Anti-Cathepsin B Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 205.86 Million |

| Market Size (2031) | USD 241.11 Million |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

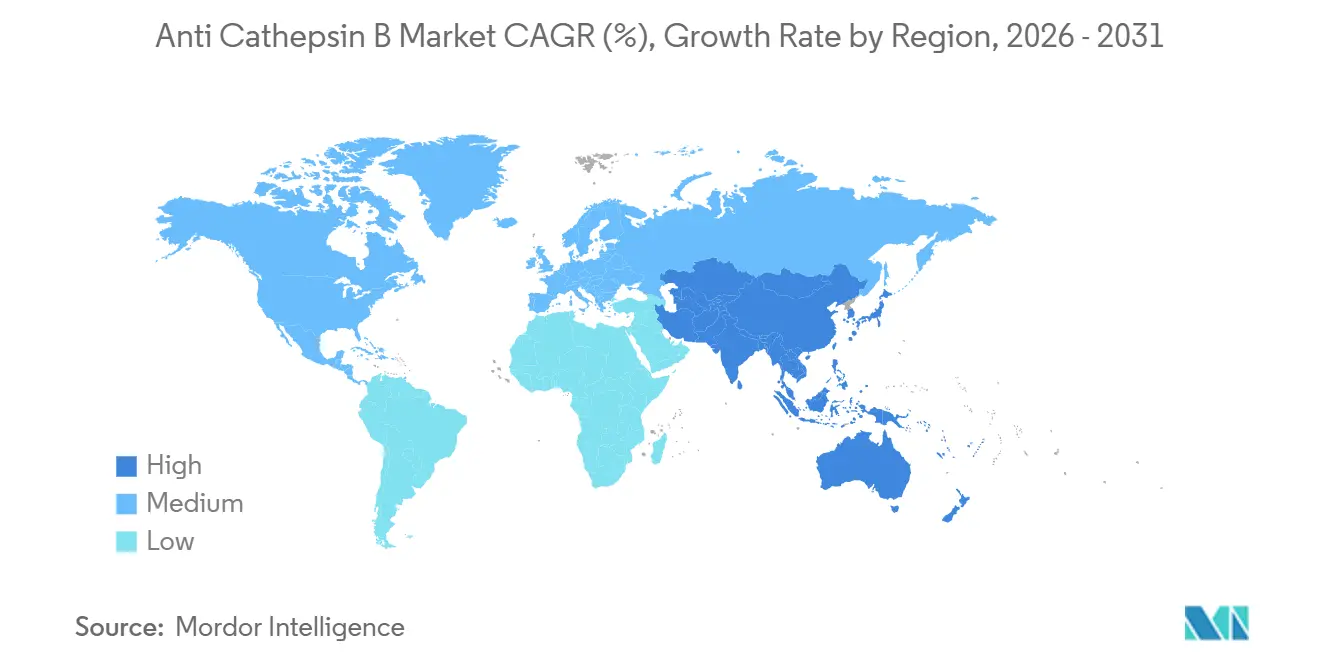

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

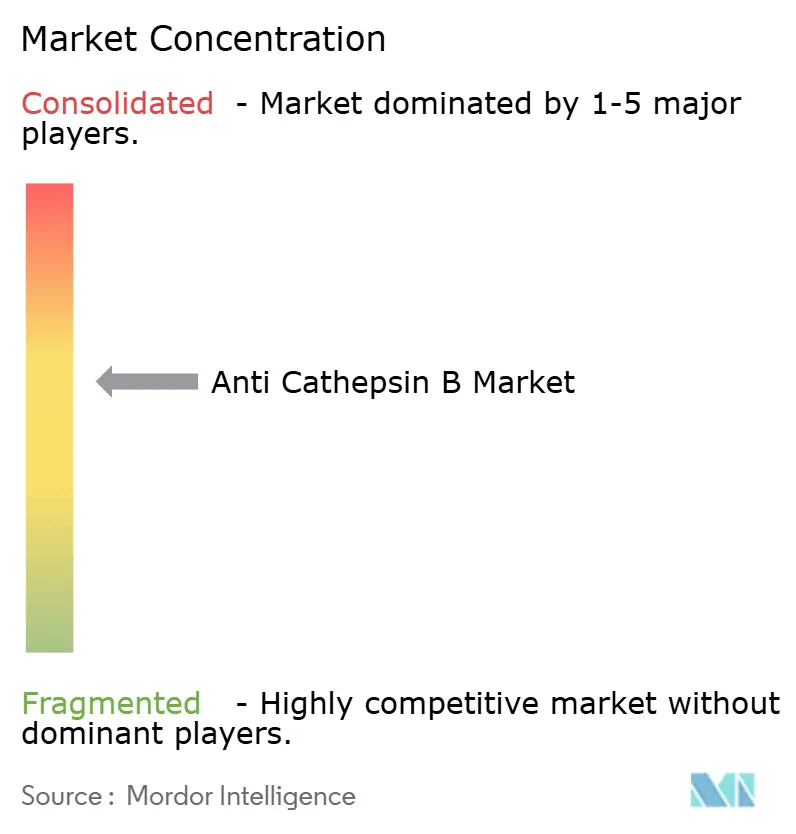

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Cathepsin B Market Analysis by Mordor Intelligence

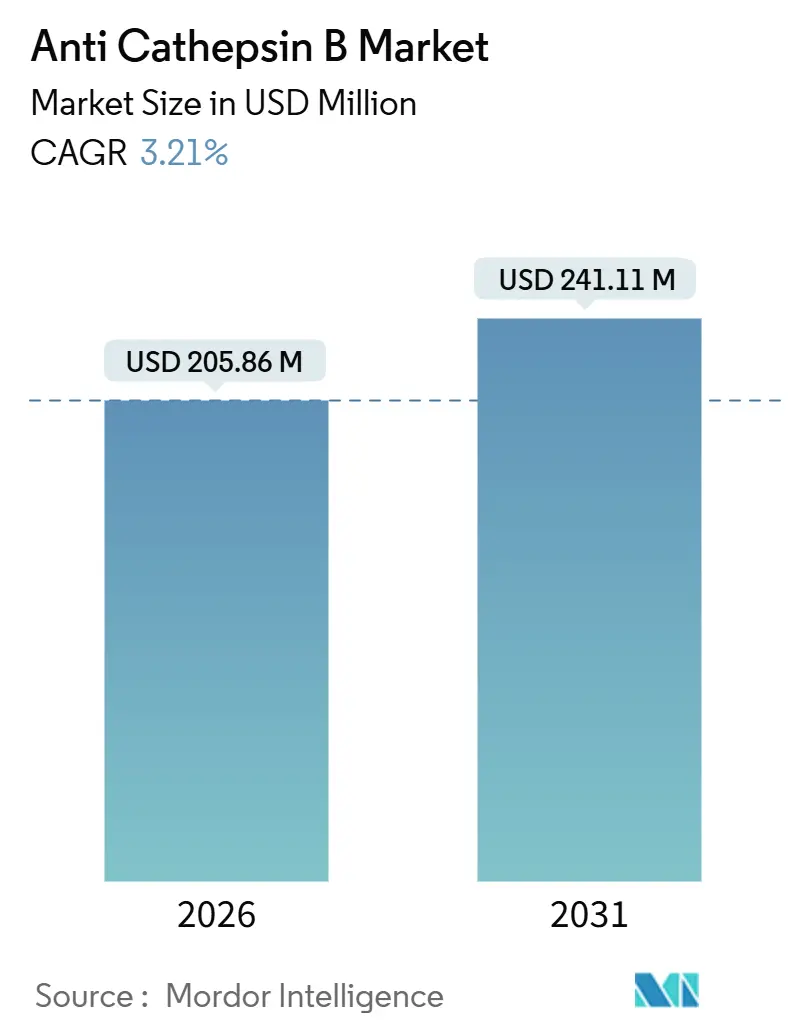

The Anti-Cathepsin B Market size is estimated at USD 205.86 million in 2026, and is expected to reach USD 241.11 million by 2031, at a CAGR of 3.21% during the forecast period (2026-2031).

This steady pace reflects the protease’s growing importance as a dual-purpose oncology biomarker and a lysosomal target in neurodegeneration programs. Increased pharmaceutical spending on antibody-drug conjugates (ADCs), the rapid scaling of reagent e-commerce, and deeper mechanistic insight into cathepsin-cleavable linkers are widening addressable demand, even as off-target effects across the 11-member cathepsin family and the limited clinical progress of small-molecule inhibitors restrain acceleration. Developers continue to favor premium recombinant enzymes for linker-cleavage validation, a trend reinforced by investor interest in ADC payload release studies. At the same time, digital procurement models shorten fulfillment cycles from weeks to days, compressing commodity pricing yet broadening global access to validated monoclonal antibodies. The net result is a measured but reliable expansion path for the Anti-Cathepsin B Market, underpinned by a diverse product mix that now spans antibodies, enzymes, fluorogenic substrates, and multiplex assay panels.

Key Report Takeaways

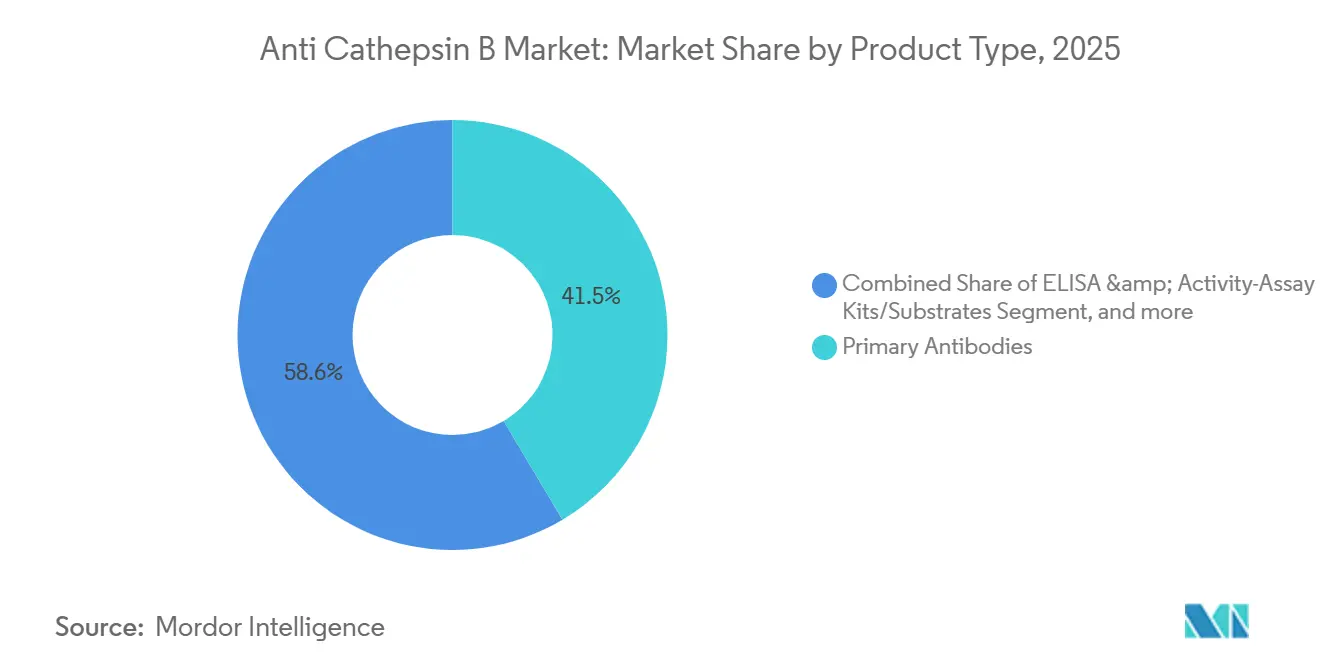

- By product type, primary antibodies led with 41.45% revenue share in 2025; recombinant proteins and enzymes are set to advance at a 4.56% CAGR through 2031.

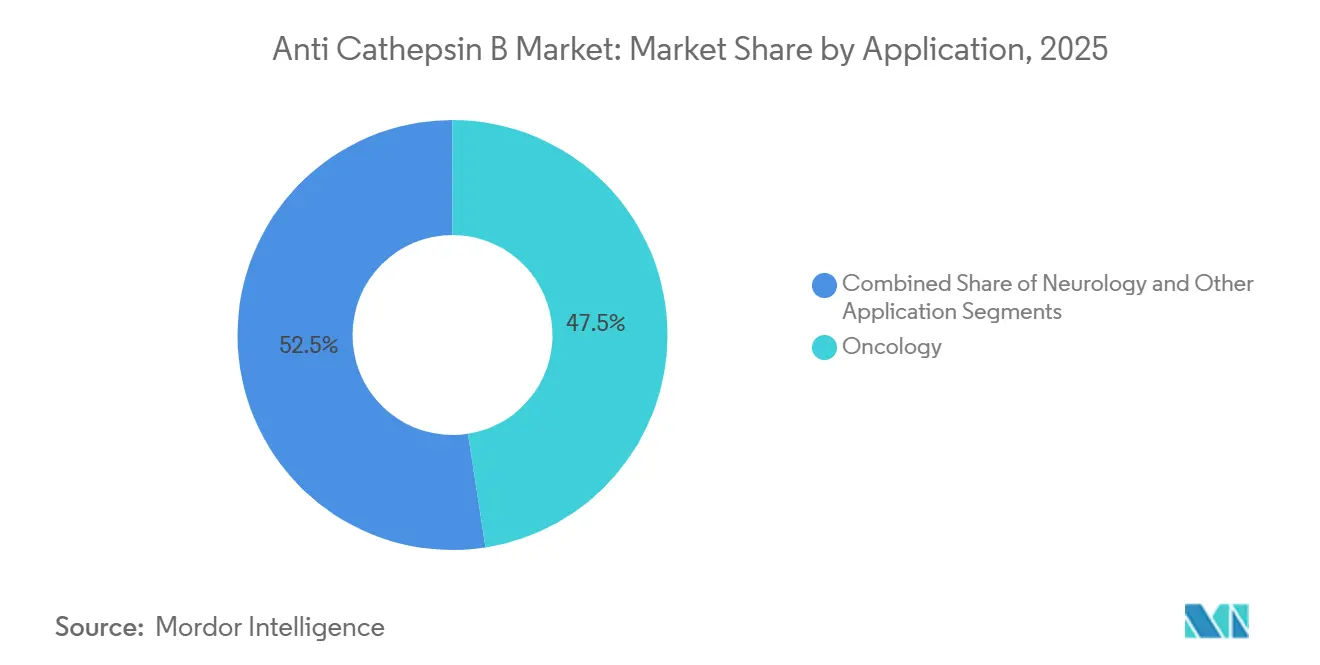

- By application, oncology captured 47.54% of 2025 revenue, and neurology is projected to grow at a 4.77% CAGR to 2031.

- By end user, pharmaceutical and biotechnology companies held 55.87% of demand in 2025, while academic and research institutes are expanding at a 5.76% CAGR through 2031.

- By geography, North America commanded 41.45% of 2025 revenue; Asia-Pacific is forecast to match the global 3.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anti-Cathepsin B Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Oncology Research Spending Targeting Protease Biomarkers | +0.9% | Global, especially North America and Europe | Medium term (2-4 years) |

| Expansion of Antibody and Reagent E-Commerce Platforms | +0.7% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Increasing Adoption of Cathepsin-Cleavable Linkers in Targeted Therapies | +0.8% | North America and Europe | Long term (≥ 4 years) |

| Growth of High-Content Screening and Cell-Based Protease Assays | +0.5% | Core regions across North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Neurodegeneration Pipeline Investments Leveraging Lysosomal Biomarkers | +0.6% | North America, Europe, early adoption in Japan | Long term (≥ 4 years) |

| Government Funding for Inflammation and Infectious-Disease Protease Research | +0.4% | Global, emphasis on NIH and EU programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Oncology Research Spending Targeting Protease Biomarkers

United States pharmaceutical oncology R&D reached USD 108 billion in 2024, and cathepsin B sits high on biomarker priority lists because its overexpression correlates with invasive phenotypes in hepatocellular carcinoma, triple-negative breast cancer, and glioblastoma. The enzyme degrades collagen IV and laminin, facilitating tumor cell migration, and its lysosomal-to-cytosolic translocation during apoptosis positions it as both a diagnostic marker and a therapeutic trigger. Cancer Research reported cathepsin B upregulation in 73% of inflammatory breast cancer biopsies, linking high expression to poor 5-year survival, which has fueled demand for validated monoclonal antibodies and activity-based probes. Laboratories are shifting from Western blot to multiplex immunofluorescence and spatial transcriptomics, creating pull-through demand for recombinant cathepsin B standards and fluorogenic substrates.

Increasing Adoption of Cathepsin-Cleavable Linkers in Targeted Therapies

Blockbuster ADCs such as trastuzumab deruxtecan rely on Val-Cit dipeptide linkers that are cleaved by cathepsin B within tumor lysosomes, thereby limiting systemic exposure. Nature Chemical Biology reported that a tetrapeptide GFLG linker achieved 40% higher payload release in HER2-positive xenograft models, demonstrating the commercial value of optimizing cleavage kinetics[1]Nature Chemical Biology, “Tetrapeptide Linkers Enhance ADC Payload Release,” nature.com. This advance stimulates demand for recombinant cathepsin B enzyme and fluorogenic substrates, as developers screen custom linker libraries supplied by contract organizations such as Creative Biolabs. Each preclinical iteration drives assays, ELISAs, and control antibody consumption, reinforcing the Anti-Cathepsin B Market’s laboratory-tool revenue base.

Growth of High-Content Screening and Cell-Based Protease Assays

High-content platforms that combine automated microscopy with image-analysis algorithms are displacing endpoint biochemistry in phenotypic discovery. SLAS Discovery showed that integrating the Magic Red substrate enabled the identification of 12 novel cathepsin B inhibitors from a 10,000-compound library[2]SAGE Publishing, “High-Content Screening Identifies Cathepsin B Inhibitors,” sagepub.com. Live-cell probes preserve native localization and kinetics, an advantage amplified by Revvity’s IVISense near-infrared agents for in vivo imaging. Each platform shift raises reagent consumption, underpinning consistent Anti-Cathepsin B market growth.

Neurodegeneration Pipeline Investments Leveraging Lysosomal Biomarkers

Acta Neuropathologica found that cathepsin B knockout mice displayed half the tau aggregation observed in controls, preserving cognition in the 3xTg-AD model[3]Springer, “Cathepsin B Knockout Mitigates Tauopathy,” springer.com. This breakthrough positions the protease upstream of tangle formation, prompting laboratories to secure antibodies for brain-tissue staining and recombinant enzyme for tau-cleavage assays. Parallel research implicates cathepsin B in lysosomal membrane permeabilization during Parkinson’s and Huntington’s disease. The resulting methodological breadth broadens the Anti-Cathepsin B Market beyond oncology into neurology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Off-Target Effects Due to Protease Redundancy Across the Cathepsin Family | -0.5% | Global | Medium term (2-4 years) |

| Limited Clinical Translation of Small-Molecule Cathepsin B Inhibitors | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Pricing Pressures from Commodity Antibody Suppliers | -0.3% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Data Variability from Cross-Laboratory Enzyme-Activity Assays | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Off-Target Effects Due to Protease Redundancy Across the Cathepsin Family

The overlapping substrate profiles of cathepsins B, L, and S complicate target validation. Trends in Pharmacological Sciences highlighted that CA-074, a standard cathepsin B inhibitor, suppresses cathepsin L at concentrations above 10 µM, prompting researchers to pair chemical inhibitors with genetic knockouts to confirm specificity. Cross-reactivity also plagues polyclonal antibodies, elevating validation costs and tempering demand for broad-spectrum reagents.

Limited Clinical Translation of Small-Molecule Cathepsin B Inhibitors

No cathepsin B-selective inhibitor has progressed beyond Phase II. Nature Reviews Drug Discovery traced failures to systemic toxicity arising from ubiquitous lysosomal expression and to suboptimal pharmacokinetics. The high-profile termination of odanacatib, a cathepsin K inhibitor, further eroded investor appetite for cysteine-protease programs. Consequently, the Anti-Cathepsin B Market remains tethered to research-tool revenue rather than therapeutic royalties, restraining upside potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Recombinant Enzymes Gain Share

Recombinant enzymes are expanding at a 4.56% CAGR, outpacing the overall Anti-Cathepsin B Market. Pharmaceutical validation of cathepsin-cleavable linkers demands endotoxin-free enzymes manufactured in mammalian systems, a preference underscored by a Bioconjugate Chemistry study showing a three-fold difference in cleavage kinetics between CHO-derived and bacterial enzymes (ACS.ORG). Primary antibodies held 41.45% of revenue in 2025, but price erosion from Chinese suppliers tempers expansion. ELISA and activity-kit demand sits in the middle, serving labs that prioritize lot-to-lot reproducibility without the flexibility of custom assay builds.

Adoption of recombinant proteins mirrors a broader life-science trend toward defined reagents accompanied by certificates of analysis. AAT Bioquest’s Magic Red substrate frequently ships with anti-cathepsin B antibodies for signal confirmation, creating a pull-through effect that raises aggregate spend per experiment. Other product types—small-molecule inhibitors, imaging probes, peptide libraries—remain niche, yet their mechanistic value sustains a premium pricing tier that cushions margins in a price-sensitive environment.

By Application: Neurology Accelerates

Oncology accounted for 47.54% of 2025 revenue, reflecting cathepsin B’s entrenched role in tumor invasion studies and ADC payload release. A Clinical Cancer Research report linked cathepsin B immunohistochemistry scores to response rates in melanoma patients receiving immune checkpoint inhibitors, extending the relevance to tumor-immune interactions. Neurology is the fastest-growing application, forecast to expand at 4.77% CAGR as lysosomal biomarkers gain traction in Alzheimer’s and Parkinson’s pipelines. Science Translational Medicine demonstrated that cathepsin B inhibition cut amyloid-β plaque burden by 30% in the 5xFAD model, catalyzing procurement of cerebrospinal fluid ELISAs and recombinant enzyme.

Inflammation, cardiovascular disease, and infectious disease applications occupy smaller slices of the anti-Cathepsin B market size, but NLRP3-inflammasome research continues to attract grant funding. Each emerging indication expands reagent diversity, reinforcing steady market growth despite oncology’s relative maturity.

By End User: Pharma Leads, Academia Grows Faster

Pharmaceutical and biotechnology firms captured 55.87% of demand in 2025, demonstrating a willingness to pay 2–3 times more for lot-consistent monoclonal antibodies and GLP-grade recombinant enzymes. A Nature Biotechnology survey found that 68% of pharma labs transitioned to monoclonal antibodies for target validation to mitigate reproducibility issues with polyclonals. Academic and research institutes are growing at 5.76% CAGR, buoyed by NIH dementia grants and EU Horizon funding. Price-sensitive universities often choose polyclonal antibodies and off-the-shelf ELISA kits, yet rising expectations for data robustness are nudging institutions toward higher-specification reagents.

Contract research organizations and diagnostic developers round out the end-user segments. Their bulk purchases of recombinant enzyme and customized assay services create recurring revenue streams, offsetting cyclical spend in academic calendars and stabilizing the Anti-Cathepsin B Market share distribution across customer classes.

Geography Analysis

North America retained 41.45% of 2025 revenue, anchored by USD 108 billion in U.S. pharmaceutical R&D and a 60% global share of ADC clinical trials. Same-day delivery in metropolitan hubs accelerates laboratory workflows, while Canadian institutes leverage federal funding to probe neurodegenerative pathways. Europe ranks second, propelled by Germany’s EUR 1.2 billion life-science budget and the European Medicines Agency’s focus on biomarker-guided oncology. The United Kingdom’s academic clusters and France’s lysosomal-storage research further enrich demand, although Italy and Spain grow more slowly under fiscal constraints.

Asia-Pacific is forecast to match the 3.21% global CAGR, as China’s venture-backed biotech sector raises USD 15 billion in 2024 and India’s contract research organizations secure ISO 9001 accreditation. Japan’s Ministry of Health earmarked JPY 50 billion for dementia research, steering reagent orders toward cathepsin-oriented lysosomal studies. South Korea’s biosimilar producers and Australia’s cancer-biology institutes provide additional demand pockets. Middle East & Africa and South America collectively contribute less than 15% of market revenue, hampered by weaker R&D infrastructure and extended supply lead times, yet e-commerce penetration is gradually easing access barriers.

Competitive Landscape

The Anti-Cathepsin B Market exhibits moderate fragmentation: the top five suppliers—Thermo Fisher Scientific, Abcam, Bio-Techne, Merck KGaA, and Cell Signaling Technology—command roughly 55% combined share. Thermo Fisher bundles antibodies with ancillary reagents into workflow kits, simplifying procurement for time-pressed scientists. Abcam’s Knockout Validated program addresses specificity concerns by proving signal loss in CRISPR-edited cell lines. Bio-Techne’s portfolio, assembled through Novus, R&D Systems, and Tocris, spans antibodies, recombinant proteins, and inhibitors, offering one-stop procurement.

White-space opportunities include intraoperative imaging probes such as Revvity’s IVISense, which currently lacks direct competition, and 1536-well-compatible activity assays enabling ultra-high-throughput screens. Chinese manufacturers, led by Sino Biological and Cusabio, discount polyclonal antibodies by up to 60%, appealing to budget-constrained academics. Creative Biolabs’ 2025 patent on a self-immolative cathepsin-cleavable linker illustrates the adjacent intellectual property that drives demand for premium enzyme lots. Vertical integration at Merck KGaA, through MilliporeSigma and Sigma-Aldrich, allows cross-selling of cathepsin B antibodies alongside chromatography resins and cell-culture media, leveraging entrenched customer relationships.

Anti-Cathepsin B Industry Leaders

Thermo Fisher Scientific

Merck KGaA

Abcam

Bio-Techne

Santa Cruz Biotechnolog

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: A study published in Aging Cell revealed that inhibiting Cathepsin B in mice can boost ovarian (oocyte) reserves by preventing the degradation of IGF1R, thereby promoting mitophagy and mitochondrial health. The research demonstrated that Cathepsin B inhibition increases IGF1R levels, which activates AKT–mTOR signaling and stimulates mitochondrial biogenesis.

- April 2025: Scientists at Konkuk University developed a novel peptide-based nano-sized Cathepsin B inhibitor (an RR–BA conjugate) that self-assembles into nanoparticles, showing potent Cathepsin B inhibition and anticancer effects against colorectal cancer in vitro and in mice, with minimal toxicity.

Global Anti-Cathepsin B Market Report Scope

As per the scope of the report, anti-cathepsin B refers to substances or antibodies that inhibit or block the activity of Cathepsin B, a lysosomal cysteine protease involved in protein degradation. It is often used in research to examine its role in diseases such as cancer, neurodegeneration, and inflammation. These inhibitors can help regulate abnormal protease activity and potentially serve as therapeutic agents.

The Anti-Cathepsin B Market is Segmented by Product Type (Primary Antibodies, ELISA & Activity-Assay Kits/Substrates, Recombinant Proteins & Enzymes, and Other Product Types), Application (Oncology, Neurology, and Other Applications), End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Primary Antibodies |

| ELISA & Activity-Assay Kits/Substrates |

| Recombinant Proteins & Enzymes |

| Other Product Types |

| Oncology |

| Neurology |

| Other Applications |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Primary Antibodies | |

| ELISA & Activity-Assay Kits/Substrates | ||

| Recombinant Proteins & Enzymes | ||

| Other Product Types | ||

| By Application | Oncology | |

| Neurology | ||

| Other Applications | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the Anti-Cathepsin B Market in 2026 and what growth is expected?

The Anti-Cathepsin B Market size reached USD 205.86 million in 2026 and is projected to rise to USD 241.11 million by 2031 at a 3.21% CAGR.

Which product category is expanding fastest within the market?

Recombinant proteins and enzymes are the fastest-growing category, advancing at a 4.56% CAGR as drug developers prioritize purified cathepsin B for linker-cleavage validation.

Which application area currently drives the most revenue?

Oncology leads with 47.54% of 2025 revenue, reflecting extensive use of cathepsin B in tumor-biology and ADC studies.

What region holds the largest share of global revenue?

North America commands 41.45% of global revenue, supported by substantial pharmaceutical R&D investment and a high concentration of ADC clinical trials.

Why have cathepsin B inhibitors struggled to progress clinically?

Overlapping substrate specificities among cathepsins and systemic toxicity risks have limited selectivity and safety profiles, preventing candidates from advancing beyond Phase II trials.

How is e-commerce influencing reagent procurement?

Digital storefronts with real-time inventory and validation data allow researchers to compare products instantly, shortening purchasing cycles and driving global access to premium reagents.

Page last updated on: