Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

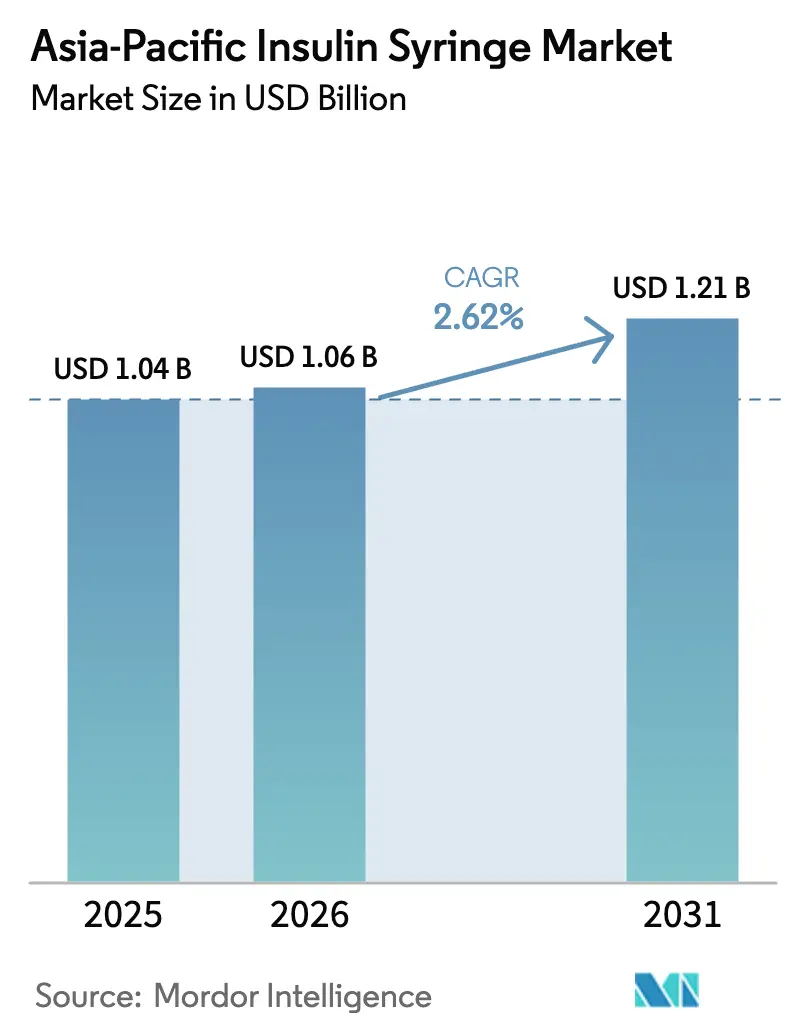

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 2.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Insulin Syringe Market Analysis by Mordor Intelligence

The Asia-Pacific Insulin Syringe Market size is projected to be USD 1.04 billion in 2025, USD 1.06 billion in 2026, and reach USD 1.21 billion by 2031, growing at a CAGR of 2.62% from 2026 to 2031.

Uptake remains anchored by the region’s 238 million diagnosed diabetics, yet the steady migration toward insulin pens and pumps tempers volume growth in the low-margin syringe category. Governments are widening screening and reimbursement, which enlarges the addressable pool of insulin prescribers, while price-cap policies in China and India compress manufacturer margins. Cost leadership, therefore, dominates competitive strategy, but suppliers simultaneously pursue ultrathin-wall needle innovations to defend pricing in urban hospitals. Near-shoring production to Malaysia and India shortens lead times and blunts China-centric supply risks, a shift that will influence raw-material sourcing and logistics during the forecast period.

Key Report Takeaways

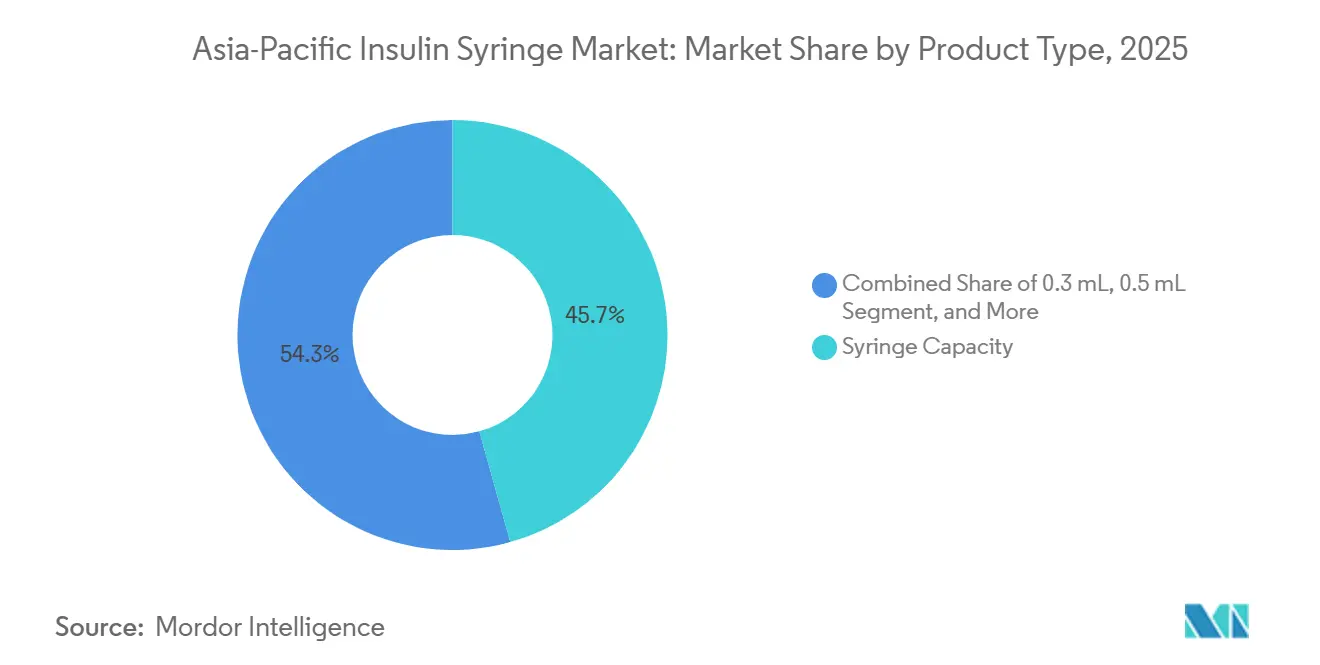

- By syringe capacity, the 0.5 mL format led with 45.67% revenue share in 2025, while the 0.3 mL is projected to expand at a 3.25% CAGR through 2031.

- By needle length, 6 mm captured 31.28% of revenue in 2025; 4 mm is on track for a 4.42% CAGR to 2031.

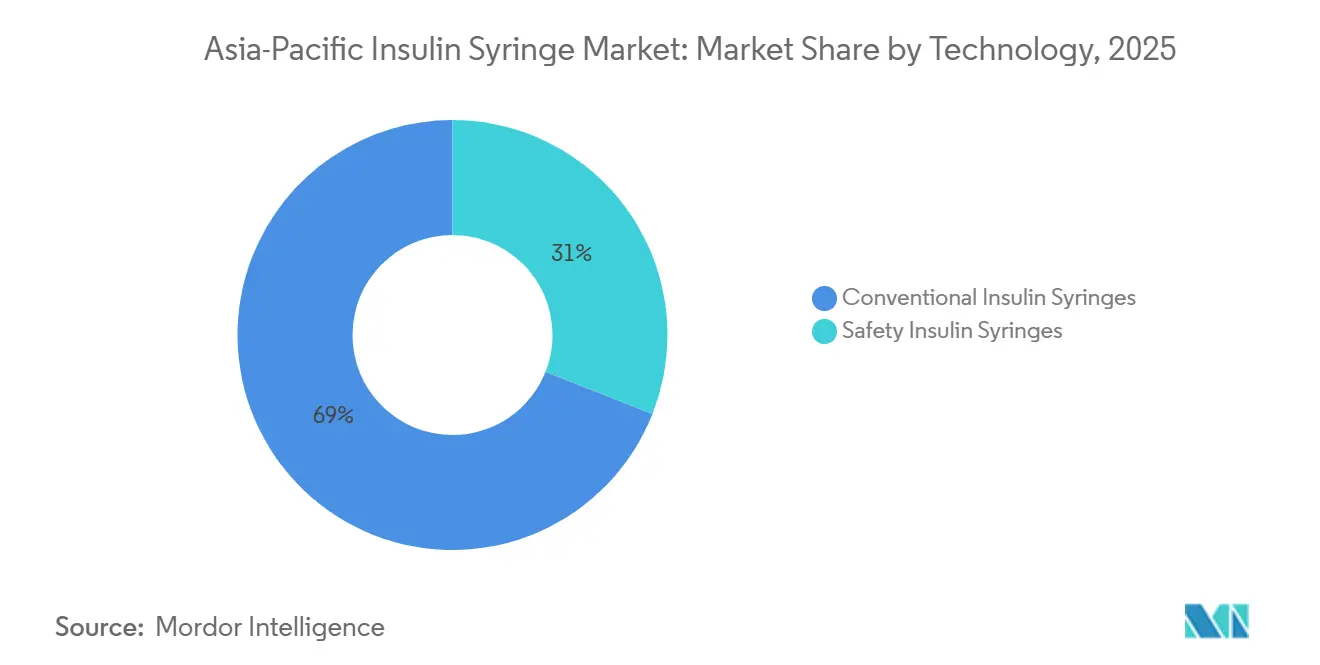

- By technology, conventional syringes accounted for 69.02% of 2025 shipments, whereas safety-engineered devices are advancing at a 2.98% CAGR.

- By end user, hospitals and clinics held a 57.39% share in 2025, yet home-care settings are growing the fastest at 3.87% through 2031.

- By geography, China accounted for 29.38% of 2025 revenue, and India is forecast to grow at a 5.18% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Insulin Syringe Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Diabetes Across Asia-Pacific | +0.7% | Global APAC, concentrated in China, India, Indonesia, with spillover to Southeast Asia | Long term (≥ 4 years) |

| Expanding Self-Administration of Insulin Therapies | +0.5% | India, Southeast Asia, China tier-2/3 cities | Medium term (2-4 years) |

| Favourable Government Reimbursement & Awareness Programmes | +0.4% | China, India, with early gains in Indonesia, Philippines, Malaysia | Medium term (2-4 years) |

| Ultra-Fine Gauge Innovation Boosting Patient Adherence | +0.3% | Japan, Australia, urban China, South Korea | Short term (≤ 2 years) |

| Growth of E-Pharmacy Supply Chains | +0.4% | China, India, urban Southeast Asia | Short term (≤ 2 years) |

| Near-Shoring of Syringe Manufacturing for Supply Security | +0.3% | Malaysia, Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes Across Asia-Pacific

More than 300 million adults in the Western Pacific and Southeast Asia were living with diabetes in 2024, yet undiagnosed rates still hovered near 50%.[1]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” diabetesatlas.org Indonesia’s undiagnosed share reached a staggering 73.2%, underlining the reservoir of latent demand that new screening programs can unlock. China’s 148 million diagnosed patients and India’s 90 million ensure a structural demand floor for the Asia-Pacific insulin syringe market even as pens gain ground. Rural affordability constraints keep syringes the default option where cold-chain infrastructure is weak. Earlier insulin initiation among younger cohorts also lengthens each patient’s lifetime device consumption.

Expanding Self-Administration of Insulin Therapies

Home-care settings are growing 3.87% per year as telemedicine removes geographic barriers to titration support. Syringes cost one-fifth as much as disposable pens in India and Indonesia, reinforcing their role as a cost-saving measure for out-of-pocket payers.[2]World Health Organization, “Global Report on Diabetes,” who.int Government reimbursement, such as India’s Ayushman Bharat, now covers both insulin and delivery devices, extending reach into low-income segments. Structured education programs mitigate dosing-error risks, although improved technique sometimes nudges urban patients toward pens, segmenting demand along socioeconomic lines. Manufacturers must therefore balance price leadership with patient-centric training materials.

Growth of E-Pharmacy Supply Chains

China’s online pharmacies processed over 1 billion prescriptions in 2024, with diabetes supplies ranking near the top. India’s e-commerce platforms expanded syringe listings by 35% after investing in cold-chain logistics for tier-3 cities. Regulators are tightening oversight; India’s drug-safety authority issued 12 alerts for counterfeit insulin syringes sold on unverified sites, making brand reputation critical. Indonesia and Malaysia granted dozens of new e-pharmacy licenses, accelerating direct-to-consumer penetration. Suppliers that secure preferred placement on these portals gain a price-volume edge, but must police gray-market imitators more vigorously.

Near-Shoring of Syringe Manufacturing for Supply Security

Malaysia will host a USD 67 million facility capable of packaging 30 million insulin doses annually from 2026, integrating on-site syringe assembly. Insulet’s USD 200 million Johor plant, opened in 2024, underscores Southeast Asia’s attractiveness as a hedge against China-centric risk. India’s Production Linked Incentive scheme reserves USD 1.2 billion for medical-device localization, targeting 50% import substitution by 2027.[3]Government of India, “Production Linked Incentive Scheme for Medical Devices,” investindia.gov.in As a result, landed costs across ASEAN will converge, eroding China’s historic 20-30% price advantage and pushing suppliers to compete on ISO 13485 quality credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of Insulin Pens & Pumps | -0.6% | Japan, Australia, New Zealand, urban China, South Korea | Short term (≤ 2 years) |

| Stringent Needle-Safety Compliance Costs | -0.3% | China, India, ASEAN markets implementing WHO sharps safety guidelines | Medium term (2-4 years) |

| Environmental Pressure on Single-Use Plastics | -0.2% | Australia, Japan, South Korea, with emerging regulations in China | Long term (≥ 4 years) |

| Domestic Price-Cap Policies in Emerging APAC | -0.4% | China, India, Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Insulin Pens & Pumps

Insulin pens accounted for 60% of new initiations in Japan and Australia in 2025, reflecting parity reimbursement and patient preference for discreet, pre-filled devices. New Zealand’s public funder now supports pump-CGM systems, cutting syringe demand in Type 1 patients. China’s tier-1 cities show similar momentum, with 48% of newly diagnosed Type 2 patients opting for pens in 2024. Yet syringes remain dominant in rural markets where affordability and limited cold-chain infrastructure inhibit pen adoption. Suppliers must therefore target value-conscious segments and public tenders while conceding market share in urban areas.

Domestic Price-Cap Policies in Emerging APAC

China’s 2024 volume-based procurement lowered median insulin prices by 42% and is now expanding to syringes, clipping margins by up to 20%. India’s price ceiling of INR 8-12 (USD 0.10-0.15) per unit forces multinationals either to localize production or exit high-volume tenders. Indonesia and the Philippines are drafting similar frameworks that favor scale players able to operate at unit costs below USD 0.05. Smaller firms face consolidation pressure as compliance costs for ISO certificates rise, even while selling prices fall.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Syringe Capacity: Pediatric Miniaturization Reinforces 0.3 mL Momentum

The Asia-Pacific insulin syringe market size for 0.5 mL formats accounted for 45.67% of 2025 revenue, yet 0.3 mL units are set to grow at 3.25% CAGR through 2031, driven by rising pediatric incidence and low-dose titration regimens. Endocrinologists prescribe smaller barrels to reduce insulin waste for children and elderly users who use 10 units or fewer per dose. China’s regulator approved six new pediatric designs in 2024, indicating policy support for diversifying capacity. However, tighter tolerances and 30-32G needles increase production costs by 8-12%, and India’s uniform price cap limits the ability to pass that premium to consumers.

The 1 mL format continues to be used for basal regimens above 30 units and remains common in obese Type 2 cohorts with insulin resistance. Syringes larger than 1 mL play a niche role in hospitals that handle U-500 insulin, but are losing relevance as pharmaceutical firms phase out high-volume vials in favor of concentrated pen cartridges. Consequently, the capacity mix will tilt toward sub-1 mL sizes while >1 mL volumes retreat to specialty clinics.

By Needle Length: Clinical Consensus Shifts Toward 4 mm

Six-millimeter needles retained 31.28% market share of the Asia-Pacific insulin syringe market in 2025, yet 4 mm variants are rising 4.42% per year as guidelines endorse shorter lengths to prevent intramuscular injections. Japan, Australia, and China integrated the 4 mm standard into 2025 protocols, accelerating hospital conversions. Manufacturers roll out ultrathin-wall steel and beveled-tip geometry that lowers insertion force by 18%, appealing to needle-phobic users.

Eight-millimeter products are declining, while ≥10 mm devices linger mainly in legacy rural inventories. Uptake of 4 mm requires a perpendicular technique and fresh patient training, driving demand for pictorial instructions and QR-code videos. Firms that embed education aids gain stickiness in the home-care channel.

By Technology: Safety Mechanisms Gain Reimbursement Traction

Conventional products accounted for 69.02% of 2025 volume, but safety syringes are advancing at 2.98% annually as WHO sharps-injury guidelines influence hospital tenders. China’s tertiary hospitals must now specify passive-retraction or shielding designs, although budget gaps delayed full roll-out. India mandated safety devices for government facilities in 2025, yet compliance reached only 38% by mid-2025 due to lagging allocations.

Home-care adoption is slower because users often reuse syringes, blunting the value proposition for single-use safety locks. Hybrid retractable needles that permit optional reuse are emerging, but their classification under ISO 23908 rules remains ambiguous. Thus, safety penetration will stay concentrated in hospitals until coverage expands

By End User: Home-Care Surge Alters Distribution Economics

Hospitals and clinics accounted for 57.39% of 2025 demand, yet home care is growing at a 3.87% CAGR as telehealth guidelines allow endocrinologists to adjust doses remotely. E-pharmacies fulfill doorstep delivery, reducing stock-out risk for chronic users. India plugged its national digital-health records into central syringe warehouses, bypassing district pharmacies prone to shortages.

Home-care growth obliges suppliers to refine packaging. A 2024 study found that 62% of first-time Indonesian users could not assemble syringes from written instructions alone; firms therefore embed multilingual QR videos to reduce error rates. Long-term care facilities and military medical services exhibit flat demand because they increasingly favor prefilled pens for workflow efficiency.

Geography Analysis

China accounted for 29.38% of 2025 revenue in the Asia-Pacific insulin syringe market, underpinned by its vast diabetic population and provincial procurement muscle. National price cuts suppress margins, and tier-1 cities now skew toward pens, yet rural areas continue to favor syringes due to affordability and limited cold-chain support. Domestic manufacturers such as Weigao secure tenders by coupling ISO 13485 compliance with low landed cost.

Japan shows the slowest growth, with pens capturing 68% of new prescriptions in 2025, and updated protocols advocate pump-CGM integration for Type 1 users. Australia follows suit after its regulator cleared four new pump models in 2024; private insurers widened coverage, compressing syringe uptake in metropolitan markets. New Zealand’s public funding for pumps in late 2024 will trim syringe volumes across Oceania.

India is forecast to expand at a 5.18% CAGR, propelled by 90 million diabetics and Production Linked Incentive support that encourages domestic syringe manufacturing. Price caps enlarge affordability but compel multinationals to localize or cede share. South Korea reimburses syringes for all Type 2 patients, but Seoul’s urban preference for pens exceeds 55%, creating a two-tier market dynamic.

The rest of Asia-Pacific, Indonesia, Thailand, Vietnam, and the Philippines, present the fastest aggregate growth. Indonesia’s 73.2% undiagnosed rate represents a sizable conversion pool as new screening programs roll out. Regulatory fragmentation across ASEAN, however, extends device registration by up to 18 months, favoring incumbents with regional compliance teams.

Competitive Landscape

The Asia-Pacific insulin syringe market is moderately fragmented. Becton, Dickinson, and Terumo lead the premium tier, leveraging ultrathin-wall needle technology and global ISO certifications to justify pricing in hospitals and diabetes centers. Chinese suppliers Weigao, Jiangsu Excel, and Zhejiang KangKang dominate public tenders through aggressive cost positioning.

Technology races center on flow-rate optimization. BD’s Neopak XtraFlow, introduced in September 2024, delivers 30% faster injection of high-viscosity formulations and pairs with Ypsomed’s autoinjector under an October 2024 alliance. Yet price-capped markets dilute returns on such R&D, forcing companies to reserve advanced products for private insurance or export channels.

Near-shoring reshapes supply chains. Pharmaniaga’s Malaysian plant will reduce transit times into Indonesia’s 20.4 million-patient market, while Insulet’s Johor facility underscores the region’s appeal to device makers hedging geopolitical risk. Mid-tier competitors lacking scale, such as Owen Mumford, which exited insulin pens in 2024, face exit or merger as compliance costs rise. E-pharmacy giants Alibaba Health and JD Health vertically integrate distribution, squeezing wholesale margins and giving preferred brands a jump in direct-to-patient volumes.

Asia-Pacific Insulin Syringe Industry Leaders

Terumo Corporation

Nipro Corporation

HMD Healthcare Ltd.

Cardinal Health Inc.

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: BD and Ypsomed collaborated on self-injection systems for high-viscosity biologics above 15 cP.

- March 2024: Owen Mumford partnered with Duopharma Biotech to scale syringe distribution in Southeast Asia.

Asia-Pacific Insulin Syringe Market Report Scope

Insulin syringes are used for self-injection and are available in multiple sizes to help deliver different doses of insulin.

The Asia-Pacific Insulin Syringe Market Report is Segmented by Syringe Capacity (0.3 mL, 0.5 mL, 1 mL, greater than 1 mL), Needle Length (4 mm, 6 mm, 8 mm, ≥10 mm), Technology (Conventional, Safety), End User (Hospitals & Clinics, Home-care, Diabetes Centres, Other), and Geography (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific). Market Forecasts are Provided in Terms of Value (USD).

By Syringe Capacity

| 0.3 mL |

| 0.5 mL |

| 1 mL |

| Greater than 1 mL |

By Needle Length

| 4 mm |

| 6 mm |

| 8 mm |

| ≥10 mm |

By Technology

| Conventional Insulin Syringes |

| Safety Insulin Syringes |

By End User

| Hospitals & Clinics |

| Home-care Settings |

| Diabetes Centres |

| Other End Users |

By Country

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Syringe Capacity | 0.3 mL |

| 0.5 mL | |

| 1 mL | |

| Greater than 1 mL | |

| By Needle Length | 4 mm |

| 6 mm | |

| 8 mm | |

| ≥10 mm | |

| By Technology | Conventional Insulin Syringes |

| Safety Insulin Syringes | |

| By End User | Hospitals & Clinics |

| Home-care Settings | |

| Diabetes Centres | |

| Other End Users | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large will the Asia-Pacific insulin syringe market be in 2031?

The Asia-Pacific insulin syringe market size is projected to reach USD 1.21 billion by 2031, reflecting a 2.62% CAGR from 2026 to 2031.

Which syringe capacity is growing the fastest?

The 0.3 mL capacity segment is forecast to post a 3.25% CAGR through 2031 as clinicians favor low-dose precision for pediatric and elderly patients.

Why are 4 mm needles gaining share?

Clinical guidelines released in 2024 recommend 4 mm lengths to cut intramuscular risk and injection pain, propelling 4.42% annual growth in this segment.

What factors are driving India’s demand?

India benefits from a 90 million-strong diabetic population, expanded insurance under Ayushman Bharat, and government incentives that localize syringe production, supporting a 5.18% CAGR.

How are e-pharmacies changing distribution?

Platforms like Alibaba Health and PharmEasy deliver syringes directly to patients, trimming stock-outs and prices while pushing manufacturers to secure digital shelf-space.

Page last updated on: