Alport Syndrome Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

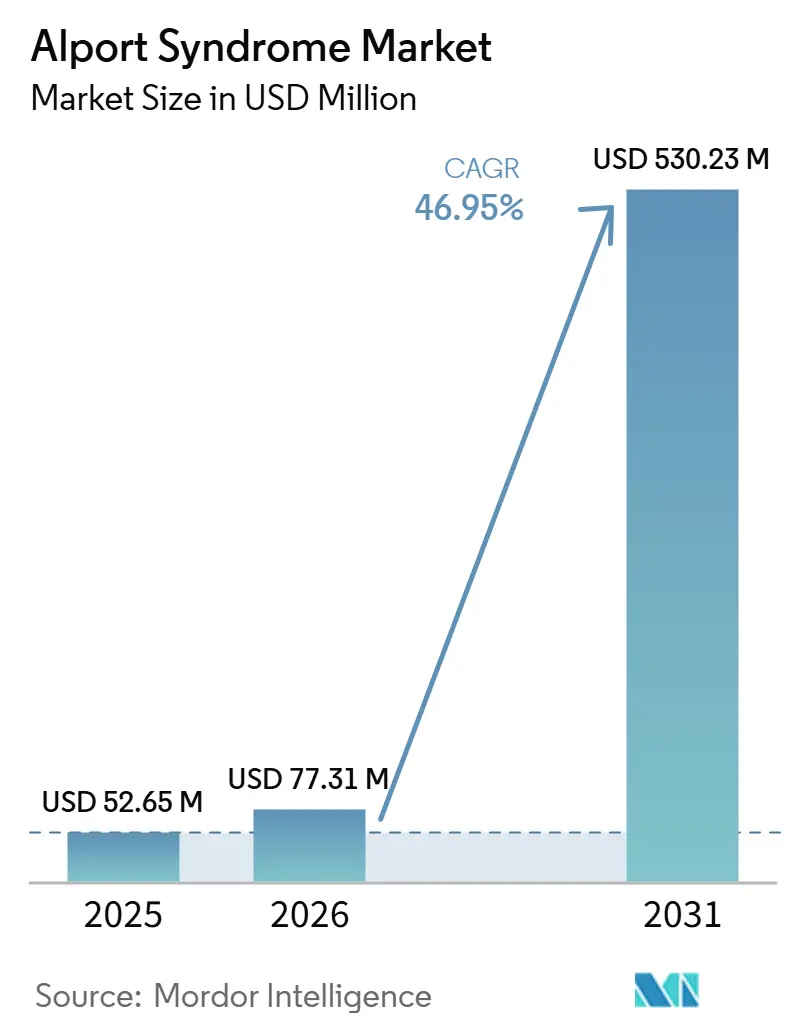

| Market Size (2026) | USD 77.31 Million |

| Market Size (2031) | USD 530.23 Million |

| Growth Rate (2026 - 2031) | 46.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alport Syndrome Market Analysis by Mordor Intelligence

The Alport Syndrome Market size is expected to increase from USD 52.65 million in 2025 to USD 77.31 million in 2026 and reach USD 530.23 million by 2031, growing at a CAGR of 46.95% over 2026-2031.

The Alport syndrome market still draws most current revenue from supportive pharmacotherapy, renal replacement services, and genetic diagnostics because no therapy has FDA or EMA approval specifically for this condition. The Alport syndrome market is now moving into a different phase because at least 4 investigational molecules were active in Phase 2 or Phase 2b development, with pivotal studies expected to begin before 2027.[1]Bayer AG, “Bayer Starts Phase IIa Study for Treatment of Patients with Alport Syndrome,” Bayer AG Press Release, bayer.com The first approved disease-modifying therapy in the Alport syndrome market would enter without a directly approved rival, and that position would be reinforced by orphan exclusivity frameworks in major jurisdictions. The Alport syndrome market is also widening through family cascade screening because variant-specific testing of at-risk relatives increases the diagnosed pool without changing true disease incidence. Trial execution remains complex because RAAS response differs by genotype, and weaker proteinuria reduction in truncating COL4A5 cases means the Alport syndrome market is moving toward more stratified treatment development.

Key Report Takeaways

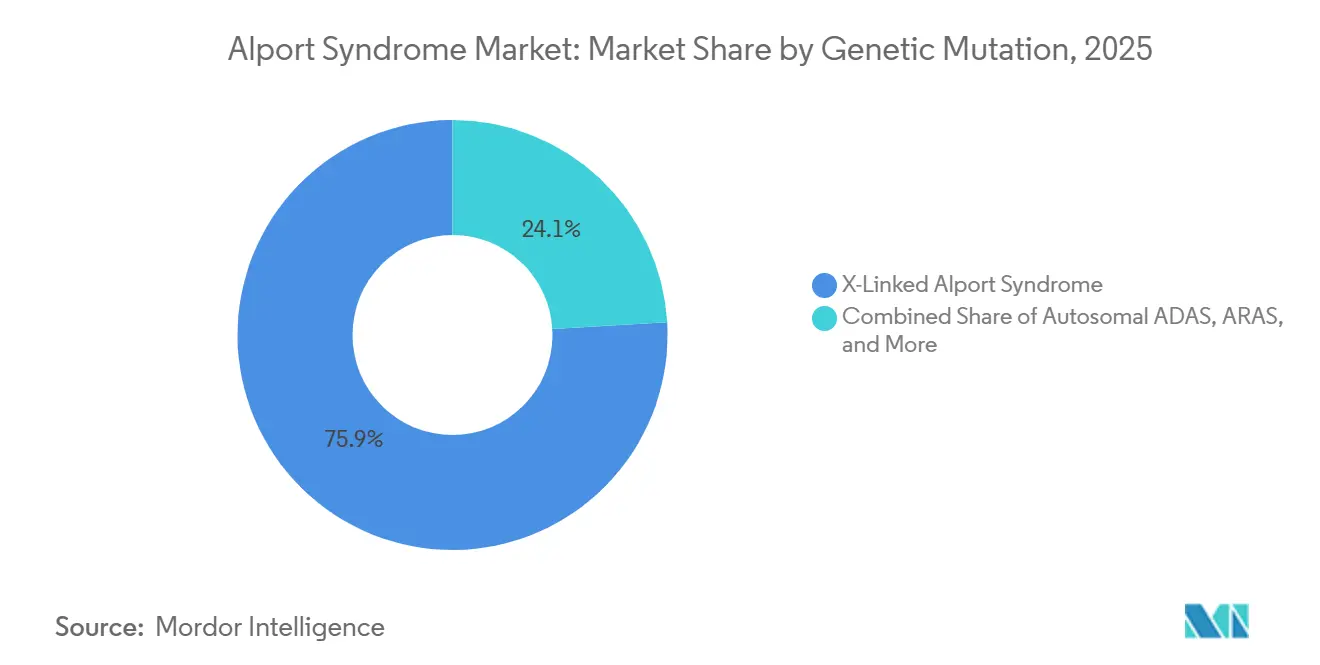

By genetic mutation, X-linked Alport syndrome held 75.94% market share in 2025, while autosomal dominant Alport syndrome is projected to grow at 52.87% CAGR through 2031.

By treatment type, supportive pharmacological therapy accounted for 65.11% share in 2025, while renal replacement therapy is forecast to expand at 55.34% CAGR through 2031.

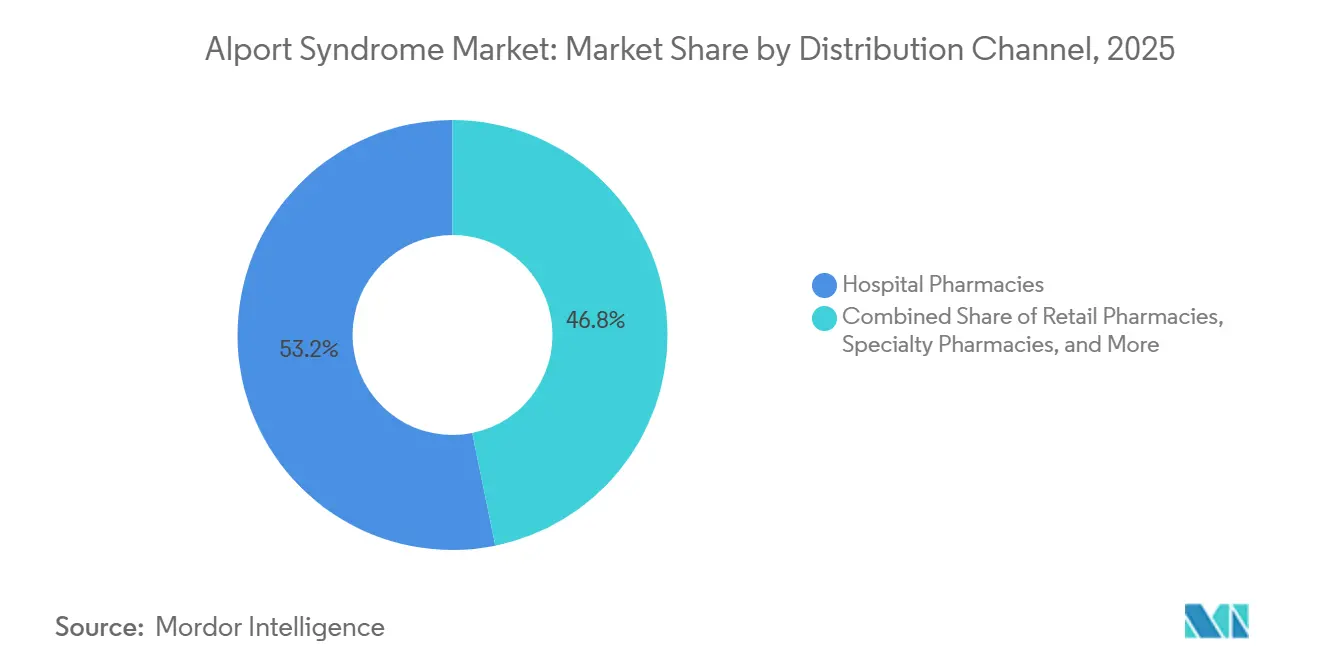

By distribution channel, hospital pharmacies represented 53.18% share in 2025, while specialty pharmacies are projected to grow at 53.17% CAGR through 2031.

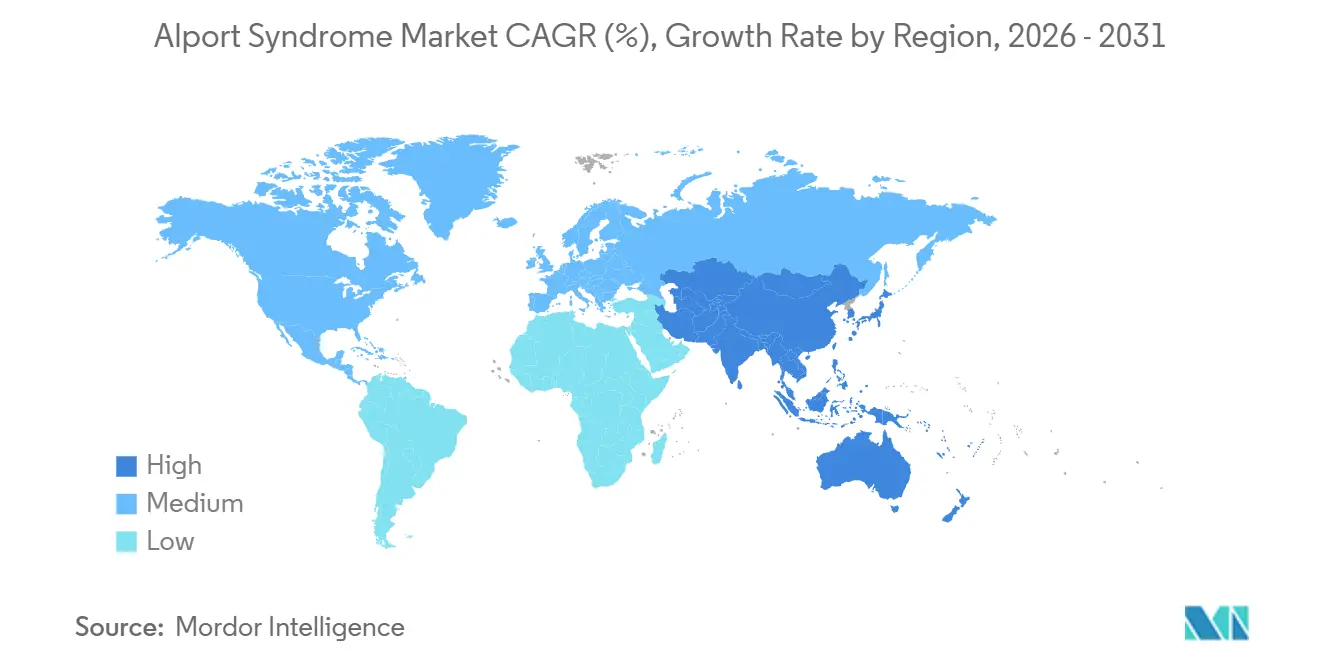

By geography, North America captured 43.98% share in 2025, while Asia-Pacific is set to advance at 57.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alport Syndrome Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded Genetic Testing Adoption In Suspected Hereditary Kidney Disease | +9.5% | Global | Medium term (2-4 years) |

| Broader Use Of Early RAAS Blockade To Delay Progression | +7.0% | Global | Short term (≤ 2 years) |

| Rising Trial Activity In Mutation-Defined Patient Subsets | +12.0% | North America and EU | Medium term (2-4 years) |

| Orphan-Drug Economics Support Faster Development For Rare Renal Therapies | +8.5% | North America and EU | Medium term (2-4 years) |

| NGS Panel Integration In Nephrology And Transplant Workups | +6.0% | Global, early gains in APAC | Medium term (2-4 years) |

| Expanded Family Cascade Screening Reveals Previously Hidden Prevalent Cases | +2.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Trial Activity in Mutation-Defined Patient Subsets

The Alport syndrome market has a more active clinical pipeline in 2026 than at any earlier point, and new programs are being designed around mutation-defined patient groups. Bayer initiated the ASSESS Phase IIa trial of BAY 3401016 in December 2025, and the program already carries FDA Fast Track and Orphan Drug Designations. Eloxx opened the EXACT Phase 2b study for enrollment in May 2026 for patients with confirmed nonsense mutations across COL4A3, COL4A4, and COL4A5. This biomarker-gated model allows sponsors to study more genetically uniform cohorts and improves the chance of showing clinically meaningful effect sizes in a small disease population. As a result, the Alport syndrome market now has parallel approval paths moving at the same time, which materially improves the chance of a first approved therapy.

Orphan-Drug Economics Support Faster Development for Rare Renal Therapies

Orphan-drug economics have become a practical development catalyst for the Alport syndrome market because they reduce cost and improve regulatory visibility. Calliditas Therapeutics received FDA Orphan Drug Designation for setanaxib, which lowered development friction and supported closer regulatory engagement around the program.[2]Calliditas Therapeutics, “Calliditas Therapeutics Reports Safety Data for Setanaxib in Patients with Alport Syndrome at the American Society of Nephrology Kidney Week,” PRNewswire, prnewswire.com Bayer's BAY 3401016 program also carries both Fast Track and Orphan Drug Designations, which support a faster review path once a submission is ready. The economics behind these frameworks are now strong enough to attract partner structures that spread discovery risk while preserving commercial upside, as shown by the Bayer and Evotec collaboration around BAY 3401016. That shift makes the Alport syndrome market look more investable than it did only a few years ago.

Expanded Genetic Testing Adoption in Suspected Hereditary Kidney Disease

The Alport syndrome market is expanding diagnostically because COL4A3, COL4A4, and COL4A5 testing is now part of the front-line workup for unexplained persistent hematuria, proteinuria, and focal segmental glomerulosclerosis of unknown origin. NGS panels with broad coding and adjacent intronic coverage now exceed 85% sensitivity for pathogenic variant detection, which makes test performance stronger than in many other inherited kidney diseases. The main gap now is referral behavior because pediatric patients with isolated microscopic hematuria and no family history are still often missed, even when testing is recommended. Closing that gap would directly expand the Alport syndrome market because undiagnosed patients also miss the only proven early intervention, RAAS blockade, that can delay kidney failure by a median of 18 years.

Broader Use of Early RAAS Blockade to Delay Progression

Early RAAS inhibition remains the foundational treatment driver in the Alport syndrome market because it is still the only intervention with randomized controlled evidence in this setting. The EARLY PRO-TECT Alport trial showed that ramipril at 6 mg/m² is safe and effective in children aged 2 and older with isolated microscopic hematuria or microalbuminuria, and that early treatment can delay kidney failure by a median of 18 years.[3]Roser Torra et al., “Diagnosis, Management and Treatment of the Alport Syndrome,” Nephrology Dialysis Transplantation, academic.oup.com The COMBINE-ALPORT trial completed primary endpoint data collection in November 2025 and tested dapagliflozin and spironolactone on top of maximum RAAS blockade, adding evidence for a possible add-on role in adults with persistent proteinuria. A clinically important complication is that RAAS response is genotype-stratified, and patients with truncating COL4A5 variants show less proteinuria reduction than missense carriers. That pattern supports earlier identification of patients who may need emerging agents rather than longer continuation of conventional care alone in the Alport syndrome market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Disease-Modifying Treatment Availability | -4.5% | Global | Short term (≤ 2 years) |

| Variable Phenotype Slows Diagnosis And Referral | -3.5% | Global, notably South America and MEA | Medium term (2-4 years) |

| Reimbursement Friction For High-Cost Rare Disease Testing And Therapy | -3.5% | North America and EU | Medium term (2-4 years) |

| AAV And Advanced Genetic Therapy Manufacturing Constraints | -2.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Disease-Modifying Treatment Availability

The absence of an approved disease-modifying therapy is still the largest structural cap on near-term revenue in the Alport syndrome market. ENYO Pharma reported Phase 2 Alpestria-1 data in January 2026 showing that vonafexor shifted eGFR trajectory from a historical mean decline of -6.4 mL/min/1.73 m²/yr to a mean gain of +4.8 mL/min/1.73 m²/yr over 24 weeks, and 73% of participants kept UACR below baseline 3 months after treatment stopped.[4]ENYO Pharma, “ENYO Pharma Announces Completion and Topline Data From Phase 2 Alpestria-1 Clinical Study in Alport Syndrome,” BusinessWire, businesswire.com Even with those results, Phase 3 was still planned for the second half of 2026, and regulatory approval was unlikely before 2028 at the earliest. That timing leaves patients dependent on generic supportive care and keeps healthcare spending tilted toward dialysis and transplantation. Until a disease-modifying option reaches the market, the Alport syndrome market will continue to carry a mismatch between disease burden and therapeutic access.

Reimbursement Friction for High-Cost Rare Disease Testing and Therapy

Reimbursement friction slows the Alport syndrome market because advanced diagnostics and future specialty therapies face a much tougher access path than standard supportive care. Future gene therapy and biologic candidates are expected to enter pricing bands already associated with strict payer review in other rare diseases, which means strong health-economic evidence will be required before broad uptake. In Europe, bodies such as G-BA, NICE, and HAS have historically asked for multi-year real-world evidence before granting full reimbursement for ultra-rare therapies, which can delay commercial access well after regulatory approval. This access lag means the Alport syndrome market can still grow scientifically while commercial uptake remains slower than clinical need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Genetic Mutation: X-Linked Subtype Anchors Revenue, Autosomal Dominant Emergence Widens the Addressable Population

X-linked Alport syndrome held 75.94% of Alport syndrome market share in 2025, reflecting both its higher clinical burden and its stronger diagnostic visibility in practice. Untreated males with COL4A5 mutations often reach kidney failure by age 40, which keeps XLAS at the center of nephrology follow-up, renal intervention, and disease monitoring costs. That concentration of severe disease burden gave XLAS a disproportionate role in present revenue allocation across the Alport syndrome market. Within XLAS, genotype-informed RAAS titration is starting to influence treatment intensity and the timing of transition for patients least likely to respond to standard care.

Autosomal dominant Alport syndrome is projected to grow at 52.87% CAGR from 2026 to 2031, making it the fastest-growing mutation segment. Population genomic datasets indicate that ADAS is far more common than older clinical case series suggested, which means many affected individuals were previously missed because presentation is milder and more variable. Cascade screening under the ERKNet framework is now bringing heterozygous relatives into the diagnosed pool, which expands the addressable base of the Alport syndrome market without any change in incidence. Autosomal recessive and digenic diseases remain smaller in count, but their severe or newly recognized presentations support more testing and more stable classification as multi-gene panels replace narrower workups.

the

By Treatment Type: Supportive Pharmacotherapy Dominates, Renal Replacement Growth Reflects Persistent Unmet Need

Supportive pharmacological therapy accounted for 65.11% of the Alport syndrome market size in 2025, which makes it the core revenue base across treatment categories. Ramipril remains the best-studied option, and the EARLY PRO-TECT evidence showed that early RAAS treatment can safely delay kidney failure by a median of 18 years in children. That evidence keeps supportive care as the standard entry point for most confirmed patients across the Alport syndrome market. Add-on use of SGLT2 inhibitors is also moving into practice for adults with persistent albuminuria despite maximum RAAS dosing, which broadens the commercial role of supportive therapy.

Renal replacement therapy is projected to grow at 55.34% CAGR through 2031, the fastest pace among treatment segments. This rise reflects a larger diagnosed population reaching end-stage disease before any approved disease-modifying therapy becomes commercially available. Emerging therapies such as vonafexor, setanaxib, BAY 3401016, and exaluren currently contribute limited revenue, but they carry most of the forward upside for the Alport syndrome market. Beyond this pipeline, early mRNA lipid nanoparticle work in XLAS mouse models suggests curative approaches could eventually move the Alport syndrome industry beyond supportive disease management, although that opportunity remains preclinical.

By Distribution Channel: Hospital Pharmacies Lead, Specialty Pharmacies Are Positioned For Launch Readiness

Hospital pharmacies accounted for 53.18% of the Alport syndrome market size in 2025, reflecting the specialist-led nature of prescribing and dispensing in rare renal disease. Tertiary centers and transplant programs still manage most patient monitoring, standard supportive therapy, and investigational drug access across the Alport syndrome market. That structure keeps hospital systems deeply embedded in the care pathway because they also provide the controlled storage and chain-of-custody support needed for clinical trial supply. The channel, therefore, benefits from both current care demand and the operating requirements of the active pipeline.

Specialty pharmacies are projected to grow at 53.17% CAGR from 2026 to 2031, making them the fastest-growing distribution channel. Their appeal comes from cold-chain logistics, prior authorization support, patient services, and coordination with manufacturer assistance programs that hospital pharmacies do not always provide at a commercial scale. Retail pharmacies continue to supply ACE inhibitor and ARB maintenance therapy, while online pharmacies are emerging as a convenience layer for repeat dispensing in underserved locations. As biologics and other premium therapies move closer to launch, distribution in the Alport syndrome market is likely to shift toward specialty pharmacy infrastructure.

Geography Analysis

North America held 43.98% of the Alport syndrome market share in 2025, making it the largest regional contributor. The region benefits from dense nephrology specialist networks, academic rare renal centers, and an orphan drug framework that lowers development risk for sponsors. The Alport Syndrome Foundation also maintained direct dialogue with the FDA in December 2025 on trial endpoints and patient-focused drug development priorities, which supports a clearer study design for the Alport syndrome market. The United States remains the main revenue center, while Canada adds support through provincial coverage that is increasingly including hereditary nephropathy panels in pediatric care.

Europe remained the second major regional base for the Alport syndrome market, supported by the ERKNet reference network across Germany, France, the Netherlands, Spain, and Italy. Those countries have already served as leading trial locations for vonafexor and setanaxib, which gives the region practical experience in rare renal study execution. Germany's DOUBLE PRO-TECT Alport Phase 3 trial is recruiting adolescents and young adults for dapagliflozin evaluation, and that independent evidence stream could influence future guideline updates and payer acceptance across the region.[5]“DOUBLE PRO-TECT Alport, Multicenter, Randomized, Placebo-Controlled Trial of Dapagliflozin in Adolescents and Young Adults With Alport Syndrome,” Orphanet, orpha.net Europe, therefore, combines strong clinical participation in the Alport syndrome market with tighter evidence expectations for reimbursement.

Asia-Pacific is projected to grow at 57.12% CAGR from 2026 to 2031, which makes it the fastest-expanding geography in the Alport syndrome market. Japan's mandatory urinalysis program has become an early detection pathway for pediatric cases, and the JP-ALPS registry gives the region a stronger molecular and clinical reference base. China is also expanding tertiary hospital testing capacity, and work from southwestern China identified novel COL4A3, COL4A4, and COL4A5 variants together with digenic inheritance patterns that point to a still incomplete diagnostic map.

Competitive Landscape

The Alport syndrome market has a split competitive structure, with a moderately fragmented diagnostics segment and a therapeutic segment that still has no approved leader. In diagnostics, Illumina provides core sequencing infrastructure, while Invitae, Natera, CENTOGENE, Eurofins, Quest Diagnostics, and other hereditary nephropathy panel providers compete at the service layer. Competition in this part of the Alport syndrome market depends less on sequencing access alone and more on panel breadth, turnaround time, payer contracting, and variant classification quality.

In therapeutics, Enyo Pharma, Calliditas Therapeutics, Bayer AG, and Eloxx Pharmaceuticals are advancing different mechanisms, which keeps the Alport syndrome market open rather than consolidated. Vonafexor targets FXR, setanaxib targets fibrosis-linked NOX pathways, BAY 3401016 targets Semaphorin 3A, and exaluren is being tested for nonsense mutation readthrough. This mechanistic spread suggests that future care may not center on one universal product, especially if response continues to vary by genotype and disease stage. Bayer strengthened its position when it moved BAY 3401016 into Phase IIa in December 2025 after the Bayer and Evotec collaboration produced the program. Eloxx also moved the field forward by opening the EXACT Phase 2b study in May 2026 for mutation-selected patients, which shows how targeted development is becoming a core pattern in the Alport syndrome market.

Strategic deal activity is also shaping the field, and Chugai Pharmaceutical's acquisition of Renalys in Q4 2025 extended sparsentan's path toward Japanese review for Alport syndrome while triggering a USD 10.2 million payment to Travere Therapeutics at closing. Illumina's continuing NovaSeq investment and population genomics partnerships support the upstream testing capacity that rare hereditary nephropathy screening depends on. White space remains in pediatric formulations, companion diagnostics, and gene therapy constructs, so the Alport syndrome market still offers room for new entrants even as several named developers have already moved ahead. That combination of active developers, open first-mover status, and unfinished diagnostic standardization keeps the Alport syndrome market dynamic but still far from concentrated.

Alport Syndrome Industry Leaders

Bayer AG

Calliditas Therapeutics AB

Chinook Therapeutics, Inc.

Novartis AG

Travere Therapeutics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eloxx Pharmaceuticals opened enrollment for the EXACT Phase 2b study (NCT07523581), a randomized, double-blind, placebo-controlled, delayed-start trial evaluating exaluren in patients with X-linked or autosomal recessive Alport syndrome carrying confirmed COL4A3/4/5 nonsense mutations, targeting 24 patients aged 12 and older across US and UK sites. This is the first mutation-class-specific nonsense readthrough program to reach Phase 2b in Alport syndrome, with primary completion expected June 2027 and full study completion December 2027.

- January 2026: ENYO Pharma released topline Phase 2 Alpestria-1 data, demonstrating that vonafexor reversed the eGFR trajectory from a historical mean decline of -6.4 mL/min/1.73 m²/yr to a mean gain of +4.8 mL/min/1.73 m²/yr over 24 weeks of treatment in 26 high-risk Alport syndrome patients on standard of care, with 73% of patients maintaining UACR reduction below baseline three months after stopping treatment. An End-of-Phase 2 FDA meeting is planned for Q2 2026 and Phase 3 initiation is targeted for the second half of 2026.

- December 2025: Bayer AG initiated the ASSESS Phase IIa trial (NCT07211685) of BAY 3401016, an investigational anti-Semaphorin 3A monoclonal antibody derived from the Bayer-Evotec multi-target renal research collaboration, in adult XLAS or ARAS patients with elevated albuminuria. The program carries FDA Fast Track and Orphan Drug Designations, establishing Bayer as the largest pharmaceutical company with an active disease-modifying Alport syndrome therapeutic program.

- November 2025: Calliditas Therapeutics, an Asahi Kasei company, presented Phase 2a safety and secondary efficacy results for setanaxib at the ASN Kidney Week High-Impact Clinical Trials session in Houston. The trial (NCT06274489) enrolled 20 patients aged 12-40 with genetically confirmed AS and met its primary safety endpoints, while setanaxib achieved a 15% mean UPCR reduction at 24 weeks and a 27% mean UPCR reduction 4 weeks post-dosing versus placebo, suggesting a sustained anti-fibrotic effect.

Global Alport Syndrome Market Report Scope

The Alport Syndrome Market encompasses therapeutics, diagnostic technologies, and supportive care solutions aimed at the diagnosis and management of Alport syndrome, a rare inherited kidney disorder caused by mutations in collagen type IV genes. The market is driven by increasing adoption of genetic testing, growing awareness of rare kidney diseases, advances in nephrology care, and the development of targeted disease-modifying therapies. Continued investment in orphan drug research, precision medicine, and early diagnosis is expected to improve patient outcomes and support market growth over the forecast period.

The Alport syndrome market is segmented by genetic mutation, treatment type, distribution channel, and geography. By genetic mutation, it is further divided into X-linked Alport syndrome, autosomal dominant Alport syndrome, autosomal recessive Alport syndrome, and digenic Alport syndrome. By treatment type, it is segmented into supportive pharmacological therapy, renal replacement therapy, and emerging disease-modifying therapies. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, specialty pharmacies, and online pharmacies. The geography segment is further divided into North America, Europe, Asia-Pacific, and the rest of the world. The report also covers the estimated market sizes and trends for 13 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| X-Linked Alport Syndrome |

| Autosomal Dominant Alport Syndrome |

| Autosomal Recessive Alport Syndrome |

| Digenic Alport Syndrome |

| Supportive Pharmacological Therapy |

| Renal Replacement Therapy |

| Emerging Disease-Modifying Therapies |

| Hospital Pharmacies |

| Retail Pharmacies |

| Specialty Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Genetic Mutation | X-Linked Alport Syndrome | |

| Autosomal Dominant Alport Syndrome | ||

| Autosomal Recessive Alport Syndrome | ||

| Digenic Alport Syndrome | ||

| By Treatment Type | Supportive Pharmacological Therapy | |

| Renal Replacement Therapy | ||

| Emerging Disease-Modifying Therapies | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Specialty Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the projected value of the Alport syndrome space by 2031?

The Alport syndrome market is forecast to reach USD 530.23 million by 2031, up from USD 52.65 million in 2025, with a 46.95% CAGR over 2026-2031.

Why is growth accelerating so quickly in this field?

Growth is being driven by active Phase 2 and Phase 2b pipelines, broader genetic testing, earlier diagnosis through cascade screening, and continued use of RAAS-based supportive treatment.

Which genetic subtype currently contributes the most revenue?

X-linked Alport syndrome led with 75.94% share in 2025 because its clinical severity and higher care intensity generate more specialist follow-up and treatment spending.

Which treatment category is growing the fastest through 2031?

Renal replacement therapy is projected to grow at 55.34% CAGR, reflecting continued progression to end-stage disease before approved disease-modifying therapies become available.

Which region is expected to expand the fastest?

Asia-Pacific is projected to grow at 57.12% CAGR through 2031, supported by Japan's screening pathway and China's expanding genetic testing capacity.

What is the biggest near-term commercial barrier for developers?

The main barrier is the lack of an approved disease-modifying therapy, followed by payer friction around advanced testing and future high-cost rare disease treatments.

Page last updated on: