Asia-Pacific Wearable Medical Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

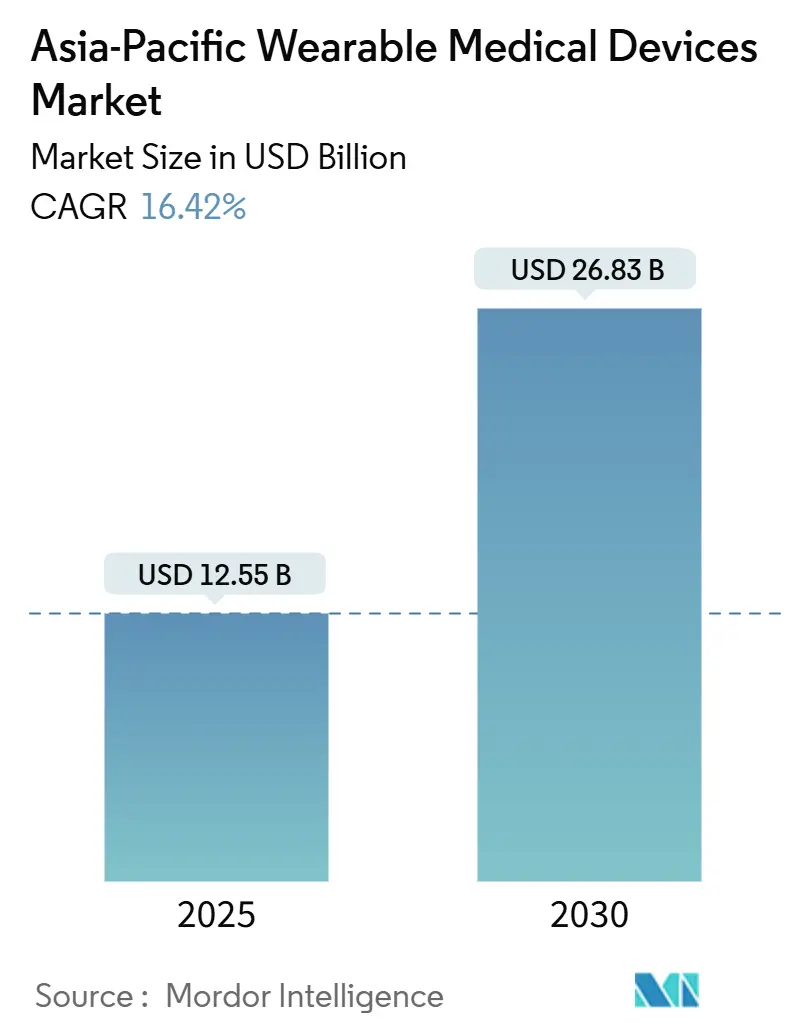

| Market Size (2025) | USD 12.55 Billion |

| Market Size (2030) | USD 26.83 Billion |

| Growth Rate (2025 - 2030) | 16.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Wearable Medical Devices Market Analysis by Mordor Intelligence

The Asia-Pacific wearable medical devices market size reached USD 12.55 billion in 2025 and is projected to climb to USD 26.83 billion by 2030, reflecting a 16.42% CAGR over the period. Faster monetization of biosensor miniaturization, insurer pilots that link reimbursement to adherence, and widespread 5G-smartphone ownership collectively sustain this pace. Ecosystem effects from more than 4.7 billion mobile-internet subscriptions, most of them in Asia-Pacific, have expanded the addressable user base for continuous telemetry and cloud analytics. Diabetes and cardiovascular disease, which already affect 257 million people across China and India alone, create a stable multiyear demand curve for continuous glucose monitors (CGMs), ECG patches, and AI-ready blood-pressure wearables. Competitive intensity remains moderate; medical-device incumbents seek regulatory approvals and reimbursement ties, while consumer-electronics leaders ride ecosystem lock-ins to convert wellness users into clinical subscribers. At the same time, government digital-health blueprints, led by India’s ABDM and Japan’s DX Vision, promote interoperability standards that lower integration costs for vendors and providers.

Key Report Takeaways

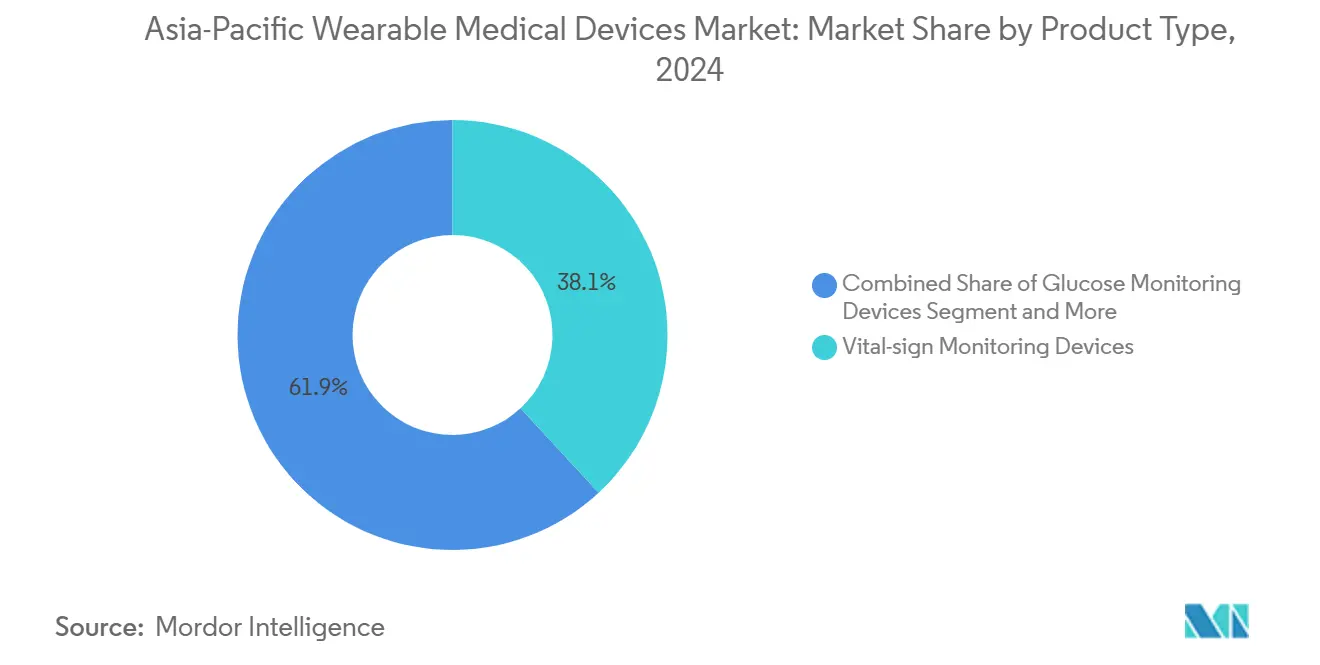

- By product type, vital-sign monitoring devices led with 38.12% Asia-Pacific wearable medical devices market share in 2024, whereas glucose and insulin monitoring platforms are advancing at a 17.6% CAGR through 2030.

- By application, sports and fitness held 48.1% of the Asia-Pacific wearable medical devices market size in 2024, while remote patient monitoring is expanding at a 19.8% CAGR to 2030.

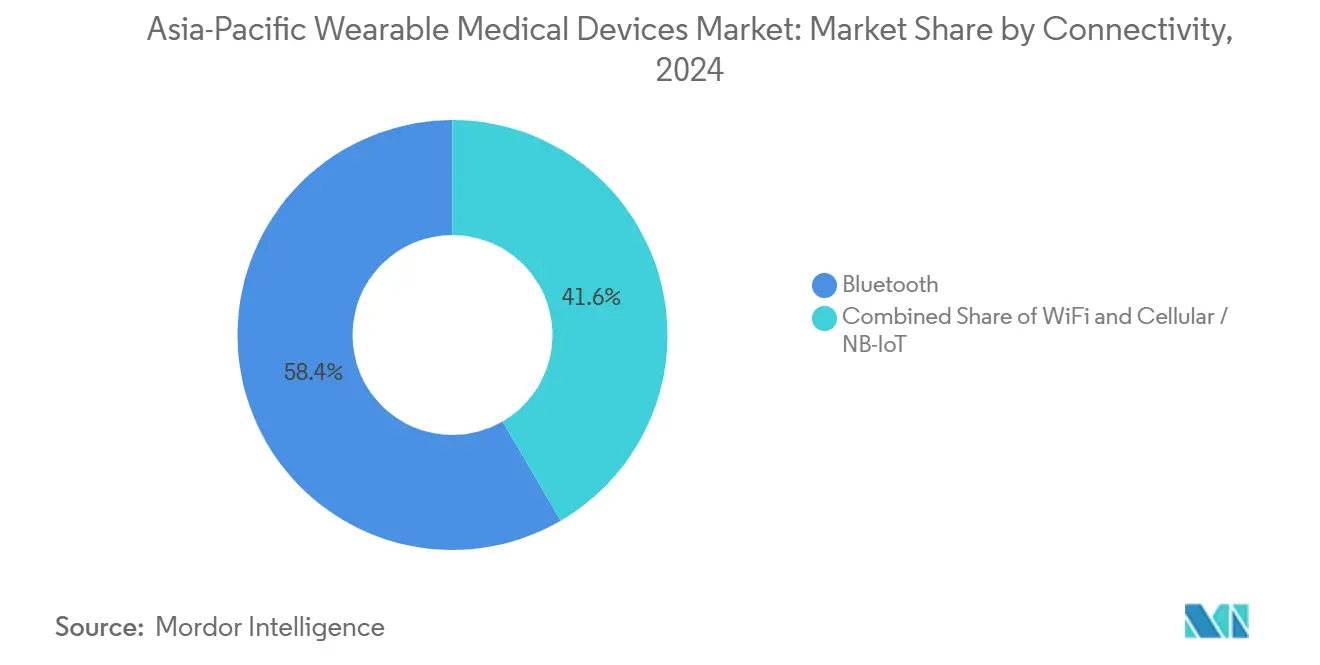

- By connectivity, Bluetooth accounted for 58.4% of 2024 shipments, yet cellular and NB-IoT links are growing at an 18.7% CAGR through 2030.

- By distribution channel, pharmacies and drug stores captured 46.5% of 2024 revenue, but online marketplaces are posting a 17.7% CAGR over the forecast window.

- China, at 36.5% of 2024 revenue, remains the largest geography; India is the fastest, registering an 18.2% CAGR through 2030.

Asia-Pacific Wearable Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread smartphone penetration & health-app ecosystem | +2.8% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Rising prevalence of diabetes & cardiovascular diseases | +3.2% | China, India, ASEAN | Long term (≥ 4 years) |

| Expanded insurer reimbursement for RPM pilots | +2.1% | China, Australia | Medium term (2-4 years) |

| AI-ready biosensor platforms enabling predictive analytics | +2.5% | Japan, South Korea, Australia | Medium term (2-4 years) |

| Government digital-health blueprints | +2.9% | India, Japan | Long term (≥ 4 years) |

| Micro-form-factor smart rings & patches targeting female health | +1.7% | Australia, Singapore, urban China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Widespread Smartphone Penetration & Health-App Ecosystem

Asia-Pacific owns the largest installed base of mobile-internet users, a reality that has turned wearables into endpoints within broader digital-care meshes. Smartphone-paired CGMs such as Abbott’s FreeStyle Libre 3 now push minute-level glucose readings to cloud dashboards that deliver predictive alerts. India’s Ayushman Bharat Digital Mission uses mobile consent flows and QR-code log-ins to link 490 million health records with wearable telemetry, demonstrating at-scale interoperability. Japanese cardiology guidelines released in 2024 endorsed smartphone-paired ECG monitors for arrhythmia screening, further normalizing mobile-centric diagnostics[2]Japanese Circulation Society, “Cardiac Arrhythmia Guidelines,” J-CIRC.OR.JP .

Rising Prevalence of Diabetes & Cardiovascular Diseases

China hosts 147.9 million diagnosed diabetes cases and India 89.8 million, magnitudes that legacy clinic infrastructures cannot manage[1]International Diabetes Federation, “IDF Diabetes Atlas, 10th Edition,” IDF.ORG . ASEAN counts 36.8 million cardiovascular patients, pushing demand for ECG patches and blood-pressure wearables that deliver real-time oversight without onsite visits. Abbott’s Libre portfolio had over 6 million active users by mid-2024, and Medtronic’s Simplera CGM, integrated with the MiniMed 780G pump since April 2025, anchors the shift toward closed-loop management.

Expanded Insurer Reimbursement for RPM Pilots (China, Australia)

China’s provincial payment codes and Australia’s Medicare Benefits Schedule now reimburse remote monitoring when adherence and outcomes are documented, effectively repositioning wearables as a reimbursable care modality. VitalConnect’s single-use VitalPatch streams ECG and respiratory rate to hospital-at-home dashboards that qualify for these codes, raising RPM adoption curves above market averages.

AI-Ready Biosensor Platforms Enabling Predictive Analytics

On-device neural networks in Dexcom G7 predict glucose excursions 20 minutes ahead, cutting hypoglycemia risk during sleep. Apple Watch Series 9 and Samsung Galaxy Watch added sleep-apnea detection validated against polysomnography, earning regulatory clearance from Australia’s TGA and Singapore’s HSA in June 2025. These advances shift product competition toward validated clinical endpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device ASP relative to disposable income | -2.4% | India, Indonesia, Vietnam, Philippines | Short term (≤ 2 years) |

| Fragmented regulatory pathways across APAC bodies | -1.8% | China, Japan, India, South Korea, Australia | Medium term (2-4 years) |

| Data-sovereignty restrictions limiting cloud services | -1.3% | China, India, Australia | Long term (≥ 4 years) |

| Battery-life & comfort trade-offs | -1.1% | Japan, Australia, global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device ASP Relative to Average Disposable Income

Libre 3 sensors retail for USD 70 per 14-day unit in India, equaling up to 20% of monthly disposable income in tier-2 cities. Dexcom’s G7 sensors cost USD 90 per 10 days, reinforcing the affordability gap. Local challengers sell sub-USD 50 trackers but lack clinical accuracy and regulatory clearances, limiting reimbursement eligibility.

Data-Sovereignty Restrictions Limiting Cross-Border Cloud Services

China’s Personal Information Protection Law and India’s draft localization rules oblige vendors to store health data on domestic servers, fragmenting cloud architectures and inflating costs. Edge-AI alleviates some constraints, yet longitudinal analytics still require centralized aggregation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Glucose Monitors Outpace Vital-Sign Incumbents

Glucose and insulin monitoring devices, expanding at 17.6% CAGR, are outrunning the broader Asia-Pacific wearable medical devices market. Abbott’s FreeStyle Libre 3 and Dexcom Stelo now serve not only diabetics but also prediabetic and wellness segments, capturing users who previously relied on finger-stick meters. Medtronic’s May 2023 acquisition of South Korea’s EOFlow adds a patch-pump layer that advances closed-loop therapy, integrating CGM input with micro-pump dosing.

Vital-sign monitoring retains scale, yet commoditization looms. Omron offsets hardware erosion by adding AI trend analysis inside its OMRON Connect app, while Garmin’s ECG-enabled Forerunner 970 seeks differentiation within the athlete-physician crossover. Respiratory, neuro, fetal, and smart-ring micro-segments remain small today but constitute a pipeline of high-growth adjacencies that could raise the Asia-Pacific wearable medical devices market size in specialized cohorts.

By Application: Remote Patient Monitoring Surges Past Fitness

Remote patient monitoring (RPM) leads growth at 19.8% CAGR as payers in China and Australia reimburse continuous telemetry tied to outcome metrics. VitalConnect patches feeding hospital-at-home dashboards qualify under new payer codes, driving institutional procurement. Sports and fitness still dominate revenue because of high-volume smartwatches, yet their share is bending downward as insurers subsidize clinical wearables. Home healthcare usage gains from aging in Japan and South Korea, where over-65 cohorts demand noninvasive blood-pressure and SpO2 monitoring. Clinical trial deployments remain small in revenue terms but deliver strategic value: the FDA’s 2023 digital-health guidance, mirrored by PMDA and TGA positions, formalizes wearable endpoints in drug submissions.

By Connectivity: Cellular Links Enable Standalone Operation

Cellular and NB-IoT wearables, moving at an 18.7% CAGR, promise always-on telemetry for users without smartphones or for those in rural zones with weak Wi-Fi. China Mobile’s nationwide NB-IoT rollout lets CGMs and cardiac patches bypass Bluetooth dependencies. While Bluetooth Low Energy remains dominant on unit volume, the clinical tier is shifting toward eSIM-based watches and NB-IoT-enabled patches that guarantee data continuity and emergency escalation.

By Distribution Channel: Online Marketplaces Gain Share

E-commerce platforms, posting a 17.7% CAGR, erode the historical lead of pharmacies. Libre and G7 sensors on Amazon, JD.com, and Tmall offer auto-ship subscriptions that cut per-unit cost and reduce lapse. Pharmacies counter with omnichannel models and in-store demo corners. Consumer-electronics retail maintains relevance for premium smartwatches but now competes with direct brand stores and brand-owned websites. The convergence compresses retailer margins and shifts leverage toward manufacturers with strong direct consumer relationships inside the Asia-Pacific wearable medical devices market.

Geography Analysis

China anchors 36.5% of regional revenue. Domestic champions Huawei, Xiaomi, and Zepp Health pair low-priced bands with WeChat and AliPay health minis, capturing urban Gen Z consumers. Yet data-localization laws necessitate on-shore data centers for multinationals, adding compliance overhead[3]Government of China, “Personal Information Protection Law,” GOV.CN. The NMPA’s Class II/III pathways further tilt early arrival toward local incumbents.

India leads growth at 18.2% CAGR, powered by the Ayushman Bharat Digital Mission’s 739 million ABHA IDs and 490 million linked records. CGM adoption is strongest in metros, while tier-2/3 affordability gaps sustain demand for sub-USD 50 trackers from GOQii and Lifesense. Draft data-protection legislation signals future localization duties likely to mirror China’s.

Japan and South Korea deliver reliable volumes on high per-capita spending and rapid 5G rollout. Japan’s PMDA relaxed software-as-medical-device approvals in 2024, letting vendors push algorithm updates faster; South Korea benefits from Samsung’s entrenched domestic supply chain. Australia, after TGA clearance of sleep-apnea detection on Apple and Samsung watches in June 2025, now pilots reimbursements for algorithm-detected breathing disorders, expanding the Asia-Pacific wearable medical devices market.

Competitive Landscape

The Asia-Pacific wearable medical devices market hosts entrenched multinational medical-device leaders such as Abbott and Medtronic, consumer-electronics titans Apple, Samsung, Huawei, Xiaomi, and agile regional players GOQii, Lifesense, and Zepp Health. Partnerships proliferate: Abbott now supplies CGM sensors for Medtronic pumps; Samsung and Oura pursue data-sharing accords with Dexcom. Venture capital underscores interest in micro-form-factor devices, as evidenced by Oura’s USD 900 million Series E raise at an USD 11 billion valuation.

White-space opportunities lie in sub-USD 50 clinical-grade devices, multiweek battery life without recharging, and true HL7 FHIR interoperability. Edge-AI and NB-IoT provide technical moats; firms with vertically integrated silicon and cloud stacks enjoy cost advantages. Patent velocity in biosensor miniaturization, low-power radios, and photoplethysmography waveforms signals accelerating differentiation pressure. Yet no player have a greater share in 2024, keeping the field moderately concentrated and primed for lateral alliances.

Asia-Pacific Wearable Medical Devices Industry Leaders

Abbott Laboratories

Apple Inc.

Philips Healthcare

Samsung Electronics Co. Ltd.

Omron Healthcare Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Samsung Galaxy Watch sleep-apnea notification gained approval from Australia’s TGA and Singapore’s HSA, expanding availability to 70 markets.

- May 2025: Apple Watch sleep-apnea detection received clearance from Australia’s TGA and Singapore’s HSA, moving beyond U.S. and European markets.

Asia-Pacific Wearable Medical Devices Market Report Scope

As per the scope of the report, a wearable medical device is a portable, often body-worn instrument or sensor that monitors, records, and sometimes analyzes health-related data in real-time. These devices are designed to be comfortable and convenient for continuous or periodic use, helping with health management, diagnosis, or treatment of medical conditions.

The Asia-Pacific wearable medical devices market is segmented by product type, application, connectivity, distribution channel, and country. By product type, the market includes vital-sign monitoring devices, heart-rate monitors, activity trackers, ECG monitors, blood-pressure wearables, glucose/insulin monitoring devices, respiratory therapy wearables, neuro-monitoring devices, fetal and obstetric wearables, and others (such as smart patches and smart rings). By application, the market is categorized into sports and fitness, remote patient monitoring, home healthcare, and clinical trials and research. By connectivity, the market is segmented into Bluetooth, Wi-Fi, and cellular/NB-IoT. By distribution channel, the market includes pharmacies and drug stores, online marketplaces, and consumer electronics retail. By country, the market covers China, Japan, India, South Korea, Australia, and the rest of Asia-Pacific. The Market Forecasts are Provided in Terms of Value (USD).

| Vital-sign Monitoring Devices | Heart-rate Monitors |

| Activity Trackers | |

| ECG Monitors | |

| Blood-pressure Wearables | |

| Glucose / Insulin Monitoring Devices | |

| Respiratory Therapy Wearables | |

| Neuro-monitoring Devices | |

| Fetal & Obstetric Wearables | |

| Others (Smart Patches, Smart Rings, among others) |

| Sports & Fitness |

| Remote Patient Monitoring |

| Home Healthcare |

| Clinical Trials & Research |

| Bluetooth |

| Wi-Fi |

| Cellular / NB-IoT |

| Pharmacies & Drug Stores |

| Online Marketplaces |

| Consumer Electronics Retail |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Product Type | Vital-sign Monitoring Devices | Heart-rate Monitors |

| Activity Trackers | ||

| ECG Monitors | ||

| Blood-pressure Wearables | ||

| Glucose / Insulin Monitoring Devices | ||

| Respiratory Therapy Wearables | ||

| Neuro-monitoring Devices | ||

| Fetal & Obstetric Wearables | ||

| Others (Smart Patches, Smart Rings, among others) | ||

| By Application | Sports & Fitness | |

| Remote Patient Monitoring | ||

| Home Healthcare | ||

| Clinical Trials & Research | ||

| By Connectivity | Bluetooth | |

| Wi-Fi | ||

| Cellular / NB-IoT | ||

| By Distribution Channel | Pharmacies & Drug Stores | |

| Online Marketplaces | ||

| Consumer Electronics Retail | ||

| By Country | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the forecast value of Asia-Pacific wearable medical devices by 2030?

The market is projected to reach USD 26.83 billion by 2030, reflecting a 16.42% CAGR from 2025.

Which product segment is growing fastest?

Glucose and insulin monitoring devices are expanding at a 17.6% CAGR, outpacing all other categories.

Why is remote patient monitoring gaining traction?

RPM adoption is accelerating at a 19.8% CAGR because insurers in China and Australia reimburse continuous telemetry tied to adherence and outcomes.

How does cellular connectivity influence adoption?

Wearables with cellular or NB-IoT links are growing at an 18.7% CAGR, enabling standalone data transmission for elderly and rural users without smartphones.

Which country is advancing most rapidly?

India leads growth at an 18.2% CAGR through 2030, boosted by the Ayushman Bharat Digital Mission and rising chronic-disease prevalence.

What regulatory hurdles do vendors face?

Fragmented approval pathways across NMPA, PMDA, CDSCO, MFDS, and TGA require separate clinical evidence, lengthening time-to-market and increasing costs.

Page last updated on: