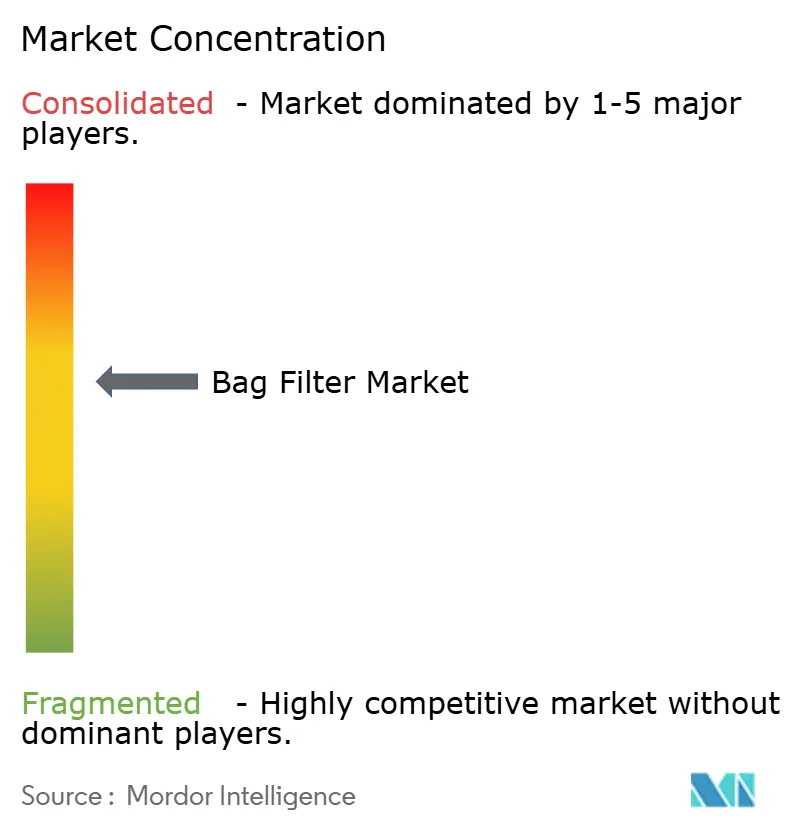

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bag Filter Market Analysis by Mordor Intelligence

The Bag Filter Market size was valued at USD 13.04 billion in 2025 and is estimated to grow from USD 14.29 billion in 2026 to reach USD 21.98 billion by 2031, at a CAGR of 8.99% during the forecast period (2026-2031). Equipment demand benefits from strict particulate-matter limits across coal, cement, and mining facilities, while retrofit activity in power, cement, and refinery stacks sustains aftermarket sales. Consolidation among global suppliers accelerates because aftermarket revenues account for more than 80% of their total filtration turnover, insulating earnings from cyclic capital spending. The pivot toward PFAS-free coatings in North America and the European Union creates parallel material streams that reward vertically integrated players able to certify both PTFE and fluorine-free products. Meanwhile, predictive-maintenance sensors embedded in pulse-jet systems cut unplanned outages and compressed-air consumption, raising the total lifetime value of connected baghouse units.

Key Report Takeaways

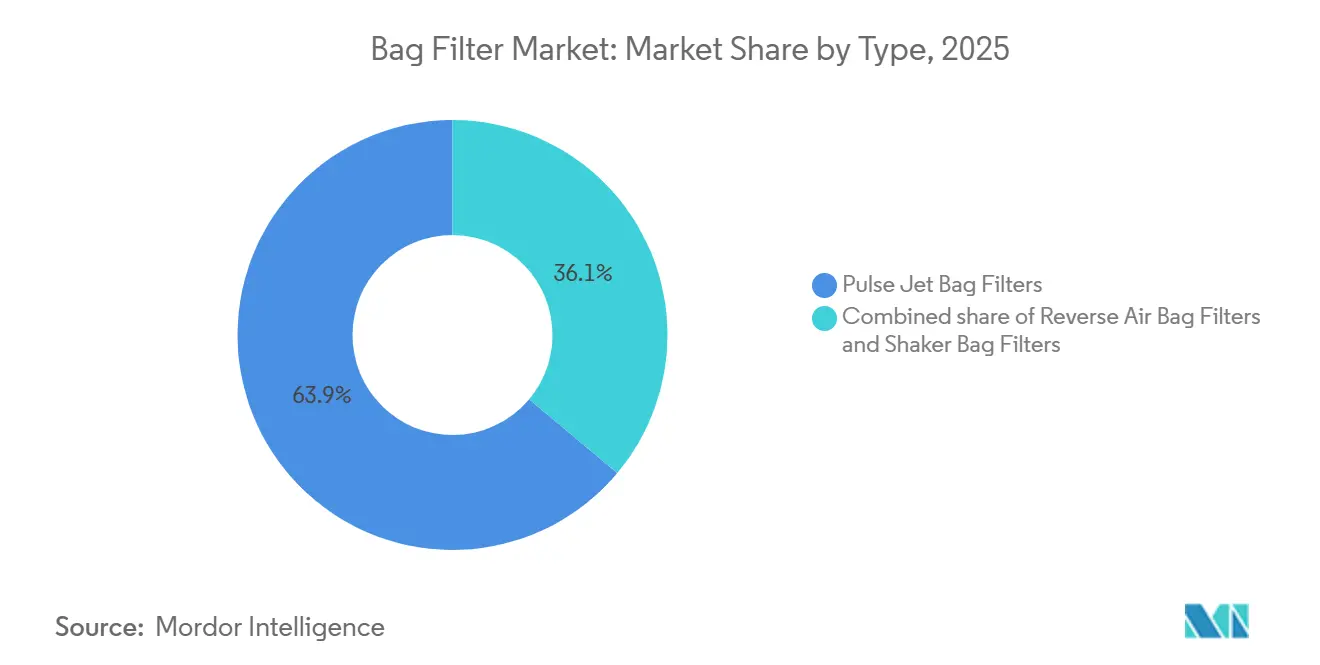

- By type, pulse-jet systems led with 63.9% of bag filter market share in 2025 and are forecast to advance at a 9.5% CAGR through 2031.

- By filter media, non-woven felts accounted for 55.1% share of the bag filter market size in 2025, while glass-fiber media is projected to deliver the fastest 9.4% CAGR to 2031.

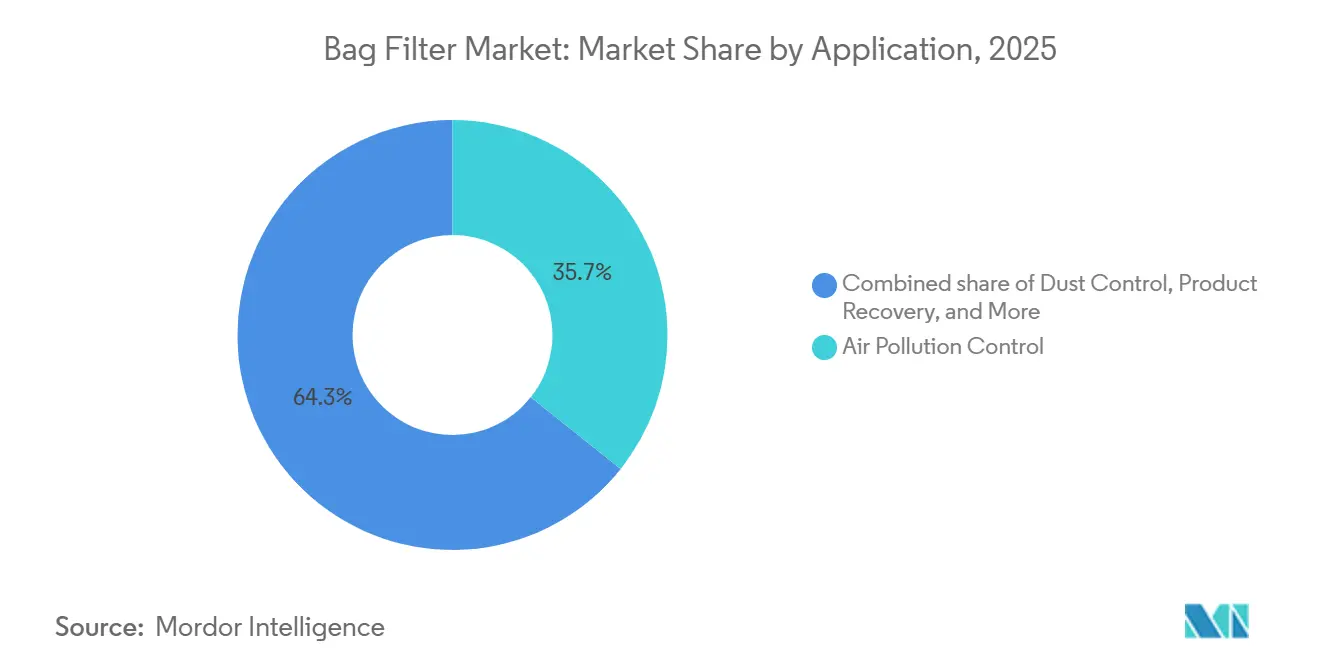

- By application, air-pollution control represented 35.7% of revenue in 2025; product recovery is poised to grow at a 10.2% CAGR through 2031.

- By end-user, power generation held 39.8% share in 2025, whereas chemical and petrochemical installations are set to post the highest 10.7% CAGR by 2031.

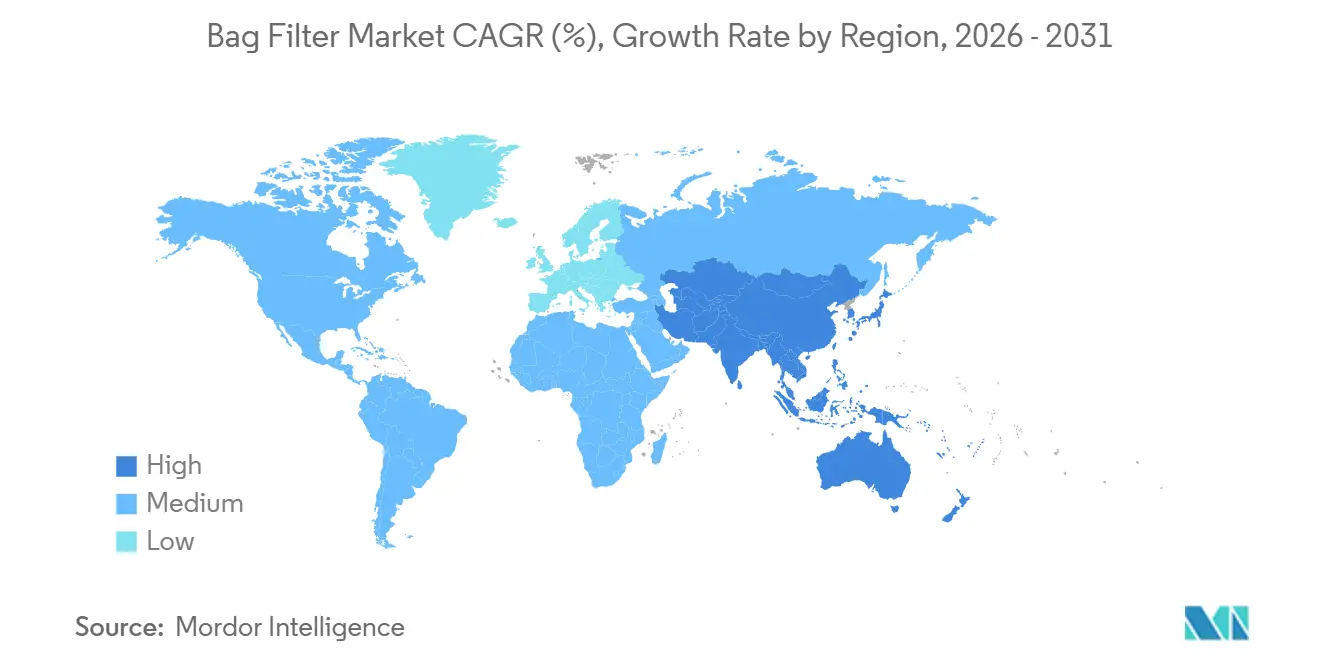

- By geography, North America captured 40.3% revenue in 2025, yet Asia-Pacific is projected to expand at an 11.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bag Filter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter industrial emission regulations | +2.1% | Global, with APAC core enforcement in China, India; EU IED tightening; U.S. state-level PFAS bans | Medium term (2-4 years) |

| Expansion of coal- & biomass-fired capacity in emerging Asia | +2.5% | APAC core (China, India, ASEAN); spill-over to South Asia for biomass co-firing | Short term (≤ 2 years) |

| Capacity additions in cement & mining industries | +1.4% | APAC (India, Indonesia, Vietnam); MEA (Egypt, Saudi Arabia); South America (Brazil) | Medium term (2-4 years) |

| Retrofit shift from ESP to baghouse systems | +1.1% | Global, concentrated in APAC cement belt and North America coal plants | Medium term (2-4 years) |

| Predictive-maintenance sensor adoption in baghouses | +0.8% | North America & EU early adopters; APAC industrial clusters following | Long term (≥ 4 years) |

| Solvent-recovery bag filters in pharmaceutical peptide lines | +0.6% | North America, EU, India pharma hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Industrial Emission Regulations

China enforces sub-30 mg/Nm³ particulate limits for new coal plants, while India mandates sub-50 mg/Nm³ for cement kilns, making fabric filtration compulsory for compliance. The European Union’s Industrial Emissions Directive revision reduces permitted dust thresholds, driving retrofits across metals and waste-to-energy sites. Illinois banned PTFE textiles effective January 2025, and the U.S. EPA now requires PFAS usage disclosure, pushing research into plasma-treated polyester and nanofiber felts. Suppliers must therefore manage dual portfolios, PTFE for Asia and fluorine-free for Western markets, to remain certified under ISO 14001 and regional air-quality codes. Vertically integrated companies that control yarn extrusion, membrane casting, and post-treatment are best placed to navigate this split.

Expansion of Coal and Biomass Capacity in Emerging Asia

China commissioned 78 GW of new coal units in 2025 and proposed another 161 GW during the same year, with a 291 GW pipeline ensuring sustained baghouse demand [1]Global Energy Monitor, “Global Coal Plant Tracker,” globalenergymonitor.org. India’s cement producers plan 160-170 million ton of grinding additions in fiscal 2026-28, triple their prior three-year pace, while ASEAN utilities co-fire biomass, which creates ash chemistry that requires redundant pulse-jet lines for reliability. These parallel investments anchor high-temperature, high-volume bag filter market growth and offset coal retirements elsewhere.

Capacity Additions in Cement and Mining Industries

India’s UltraTech, JK Lakshmi, and Jindal Cement collectively channel more than USD 720 million into kiln and grinding line upgrades that specify pulse-jet collectors rated up to 1 million m³/hr. Vietnam’s cement output rose 11% year over year in 2025, and Rio Tinto’s Paraburdoo mine operates a 318,600 m³/hr baghouse that showcases the scale needed for open-pit ore handling. New dedusting projects increasingly include predictive sensors and corrosion-resistant felts that limit unplanned downtime and media wear.

Retrofit Shift from ESP to Baghouse Systems

PT Semen Padang’s Indarung IV kiln retrofit cut particulate emissions from 40 mg/Nm³ to 9 mg/Nm³, validating baghouse conversions where ESP plates blind under alternative fuels. More than 650 hybrid ESP-bag houses operate in global cement plants, pre-removing coarse ash to extend bag life by 30% and lowering cleaning air by 20%. Greenfield projects prefer full pulse-jet designs, while space-constrained brownfields adopt hybrid cartridge-ESP units, segmenting the retrofit opportunity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slowdown of coal power build-out in OECD | -0.9% | North America, EU, Japan, Australia | Short term (≤ 2 years) |

| Volatile prices of polyester/PTFE filter media | -0.7% | Global supply chains; acute in regions dependent on imported media | Short term (≤ 2 years) |

| Hybrid cartridge-ESP solutions eroding bag filter share | -0.5% | Global, with faster adoption in space-constrained industrial parks (EU, Japan) | Medium term (2-4 years) |

| PFAS concerns over PTFE-coated bags | -0.4% | North America (Illinois, New York bans); EU REACH restrictions; minimal APAC impact near-term | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slowdown of Coal Power Build-Out in OECD

The United States and the European Union retire more coal units than they build, and coal generated less than 20% of U.S. electricity in 2025 [2]U.S. Energy Information Administration, “Electric Power Monthly,” eia.gov. Bag filter demand in these regions, therefore, tilts toward retrofits and aftermarket bags, pressuring equipment sales but sustaining consumables revenue for diversified suppliers.

Volatile Prices of Polyester and PTFE

Polyester staple fiber swung between USD 1,200–1,600 per ton during 2024-25, while PTFE resin prices moved sharply on fluorspar shortages in China [3]Fiber2Fashion, “Polyester Staple Fibre Price Trend,” fiber2fashion.com. Fixed-price contracts in competitive cement bids squeeze converter margins, making vertical integration or price indexation clauses critical risk-mitigation levers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pulse Jet Systems Anchor High-Throughput Installations

Pulse-jet units captured 63.9% of 2025 revenue and are on track for a 9.5% CAGR through 2031, supported by multi-gigawatt coal plants in China that require continuous cleaning and sub-30 mg/Nm³ guarantees. Pulse-jet designs integrate differential-pressure sensors that optimize solenoid timing, saving up to 15% compressed air per year. Reverse-air systems serve fragile powder lines in pharmaceuticals and specialty chemicals, while shaker units persist in sawmills and grain elevators where simplicity trumps performance. Freudenberg’s 2026 low-pressure-drop media further improve energy efficiency in pulse-jet installations. Centralized pulse-jet collectors that link several dust sources, as promoted in the GEMCO wood-pellet guide, cut installed cost by 30% and demonstrate why this configuration dominates the bag filter market.

By Filter Media: Non-Woven Felts Balance Cost and Performance

Non-woven felts held 55.1% share in 2025, thanks to scalable needle-punch production that keeps cost 25% below woven fabrics while allowing PTFE or plasma top-layers for hydrophobicity. Hangzhou Hengke’s 500,000-piece monthly capacity exemplifies the scale that underpins global supply. Glass fiber supports waste-to-energy stacks above 260 °C, though brittleness and acid attack limit volumes. Automated heat-welding of thermoplastic felts removes stitch holes, boosting burst strength by 30% and making non-woven designs attractive for sterile-grade food and pharma bags. The shift to PFAS-free coatings accelerates investments in plasma chambers and nanofiber lines, sustaining a 9.4% CAGR for non-woven media through 2031.

By Application: Product Recovery Delivers Premium Margins

Air-pollution control remained the largest slice at 35.7% in 2025, yet product recovery is forecast to grow 10.2% annually to 2031 as solvent recycling in peptide lines justifies bags priced 50-100% above commodity dust units. Sefar’s GMP bags and Parker’s single-use skids recover solvents worth hundreds of thousands of USD per batch, while chemical catalyst recovery slashes raw-material expense by 20%. Dust-control stations in cement and grain handling continue to drive volume but face price pressure. Water-treatment bags remove 1 µm solids in municipal and refinery streams, but permanent scraper filters from Shanghai Vithy start to displace disposables where zero-waste targets apply.

By End-User: Chemical and Petrochemical Lines Outpace Power

Power plants provided 39.8% of 2025 turnover, yet chemical and petrochemical users will deliver the highest 10.7% CAGR, driven by catalyst recovery and VOC caps in China and the Middle East. DrM’s FUNDABAC enclosed filters enable solvent reuse and dry-cake catalyst discharge across epoxy resin and PTA units, cutting disposal 60%. Cement remains the second-largest market as India and ASEAN add grinding lines that specify pulse-jet collectors and hybrid ESP retrofits. Pharmaceutical plants demand stainless housings and 0.2 µm absolute ratings, commanding premium unit pricing that offsets their relatively small volume share.

Geography Analysis

North America generated 40.3% of 2025 revenue, supported by coal-to-gas retrofits, PFAS legislation, and dense pharmaceutical clusters in New Jersey and North Carolina. Illinois’ PTFE ban and EPA disclosure rules force suppliers to qualify fluorine-free felts, favoring vertically integrated producers with in-house plasma technology. Donaldson’s USD 820 million Facet deal underscores the push for consumables exposure in a mature equipment market.

Asia-Pacific will post an 11.6% CAGR to 2031, led by China’s 78 GW of 2025 coal additions and India’s 160-170 million ton cement expansion pipeline. Tight particulate standards of 30 mg/Nm³ in China and 50 mg/Nm³ in Indian kilns cement the need for fabric filtration. ASEAN biomass co-firing introduces corrosive ash that drives demand for chemically resistant felts and redundant baghouses.

Europe tightens dust limits under the updated Industrial Emissions Directive and advances PFAS bans, favoring PFAS-free media and predictive sensors. LoRaWAN deployments across UK factories prove the region’s leadership in digital maintenance. Russia, South America, and the Middle East add mining, cement, and petrochemical projects where Chinese OEMs compete aggressively on capital cost.

Competitive Landscape

The Bag Filter Market is moderately concentrated. Donaldson, Parker-Hannifin, Camfil, Babcock & Wilcox, and Eaton control about 37% of global revenue, while hundreds of regional converters fill application niches. Parker’s USD 9.25 billion Filtration Group purchase created a USD 2 billion filtration unit with 85% aftermarket mix, and Donaldson’s Facet deal maintains a similar consumables focus. Technology differentiation now centers on PFAS-free membranes such as H&V’s NANOWEB and AGC Plasma-treated felts, along with IoT-enabled collectors like Camfil’s CC X-Series that connect to building management systems. Chinese suppliers such as Hangzhou Hengke challenge incumbents on price and delivery, shipping 500,000 polyester bags a month at a 20-30% discount. Hybrid cartridge-ESP innovators like ELEX win projects in Europe and Japan, where power costs make pressure drop critical. The market therefore splits between full-service multinationals offering lifecycle contracts and low-cost regional manufacturers targeting first-cost-sensitive buyers in cement and mining.

Bag Filter Industry Leaders

Donaldson Company Inc.

Parker-Hannifin Corp.

Camfil AB

Babcock & Wilcox Enterprises

Eaton Corp. plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Tri-Mer Corporation has launched a new range of industrial bag filters designed to handle gas volumes of up to 880,000 acfm. The system accommodates various filter media options, including PTFE, Nomex, fiberglass, and aramid, and aims to enhance cleaning efficiency while increasing the service life of filter bags.

- February 2026: Cleanova introduced Sentinel Connect™, an Industrial IoT monitoring platform designed for baghouses and dust collectors. The platform offers real-time performance monitoring, predictive maintenance insights, and remote diagnostics, aiming to minimize downtime and enhance filtration efficiency.

- January 2026: CleanAir Group introduced EcoSense, a sensor-based monitoring solution designed for integration with baghouse filters. This technology facilitates detailed monitoring of operating conditions, cleaning efficiency, and component health, enabling operators to optimize maintenance and energy usage.

- January 2025: Allied Filter Systems was sold to private-equity-backed Cleanova, enhancing Cleanova’s global platform.

Global Bag Filter Market Report Scope

A bag filter is an air pollution control device used in industrial processes to remove dust and particulate matter from gas streams. It operates by passing contaminated air through fabric filter bags, which trap particles while allowing clean air to exit. This high-efficiency solution is commonly utilized in industries such as cement, power, and manufacturing.

The battery scrap market is segmented by type, application, end-user, and geography. By type, the market is segmented into lead-acid, lithium-ion, nickel-based, and other chemistries. By application, the market is segmented into automotive, industrial motive-power, consumer electronics, stationary energy-storage, aerospace and defense, and other niche uses. By end-user, the market is segmented into dedicated recycling facilities, OEM take-back programs, utilities, third-party waste-management providers, and informal collectors. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report also covers the market sizes and forecasts for the battery scrap market across major countries within these regions. For each segment, the market sizing and forecasts have been carried out on the basis of value (USD).

| Pulse Jet Bag Filters |

| Reverse Air Bag Filters |

| Shaker Bag Filters |

| Woven Media |

| Non-Woven Media |

| Glass Fiber Media |

| Others |

| Dust Control |

| Air Pollution Control |

| Product Recovery |

| Water Treatment |

| Others |

| Power Generation |

| Cement Production |

| Chemical and Petrochemicals |

| Pharmaceutical and Biotech |

| Food and Beverage Processing |

| Mining and Metallurgy |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Pulse Jet Bag Filters | |

| Reverse Air Bag Filters | ||

| Shaker Bag Filters | ||

| By Filter Media | Woven Media | |

| Non-Woven Media | ||

| Glass Fiber Media | ||

| Others | ||

| By Application | Dust Control | |

| Air Pollution Control | ||

| Product Recovery | ||

| Water Treatment | ||

| Others | ||

| By End-user | Power Generation | |

| Cement Production | ||

| Chemical and Petrochemicals | ||

| Pharmaceutical and Biotech | ||

| Food and Beverage Processing | ||

| Mining and Metallurgy | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the bag filter market be by 2031?

The bag filter market size is forecast to reach USD 21.98 billion by 2031, growing at an 8.99% CAGR from 2026.

Which filter type dominates new industrial installations?

Pulse-jet baghouses dominate with 63.9% share in 2025 because they handle high dust loads and support automated cleaning cycles.

Why are chemical and petrochemical plants boosting demand?

Stricter VOC limits and the economic value of catalyst recovery push these plants toward enclosed bag filters, driving a 10.7% CAGR through 2031.

What region offers the fastest growth opportunity?

Asia-Pacific leads with an 11.6% CAGR thanks to large coal-fired power additions and rapid cement capacity expansion in China and India.

How are PFAS regulations shaping filter media choices?

U.S. state bans and EU REACH rules accelerate the shift from PTFE coatings to plasma-treated polyester and nanofiber felts despite higher costs.

Page last updated on: