Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

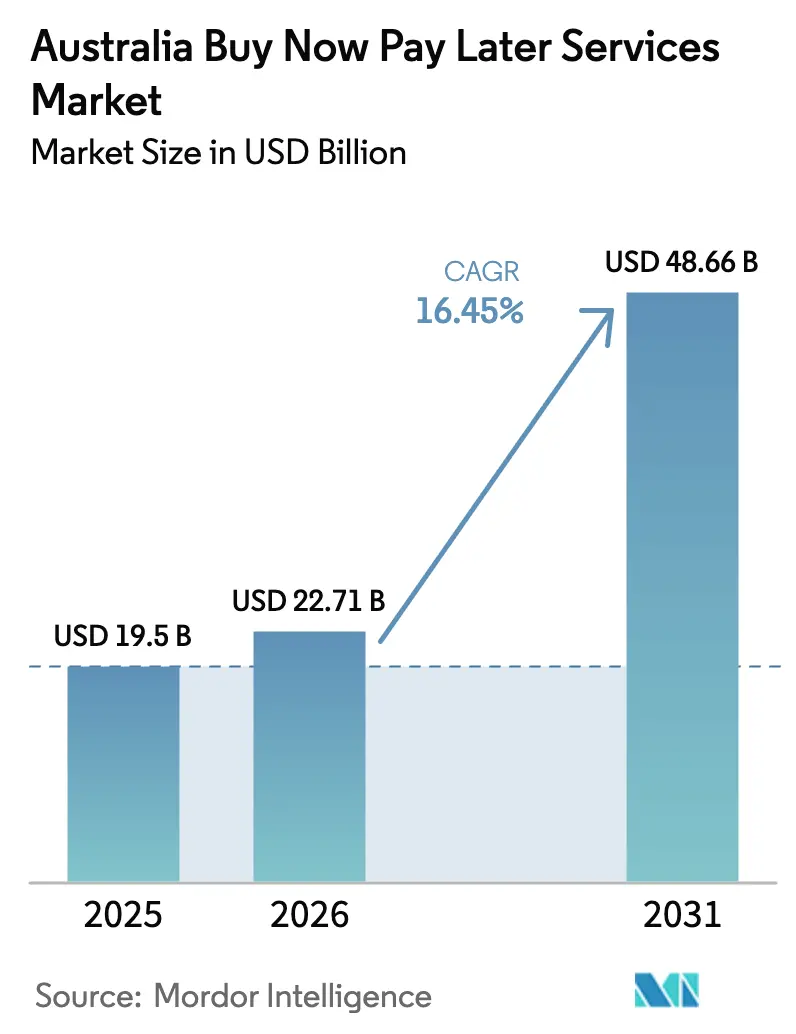

| Base Year Market Size (2025) | USD 19.50 Billion |

| Market Size (2026) | USD 22.71 Billion |

| Market Size (2031) | USD 48.66 Billion |

| Growth Rate (2026 - 2031) | 16.45% CAGR |

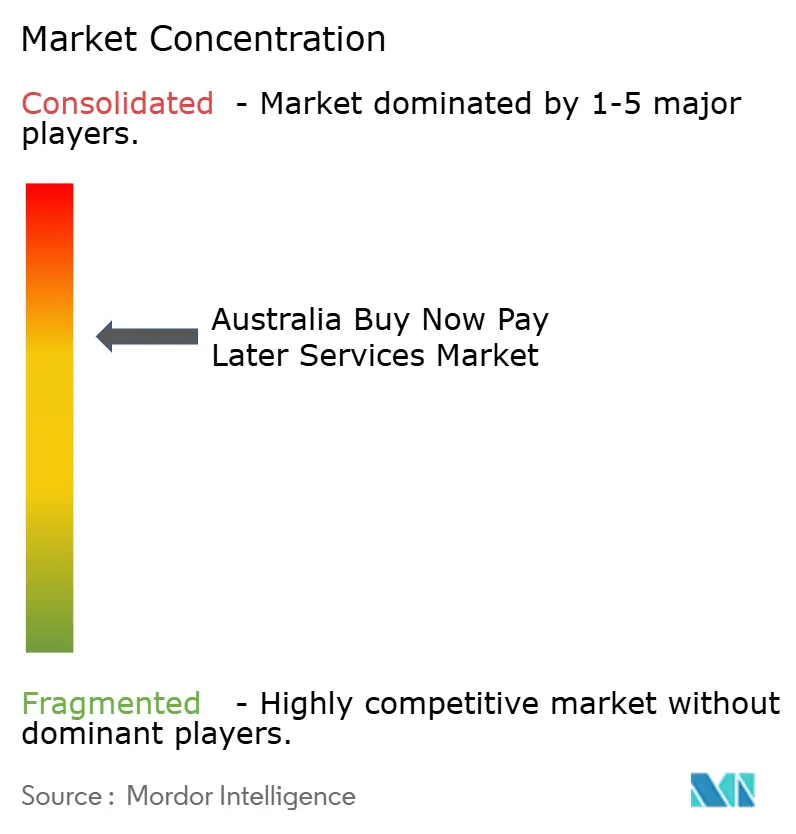

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Buy Now Pay Later Services Market Analysis by Mordor Intelligence

Australia BNPL services market size in 2026 is estimated at USD 22.71 billion, growing from 2025 value of USD 19.50 billion with 2031 projections showing USD 48.66 billion, growing at 16.45% CAGR over 2026-2031. Strong digital-commerce activity, high smartphone penetration, and real-time payment rails continue to propel the Australia BNPL market even as new credit-licensing rules alter competitive priorities. Fintech leaders are reinvesting in fraud analytics and omnichannel acceptance while banks leverage compliance infrastructure to scale. Online checkout remains the dominant use case, yet in-store rollouts tied to contactless POS terminals are expanding faster. Providers that blend responsible lending processes with friction-free user journeys have the best chance to capture incremental share across a tightening regulatory landscape.

Key Report Takeaways

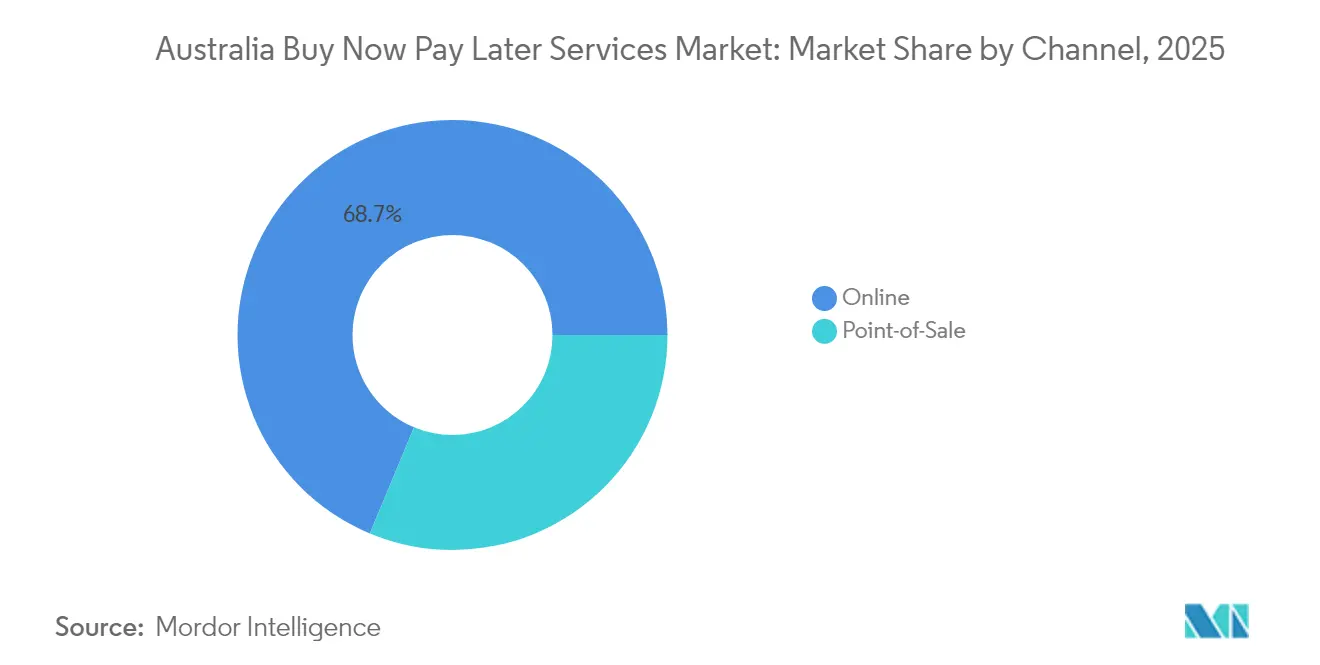

- By channel, the online segment held 68.72% of the Australia BNPL market share in 2025; in-store BNPL is forecasted to grow at an 18.15% CAGR through 2031.

- By end-use industry, fashion and apparel led with a 26.85% share of the Australia BNPL market in 2025, whereas healthcare and wellness are set to expand at a 19.42% CAGR to 2031.

- By age group, millennials controlled 44.25% of the Australia BNPL market size in 2025, while Generation Z records the highest projected CAGR at 19.78% through 2031.

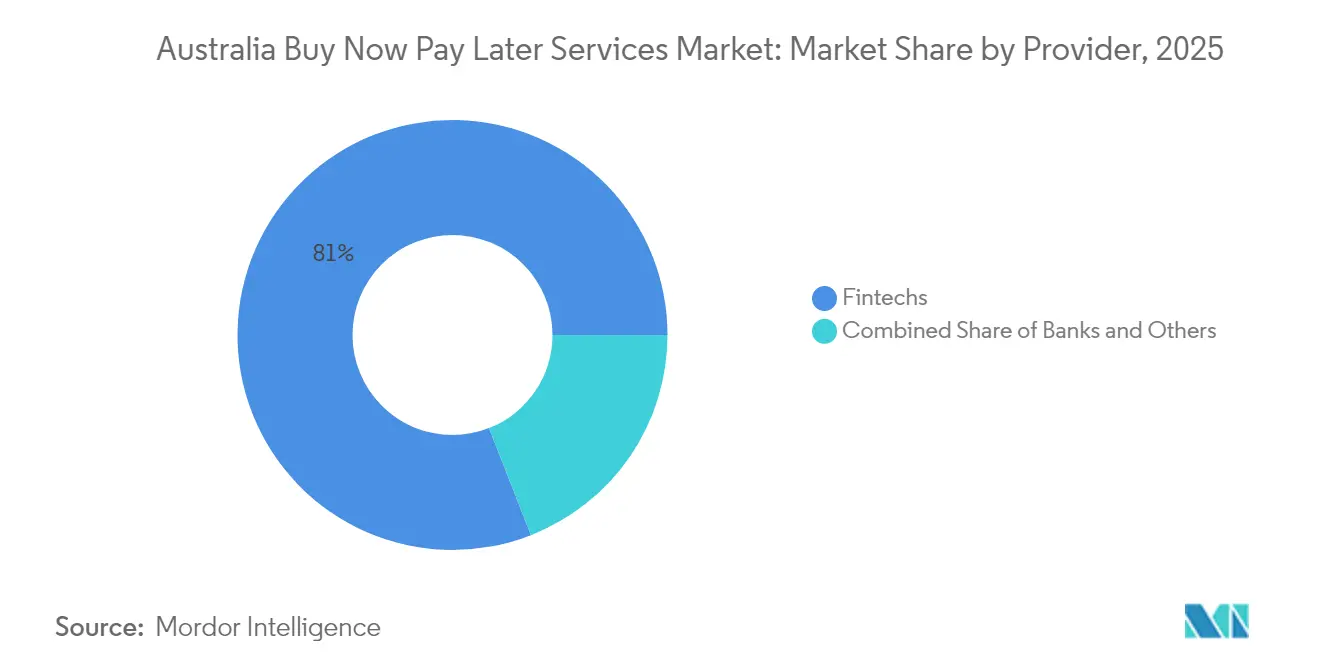

- By provider, fintech firms commanded 80.95% of the Australia BNPL market share in 2025, whereas banks are expected to post a 17.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Buy Now Pay Later Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Millennials and Gen Z shift to credit alternatives | +5.1% | National with urban concentration | Medium term (2-4 years) |

| Merchant adoption to lift e-commerce conversion | +4.2% | National, metro focus | Short term (≤ 2 years) |

| Smartphone reach and NPP real-time rails | +3.7% | National | Medium term (2-4 years) |

| BNPL integration inside digital wallets | +2.9% | National | Short term (≤ 2 years) |

| In-store BNPL via POS rollouts | +2.2% | Sydney, Melbourne, Brisbane first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Millennial and Gen Z Preference for Credit Alternatives in Australia

Millennials and Gen Z account for the largest and fastest-growing user pools in the Australia BNPL market, favoring predictable instalments over revolving cards. Generation Z alone already counts 58% penetration and is positioned to drive 48% of national retail spend by 2030, reinforcing a structural demand shift toward interest-free credit. Reduced appetite for traditional cards aligns with household budgeting needs, and purchase values increase once BNPL is presented at checkout. The demographic effect multiplies as younger cohorts consolidate everyday spending inside super-apps that bundle payments, rewards, and savings.

Merchant Adoption Driven by Higher Conversion Rates in Australian E-Commerce

Australian merchants report lower cart abandonment and larger ticket sizes when BNPL is offered. An internal PayPal study found that 75% of merchants saw order-value lifts after adding instalment options. BNPL now powers close to 15% of national online transactions, becoming a required line-item on most major retail sites. Merchants increasingly leverage BNPL data to refine marketing and loyalty offers, creating a feedback loop that reinforces adoption. Competitive differentiation shifts from price toward payment flexibility, and omnichannel retailers notice similar benefits after in-store launches.

High Smartphone Penetration & Real-Time Payments Infrastructure (NPP) Enabling Seamless BNPL Checkouts

Mobile commerce captures nearly all digital shoppers in Australia, supported by 95% smartphone usage[1]Parliament of Australia, “Digital payments adoption,” aph.gov.au. The New Payments Platform settles funds instantly, allowing BNPL providers to verify accounts and disburse merchant payments in real time. Seamless authorization drives customer trust, which is critical given that 68% of consumers exit if checkout appears insecure. Embedded finance opportunities blossom as retailers integrate BNPL natively instead of redirecting to external portals. Enhanced performance analytics further lower fraud risk and operational cost for each instalment plan.

Integration of BNPL with Digital Wallets (Apple Pay, Google Pay)

Digital-wallet penetration keeps rising, and wallet operators now embed BNPL on the same device credential. Splitit’s ¬white-label rollout through Apple Pay and Google Pay allows contactless instalment approvals at any NFC terminal, accelerating usage inside grocery and convenience channels. Wallet aggregation eliminates the need for separate apps, resonating strongly with Gen Z users who toggle between social, banking, and shopping screens in one session. Seamless token-based provisioning lowers fraud exposure and increases merchant acceptance rates.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ASIC / AFIA rules on late fees and credit checks | -3.6% | National | Short term (≤ 2 years) |

| Consumer debt delinquencies in living-cost crunch | -2.8% | Lower-income districts | Medium term (2-4 years) |

| Interest-free credit cards from major banks | -1.9% | National | Medium term (2-4 years) |

| Merchant surcharge backlash | -1.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Impending ASIC/AFIA Regulatory Tightening on Late Fees & Credit Checks

The Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Act 2024 reclassifies BNPL as low-cost credit contracts. From June 10, 2025, providers must secure Australian credit licences and follow responsible lending obligations. ASIC has issued Regulatory Guide 281 and urged unlicensed operators to apply, signaling strict enforcement[2]Australian Securities and Investments Commission, “Regulatory Guide 281 Low-cost credit contracts,” asic.gov.au. Consumer groups warn that late-fee caps may create a “poverty premium,” while compliance expenses push smaller firms to merge or exit. Large incumbents with mature risk frameworks can adapt, but growth momentum slows as underwriting rules tighten.

Rising Consumer Debt Delinquencies Amid Cost-of-Living Crisis

Inflationary pressure is raising default rates. Zip Co’s bad debts quadrupled in 2022, and Afterpay experienced a 50% jump in expected credit losses. Surveys show some households trim essentials to stay current on instalments, highlighting vulnerability in lower-income bands. Generation Z often operates several BNPL accounts at once, which compounds repayment risk. Providers are responding with AI-driven affordability checks, yet conservative lending could dampen transaction volumes, tempering the Australia BNPL market during economic stress.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Online Dominance Holds as In-Store Momentum Builds

The online segment accounted for 68.72% of the Australia BNPL market share in 2025, reflecting the digital-native origin of the model. Simple widget integrations, one-click authentication, and direct settlement into merchant dashboards preserve online supremacy. The Australia BNPL market size for online sales will still expand, yet growth gradually tapers as penetration nears saturation. Providers focus on loyalty bundles and cross-border checkout to hold engagement.

Point-of-sale adoption becomes the fastest lever for incremental volume, advancing at an 18.15% CAGR between 2026 and 2031. Tap-to-pay acceptance, QR prompts, and dynamic instalment offers at POS counters give shoppers the same flexibility they enjoy online. Contactless infrastructure and token-based credentials cut implementation hurdles, enabling even micro-merchants to switch on BNPL in minutes. As omnichannel journeys blend, consistent repayment dashboards keep customer trust intact and minimize cannibalization risk.

By End-Use Industry: Fashion Presence Endures while Healthcare Accelerates

Fashion and apparel retained 26.85% of the Australia BNPL market size in 2025 through an intuitive fit between seasonal cycles and instalment budgets. High-velocity stock-keeping units and influencer-driven launches sustain repeat usage, anchoring fashion as the performance barometer for the sector. Merchants push BNPL-exclusive discount codes, nudging adoption beyond purely price-driven shoppers.

Healthcare and wellness emerge as the fastest-growing vertical at a 19.42% CAGR through 2031, signaling a pivot from discretionary to essential spend. Dental, optical, and elective medical providers now feature BNPL at reception desks, often for ticket sizes that exceed immediate savings. Extended tenures of up to 24 months meet patient budgets without stretching provider receivables. The diversification builds counter-cyclical resilience into the Australia BNPL market, guarding revenue when retail categories slow.

By Age Group: Digital Natives Shape Long-Run Usage Curve

Millennials captured 44.25% of the Australia BNPL market in 2025, combining strong purchasing power and familiarity with fintech apps. Many already hold multiple accounts and now crave credit-score-building variants. Lifecycle triggers such as home furnishing or family health costs keep this cohort active, and loyalty integrations deepen wallet share.

Generation Z shows a 19.78% CAGR through 2031, making it the core acceleration band for the Australia BNPL market. High mobile screen time and aversion to revolving debt make instalments appealing. Social-checkout pathways that embed BNPL inside creator commerce resonate with this demographic. Older cohorts, including Generation X and Baby Boomers, adopt BNPL once healthcare and travel instalments gain visibility, further broadening the user pool.

By Provider: Fintech Scale Meets Bank Resurgence

Fintech pioneers held 80.95% of the Australia BNPL market share in 2025 after years of brand-led acquisition. Afterpay alone counts about 3.5 million local users and benefits from Block’s balance-sheet strength. Product roadmaps now prioritize licence readiness, AI fraud controls, and extended credit tenures to maintain leadership.

Banks deliver the fastest growth at 17.55% CAGR from 2026 to 2031 by bundling BNPL with everyday current accounts. Commonwealth Bank’s StepPay highlights how existing regulatory approvals, customer data, and branch networks ease onboarding challenges. Hybrid models emerge, where banks underwrite but fintechs front-end the experience. Over time, merchant-provided instalment plans may also surface as large retailers eye fee savings and data ownership, adding layers of competition across the Australia BNPL market.

Geography Analysis

Metropolitan corridors on Australia’s eastern seaboard-Sydney, Melbourne, and Brisbane-generate around 64.35% of national BNPL spend, driven by dense merchant networks and high digital wallet usage. Urban residents receive marketing earlier, accelerating adoption cycles. Strong fibre and 5G coverage in these centres lowers checkout latency and improves conversion.

Western Australia and South Australia follow with rising penetration as local merchants integrate BNPL into omnichannel platforms. Regional shoppers initially met BNPL online; now, in-store activations mirror this behavior, narrowing the urban-regional gap. Provider outreach focuses on trade associations and chamber-of-commerce events to educate small merchants on compliance and fee handling.

Rural penetration trails yet carries long-run upside for the Australia BNPL market. Infrastructure limitations, lower income levels, and fewer large-format retailers slow take-up, but aggregated digital marketplaces start to bridge the divide. As contactless cards grow ubiquitous even in remote stores, BNPL providers can add instalment screens with minimal hardware requirements. Targeted financial-literacy campaigns and transparent cost disclosures build trust among rural consumers and regulators alike.

Competitive Landscape

The Australia BNPL market exhibits high concentration. Afterpay and Zip Co form the dual leaders, reinforced by cross-border acquisitions and strategic tech integrations. Afterpay’s merger with Block injects back-end synergies, while Zip’s latitude acquisition broadens its merchant base and user profiles. Both firms headline merchant marketing that promotes BNPL as a mainstream tender type.

Traditional banks intensify competitive pressure. Commonwealth Bank leverages StepPay inside its digital banking app, instantly reachable by millions of existing customers. National Australia Bank and Westpac pilot similar instalment features, using credit-bureau insights to keep default levels within conventional lending thresholds. Bank entries raise average compliance standards and implicitly validate the product class with regulators.

The fast-growing middle layer includes global entrants such as Klarna, Sezzle, and Laybuy, each targeting specific niches—grocery, lifestyle, or cross-border retail. White-label platforms like Splitit power merchant-branded instalments that keep customer data in-house. AI-driven risk engines, loyalty tie-ins, and healthcare vertical suites serve as the new battlegrounds for differentiation, sustaining innovation velocity even as licensing rules tighten.

Australia Buy Now Pay Later Services Industry Leaders

Afterpay Limited

Zip Co Limited

PayPal Australia Pty Ltd

Humm Group Limited

CommBank StepPay (Commonwealth Bank of Australia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ASIC published Regulatory Guide 281 detailing low-cost credit contract obligations and urging unlicensed BNPL providers to apply for credit licences before the June 10, 2025, cut-off.

- April 2025: Splitit expanded its white-label BNPL service to integrate with leading healthcare practice-management systems across Australia.

- March 2025: Klarna secured exclusive BNPL arrangements with DoorDash and Walmart, replacing Affirm in the Walmart portfolio.

- February 2025: Block announced that Afterpay’s integration with Cash App processed over USD 1.2 billion in BNPL transactions in Q4 2024.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats Australia's buy now pay later (BNPL) services market as the value of consumer-facing, short-tenor installment plans that are offered at checkout and settled in fixed, largely interest-free tranches. Transactions routed through proprietary fintech apps, bank-linked installments, and in-store point-of-sale offers are all captured because, together, they mirror actual spending behavior.

Business-to-business pay-later arrangements and traditional credit-card balance conversion plans remain outside the frame.

Segmentation Overview

- By Channel

- Online

- Point-of-Sale (In-store)

- By End-Use Industry

- Consumer Electronics

- Fashion & Apparel

- Healthcare & Wellness

- Home Improvement

- Travel & Leisure

- Media & Entertainment

- Other End-Use Industries

- By Age Group

- Generation Z (18-28 Years)

- Millennials (29-44 Years)

- Generation X (45-60 Years)

- Baby Boomers (61-79 Years)

- Silent Generation (80 Years and Above)

- By Provider

- Fintechs

- Banks

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with BNPL product managers at fintechs and banks, large omnichannel retailers, and payments consultants across Sydney, Melbourne, and Brisbane. These conversations validated average ticket sizes, charge-off experience, and the likely impact of June 2025 credit-license rules, enabling us to fine-tune adoption curves by age group.

Desk Research

We grounded the model in publicly available macro and sector data. Sources such as the Reserve Bank of Australia's retail-payments statistics, Australian Bureau of Statistics monthly online sales, and ASIC consultation papers on credit licensing revealed volume, penetration, and regulatory triggers. Trade association releases from the Australian Finance Industry Association, coupled with consumer behavior surveys issued by the Treasury, helped us recognize shifting user profiles. Company filings and presentations, Dow Jones Factiva news feeds, and D&B Hoovers financial extracts enriched provider level benchmarks. The list above is illustrative; many other publications were reviewed to cross-check facts and fill gaps.

Market-Sizing & Forecasting

A top-down build starts from total Australian retail and travel e-commerce outlays, then applies BNPL penetration rates observed in card-scheme data and verified by merchant interviews. Results are stress-tested through bottom-up checks that multiply sampled active customer counts by annual spend per user. Key model inputs include smartphone penetration, online basket values, merchant service-fee trajectories, delinquency ratios, the share of in-store tap-to-pay BNPL, and forecast personal-consumption growth. Multivariate regression, supported by scenario analysis for regulatory tightening, projects values through 2030. Gaps in provider roll-ups are bridged using average selling price assumptions discussed with experts.

Data Validation & Update Cycle

Outputs pass two internal analyst reviews; variance thresholds trigger re-work, and quarterly monitoring of RBA and merchant disclosures alerts us to material shifts. Reports refresh each year and are revalidated immediately before client delivery to ensure the latest baseline.

Why Mordor's Australia Buy Now Pay Later Services Baseline Commands Reliability

Published estimates vary because firms adopt different scopes, pricing metrics, and refresh cadences.

Some quote gross merchandise value while others cite fee revenue, leading to large headline gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.50 B (2025) | Mordor Intelligence | - |

| USD 13.05 B (2024) | Regional Consultancy A | Excludes in-store POS and ignores credit-licensed bank products |

| USD 0.72 B (2024) | Global Consultancy B | Measures provider revenue, not consumer spend, and limits scope to online checkouts |

The comparison shows that Mordor's age-cohort coverage, channel inclusion, and annual model refresh create a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current value of the Australia BNPL market?

The Australia BNPL market size stands at USD 22.71 billion in 2026 and is forecast to reach USD 48.66 billion by 2031.

How fast is the sector growing?

The market is expanding at a 16.45% CAGR for the 2026-2031 period, driven by widespread smartphone usage, real-time payments rails, and merchant adoption.

Which segment holds the largest share?

Online checkouts held 68.72% of the Australia BNPL market share in 2025, reflecting the model’s digital roots.

What impact will new regulations have?

From June 2025, BNPL providers must hold Australian credit licences and apply responsible-lending checks, likely prompting consolidation among smaller operators.

Which vertical shows the fastest growth?

Healthcare and wellness leads with a 19.42% CAGR through 2031 as consumers seek installment options for medical expenses.

Are banks entering the BNPL space?

Yes, banks such as Commonwealth Bank report double-digit growth for in-house BNPL services, leveraging existing compliance frameworks to scale quickly.

Page last updated on: