Ascites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ascites Market Analysis by Mordor Intelligence

The Ascites Market size was valued at USD 1.88 billion in 2025 and is estimated to grow from USD 1.98 billion in 2026 to reach USD 2.56 billion by 2031, at a CAGR of 5.29% during the forecast period (2026-2031).

The Ascites Market is expanding as the patient pool with advanced liver disease continues to grow, particularly in healthcare settings where metabolic dysfunction-associated steatohepatitis (MASH) and cirrhosis are increasing pressure on hospital systems. Decompensated disease drives significantly higher treatment costs than compensated disease, keeping repeat procedures, inpatient care, and supportive therapies central to the Ascites Market over the forecast period. Growth is further supported by the first active implantable pump approved in the United States, which has created a new treatment category between repeated paracentesis and more invasive escalation pathways. However, the market continues to rely heavily on palliative management, as no approved therapy reverses established cirrhosis at scale, sustaining treatment utilization while limiting broader market transformation.

Key Report Takeaways

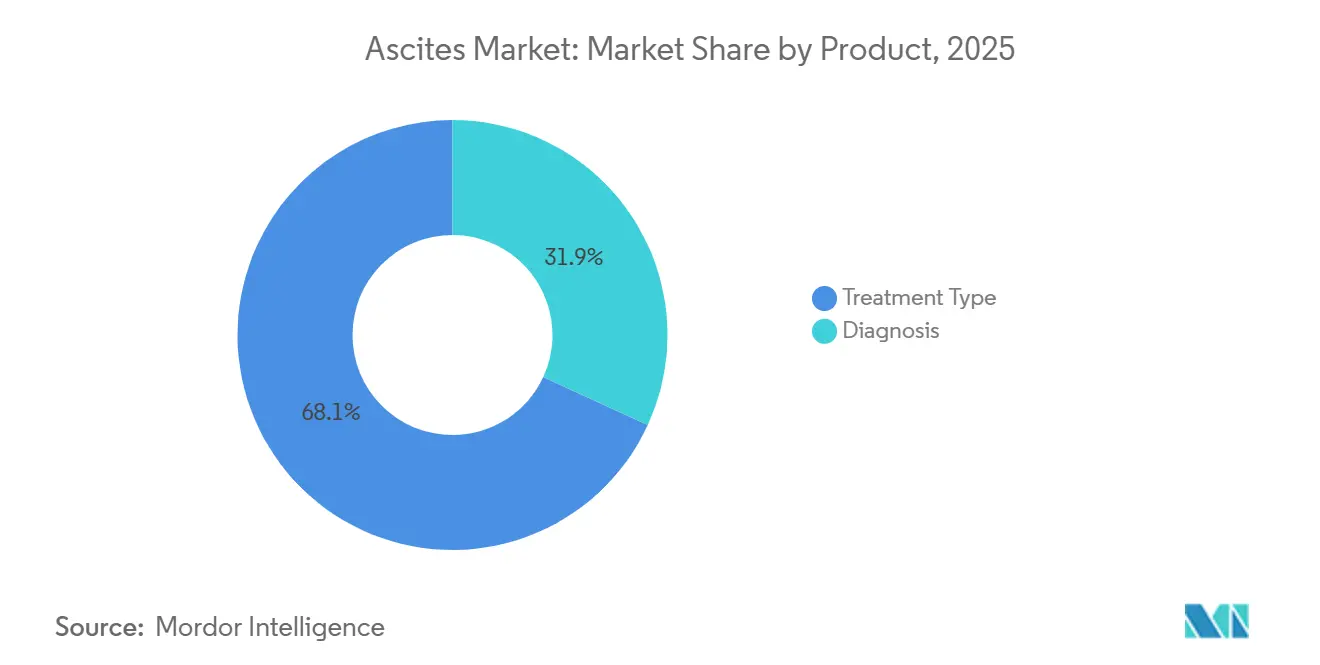

- By product, treatment type held 68.12% share in 2025, while diagnosis is projected to expand at a 5.93% CAGR through 2031.

- By ascites type, refractory ascites accounted for 46.45% share in 2025, while malignant ascites is projectedto grow at a 6.67% CAGR through 2031.

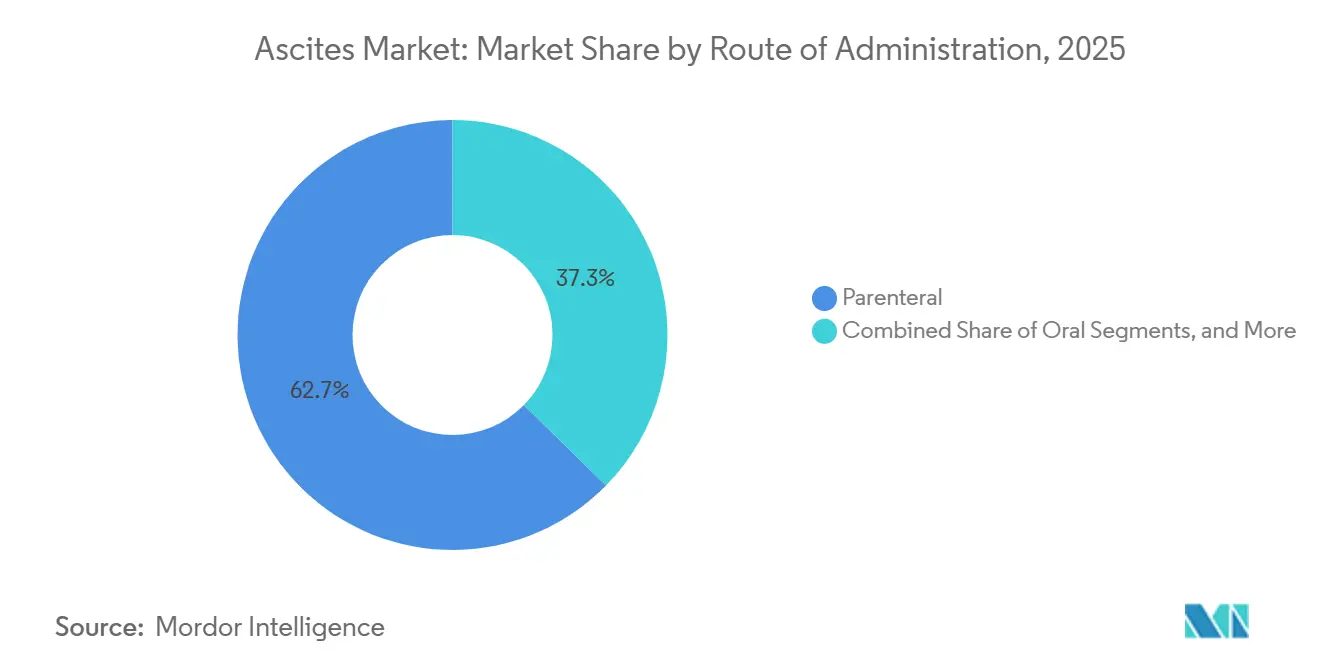

- By route of administration, parenteral captured 62.66% share in 2025, while device-based delivery is expected to record the highest 7.35% CAGR through 2031.

- By end user, hospitals represented 52.34% share in 2025, while home care settings are projected to grow at a 6.78% CAGR through 2031.

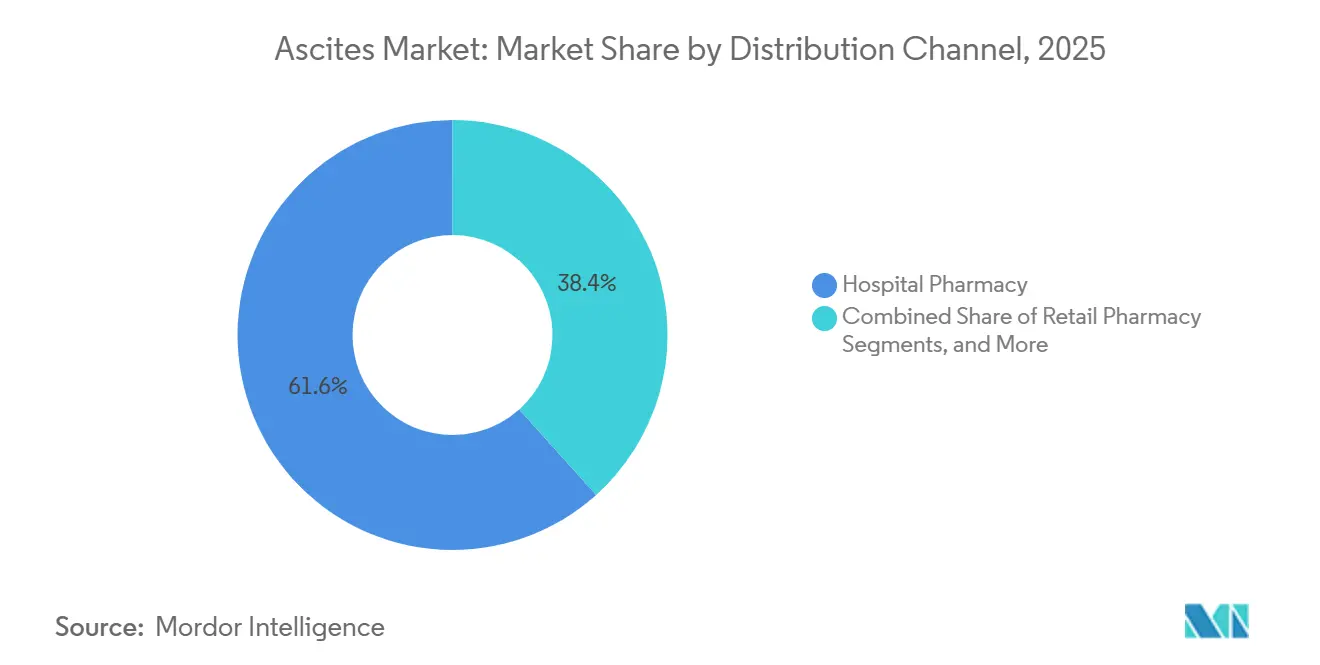

- By distribution channel, hospital pharmacy held 61.65% share in 2025, while retail pharmacy is projected to advance at an 8.24% CAGR through 2031.

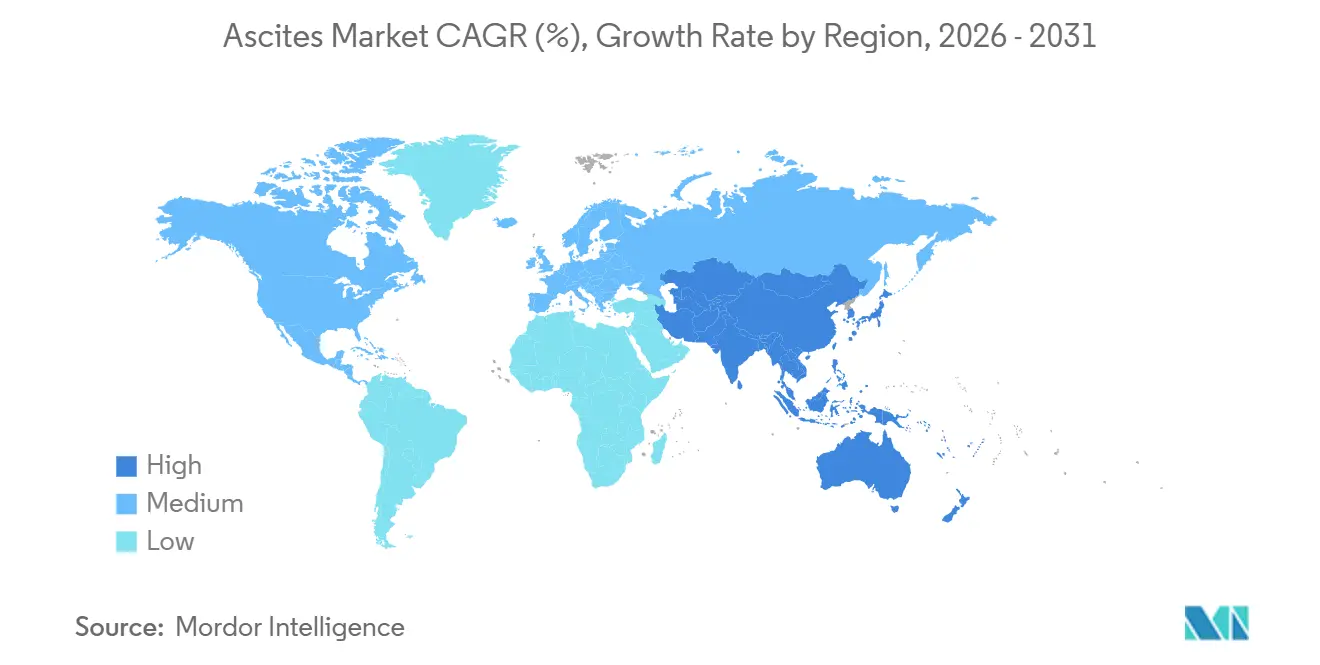

- By geography, North America commanded 39.56% of the Ascites market share in 2025, while Asia-Pacific is expected to post the fastest regional 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ascites Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising cirrhosis and MASH-linked ascites burden | +1.4% | Global, concentrated in North America and Asia-Pacific | Long term (≥ 4 years) |

| Repeat paracentesis demand in refractory ascites | +0.9% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Broader use of albumin after large-volume paracentesis | +0.8% | Global, with compliance factors active in North America and EU | Medium term (2-4 years) |

| First us approval of an active implantable ascites pump | +0.7% | North America primary, spill-over to EU and APAC | Short term (≤ 2 years) |

| Earlier intervention in high-risk decompensated liver disease | +0.6% | Global, with early gains in North America, EU, Japan | Medium term (2-4 years) |

| Remote monitoring and digital follow-up for chronic ascites care | +0.4% | North America and EU, early APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cirrhosis And MASH-Linked Ascites Burden

The Ascites Market remains closely tied to the growing burden of advanced liver disease, with MASH-linked cirrhosis emerging as a key long-term demand driver. JAMA Network Open projected United States MASH cases to increase from 14.9 million in 2020 to 23.2 million by 2050, while MASH cirrhosis cases are projected to rise by 91.1%, from 1.147 million to 2.192 million. This is important because ascites is a common late-stage complication of cirrhosis, creating sustained demand for hospitalization, albumin use, imaging, drainage, and follow-up care.[1]JAMA Network Open, “Estimated Burden of Metabolic Dysfunction-Associated Steatotic Liver Disease in US Adults, 2020 to 2050,” JAMA Network Open, jamanetwork.com Liver Cancer International showed that total healthcare costs for MASH patients with cirrhosis were 1.3 to 2.7 times higher than for those without cirrhosis, while inpatient costs were as much as 13 times higher in decompensated disease than in compensated disease. China’s projected increase in the age-standardized Metabolic Dysfunction-Associated Steatotic Liver Disease (MASLD)-related cirrhosis burden through 2036 further strengthens the Asia-Pacific outlook and supports a broader treatment base in the region.

Repeat Paracentesis Demand In Refractory Ascites

The Ascites Market continues to gain from repeat procedure demand, as clinicians mainly manage refractory ascites through symptom control rather than durable reversal. Refractory Ascites held a 46.45% share in 2025, generating recurring hospital traffic through repeated large-volume paracentesis, albumin replacement, and ongoing monitoring. Current Hepatology Reports noted that each large-volume paracentesis session removes 21 g of protein per liter of ascitic fluid, contributing to malnutrition and sarcopenia.[2]Liver Cancer International, “The Economic Burden of Metabolic Dysfunction-Associated Steatohepatitis With Cirrhosis, A Systematic Review,” Liver Cancer International, doi.org This reinforces recurring demand for kits, consumables, infusion therapies, and hospital services, especially where repeat drainage remains the standard pathway for late-stage patients. The REDUCe2 trial in England is comparing palliative long-term abdominal drains with hospital-based large-volume paracentesis, indicating that future demand may shift toward a more distributed care model rather than decline. The same treatment burden is also supporting earlier intervention discussions, which may move some revenue from late-stage repetitive procedures toward earlier interventional management.

Broader Use Of Albumin After Large-Volume Paracentesis

Broader and more clearly defined albumin use in routine care, particularly after paracentesis, continues to support the Ascites Market. The American Gastroenterological Association (AGA) Clinical Practice Update recommended 20-25% intravenous albumin at 6-8 g per liter removed after paracentesis exceeding 5 L. It also recommended considering albumin in lower-volume procedures when patients present with hypotension, renal insufficiency, or electrolyte abnormalities. This expands albumin use beyond a strict volume threshold and provides a clearer framework for repeated supportive therapy in higher-risk patients. The Chinese guidelines on the management of ascites in cirrhosis, published in 2024, also embedded intravenous albumin as protocol-standard therapy after large-volume paracentesis. These updates support stronger hospital adherence, formulary planning, standardized procurement, and repeat utilization, making supportive care a dependable revenue pillar for the Ascites Market.

First US Approval Of An Active Implantable Ascites Pump

The Ascites Market reached an important turning point when the United States approved the first active implantable pump for recurrent or refractory ascites due to liver cirrhosis. Sequana Medical received United States Food and Drug Administration (FDA) Premarket Approval for the alfapump in December 2024, creating the first Class III active implantable device in this care setting and offering a device-based alternative to repeated therapeutic drainage. The company reported in February 2026 that the POSEIDON study showed virtual elimination of therapeutic paracentesis and quality-of-life improvement at 6 and 24 months. It also reported that five United States centers had already completed implants since launch, with discussions active at more than 20 additional institutions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited disease-modifying options for root-cause reversal | -1.0% | Global | Long term (≥ 4 years) |

| Procedure dependence and infection risk in long-term drainage | -0.8% | Global, highest in low-to-middle-income markets | Medium term (2-4 years) |

| Reimbursement variability across care settings and countries | -0.7% | Global, highest impact in APAC, MEA, South America | Long term (≥ 4 years) |

| Narrow eligible population for device-based therapy | -0.5% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Disease-Modifying Options For Root-Cause Reversal

A key structural restraint in the Ascites Market is the lack of a broadly approved therapy that can reverse the underlying disease process in established cirrhosis. The 2025 review in Annals of Hepatology found that long-term albumin can reduce the incidence of complications, but randomized evidence has not yet demonstrated a transplant-free survival benefit at the population level. This gap keeps the treatment pathway focused on symptom control and sustains demand through repeated treatment cycles. However, these cycles do not fully reset patient risk or materially shorten disease duration. Patients must still follow sodium restriction below 2,000 mg/day, undergo long diuretic titration periods, make repeat hospital visits, and receive ongoing monitoring. These requirements can weaken adherence and reduce the real-world effectiveness of standard care. As a result, the market continues to generate demand from chronic care but struggles to unlock the value expansion typically associated with durable therapeutic change. Until care moves beyond palliative control, the Ascites Market will continue to grow through higher volume and treatment intensity rather than a true transformation of the treatment pathway.

Procedure Dependence And Infection Risk In Long-Term Drainage

The Ascites Market also faces a practical restraint, as long-term drainage approaches can carry meaningful complication risks, particularly outside tightly managed specialist settings. The 2025 review published by Karger reported kidney injury in 17-50% of patients when drainage exceeded 1.5 liters per day, while catheter-related infections, including cellulitis and peritonitis, occurred in 7-58% of patients. These risks are significant because the market’s fastest-growing care settings depend on safe expansion beyond hospitals. However, infection management, antibiotic access, and timely clinical response vary across countries. This uneven access slows the scalability of home-based drainage models in cost-sensitive systems and limits the pace at which parts of the Ascites Market can shift toward lower-acuity care channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Treatment Type Anchors Revenue While Diagnostics Extend The Care Pathway

Treatment type is expected to account for 68.12% of the Ascites market size in 2025, showing that active management of fluid accumulation continues to drive commercial activity across the care pathway. This segment includes diuretics, paracentesis, albumin infusion, transjugular intrahepatic portosystemic shunt, liver transplantation, implantable pump therapy, and palliative long-term abdominal drainage.

Diagnosis is projected to grow at a CAGR of 5.93% through 2031, making it the fastest-growing product category in the Ascites Market despite its smaller 2025 revenue base compared to treatment. Growth reflects a more protocol-driven care pathway supported by ultrasound-guided paracentesis, imaging-based quantification, and more consistent differential diagnosis. Regular disease monitoring increases diagnostic use, as each imaging touchpoint can support treatment selection, procedural planning, or complication follow-up.

By Ascites Type: Refractory Dominates While Malignant Ascites Draws The Pipeline

Refractory ascites is expected to hold a 46.45% share in 2025, making it the largest type-based contributor to the Ascites Market and highlighting the revenue impact of late-stage patients. These patients often need repeated large-volume paracentesis, frequent albumin use, closer inpatient observation, and complex escalation decisions, which increases resource utilization. The clinical burden extends beyond fluid accumulation, as spontaneous bacterial peritonitis, hepatorenal syndrome, and repeat hospitalization often accompany refractory disease. This keeps the refractory patient pool central to the Ascites Market, especially in North America and Europe, where specialized hepatology infrastructure supports recurring procedural care at scale.

Malignant ascites is expected to advance at a CAGR of 6.67%, making it the fastest-growing type segment and one of the key innovation-led areas of the Ascites Market through 2031. Growth is expected to come from pipeline-led advances rather than only incremental improvements in drainage. A Phase III randomized trial of M701, an EpCAM×CD3 bispecific antibody administered intraperitoneally, is expected to report results at American Society of Clinical Oncology (ASCO) 2026, underscoring active development in malignant ascites. Multiple early-phase programs mentioned in the user draft, including autologous tumor-reactive T-cell and other biologic approaches, are positioning the intraperitoneal setting as a therapeutic target rather than only a drainage challenge.

By Route Of Administration: Parenteral Sustains Volume While Device-Based Delivery Redefines Care Boundaries

Parenteral administration is expected to hold 62.66% of the Ascites market size in 2025, reflecting the continued importance of intravenous albumin, inpatient diuretic use, and other hospital-based supportive interventions. This route remains dominant because albumin remains linked to large-volume paracentesis protocols, and many patients enter care when oral control is no longer adequate. Parenteral therapy also captures a sizable share of hospital admission value, as fluid management, complication control, and monitoring often occur together in higher-acuity settings.

Device-based delivery is forecast to grow at a CAGR of 7.35%, the fastest pace among all routes, creating a meaningful shift in treatment delivery within the Ascites Market. The planned commercial launch of the alfapump from Q4 2025 is expected to give recurrent or refractory cases a technology-led option that can reduce reliance on repeat therapeutic paracentesis. Device-based care also has a clearer reimbursement pathway, as Centers for Medicare & Medicaid Services (CMS) support and procedure coding reduce adoption barriers for transplant and advanced hepatology centers.

By End User: Hospitals Anchor Care While Home Settings Accelerate

Hospitals are expected to represent a 52.34% share in 2025, and they remain the leading end-user category in the Ascites Market because complex patients require specialist oversight, inpatient stabilization, and interventional escalation. Hospital systems manage the heaviest burden of refractory disease, spontaneous bacterial peritonitis, hepatorenal syndrome, implant procedures, and advanced imaging. They also influence purchasing decisions for albumin, paracentesis kits, drainage systems, and procedural support products through formulary and procurement structures.

Home care settings are projected to grow at a CAGR of 6.78%, making them the fastest-growing end-user group in the Ascites Market as providers pursue lower-acuity and more patient-convenient care models. Growing support for palliative long-term abdominal drains and telehealth-guided follow-up indicates that home care is becoming a more recognized part of the care pathway. Even a partial migration of stable follow-up and selected drainage support can influence product mix and dispensing channels.

By Distribution Channel: Hospital Pharmacy Dominates But Retail Disruption Is Underway

Hospital pharmacy is expected to hold 61.65% of the Ascites market size in 2025, consistent with a treatment pathway centered on inpatient care, infusion support, and hospital-administered therapies. This channel remains dominant because albumin, intravenous diuretics, and a large share of supportive medicines are tied to hospital episodes rather than routine community refills. Procurement concentration strengthens this role, as hospital systems often negotiate directly with suppliers and place volume through structured contracts.

Retail pharmacy is projected to grow at a CAGR of 8.24%, the fastest among distribution channels, indicating a gradual outpatient shift in the Ascites Market. Stable cirrhosis patients who remain on oral diuretics or move through community-based follow-up naturally expand retail dispensing volume, provided adherence and monitoring can be maintained.

Geography Analysis

North America is expected to account for 39.56% of the ascites market share in 2025, making it the largest regional contributor and reinforcing its position as the commercial center of the ascites market. The United States leads the region, supported by advanced hepatology networks, high procedural capacity, strong hospital purchasing systems, and the first approved active implantable device for recurrent or refractory cirrhotic ascites. The expected alfapump launch in the fourth quarter (Q4) of 2025 is set to add a device-backed treatment option to the US care pathway and reduce reliance on repeated drainage. Centers for Medicare & Medicaid Services (CMS) New Technology Add-on Payment support, effective October 1, 2025, is expected to improve inpatient reimbursement and support hospital adoption.

Europe represents the second major regional block in the ascites market, backed by established hepatology practice, broad use of paracentesis and albumin, and relevant experience with device-led care. Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe support a structured care environment for advanced liver disease through specialist referrals and hospital-based management. Prior familiarity with the alfapump under European approval pathways gives the region a clinical base for future uptake where reimbursement and patient selection align. The REDUCe2 trial in the United Kingdom is expected to provide health-system evidence on palliative long-term abdominal drains and may influence procurement in home-oriented care models.

Asia-Pacific is forecast to expand at a CAGR of 8.56%, making it the fastest-growing regional part of the ascites market through 2031. Large hepatitis B and hepatitis C patient pools, the continuing burden of alcohol-related liver disease, and improving interventional radiology capacity support regional growth. India remains a key market, with 40 million people affected by hepatitis B, 12 million affected by hepatitis C, and the Ayushman Bharat program reaching 500 million people, supporting broader access to hepatology services. China is also important, as a 2025 trial in Gut showed that rice-derived recombinant human serum albumin performed comparably to plasma-derived albumin in decompensated cirrhosis, with implications for supply and cost dynamics.

Competitive Landscape

The Ascites Market is moderately fragmented, with competition spread across large procedural suppliers, albumin manufacturers, and clinical-stage innovators rather than led by a single dominant company. BD, Cardinal Health, B. Braun, AngioDynamics, Cook Medical, Teleflex, Baxter, Fresenius, and Boston Scientific compete across consumables, access products, and hospital relationships that support routine drainage and related procedures. These companies gain strength from contract execution, sterile supply standards, logistics, and their presence in high-volume hospital workflows. As a result, procurement strategy plays a key role in the Ascites Market, where vendor scale, reliability, and institutional relationships often carry as much weight as clinical differentiation in standard procedural care.

Albumin and infusion-related suppliers form a second competitive layer in the Ascites Market, with positioning driven by guideline alignment, hospital formulary access, and repeat clinical use. Albumin remains a protocol-backed component of care after large-volume paracentesis and in selected higher-risk patients, supporting recurring hospital demand. Clinical-stage developers form a third layer as they work to move the Ascites Market beyond repeated drainage and symptomatic control. Sequana Medical remains the clearest example, with expected United States approval in December 2024, planned first commercial implants in Q4 2025, and targeted expansion to five US implanting centers by February 2026. BioVie also reflects strategic movement, as its planned 2026 S-1 registration statement filing for Option Therapeutics is designed to house BIV201 and support a planned registrational Phase 3 program with USD 25-30 million in targeted funding.

Pipeline activity shows that the Ascites Market is not moving in a single direction, as cirrhosis-linked ascites and malignant ascites are attracting different competitive strategies. Device-led companies are focusing on reducing procedure repetition and improving quality of life, while biologic and oncology-focused developers are assessing whether the peritoneal setting can support more active disease-directed treatment. Intellectual property remains important because patent positions can influence investor interest, clinical partnering, and eventual market access before commercialization.

Ascites Industry Leaders

F. Hoffmann-La Roche Ltd

BioVie Inc.

Novartis AG

Sequana Medical N.V.

Boston Scientific Corporation

AngioDynamics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Sequana Medical presented EASL Congress 2026 data showing hepatic recompensation signals after alfapump placement in decompensated cirrhosis patients, supporting potential disease-modification claims.

- February 2026: Sequana Medical reported commercial alfapump implantations at five leading US centers since the Q4 2025 launch and advanced discussions with more than 20 additional institutions.

- February 2026: BioVie filed an S-1 registration for Option Therapeutics, a planned spinout for BIV201, to raise USD 25-30 million for a registrational Phase 3 trial in decompensated cirrhosis patients with ascites and acute kidney injury.

Global Ascites Market Report Scope

As per the scope of the report, ascites is the abnormal buildup of excessive fluid in the abdominal cavity. This accumulation happens within the peritoneal space, the lining that covers abdominal organs like the liver and intestines. It most commonly occurs due to severe liver disease (cirrhosis) or advanced cancer.

The ascites market is segmented by product, ascites type, route of administration, end user, distribution channel, and geography. By product, the market includes treatment type and diagnosis. By treatment type, the market is segmented into diuretics, paracentesis, albumin infusion, transjugular intrahepatic portosystemic shunt, liver transplantation, implantable ascites pump therapy, and palliative long-term abdominal drainage. By diagnosis, the market is segmented into physical examination, ultrasound, computed tomography, magnetic resonance imaging, diagnostic paracentesis, and laboratory testing. By ascites type, the market is segmented into refractory ascites, recurrent ascites, malignant ascites, chylous ascites, and other ascites types. By route of administration, the market is segmented into oral, parenteral, and device-based delivery. By end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, home care settings, and others. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Treatment Type | Diuretics |

| Paracentesis | |

| Albumin Infusion | |

| Transjugular Intrahepatic Portosystemic Shunt | |

| Liver Transplantation | |

| Implantable Ascites Pump Therapy | |

| Palliative Long-Term Abdominal Drainage | |

| Diagnosis | Physical Examination |

| Ultrasound | |

| Computed Tomography | |

| Magnetic Resonance Imaging | |

| Diagnostic Paracentesis | |

| Laboratory Testing |

| Refractory Ascites |

| Recurrent Ascites |

| Malignant Ascites |

| Chylous Ascites |

| Other Ascites Types |

| Oral |

| Parenteral |

| Device-Based Delivery |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Home Care Settings |

| Others |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Treatment Type | Diuretics |

| Paracentesis | ||

| Albumin Infusion | ||

| Transjugular Intrahepatic Portosystemic Shunt | ||

| Liver Transplantation | ||

| Implantable Ascites Pump Therapy | ||

| Palliative Long-Term Abdominal Drainage | ||

| Diagnosis | Physical Examination | |

| Ultrasound | ||

| Computed Tomography | ||

| Magnetic Resonance Imaging | ||

| Diagnostic Paracentesis | ||

| Laboratory Testing | ||

| By Ascites Type | Refractory Ascites | |

| Recurrent Ascites | ||

| Malignant Ascites | ||

| Chylous Ascites | ||

| Other Ascites Types | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Device-Based Delivery | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Home Care Settings | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the Ascites Market in 2026 and 2031?

The Ascites Market stands at USD 1.98 billion in 2026 and is forecast to reach USD 2.56 billion by 2031, growing at a 5.29% CAGR.

Which product group leads ascites care revenue today?

Treatment Type leads with 68.12% share in 2025 because diuretics, paracentesis, albumin infusion, and related interventions still account for most care activity.

Which part of care is growing fastest by product?

Diagnosis is growing fastest at a 5.93% CAGR through 2031 as imaging-guided workflows and more structured disease assessment become more common.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific is projected to grow at 8.56% CAGR because of its large liver disease burden, improving interventional capacity, and broader access expansion in countries such as China and India.

What is changing in device-based treatment for recurrent or refractory ascites?

Device-Based Delivery is forecast to grow at 7.35% CAGR, helped by the US approval and early commercial rollout of the alfapump, which offers an alternative to repeated therapeutic paracentesis.

Which care setting is expanding fastest outside hospitals?

Home Care Settings are expected to grow at 6.78% CAGR as evidence builds for more distributed follow-up and selected long-term drainage support, even though hospitals still hold the largest 52.34% share.

Page last updated on: