Automotive Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.70 Billion |

| Market Size (2031) | USD 32.98 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

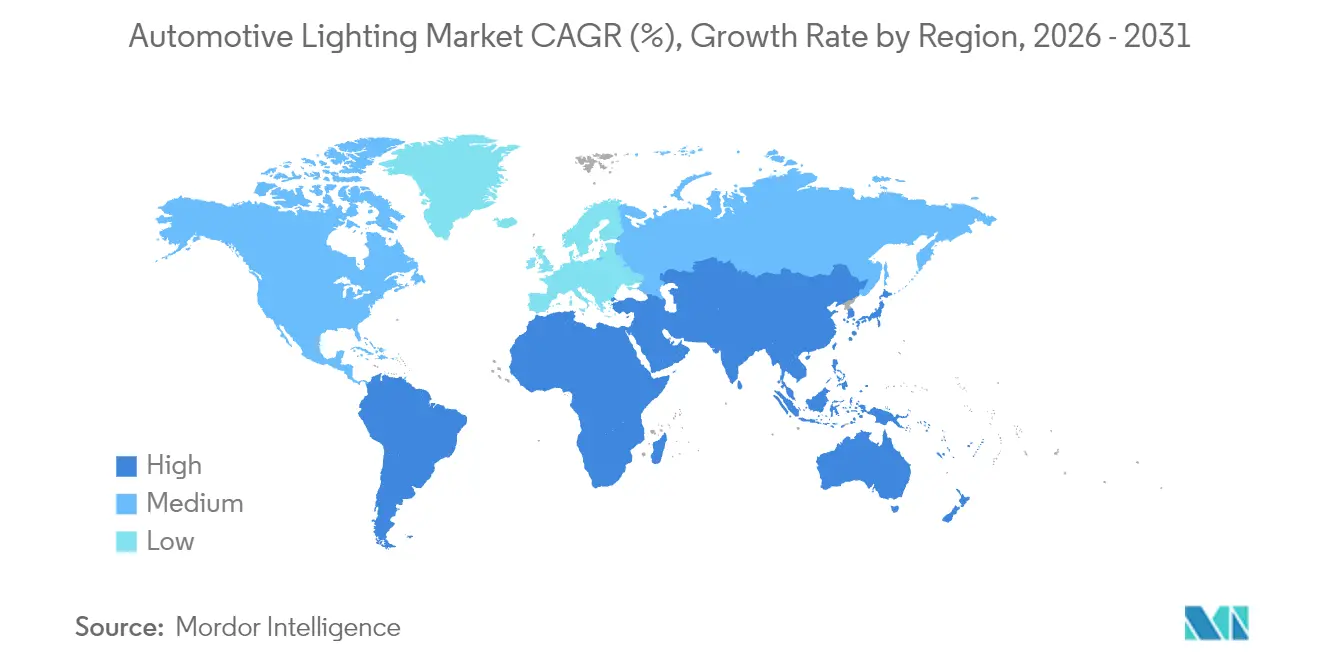

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Lighting Market Analysis by Mordor Intelligence

Automotive lighting market size in 2026 is estimated at USD 25.7 billion, growing from 2025 value of USD 24.45 billion with 2031 projections showing USD 32.98 billion, growing at 5.12% CAGR over 2026-2031. The market's growth is primarily linked to stricter global energy-efficiency policies, rapid LED penetration, and rising demand for smarter, personalization-ready lighting modules. Automakers continue to shift away from power-hungry halogen solutions toward highly integrated LED, OLED, and laser platforms that deliver lower electrical loads and richer functionality. Intensifying electric-vehicle production magnifies the importance of every watt saved, while adaptive driving beam approvals in key regions accelerate premium feature uptake. On the supply side, strategic partnerships between lighting specialists and semiconductor suppliers are shortening development cycles and unlocking digital-light projection opportunities that support advanced driver-assistance systems (ADAS) communication. Asia-Pacific remains the manufacturing hub, yet the Middle East and Africa promise the fastest volume gains as policymakers harmonize safety rules and build charging infrastructure.

Key Report Takeaways

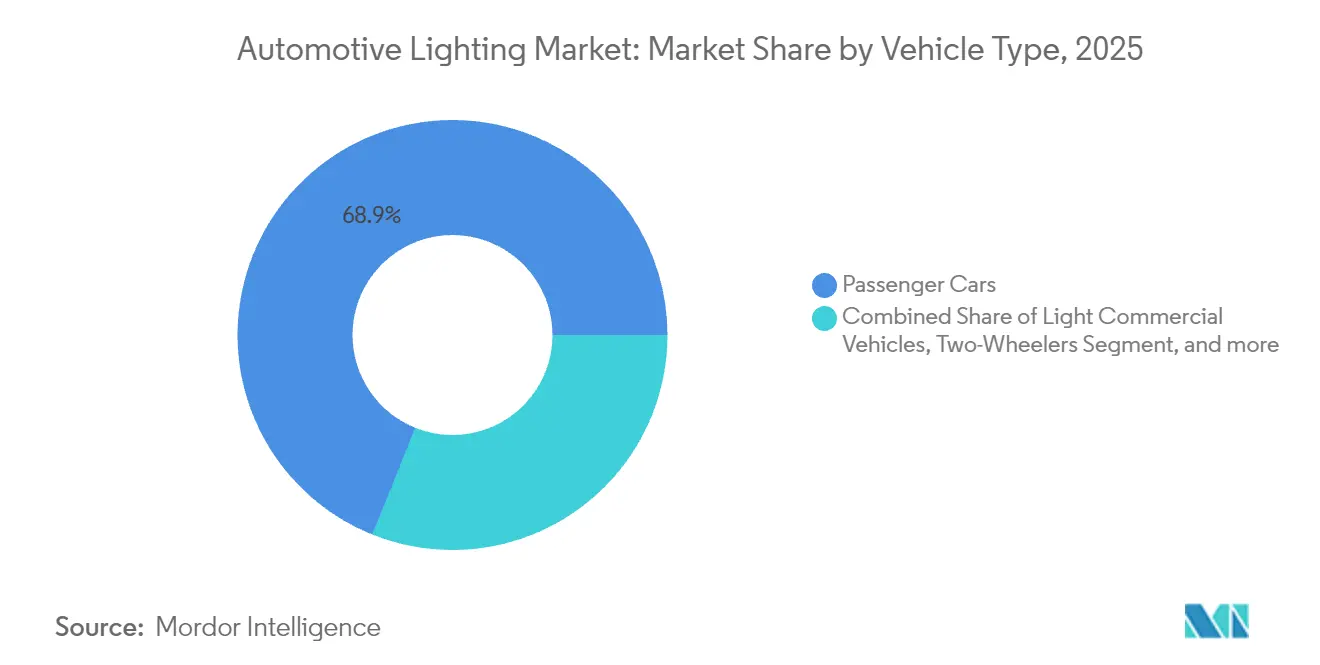

- By vehicle type, Passenger Cars led with a 68.92% automotive lighting market share in 2025; Two-Wheelers are projected to expand at a 7.15% CAGR to 2031.

- By application, Exterior lighting dominated with 78.02% revenue share in 2025; Interior/Ambient lighting is forecast to grow at a 7.88% CAGR through 2031.

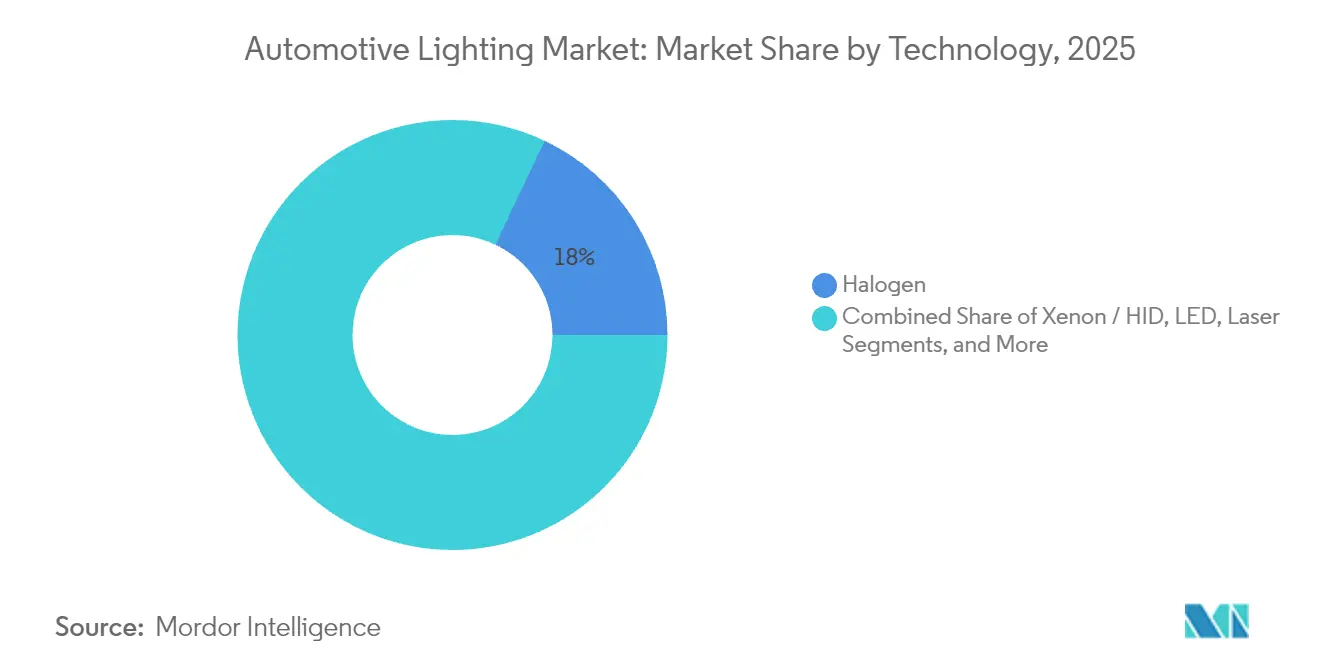

- By technology, Halogen retained 17.95% of the automotive lighting market size in 2025, while OLED solutions are advancing at a 11.74% CAGR between 2026-2031.

- By sales channel, the OEM segment in the automotive lighting market held 87.10% of 2025 revenues, whereas the Aftermarket segment records the highest projected CAGR at 8.55% to 2031.

- By region, Asia-Pacific commanded 32.22% of global revenues in 2025 in the automotive lighting market, and Middle East & Africa is pacing ahead at a 6.88% CAGR through 203

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | Qualitative Impact | (~)% Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|---|

| LED-Penetration Mandates | Strong | +1.8% | Global, with early adoption in EU & North America | Medium term (2-4 years) |

| Smart-Cockpit and Ambient-Experience Demand | Moderate | +1.2% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| EV Energy-Efficiency Requirements | Moderate | +1.0% | Global, led by China & EU markets | Medium term (2-4 years) |

| Digital-light Projection for ADAS/V2X | Moderate | +0.8% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| OTA-Enabled Lighting Personalization | Weak | +0.6% | Premium segments in developed markets | Long term (≥ 4 years) |

| Safety-Visibility Regulations | Weak | +0.4% | Global regulatory harmonization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | ||||

LED-penetration mandates

Policymakers are phasing out energy-intensive lamps to meet CO₂-reduction targets, pushing LEDs into every vehicle segment. European fleet calculations show potential savings of 1.48 TWh per year when full LED deployment is achieved. The United States amended FMVSS 108 in 2024, legalising adaptive driving beams and further incentivising LED headlamp adoption. UN Regulation 148 unifies approval codes, easing global homologation for next-generation devices[1]“UN Regulation No. 148,” United Nations Economic Commission for Europe, unece.org.

Smart-cockpit and ambient-experience demand

Interior modules in the automotive lighting market now blend thousands of RGB LEDs to create wellness-centric cabins that synchronise with infotainment cues. Mercedes-Benz DIGITAL LIGHT packs over 2 million pixels and projects road symbols to augment driver awareness. Laboratory studies confirm that advanced calibration improves colour accuracy and uniformity in direct-lit guides, removing hotspot artefacts in premium dashboards.

EV energy-efficiency requirements

Testing shows LED headlamps can stretch battery-electric range by up to 6 miles versus halogen units, owing to a power drop from 240 W to just 56 W. When extrapolated across Europe’s vehicle parc, LED indicators alone cut grid demand by 75%.

Digital-light projection for ADAS/V2X

Texas Instruments DLP chips in the automotive lighting market deliver more than 1.3 million dynamically controlled pixels, allowing vehicles to paint navigation arrows and hazard symbols directly on asphalt. User-distraction studies show projections capture attention for less than 1 second, below the 1.6-second safety threshold.

Restraints Impact Analysis*

| Restraint | Qualitative Impact | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|---|

| High Upfront Cost of Advanced Modules | Strong | -1.5% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Semiconductor and Raw-Material Volatility | Moderate | -1.2% | Global supply chains, concentrated in APAC | Medium term (2-4 years) |

| Stricter Glare/Photobiological Safety Caps | Weak | -0.8% | EU & North America regulatory frameworks | Medium term (2-4 years) |

| End-of-Life Recycling Liabilities | Weak | -0.5% | EU leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | ||||

High upfront cost of advanced modules

Digital OLED tail-lamps in luxury models such as the Audi Q5 use 18 individually addressable segments that raise BOM and tooling costs. Tandem-stack OLED prototypes achieve 77% external quantum efficiency at 46,000-hour lifetimes, yet manufacturing complexity limits mass-market migration. Micro-LED replacements can shave 30 W and 1 kg from a headlamp assembly, but capital equipment costs remain significant.

Semiconductor and raw-material volatility

SiC device yields, wafer pricing, and geopolitical trade risks are constraining LED-driver and power-module availability. Wolfspeed reported a 7% revenue dip in early 2025 due to supply imbalances, despite surging EV demand. ZF’s cancelled SiC fab joint venture underlines the challenge of scaling new capacity amid uncertain demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Drive Electrification Momentum

The passenger cars segment domin ated the Automotive Lighting Market with a 68.92% Share in 2025 revenues. Meanwhile, Two-wheelers are expected to register the fastest 7.15% CAGR. The automotive lighting market size within Two-wheelers will climb as e-scooters prioritize low-draw LEDs to preserve battery autonomy. Fiem Industries disclosed more than 80 active LED projects for bikes scheduled to hit assembly lines within three years. Light commercial fleets lean on adaptive headlamps to increase last-mile safety in dense urban corridors. Medium and heavy trucks upgrade more slowly, but mandatory conspicuity tape and running-light laws still feed a steady retrofit pipeline.

Adaptive LED headlamps using multi-sensor fusion debuted on several 2025 domestic Chinese sedans and cascaded to motorcycle variants to counter bend-lighting blind spots. Passenger-car premium trims already bake in digital-light projection and signature DRL patterns to reinforce brand identity, whereas fleet operators concentrate on durability and cost per lumen. Over the forecast horizon, small-format LEDs and heatsink-free optics will let low-cost scooters adopt ADB features previously limited to luxury cars.

By Application: Interior Lighting Accelerates Smart Integration

Exterior modules segment dominated the Automotive Lighting Market with a 78.02% share in global revenues in 2025, but Interior solutions are set to outpace with an 7.88% CAGR. Roof and foot-well zones now host addressable RGB arrays that coordinate with climate controls and infotainment events. Studies confirm that harmonized color temperature can cut driver fatigue during night-time commutes.

Headlamps remain technology testbeds: FMVSS updates permit adaptive driving beams, letting LEDs dynamically mask glare for oncoming traffic. OLED tail lights in premium SUVs deliver uniform luminance across complex shapes, which is impossible with discrete LEDs. Interior light bars that mirror ADAS warnings are now bundled with Level-3 autonomy packages, linking ambient cues to external lamp behavior.

By Technology: OLED Emerges as Premium Differentiator

The halogen lamps segment dominated the Automotive Lighting Market and covered 17.95% of the 2025 demand, but OLED modules are expected to grow at a 11.74% CAGR. The automotive lighting market size attributed to OLED is expanding thanks to flexible substrates that simplify seamless rear-signature designs. Research prototypes have extended the red-emitter lifetime to 46,000 hours at 85 °C, meeting OEM qualification bars. LEDs, however, keep scaling into value trims as package costs drop and thermal efficiency improves.

Xenon/HID units retreat to niche performance enthusiasts, while laser headlamps serve halo cars that justify the cost for extreme beam reach. Audi’s digital OLED matrix lets owners choose animated patterns during vehicle lock-unlock cycles. Over the outlook period, modular driver ICs will simplify mixed-technology setups, allowing brands to pair low-beam LEDs with OLED DRLs in the same assembly.

By Sales Channel: Aftermarket Gains Retrofit Momentum

OEM segment dominated the Automotive Lighting Market and secured 87.10% in 2025, but the Aftermarket is expected to register an 8.55% CAGR as enthusiasts retrofit aging vehicles. Federal guidance specifies that headlamp conversions must be DOT-certified as complete units, curtailing bulb-only swaps. Accordingly, aftermarket suppliers pivot toward compliant fog-lamp kits and sealed assemblies with proper beam-pattern tests.

Consumer appetite for factory-style DRLs, smoked tail-lamp lenses, and dynamic turn signals underpin accessory margins. Online tutorials amplify demand, yet state inspections enforce beam-height alignment and lumen caps, fostering opportunities for professional installers. Automakers counter the retrofit wave by offering dealer-installed accessory lines that maintain warranty coverage, further blurring OEM and aftermarket boundaries.

Geography Analysis

Asia-Pacific dominated the Automotive Lighting Market and holds 32.22% of 2025 revenues, cementing its role as a production center for global carmakers. Chinese tier-one suppliers now export adaptive LED modules compliant with UN Regulation 148, widening market options beyond traditional Japanese and European incumbents. Local champions in Guangdong reported that smart-lighting contracts accounted for 41.5% of 2024 revenue. Apan refines multi-sensor headlamp fusion, while India’s two-wheeler boom accelerates LED demand across commuter bikes.

The Middle East and Africa are expected to log the fastest 6.88% CAGR as Gulf states build EV charging corridors and roll out national safety codes that mirror EU glare thresholds. Saudi Arabia targets more than 5 million light-vehicle sales by 2025, and the UAE aims for 50% EV penetration by 2050, both policies fuelling the need for energy-efficient lamps. Governments also pursue photobiological safety audits, prompting OEMs to validate blue-light ratios before market entry.

Europe and North America are expected to expand at 4.65% and 5.35%, respectively, sustained by energy-conservation directives and premium-vehicle density. EU CO₂ standards reward automakers who cut electrical loads, positioning LEDs as low-hanging fruit. The United States sees heightened activity after FMVSS adaptive-beam approval, with domestic truck platforms planning digital-light updates in 2026 production cycles. South America advances at 6.55% CAGR as regional assemblers adopt consolidated platform architectures that integrate global-spec lighting modules, reducing cost per unit and easing aftermarket certification.

Mordor Intelligence provides coverage of the automotive lighting market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The top five suppliers hold a majority of global revenues, indicating a moderately concentrated field that still leaves room for regional challengers. Koito Manufacturing’s prevalence reflects deep integration with Japanese and US OEM platforms and early stakes in adaptive beam R&D. Valeo leverages pixel-matrix technology for high-resolution projections, while FORVIA HELLA converts software-defined lighting orders into billion-dollar contracts with US automakers, underscoring the importance of domestic sourcing.

Joint ventures continue to unlock local-content benefits: HELLA’s Chinese alliances provide cost-competitive modules tuned to regional homologation. Semiconductor partners such as Texas Instruments and on-board network firms extend ecosystem reach, ensuring seamless integration into domain controller architectures. Patents on current-control algorithms and pixelated light engines surge, reflecting the race to enable SAE Level-3+ autonomous driving cues. Start-ups focused on micro-LED arrays and holographic wave-guides target premium clusters, but cost hurdles limit immediate displacement of incumbent solutions.

Supply-chain resilience remains a board-level agenda. Players diversify substrate sourcing, holding safety stock of SiC driver ICs and high-brightness LED dies. Some pursue vertical integration of phosphor-converted emitters to mitigate geopolitical shocks. Meanwhile, sustainability narratives gain traction: recycled aluminium housings and biopolymer lenses offer measurable CO₂ savings that strengthen OEM ESG disclosures.

Automotive Lighting Industry Leaders

Koito Manufacturing Co. Ltd

Stanley Electric Co. Ltd

Valeo Group

Magneti Marelli SpA

HELLA KGaA Hueck & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: FORVIA HELLA secured billion-dollar lighting orders from a major US automaker, reinforcing its North American footprint and signalling confidence in software-defined lamp architectures.

- April 2024: Marelli and Hesai unveiled a lidar-integrated headlamp that merges sensing and illumination, previewing production readiness for 2026 ADAS packages.

Global Automotive Lighting Market Report Scope

The automotive lighting market has been segmented on the basis of vehicle type (passenger cars and commercial vehicles), application type (interior lighting and exterior lighting), technology (halogen, xenon, LED, and other technologies), and sales channel (OEM and aftermarket). The report also covers market size and forecast for the automotive lighting market in 17 countries across the major regions. The report offers the automotive lighting market size and forecast in terms of value (USD billion) for all the above segments.

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Two-Wheelers |

| Exterior | Headlamps |

| Taillights | |

| Daytime Running Lights (DRLs) | |

| Fog Lamps | |

| Interior | Ambient / Footwell |

| Roof / Dome |

| Halogen |

| Xenon / HID |

| LED |

| Laser |

| OLED |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| By Application | Exterior | Headlamps |

| Taillights | ||

| Daytime Running Lights (DRLs) | ||

| Fog Lamps | ||

| Interior | Ambient / Footwell | |

| Roof / Dome | ||

| By Technology | Halogen | |

| Xenon / HID | ||

| LED | ||

| Laser | ||

| OLED | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive lighting market?

The automotive lighting market is valued at USD 25.7 billion in 2026 and is expected to hit USD 32.98 billion by 2031.

Which vehicle segment is growing fastest in automotive lighting demand?

Two-Wheelers lead growth with a 7.15% CAGR through 2031, propelled by electric scooter sales and LED retrofits.

Why are LEDs critical for electric vehicles?

LEDs cut headlamp power draw from 240 W to 56 W, adding up to 6 miles of driving range in battery-electric cars

What technology is emerging as the premium differentiator in vehicle lighting?

OLED modules are scaling at a 11.74% CAGR because they enable uniform surfaces and dynamic patterns impossible with discrete LEDs.

How will digital-light projection influence future headlights?

High-resolution pixel arrays from providers like Texas Instruments allow symbols and navigation cues to be projected on the road surface, supporting ADAS communication and enhanced driver awareness.

Which region offers the highest growth potential?

Middle East and Africa registers a 6.88% CAGR to 2031, driven by rapid EV policy adoption and expanding safety regulations.

Page last updated on: