ASEAN Inland Waterway Freight Transport Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

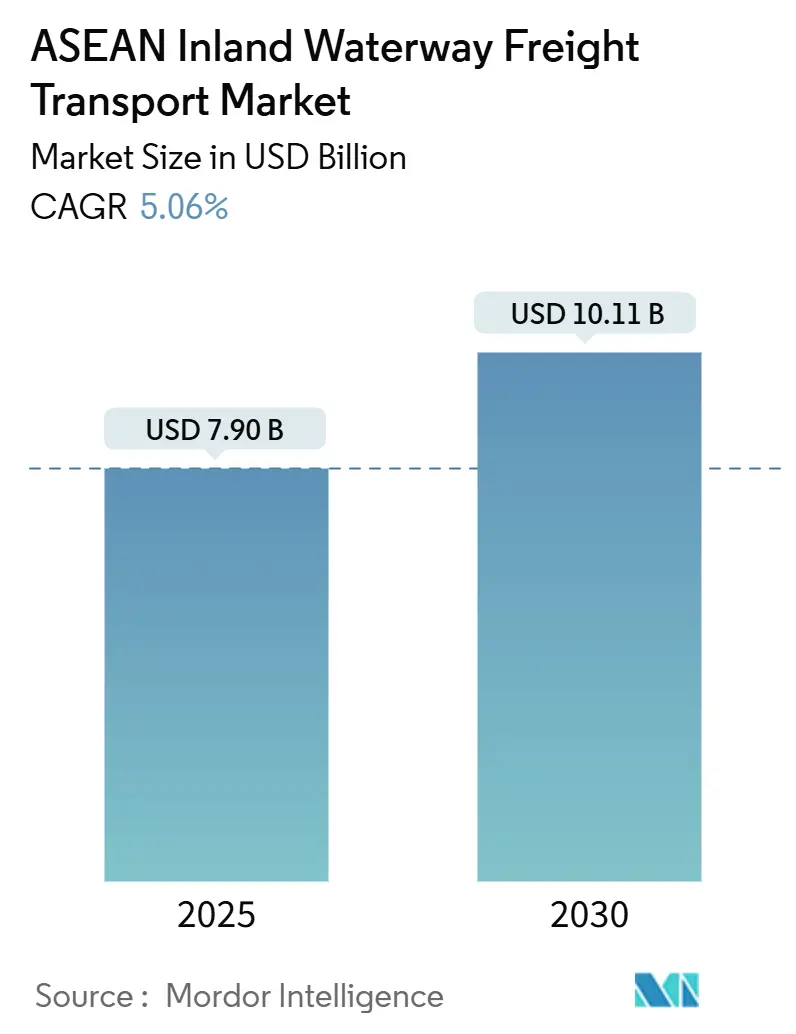

| Market Size (2025) | USD 7.90 Billion |

| Market Size (2030) | USD 10.11 Billion |

| Growth Rate (2025 - 2030) | 5.06% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Inland Waterway Freight Transport Market Analysis by Mordor Intelligence

The ASEAN Inland Waterway Freight Transport Market size is estimated at USD 7.90 billion in 2025, and is expected to reach USD 10.11 billion by 2030, at a CAGR of 5.06% during the forecast period (2025-2030).

Rising government investment in canals and river-port connectivity, a widening road-to-water freight cost gap, and mounting decarbonization pressure collectively underpin demand growth. Flagship projects such as Cambodia’s USD 1.7 billion Funan Techo Canal and China-backed Pinglu Canal are shortening export corridors and reinforcing the strategic value of cross-border waterways[1]Khmer Times, “Funan Techo Canal Project to Transform Cambodia's Economy,” khmertimeskh.com. Continuous dredging on Vietnam’s Mekong Delta and Indonesia’s Musi River, coupled with sustainable-finance flows from the Asian Development Bank and the International Finance Corporation, is accelerating upgrade cycles[2]World Bank, “World Bank Approves $400 Million for Vietnam Waterway Project,” worldbank.org. Simultaneously, digital river information systems in Thailand and Singapore are cutting idle time, while emerging carbon-pricing schemes across ASEAN tilt cargo away from congested highways toward barges.

Key Report Takeaways

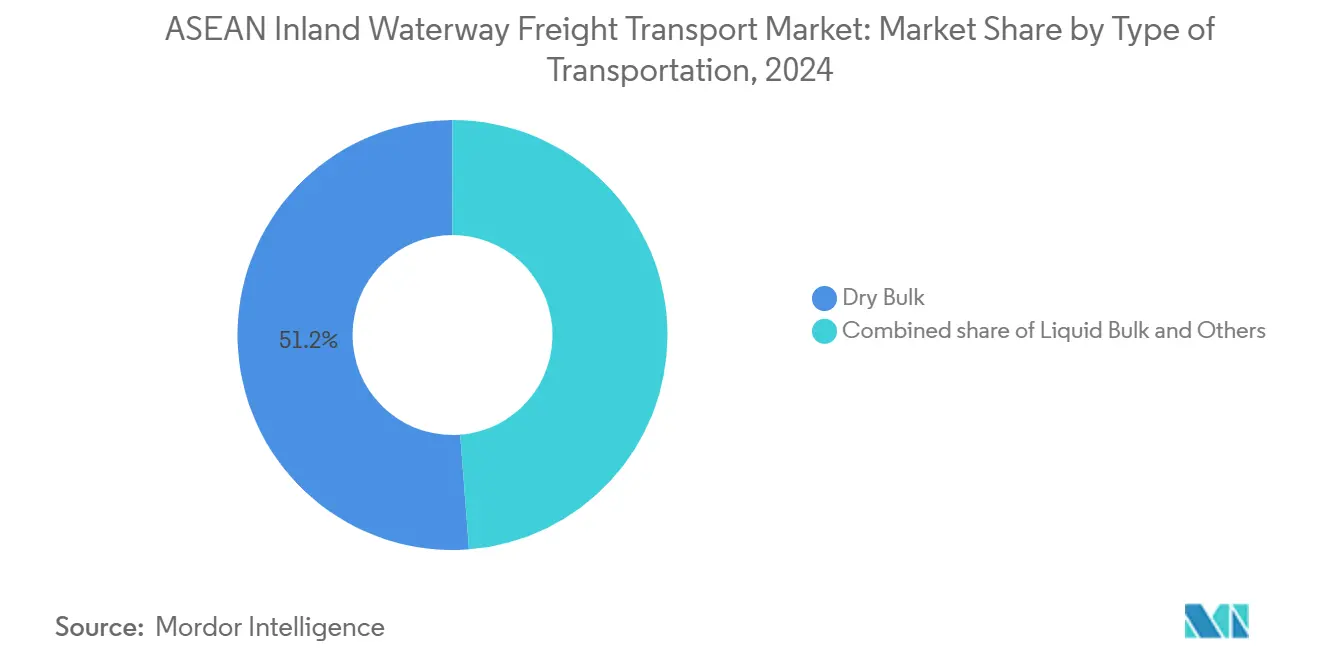

- By type of transportation, dry bulk held 51.23% of the ASEAN inland water freight transport market share in 2024, while liquid bulk is projected to expand at a 5.19% CAGR through 2030.

- By geography, Vietnam accounted for 21.81% share of the ASEAN inland water freight transport market size in 2024, and Indonesia is advancing at a 5.61% CAGR to 2030.

ASEAN Inland Waterway Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enhanced connectivity & inter-modal integration | +1.2% | Vietnam, Thailand, Cambodia, spillover to Malaysia | Medium term (2-4 years) |

| ASEAN export-led manufacturing fuelling container demand | +1.0% | Vietnam, Thailand, Indonesia, industrial corridors | Short term (≤ 2 years) |

| Digital river-information systems deployment | +0.6% | Thailand, Vietnam, pilot programs in Singapore | Medium term (2-4 years) |

| Cross-border carbon-pricing incentives shifting freight to water | +0.8% | Regional framework, early adoption in Singapore and Thailand | Long term (≥ 4 years) |

| Hydropower-lock openings extending navigable stretches | +0.7% | Mekong Basin and Chao Phraya | Long term (≥ 4 years) |

| Sustainable-finance-linked port investments | +0.5% | Vietnam, Indonesia, ADB and World Bank corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Enhanced Connectivity and Inter-Modal Integration

Inter-modal hubs that shift containers between barges, trains, and trucks are compressing transit times across the ASEAN inland water freight transport market. Vietnam’s USD 400 million Southern Waterway Connectivity Project will modernize 12 ports and build eight hubs by 2027, trimming Mekong-to-Ho Chi Minh City transit by 20%. Thailand’s proposed land-bridge, anchored by dual-gauge rail and river-barge feeders, is positioned as an alternative to the Malacca Strait, although feasibility remains under review. Cambodia’s 180-kilometer Funan Techo Canal will handle 3,000-tonne vessels and create a direct Phnom Penh-to-sea route by 2028. Across the region, harmonized draft standards under the ASEAN Connectivity Master Plan 2025 are being phased in, fostering interoperable barge fleets. These linkages collectively raise waterway capacity and reduce highway congestion.

ASEAN Export-Led Manufacturing Fueling Container Demand

Electronics, apparel, and processed-food clusters use inland barges to bypass congested roads and move boxes to deep-water ports, supporting growth in the ASEAN inland water freight transport market. Mekong Delta industrial parks generated 1.2 million TEU of barge traffic in 2024. Thailand’s Eastern Economic Corridor saw river-borne volumes rise 12% year-on-year as automotive and petrochemical exporters shifted to the Chao Phraya and Bang Pakong rivers. Java’s Ciliwung and Brantas rivers support 500-TEU barges linking factories to Tanjung Priok, although shallow drafts cap vessel size. Water freight costs average USD 0.04 per tonne-kilometer versus USD 0.12 by road, a differential that widens with higher fuel prices As export volumes scale, containerized barge demand keeps pace.

Digital River-Information Systems (RIS) Deployment

Real-time data platforms improve predictability and cut idle time, boosting throughput in the ASEAN inland water freight transport market. Thailand’s Chao Phraya RIS combines satellite altimetry, automated weather stations, and AIS feeds to deliver 48-hour draft forecasts, lowering turnaround time 15% during dry months. Vietnam is co-developing a Mekong RIS with the European Union for rollout on the Tien and Hau rivers by 2026. Singapore’s barge-scheduling API enables berth reservations 72 hours in advance and is already reducing idle time 20% for 23 operators[3]Maritime and Port Authority of Singapore, “Barge Scheduling API Launch 2024,” mpa.gov.sg. The ASEAN Digital Masterplan sets aside USD 50 million for cross-border data integration, though cybersecurity concerns have slowed adoption. As digital coverage widens, reliability and asset utilization rise.

Cross-Border Carbon-Pricing Incentives Shifting Freight to Water

Carbon policies are reshaping route decisions across the ASEAN inland water freight transport market. Singapore raised its carbon tax to SGD 25 per tonne in 2024, rising to SGD 45 by 2026, extending coverage to maritime bunkers and nudging shippers toward barges. Thailand’s voluntary carbon-credit pilot rewards operators that shift loads from road to water at THB 150 per tonne of avoided CO₂, attracting 12 logistics firms by early 2025. Vietnam’s Gemadept and Indonesia’s Pelabuhan Indonesia now issue carbon-intensity certificates to help exporters comply with the EU’s Carbon Border Adjustment Mechanism from 2026. Adoption remains uneven because Malaysia and the Philippines have yet to legislate binding carbon prices, but regional harmonization talks continue under the ASEAN Green Deal.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity & customs delays | −0.9% | Cross-border Mekong and Chao Phraya corridors | Short term (≤ 2 years) |

| Aging lock & channel infrastructure | −0.7% | Vietnam, Thailand, Indonesia | Medium term (2-4 years) |

| Draft volatility from climate-driven river levels | −0.8% | Mekong Basin, Chao Phraya | Long term (≥ 4 years) |

| Competition from emerging freight-rail corridors | −0.6% | Thailand-China, Malaysia ECRL, Vietnam North-South | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity and Customs Delays

Fragmented documentation and divergent vessel standards add two to four days of dwell time and erode the cost advantage of the ASEAN inland water freight transport market. Only 60% of river ports are linked to the ASEAN Single Window, forcing operators to file paper manifests at many crossings. Vietnam and Cambodia lack mutual recognition of barge registration, compelling duplicate fees of roughly USD 1,200 per crossing. Thailand’s pre-arrival clearance pilot trims processing from 18 hours to six on the Chao Phraya, yet it is not interoperable with neighboring Laos. Divergent safety rules further complicate operations; Indonesia mandates double-hull petroleum barges, while Malaysia still accepts legacy single-hull vessels.

Aging Lock and Channel Infrastructure

Legacy locks and underfunded dredging schedules constrain load factors and raise unit costs within the ASEAN inland water freight transport market. The average chamber length in Vietnam’s Mekong Delta is 60 meters, forcing operators to split 1,000-tonne convoys into 300-tonne segments and increasing handling costs by 25%. Thailand’s 1957-era Chai Nat lock suffers 12 mechanical failures annually, creating harvest-season queues of up to 48 hours. Budget gaps stretched dredging intervals on Indonesia’s Musi River from six to 14 months, reducing navigable days 30% in 2024. The Asian Development Bank pegs the upgrade bill at USD 12 billion over the next decade, dwarfing current funding commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Transportation: Bulk Dominance Masks Liquid Surge

Dry bulk cargo commanded 51.23% of the ASEAN inland water freight transport market in 2024, reflecting the region’s outsized movement of rice, coal, and construction aggregates along the Mekong, Chao Phraya, and Sumatran rivers. Within this mix, Vietnam routed 40% of its 7.8 million-tonne rice exports by barge, while Kalimantan floated one-quarter of Indonesia’s 120 million-tonne coal exports to coastal transshipment zones. Urban mega-projects in Bangkok, Jakarta, and Ho Chi Minh City collectively absorbed 15 million tonnes of sand and gravel by river, though Cambodia and Vietnam have begun curbing riverbed dredging to stem ecological damage. Looking forward, dry bulk tonnage is expected to rise in line with construction and energy demand, yet modal substitution toward rail in Thailand and Vietnam could soften its share after 2028.

Liquid bulk, although smaller, is advancing fastest at a projected 5.19% CAGR as refiners and chemical producers seek flexible, lower-carbon distribution. Singapore’s 1.5 million-barrel-per-day refining hub now dispatches diesel and gasoline upriver to Malaysia and Thailand, sidestepping congested tanker trucking. Chemical feedstocks for Thailand’s plastics plants increasingly move via tank barges on the Chao Phraya, with 2024 volumes up 18% year-on-year. Edible-oil flows remain pivotal; 2.5 million tonnes of palm oil traversed the Musi and Rajang rivers in 2024, underlining river dependency in Sumatra and Sarawak. Emerging electric-powered tugboats and shore power at terminals, funded through green bonds, will further lift the competitiveness of liquid-bulk barging.

Geography Analysis

Vietnam’s dominant 21.81% share in 2024 stems from unrivaled channel density, strong rice and seafood exports, and growing containerized electronics output. The ongoing Southern Waterway Connectivity Project will dredge 450 kilometers for 1,000-tonne barges and install eight inter-modal hubs, aiming for a 20% transit-time reduction to Cai Mep by 2027. Complementing these upgrades, a Mekong RIS platform is slated to go live in 2026, allowing shippers to optimize routing using real-time data.

Indonesia’s 5.61% CAGR through 2030 reflects coal and palm-oil corridors in South Kalimantan and Sumatra. Three new river terminals add 5 million-tonne coal capacity and have already cut coastal truck queues 30%. Nonetheless, the Musi River’s extended dredging intervals reduced navigable days by 30% in 2024, highlighting a need for sustained capital allocation. The government targets logistics-cost reduction from 24% to 17% of GDP by 2030 under the National Logistics Ecosystem Roadmap.

Thailand leverages the Chao Phraya and Bang Pakong for agro-industrial flows, but aging locks and variable drafts impose capacity ceilings. The new RIS reduced dry-season delays and supports automotive exports from the Eastern Economic Corridor, where barge volumes climbed 12% in 2024. Singapore, despite limited inland rivers, drives regional efficiency with its berth-reservation API, now used by 23 operators. Malaysia’s Sarawak-based Rajang supports timber, and the Philippines advances Pasig River logistics to relieve Metro Manila road congestion.

Competitive Landscape

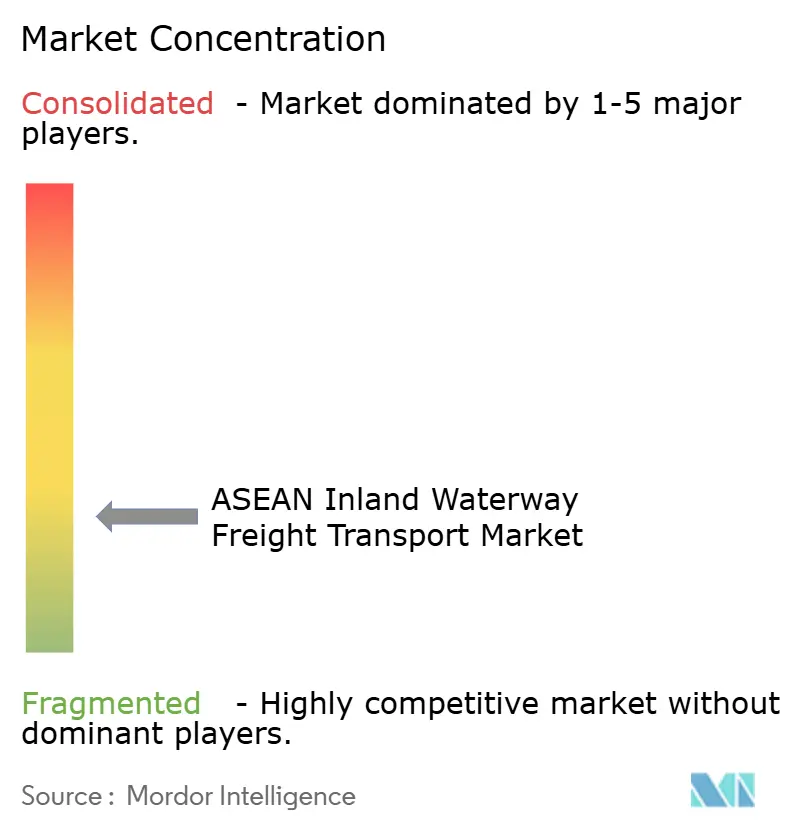

The ASEAN inland water freight transport market exhibits moderate fragmentation, with global container lines partnering local specialists to extend hinterland reach. CMA CGM’s 30% stake in Gemadept aligns both firms on developing Mekong Delta terminals. Maersk’s 10-year pact with Siam Shipping deploys 15 dedicated barges linking Thai upcountry depots to Laem Chabang, enhancing service reliability for automotive exporters.

Regional specialists differentiate through digitalization and sustainability. Gemadept’s green bond finances electric tugboats and shore power at Can Tho, targeting a 40% diesel cut. PT Pelabuhan Indonesia’s sustainability-linked loan ties interest rates to ISO 14001 certification at 80% of river ports by 2027. Digital differentiation spans real-time draft monitoring, automated lock scheduling, and carbon-intensity reporting, capabilities that attract multinationals seeking verifiable low-emission logistics.

White-space opportunities center on cross-border canals and under-served eastern Indonesian rivers. The 180-kilometer Funan Techo Canal will let Cambodia bypass Vietnamese routes and could redirect container lines seeking fresh capacity. Eastern Kalimantan and Papua, producing 60% of Indonesia’s coal and timber, host undercapitalized river systems with fewer than 20 operators, presenting scope for consolidation and shallow-draft fleet investment.

ASEAN Inland Waterway Freight Transport Industry Leaders

CMA CGM

Rhenus Logistics

Gemadept Corporation

DP World

Maersk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Gemadept secured a VND 3 trillion (USD 120 million) green bond to finance electric tugboats and shore-power installations, targeting a 40% diesel reduction at Mekong Delta terminals.

- June 2024: PT Pelabuhan Indonesia opened three South Kalimantan river terminals with 5 million-tonne capacity, easing coastal congestion by 30%.

- June 2024: The International Finance Corporation extended a USD 150 million sustainability-linked loan to PT Pelabuhan Indonesia, tying rates to ISO 14001 certification for 80% of river ports by 2027.

- March 2024: Gemadept announced a USD 200 million expansion of Can Tho Port, adding 2 million TEU capacity and automated cranes for 1,000-tonne barges by 2026.

ASEAN Inland Waterway Freight Transport Market Report Scope

| Liquid Bulk |

| Dry Bulk |

| Others |

| Singapore |

| Thailand |

| Vietnam |

| Indonesia |

| Malaysia |

| Philippines |

| Rest of ASEAN |

| By Type of Transportation | Liquid Bulk |

| Dry Bulk | |

| Others | |

| By Country | Singapore |

| Thailand | |

| Vietnam | |

| Indonesia | |

| Malaysia | |

| Philippines | |

| Rest of ASEAN |

Key Questions Answered in the Report

How large is the ASEAN inland waterway freight transport market in 2025?

The market is valued at USD 7.90 billion in 2025 and is projected to expand to USD 10.11 billion by 2030.

Which cargo type leads ASEAN inland waterways?

Dry bulk holds 51.23% share, led by rice, coal, and construction aggregates.

Which segment is growing fastest?

Liquid bulk is advancing at a 5.19% CAGR thanks to petroleum, chemical, and edible-oil flows.

Which country dominates regional inland waterway freight?

Vietnam accounts for 21.81% of traffic due to its dense Mekong Delta network and port upgrades.

Where is growth strongest through 2030?

Indonesia is forecast to post a 5.61% CAGR as new river terminals ramp up in Sumatra and Kalimantan.

What technology boosts efficiency on ASEAN rivers?

Real-time river-information systems and berth-reservation APIs cut idle time and improve load planning.

Page last updated on: