Ambulatory Blood Pressure Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

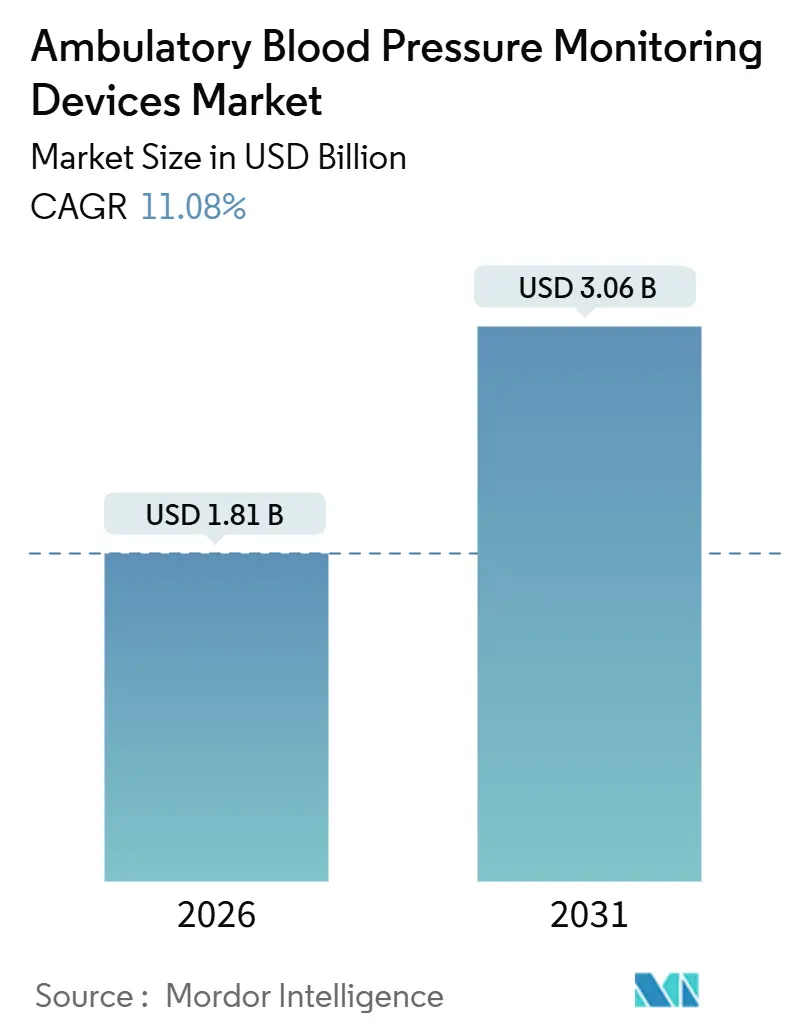

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

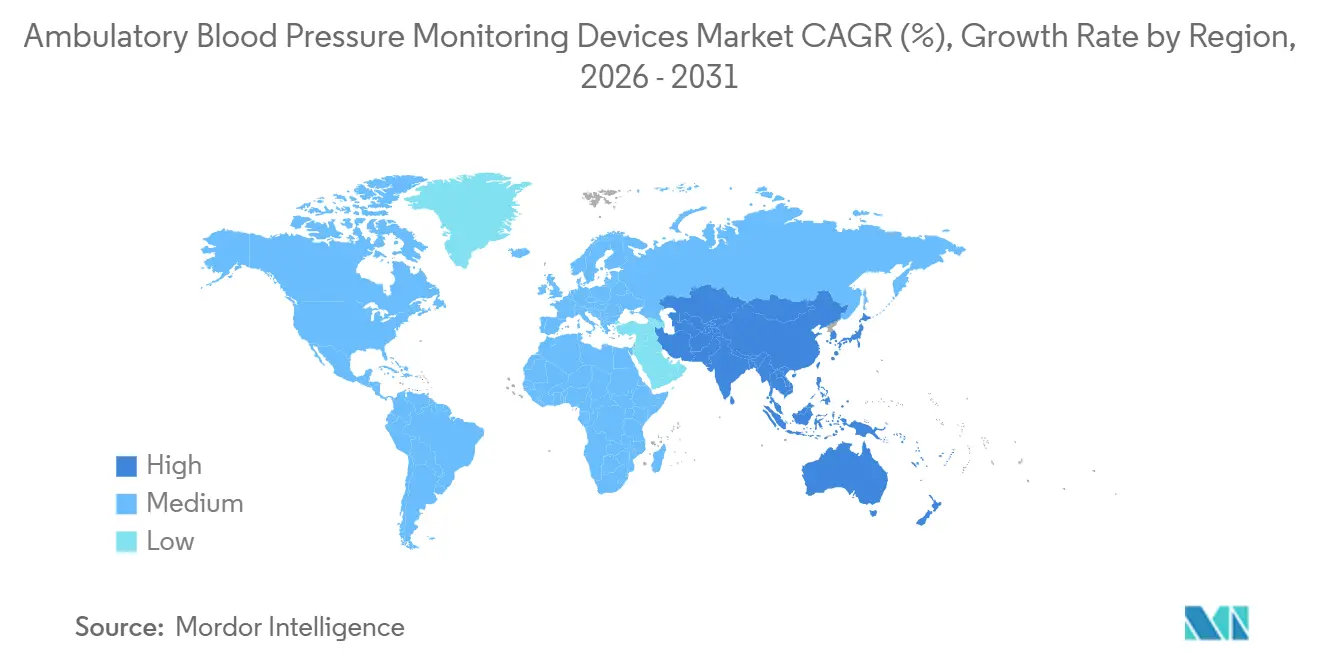

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

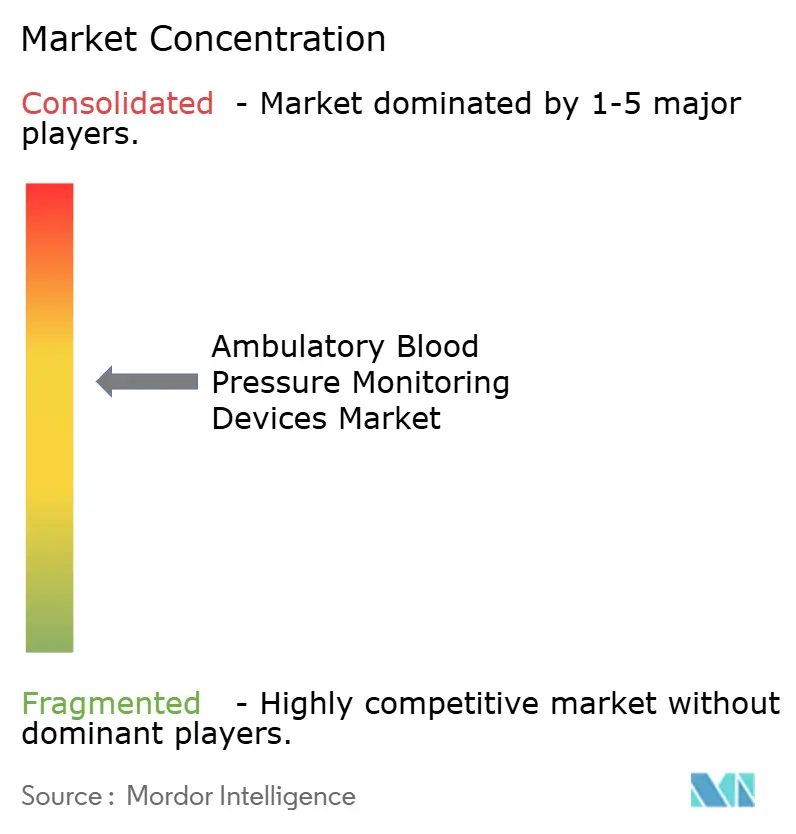

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambulatory Blood Pressure Monitoring Devices Market Analysis by Mordor Intelligence

The Ambulatory Blood Pressure Monitoring Devices Market size is estimated at USD 1.81 billion in 2026, and is expected to reach USD 3.06 billion by 2031, at a CAGR of 11.08% during the forecast period (2026-2031).

Growth is underpinned by reimbursement schemes that now reward out-of-office readings, AI-driven cuffless algorithms that ease patient compliance, and a decisive shift toward near-shore manufacturing that reduces tariff exposure. Wider hypertension prevalence, expanding telehealth infrastructure, and stronger validation standards for diverse cohorts further raise purchasing urgency across provider settings. Competitive strategies center on real-time data integration, pediatric-ready designs, and software subscriptions that supplement one-time hardware sales. Taken together, these dynamics position the ambulatory blood pressure monitoring devices market for sustained double-digit expansion.

Key Report Takeaways

- By product type, arm devices held 72.55% of 2025 ambulatory blood pressure monitoring devices market share; wrist units are poised to grow at a 12.25% CAGR to 2031.

- By measurement technology, oscillometric platforms commanded 62.53% share of the ambulatory blood pressure monitoring devices market in 2025, while hybrid volume-clamp and PPG systems are forecast to grow at a 13.85% CAGR through 2031.

- By connectivity, Wi-Fi and cloud-integrated models are projected to expand at a 15.55% CAGR, outpacing the 53.23% revenue growth of standalone counterparts in 2025.

- By end user, ambulatory surgical centers recorded the fastest growth trajectory, with a 13.51% CAGR to 2031, as cardiovascular procedures migrate to outpatient settings.

- By geography, North America maintained 43.13% market share of ambulatory blood pressure monitoring devices in 2025, but Asia-Pacific is expected to record the highest regional CAGR of 14.81% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ambulatory Blood Pressure Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hypertension Prevalence Globally | +2.3% | Global, highest in APAC & Sub-Saharan Africa | Long term (≥ 4 years) |

| Aging Population Increasing Cardiovascular Risk | +1.8% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Adoption of Telehealth & Remote Patient Monitoring | +2.5% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Payer Guideline Shifts Rewarding Out-of-Office BP Measurement | +1.9% | United States, Germany, United Kingdom, Australia | Short term (≤ 2 years) |

| Near-Shoring of ABPM Manufacturing Amid Tariff Risks | +0.7% | North America, European Union | Medium term (2-4 years) |

| AI-Enabled Cuffless Algorithms Boosting Adherence | +1.9% | Global, early adoption in United States, China, Israel | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Hypertension Prevalence Globally

Eight in ten adults with hypertension in low- and middle-income economies remain undiagnosed or undertreated, and ministries of health in India, Indonesia, and Brazil now pilot community ABPM campaigns that surface masked or white-coat hypertension, redirecting procurement toward portable units suited for non-clinical environments[1]World Health Organization, “Hypertension,” WHO Fact Sheets, who.int . China’s tier-2 and tier-3 hospitals must now maintain at least one device per 50 cardiology beds, adding about 12,000 units annually and broadening the pipeline for ambulatory blood pressure monitoring devices. Suppliers respond with robust batteries and simplified interfaces that cut calibration needs, acknowledging field-use constraints where biomedical engineers are scarce.

Aging Population Increasing Cardiovascular Risk

By 2030, the entire U.S. baby-boomer cohort will surpass 65 years, lifting Medicare-eligible lives to 73 million and concentrating hypertension prevalence above 60%. Nocturnal hypertension detection, which is unreachable with clinic sphygmomanometers, has become essential, especially after Japan and Germany added universal ABPM reimbursement for geriatric patients. Device utilization jumped 40% across Japanese prefectures over the past half year, signaling enduring upside for the ambulatory blood pressure monitoring devices market.

Adoption of Telehealth & Remote Patient Monitoring

Physicians can earn USD 50-65 per month in RPM fees when at least 16 days of physiologic data are transmitted, prompting the broad deployment of Bluetooth-enabled cuffs that automatically upload measurements to EHRs. Omron disclosed that connectivity subscriptions account for 38% of its U.S. ABPM sales, while IEEE is preparing a P11073 data standard that should reduce integration friction in multi-vendor fleets. Interoperability gaps persist, but the economic pull of RPM remuneration keeps the demand for ambulatory blood pressure monitoring devices elevated.

Payer Guideline Shifts Rewarding Out-of-Office BP Measurement

The American College of Cardiology upgraded ABPM to a Class I recommendation for confirming diagnosis, obligating United States insurers to cover the test as a preventive service[2]American Heart Association, “Heart Disease and Stroke Statistics – 2024 Update,” heart.org . NICE has a similar mandate, and Australia now reimburses up to 80% of device rental costs for resistant hypertension cases, thereby collectively multiplying first-time purchases in primary care. Such guideline momentum helps migrate the ambulatory blood pressure monitoring devices market from specialist domains into frontline clinics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost & Limited Reimbursement in LMICs | -1.2% | Sub-Saharan Africa, South Asia, Latin America (ex-Brazil) | Long term (≥ 4 years) |

| Patient Discomfort & Compliance Issues with 24-Hour Wear | -0.9% | Global, most acute in elderly & pediatric cohorts | Medium term (2-4 years) |

| Data-Privacy Regulations Hindering Cloud ABPM Roll-Outs | -0.6% | EU (GDPR), California (CCPA), China (PIPL) | Short term (≤ 2 years) |

| Validation Gaps for Diverse Patient Cohorts | -0.8% | United States, EU, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost & Limited Reimbursement in LMICs

Unit prices of USD 300-800 equal 40-60% of annual per-capita spend in Nigeria, Bangladesh, and Guatemala, placing ownership beyond public budgets[3]World Bank, “Health Expenditure Per Capita – Low and Middle Income Countries,” worldbank.org . In the absence of insurance support, doctors must self-ration tests, concentrating shipments in academic hospitals. Refurbished programs and tiered pricing exist but deliver thin margins, slowing scale across the ambulatory blood pressure monitoring devices market in resource-constrained geographies.

Patient Discomfort & Compliance Issues with 24-Hour Wear

Arm pain, sleep interruption, and social discomfort led 22% of 1,200 monitored patients to remove devices prematurely in a 2024 study, forcing repeat testing and eroding clinician confidence. Wrist ergonomics help, yet positional accuracy risks persist. Cuffless approaches promise relief, but until validation parity arrives, non-completion will curb data quality, holding back the ambulatory blood pressure monitoring devices market in home care.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product type: Miniaturization Drives Wrist Adoption

Arm models dominated the 2025 landscape, yet wrist units are advancing at a 12.25% CAGR as users favor sub-100-gram designs that can be hidden under clothing. Hospitals still rely on arm cuffs because existing protocols and accessories match that form, sustaining a 72.55% 2025 ambulatory blood pressure monitoring devices market share for the category. Wrist devices shine in outpatient and home scenarios. Omron’s clinically validated HEM-6410T crystallized this trend, though maintaining heart-level positioning remains vital. Firms add inertial sensors that discard off-axis readings, but these components add USD 40-60 to costs, marginally slowing broad adoption.

The convenience of wrist devices accelerates uptake in retail pharmacies and employer wellness programs, improving adherence among active adults who value discretion. Nevertheless, marginal underestimation of ambulatory systolic pressure, averaging 4.2 mmHg when patients walk, complicates medication titration decisions. Many cardiologists thus bifurcate workflows, reserving arm units for high-risk cases and deploying wrist units for screening. As positional-error algorithms mature, wrist form factors could capture a larger share of the ambulatory blood pressure monitoring market, especially where home readings dominate clinical management. Manufacturers investing in pediatric cuffs and slender strap designs may find additional white-space demand. Overall, form-factor evolution reflects the industry’s push to harmonize comfort and accuracy, a prerequisite for mass home deployment over the forecast horizon.

By Measurement Technology: Oscillometric Dominance Faces Hybrid Challenge

Oscillometric devices delivered 62.53% 2025 ambulatory blood pressure monitoring devices market share, securing entrenched positions in hospitals and clinics. Volume-clamp and PPG hybrids, however, promise beat-to-beat data without periodic inflation and are tracking a 13.85% CAGR forward. Finapres’ NOVA finger system exemplifies the shift, serving anesthesia and ICU scenarios where minute-level trends matter. Hybrid systems excel in capturing rapid hemodynamic fluctuations, a trait that oscillometric cuffs cannot match.

Providers weigh the costs and staff retraining against hybrid benefits, frequently piloting the technology in procedural areas before a wholesale replacement. As hybrid accuracy studies accumulate, payer coverage will likely widen, encouraging scale. Auscultatory digital hybrids persist in pockets that still teach Korotkoff detection, yet their share erodes as younger clinicians adopt automated workflows. If cuffless PPG algorithms achieve ISO’s 5 mmHg threshold across skin tones and BMI ranges, they could leapfrog both oscillometric and volume-clamp systems in home settings. Regulatory agencies seek multi-year outcome data tying algorithm performance to cardiovascular events, a high bar that keeps oscillometric devices entrenched in medication-adjustment protocols. Consequently, the ambulatory blood pressure monitoring devices market will exhibit parallel pathways: cuff-based platforms in clinical care and emergent cuffless solutions in preventive and consumer channels.

By Connectivity: Cloud Integration Accelerates Despite Privacy Hurdles

Standalone architecture accounted for 53.23% of revenue in 2025, a residue of legacy fleets lacking network links. Yet Wi-Fi- and cellular-enabled systems are poised for a 15.55% CAGR as providers chase real-time alerts that cut stroke and emergency-department visits. Cloud dashboards grant cardiologists population-level insight, unlocking predictive analytics subscriptions that diversify revenue beyond hardware. Philips’ HealthSuite demonstrates the strength of this proposition, unifying ABPM, lab, and medication data into a single set of views tailored for chronic-care management.

Cybersecurity risks remain salient; fourteen ransomware incidents in 2024 spotlighted vulnerabilities, leading FDA to insist on multi-factor authentication for all new connected devices. Vendors respond with hardware encryption modules, adding USD 25-40 per unit, a premium many hospitals accept, given mounting penalties for data breaches. GDPR and PIPL require separate regional clouds, but the benefits of near-real-time triage outweigh the setup costs for large health systems. Small practices and cash-pay customers may still prefer Bluetooth-only devices that store readings on patient phones. Over time, enterprise demand is likely to shift shipments toward networked models, solidifying cloud connectivity as a default specification across the ambulatory blood pressure monitoring devices market.

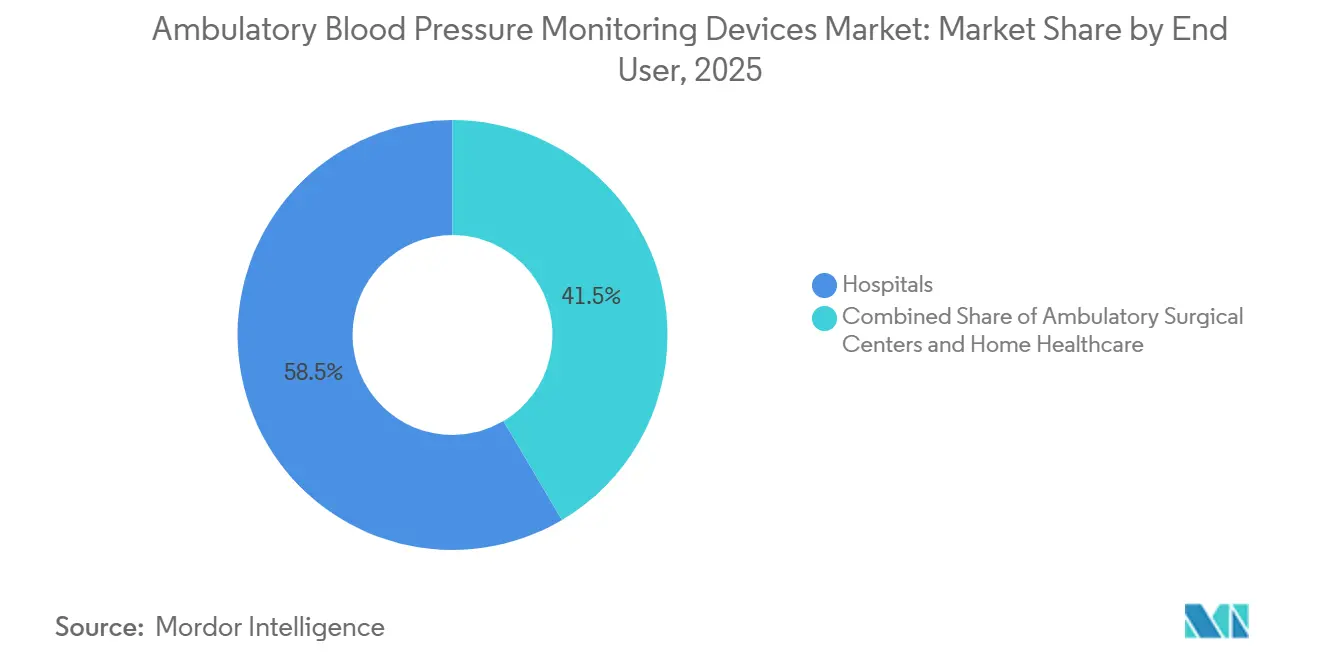

By End User: Ambulatory Surgical Centers Emerge as Growth Pocket

Hospitals remained the backbone purchaser at 58.53% in 2025, yet ambulatory surgical centers (ASCs) headline growth, mirroring cardiovascular procedure migration to outpatient suites. Post-procedure ABPM cut 30-day readmissions for hypertensive crises by 40% in ASC studies, validating its utility beyond diagnostics. Reimbursement also favors home assessment, prompting home health agencies to order cellular-embedded kits that elderly patients use with limited technical guidance.

SunTech’s Oscar 2 exemplifies fit-for-purpose design, integrating vibration guides for cuff placement and SIM-based upload that skips smartphones, trimming help-desk costs by 60%. The upfront price remains roughly USD 650, and CMS RPM payments offset capital outlays within six months, encouraging further deployments. Pediatric and prenatal clinics show nascent interest as validation studies proliferate, pointing toward future micro-segments. Collectively, expanding care settings diversify revenue pipelines and deepen the ambulatory blood pressure monitoring devices market penetration beyond cardiology departments.

Geography Analysis

North America accounted for 43.13% of global revenue in 2025, driven by Medicare RPM payments and Class I guideline endorsements. About 18 million U.S. adults receive a new hypertension diagnosis annually, and 12-15% undergo ABPM to rule out white-coat effects. Canada’s universal coverage broadened ABPM use by 35% in leading provinces after 2024 policy inclusion. Mexico lags because public insurers have yet to reimburse the test, confining demand to private cardiology practices in major urban centers. Short-term regulatory scrutiny on demographic validation may extend approval timelines but will ultimately fortify adoption across the region’s multiethnic patient base.

Asia-Pacific is the growth engine, set for 14.81% CAGR through 2031. China’s Healthy China mandate compels procurement across thousands of hospitals, while private insurers in tier-1 cities push connected models that feed tele-cardiology networks. India delineates a two-speed pattern: employer programs drive city uptake, whereas rural penetration waits on technician training and low-cost models. Japan, despite advanced aging, under-indexes because physicians prefer home BP monitors, which are reimbursed more generously, but national coverage for ABPM in elderly high-risk cohorts is increasing utilization. Australia’s Pharmaceutical Benefits Scheme added generous reimbursement in 2025, doubling unit demand in less than a year.

Europe, Middle East, and Africa present heterogeneous landscapes. Germany’s blanket reimbursement and the U.K.’s NHS leasing scheme propel volume, though device shortages linger in smaller jurisdictions. France and Italy remain concentrated in tertiary settings, while GCC states allocate transformation budgets in cardiovascular prevention that include ABPM. Sub-Saharan Africa sees sub-0.5 devices per 100,000 population owing to affordability and training shortfalls. South America’s adoption clusters in Brazil and Argentina where private insurers cover ABPM for diabetes and chronic kidney disease cohorts, reinforcing the ambulatory blood pressure monitoring devices market’s regional patchwork.

Competitive Landscape

The top five suppliers hold a noteworthy share, placing the market in a moderately concentrated band. Software emerges as the battleground; Omron’s partnership with Mayo Clinic on nocturnal dipping algorithms and Philips’ acquisition of a telehealth analytics firm highlight the pivot toward recurring revenue. Pediatric, cuffless, and ring-based concepts attract venture funding, though regulatory hurdles remain steep. ISO 81060-2 accuracy compliance stays the gating factor, and 2025 FDA draft guidance cements the need for broad demographic trials. Market leaders that blend validated accuracy with predictive analytics and responsive supply chains will preserve share despite price erosion at the low end.

Ambulatory Blood Pressure Monitoring Devices Industry Leaders

Baxter International, Inc.

GE Healthcare

Meditech Ltd.

Mindray Bio-Medical Electronics

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Biobeat Technologies closed a USD 50 million Series B to scale its patch-based, cuffless 24-hour ABPM platform.

- September 2025: Sky Labs unveiled CART BP, a ring-type monitor cleared by Korea’s MFDS for everyday BP tracking and clinical ABPM use.

Global Ambulatory Blood Pressure Monitoring Devices Market Report Scope

As per the report's scope, ambulatory blood pressure monitoring (ABPM) devices are portable medical devices used to measure blood pressure continuously over 24 hours while a patient goes about normal daily activities. They automatically record readings at preset intervals during daytime and nighttime, providing a more accurate assessment than single clinic measurements. ABPM devices help diagnose hypertension, white-coat hypertension, and masked hypertension, and support better treatment decisions.

Ambulatory blood pressure monitoring market segmentation includes product type, measurement technology, connectivity, end user, and geography. By product type, the market is segmented into arm ABPM devices and wrist ABPM devices. By measurement technology, the market is segmented into oscillometric, volume-clamp/PPG hybrid, and auscultatory digital hybrid. By connectivity, the market is segmented into standalone, Bluetooth-enabled, and Wi-Fi / cloud-integrated. By end user, the market is segmented into hospitals, ambulatory surgical centers, and home healthcare. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Arm ABPM Devices |

| Wrist ABPM Devices |

| Oscillometric |

| Volume-clamp/PPG Hybrid |

| Auscultatory Digital Hybrid |

| Standalone |

| Bluetooth-Enabled |

| Wi-Fi / Cloud-Integrated |

| Hospitals |

| Ambulatory Surgical Centers |

| Home Healthcare |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Arm ABPM Devices | |

| Wrist ABPM Devices | ||

| By Measurement Technology | Oscillometric | |

| Volume-clamp/PPG Hybrid | ||

| Auscultatory Digital Hybrid | ||

| By Connectivity | Standalone | |

| Bluetooth-Enabled | ||

| Wi-Fi / Cloud-Integrated | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home Healthcare | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the ambulatory blood pressure monitoring devices market by 2031?

The market is expected to reach USD 3.06 billion by 2031.

Which product form factor currently leads global revenue?

Arm-based devices commanded 72.55% of 2025 revenue.

Why are ambulatory surgical centers adopting ABPM rapidly?

ASCs use ABPM to verify post-procedure hemodynamic stability, reducing 30-day readmissions by 40%.

How quickly are Wi-Fi and cloud-integrated monitors expanding?

These connected models are projected to grow at 15.55% CAGR through 2031.

Which region is forecast to post the highest growth?

Asia-Pacific is set to expand at 14.81% CAGR, driven by mandatory screening programs and rising private insurance coverage.

What technological shift could disrupt cuff-based platforms?

AI-enabled cuffless algorithms validated across diverse cohorts may capture the home-health segment once they clear regulatory accuracy thresholds.

Page last updated on: