Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

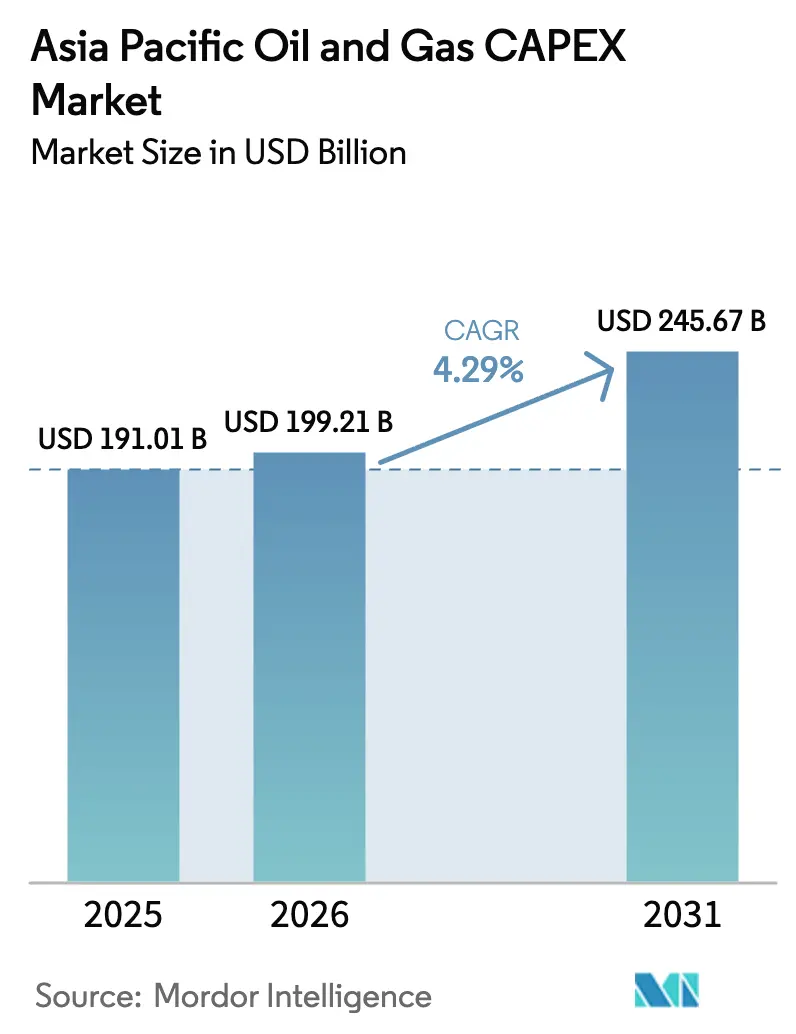

| Base Year Market Size (2025) | USD 191.01 Billion |

| Market Size (2026) | USD 199.21 Billion |

| Market Size (2031) | USD 245.67 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Oil And Gas CAPEX Market Analysis by Mordor Intelligence

The Asia Pacific Oil And Gas CAPEX Market size was valued at USD 191.01 billion in 2025 and estimated to grow from USD 199.21 billion in 2026 to reach USD 245.67 billion by 2031, at a CAGR of 4.29% during the forecast period (2026-2031).

Persistently high regional energy demand, sizable domestic resource potential, and accelerated transition infrastructure are keeping spending on an upward trajectory despite tightening green-finance rules. Governments deploy capital toward new LNG, hydrogen, and CCUS assets to secure supply, while national oil companies maintain conventional upstream programs, safeguarding energy security during the transition period. International operators are rotating their portfolios toward the region because regulatory frameworks are clearer than in several Middle East jurisdictions, and because deep-water and LNG projects now deliver globally competitive break-even levels. Technology spending also rises as digital oilfield programs extend asset life, and modular refinery projects enhance product slate flexibility across India and China.

Key Report Takeaways

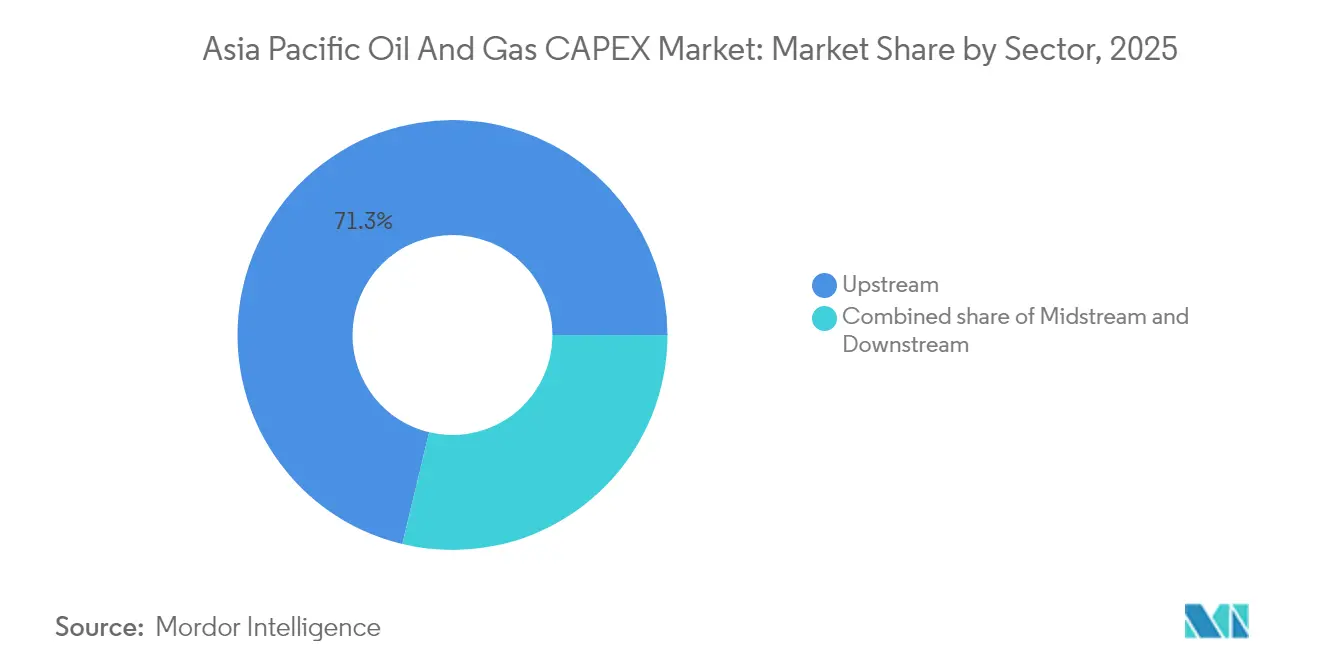

- By sector, upstream commanded 71.25% of the Asia Pacific oil and gas CAPEX market share in 2025; the downstream segment is the fastest-growing, advancing at a 4.98% CAGR to 2031.

- By location, onshore projects accounted for 65.25% of the Asia Pacific oil and gas CAPEX market size in 2025, while offshore spend is projected to expand at a 6.84% CAGR over the same horizon.

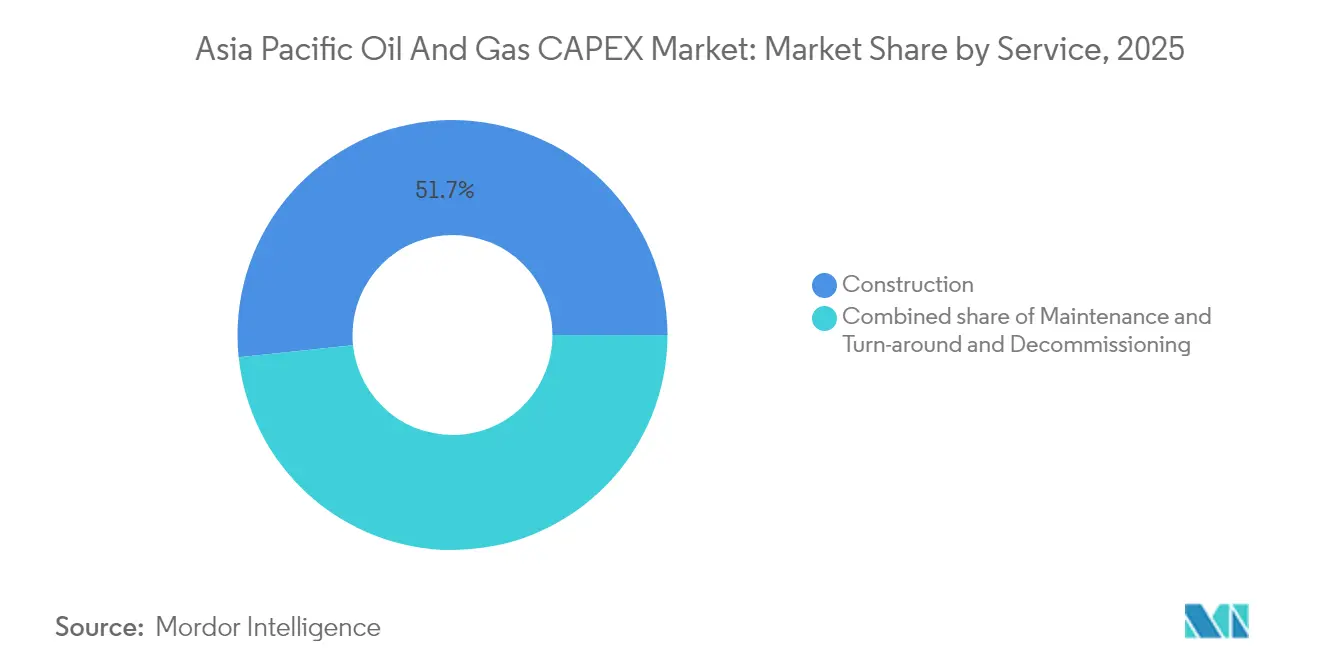

- By service, construction activities led with a 51.65% share of the Asia Pacific oil and gas CAPEX market size in 2025; decommissioning is projected to record the highest 7.58% CAGR through 2031.

- By geography, China held a commanding 56.15% share of the Asia Pacific oil and gas CAPEX market in 2025, whereas Malaysia is projected to present the fastest growth at a 5.28% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Oil And Gas CAPEX Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging LNG infrastructure investments across Southeast Asia | +1.20% | Indonesia, Malaysia, Thailand, Vietnam | Medium term (2-4 years) |

| Government-led hydrogen & CCUS CAPEX commitments in Australia and Japan | +0.80% | Australia, Japan | Long term (≥ 4 years) |

| National-oil-company push for deep-water gas projects in China & Malaysia | +1.00% | China, Malaysia | Medium term (2-4 years) |

| IOCs reallocating portfolios toward low-cost APAC plays amid Middle-East risk | +0.60% | Regional, concentrated in Australia, Malaysia | Short term (≤ 2 years) |

| Rapid growth of digital-oilfield CAPEX for asset-life extension | +0.40% | China, Australia, Indonesia | Medium term (2-4 years) |

| Modular refinery projects targeting petrochemical-import substitution in India | +0.50% | India, with spillover to Bangladesh, Sri Lanka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging LNG Infrastructure Investments Across Southeast Asia

Indonesian state major Pertamina earmarked USD 20 billion for LNG capacity additions running to 2028, while Petronas committed USD 15 billion to three floating LNG units that will lift Malaysia’s exportable gas by mid-decade. Storage, regasification, and shipping assets accompany these upstream builds, driving multi-year contracting opportunities for construction and engineering firms. The investment wave positions Southeast Asian exporters to capture 15–20% of global LNG trade by 2030, insulating them from oil-price volatility and boosting foreign-exchange inflows.(1)Asian Development Bank, “Energy Infrastructure Investment in Asia-Pacific,” adb.org Domestic markets also shift away from pipeline gas in favor of flexible LNG imports that back-stop intermittent renewables. The momentum of these schemes directly feeds the Asia Pacific oil and gas CAPEX market, ensuring a sturdy demand floor across the medium term.

Government-Led Hydrogen & CCUS CAPEX Commitments in Australia and Japan

Japan’s Green Innovation Fund has earmarked JPY 2 trillion (USD 15 billion) for hydrogen value-chain projects, mirroring Australia’s AUD 70 billion (USD 47 billion) allocation aimed at production hubs, transport corridors, and geological storage.(2)Ministry of Economy Trade and Industry Japan, “Green Innovation Fund Guidelines,” meti.go.jp The bilateral framework connects Australia’s resource endowment with Japanese offtake demand, ensuring bankable offtake against long-dated assets. Public capital absorbs early technology risk, catalyzing private participation and lowering the weighted-average cost of capital, which sustains the Asia Pacific oil and gas CAPEX market even as traditional hydrocarbons plateau. Long-term offtake agreements already under negotiation signal that project pipelines will lengthen well beyond the current forecast period.

National-Oil-Company Push for Deep-Water Gas Projects in China & Malaysia

CNOOC has set aside USD 15 billion for multiple deep-water developments through 2027, deploying next-generation subsea systems that reduce operating costs and minimize surface footprints. Petronas pursues comparable efforts in the South China Sea, adding floating production, storage, and offloading units that monetize fields previously inaccessible due to water depth and security concerns. These programs span 7–10 years, delivering dependable EPC backlogs that support the Asia Pacific oil and gas CAPEX market. Because deep-water gas displaces imported LNG, governments support approvals even amid maritime disputes, thereby locking in the positive demand impact for the medium term.

IOCs Reallocating Portfolios Toward Low-Cost APAC Plays Amid Middle-East Risk

Heightened geopolitical uncertainty in the Gulf has prompted Shell to commit USD 12 billion to Australian LNG trains and BP to partner with Indonesian NOCs on multi-field gas projects. The shift favors jurisdictions with transparent regulation, contractual sanctity, and ready export infrastructure. Short-cycle tie-backs further de-risk cash flow, meaning IOC capital turns faster, sustaining service-sector utilisation in the Asia Pacific oil and gas CAPEX market. Risk diversification remains the primary motivator, but carbon-intensity reduction also weighs in, making APAC’s relatively young asset base an attractive platform for digital optimization and methane-emission control programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightened green-finance rules restricting fossil-fuel project lending | -0.80% | Global, particularly affecting Australia, Japan | Short term (≤ 2 years) |

| Rising EPC inflation & local-content mandates inflating build costs | -0.60% | Regional, concentrated in Indonesia, India, Malaysia | Medium term (2-4 years) |

| Accelerating EV uptake dampening long-term refined-products demand | -0.40% | China, India | Long term (≥ 4 years) |

| Maritime-security risks in the South China Sea delaying offshore FIDs | -0.30% | China, Malaysia, Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightened Green-Finance Rules Restricting Fossil-Fuel Project Lending

Singapore’s Monetary Authority slashed fossil-fuel lending eligibility by 60% in 2024, and Australia’s banks followed suit, lifting borrowing costs for mid-scale upstream ventures by 200–300 basis points(3).Monetary Authority of Singapore, “Environmental Risk Management Guidelines,” mas.gov.sg Developers either pivot to export-credit agencies or raise mezzanine tranches, delaying final investment decisions and reducing near-term spending in the Asia Pacific oil and gas CAPEX market. Short-cycle projects with visible transition pathways still reach financial close, but high-carbon barrels bear clear funding penalties.

Rising EPC Inflation & Local-Content Mandates Inflating Build Costs

Indonesia imposes 40% local-content requirements on upstream projects, while Malaysia has similar thresholds, forcing international contractors to form JVs and nurture local supply chains that add 15–25% to total installed cost. Material and labor price spikes amplify the effect, squeezing internal rates of return and causing operators to stagger work scopes. Extended timelines reduce annual cash draws into the Asia Pacific oil and gas CAPEX market during the ramp-up window, though total lifetime spend eventually rebounds once procurement pipelines mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Sustains Energy Security Efforts

Upstream commanded 71.25% of the Asia Pacific oil and gas CAPEX market in 2025, reflecting state directives to shore up indigenous supply amid volatile import prices. National oil companies led the way in spending on deep-water gas, shale blocks, and coal-bed methane, leveraging digital drilling and real-time reservoir imaging to boost recovery rates. These outlays keep local content factories busy and generate a continuous flow of contracts for service specialists. Midstream outlays center on brownfield pipeline looping and LNG storage, pairing with upstream developments to assure takeaway capacity.

Downstream expenditure, although comprising a smaller 28.75% share in 2025, is projected to accelerate at a 4.98% CAGR through 2031. Petrochemical integration drives revamp programs that swap simple fuels for higher-margin olefins and aromatics. India’s Jamnagar complex and China’s Fujian hub typify the shift: once gasoline-centric, the sites now channel incremental cash toward steam crackers and PDH units. Because each retrofit requires compressors, reactors, and automation, downstream continues to pull material volumes into the Asia Pacific oil and gas CAPEX market size tally, despite plateauing fuel demand.

By Location: Offshore Growth Outpaces Onshore Maturity

Onshore activities retained 65.25% of the Asia Pacific oil and gas CAPEX market size in 2025, anchored by Chinese shale, Australian coal-seam gas, and India’s Rajasthan tight-oil plays. Land projects enjoy quicker approvals and modest water-depth complexity, allowing NOCs to sanction multiple pads within a single budget cycle. Infrastructure such as trunk pipelines and gas-gathering networks gets bundled, locking in parallel opportunities for compressors and metering-skid providers.

Offshore CAPEX grows quicker at 6.84% CAGR, fueled by Malaysia’s deep-water gas surge, Indonesia’s floating LNG fleet, and Australia’s Browse and Scarborough fields. Next-generation FPSOs integrate CCS modules, meeting emissions regulations while unlocking marginal reservoirs. Specialist subsea contractors, therefore, gain share in the Asia Pacific oil and gas CAPEX market, while equipment OEMs secure frame agreements that stretch the backlog into the 2030s.

By Service: Construction Leads While Decommissioning Scales Fast

Construction accounted for 51.65% of the 2025 spend as LNG trains, pipelines, and integrated refinery-petrochemical complexes broke ground across six major economies. EPC players coordinate massive workforces, heavy-lift assets, and advanced project controls to deliver under tight commissioning windows. Maintenance and turnaround posted steady, inflation-indexed growth, catering to maturing asset fleets in China and Australia.

Decommissioning remains a modest absolute slice but expands at an 7.58% CAGR, the fastest within services. Regulators now demand escrowed removal provisions and enforce strict post-plugging seabed clearance, compelling operators to award multi-year dismantling contracts. Skills developed in the North Sea migrate to the Asia Pacific, benefiting specialized contractors and keeping niche opportunities alive in the Asia Pacific oil and gas CAPEX market share for services.

Geography Analysis

China’s 56.15% stake in 2025 stems from upstream megaprojects such as Lingshui 17-2 and Shenhai-1, each exceeding USD 2 billion in development outlays. State agencies synchronize pipeline routes, port upgrades, and storage builds that compress execution timelines and heighten domestic multiplier effects. The strategy stabilizes regional supply chains and anchors equipment demand for the Asia Pacific oil and gas CAPEX market.

India’s push toward petrochemical self-sufficiency shapes its CAPEX profile. Modular refinery packages in Rajasthan and Gujarat require lower ticket sizes—USD 1–2 billion versus legacy megaprojects—yet the aggregate spend remains high because the model is repeated across several states. Gas grid expansion from Dahej southward underpins fertilizer and city-gas plans, extending midstream capex tails into the early 2030s.

Australia sits third in value terms but leads in technology. Brownfield LNG compression debottlenecks and CCS retrofits at Gorgon and Wheatstone keep service firms engaged, while the Pilbara hydrogen spine lines up USD 15 billion in electrolyzer, storage, and port infrastructure.Government grants lower first-mover risk, making Australia critical to future-fuel cost curves.

Malaysia’s 5.28% CAGR owes to Petronas’s three-string floating LNG roadmap plus Kasawari CCS, South East Asia’s largest carbon-capture facility under construction. Ancillary pipelines and shore-based enhancements magnify multiplier effects across Johor and Sarawak, pushing supplier-based localization above 50%.

Indonesia, Thailand, and Vietnam round out the core, each channeling niche CAPEX into domestic gas monetization and regas terminal additions. Bangladesh and the Philippines, grouped under Rest of Asia-Pacific, accelerate late in the period as improved sovereign credit ratings unlock concessional financing for import terminals and storage caverns.

Competitive Landscape

National oil companies dominate spend due to sovereign mandates and ready access to state-backed finance. CNPC, CNOOC, and Sinopec collectively exceed USD 60 billion annual capex, dwarfing international rivals and cementing China’s equipment ecosystem. Petronas and ONGC follow, each leveraging integrated operations to expedite projects that align with national energy security agendas.

International majors adopt partnership models that blend technical edge with local market familiarity. Shell co-operates on FLNG, LNG bunkering, and hydrogen pilots with Petronas; TotalEnergies teams up on combined LNG and CCS developments, while BP piggybacks Indonesian NOC infrastructure to hedge geopolitical exposure. Carbon-management know-how and digital-optimization suites emerge as the main differentiators, granting international players continued relevance in the Asia Pacific oil and gas CAPEX market.

Service-sector competition intensifies as decommissioning and CCS niches open. Saipem, Subsea 7, and Technip Energies position themselves for turnkey scopes that incorporate well-plugging, topside removal, and carbon-storage site preparation. Domestic yards in China, Indonesia, and Malaysia claw share through favorable local-content policies, although complex subsea hardware still flows from Western OEMs, maintaining a balanced supplier field.

Asia Pacific Oil And Gas CAPEX Industry Leaders

Exxon Mobil Corporation.

Shell plc

Pacific Oil & Gas Ltd

Chevron Corporation

BP plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Petronas announced a USD 8 billion investment in Malaysia's deep-water gas development program, targeting 3 new floating production platforms in the South China Sea.

- September 2025: China National Petroleum Corporation (CNPC) secured regulatory approval for a USD 12 billion shale gas development project in Sichuan Province, incorporating advanced hydraulic fracturing technologies and digital monitoring systems.

- August 2025: Shell and Japan's INPEX formed a joint venture to develop Australia's largest hydrogen production facility, with combined investments totaling USD 15 billion through 2030.

- July 2025: India's Oil and Natural Gas Corporation (ONGC) announced a USD 6 billion offshore drilling program targeting deep-water reserves in the Krishna-Godavari basin.

- June 2025: TotalEnergies and Malaysia's Petronas signed a USD 10 billion partnership agreement for integrated LNG and carbon capture development, combining conventional gas production with carbon sequestration technologies.

Asia Pacific Oil And Gas CAPEX Market Report Scope

The Scope of the Asia-Pacific Oil & Gas CAPEX Market includes:-

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

By Geography

| China |

| India |

| Australia |

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning | |

| By Geography | China |

| India | |

| Australia | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is Asia Pacific oil and gas CAPEX spending in 2026?

The Asia Pacific oil and gas CAPEX market size stands at USD 199.21 billion in 2026, tracking the 4.29% CAGR projected for the remainder of the decade.

The Asia Pacific oil and gas CAPEX market size stands at about USD 199.21 billion in 2026, tracking the 4.29% CAGR projected for the remainder of the decade.

Offshore developments show the highest growth, advancing at a 6.84% CAGR as deep-water gas and floating LNG projects proliferate.

Why is Malaysia considered a hotspot for new investment?

Petronas’s floating LNG program, deep-water gas fields, and CCS initiatives push Malaysia’s spending up at a 5.28% CAGR—the fastest rate in the region.

How do green-finance rules influence capital spending?

Tighter lending criteria lift borrowing costs by up to 300 basis points, delaying some mid-scale projects but accelerating low-carbon investments like hydrogen and CCS.

What opportunities exist for service companies?

Construction retains the largest wallet share, yet decommissioning and digital-oilfield upgrades grow quickest, offering specialist contractors high-margin niches.

Which technologies are most in demand?

Subsea production systems, floating LNG, carbon capture, and predictive analytics platforms dominate procurement pipelines across upcoming projects.

Page last updated on: