Africa Roaming Tariff Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

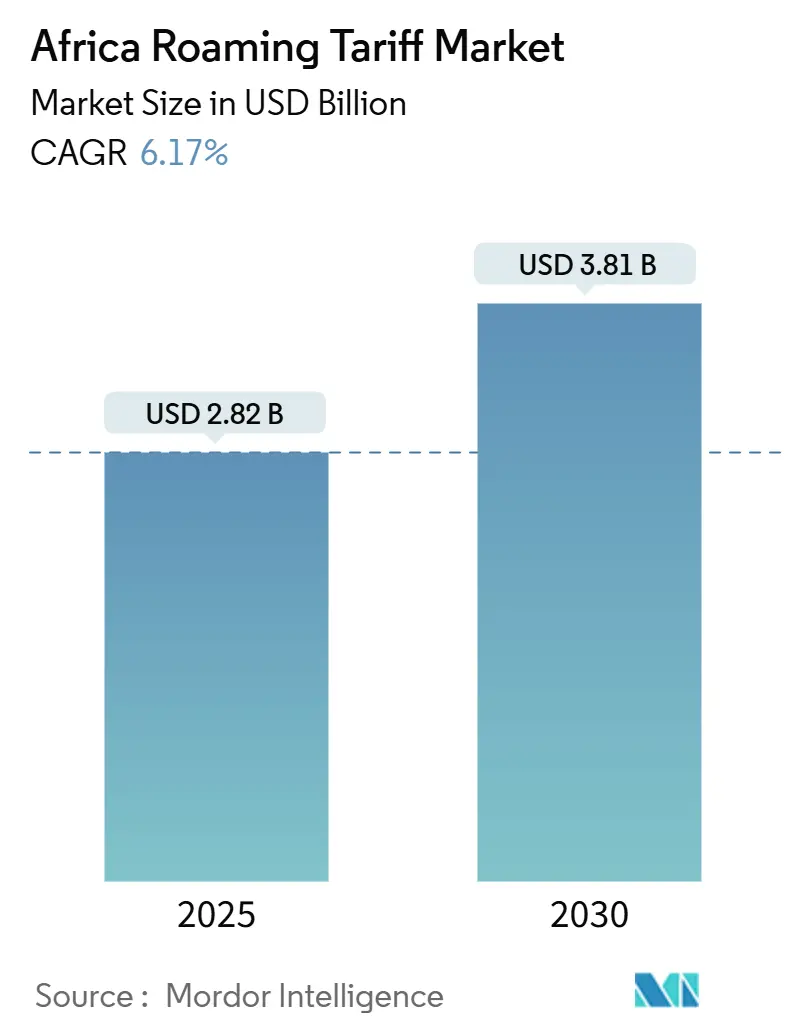

| Market Size (2025) | USD 2.82 Billion |

| Market Size (2030) | USD 3.81 Billion |

| Growth Rate (2025 - 2030) | 6.17% CAGR |

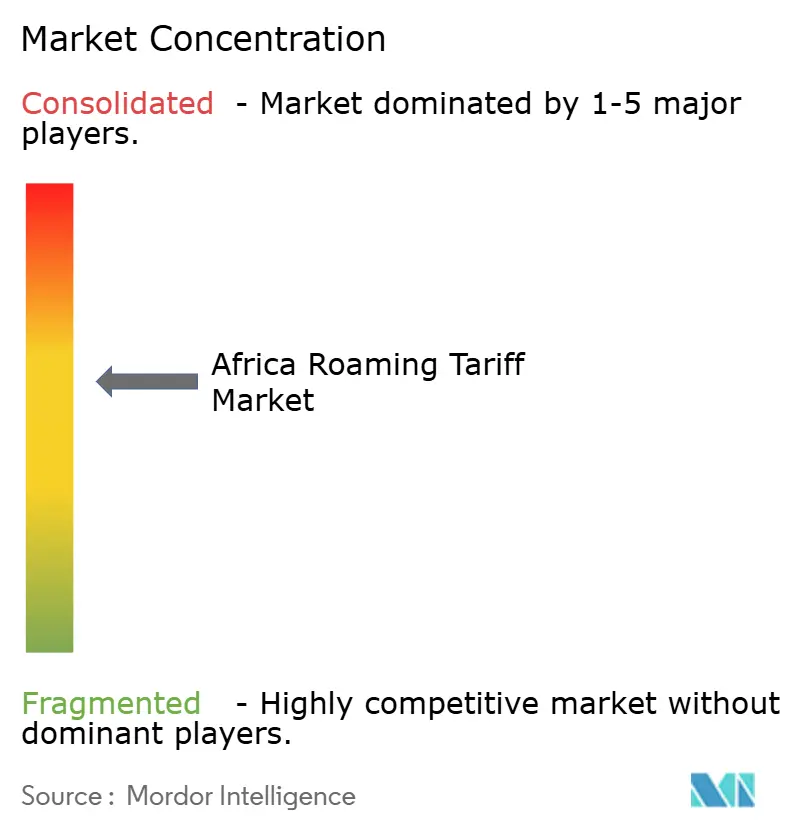

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Roaming Tariff Market Analysis by Mordor Intelligence

The Africa roaming tariff market size stands at USD 2.82 billion in 2025 and is forecast to reach USD 3.81 billion by 2030, reflecting a 6.17% CAGR. This expansion is fueled by accelerating adoption of Roam-Like-At-Home frameworks, strong growth in data-centric services, and enlarging cross-border travel under the African Continental Free Trade Area. Regulatory momentum across regional economic communities is narrowing wholesale price disparities, while operators deploy 4G and 5G networks that support premium roaming tiers. The integration of mobile money with roaming, combined with eSIM uptake, is anchoring new revenue streams that offset voice and SMS decline. However, persistent wholesale IOT price gaps and multiple-SIM ownership in rural areas still constrain organic demand, prompting operators to emphasize infrastructure sharing and flexible pricing models.

Key Report Takeaways

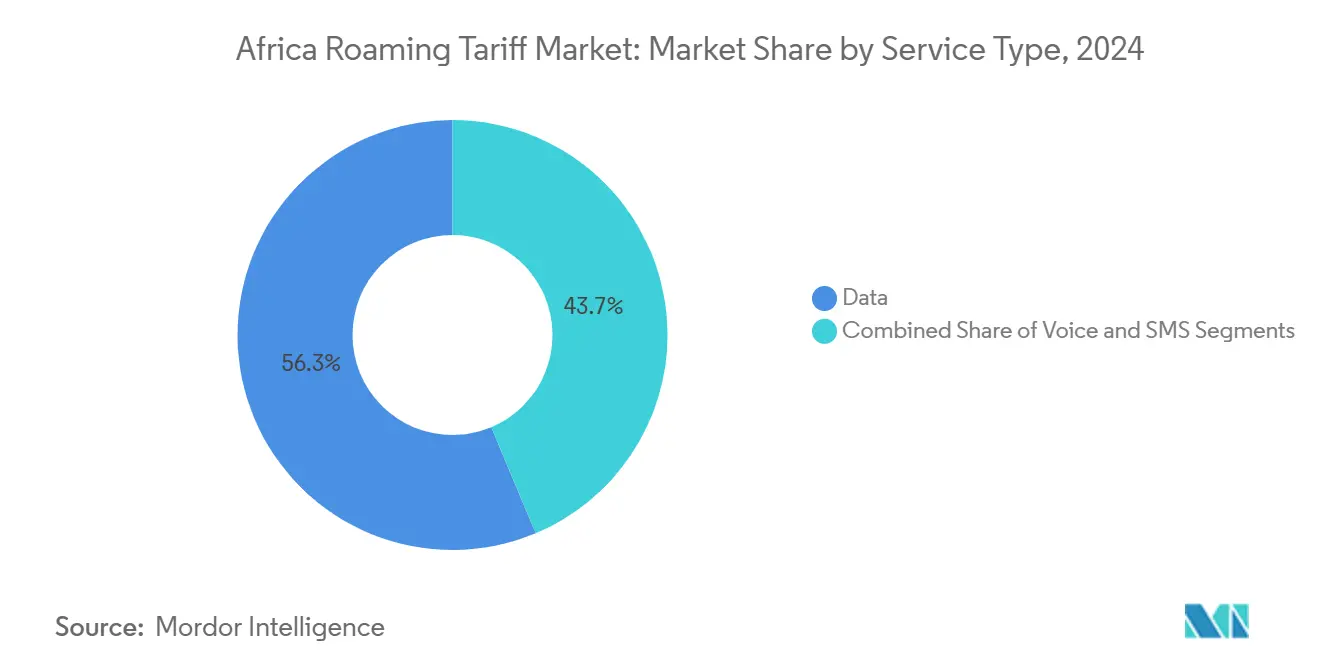

- By service type, data services led with a 56.32% share of the Africa roaming tariff market in 2024 and are projected to grow at a 6.78% CAGR through 2030.

- By roaming type, outbound roaming commanded a 62.59% share of the Africa roaming tariff market size in 2024, while inbound roaming is projected to grow at a 7.11% CAGR to 2030.

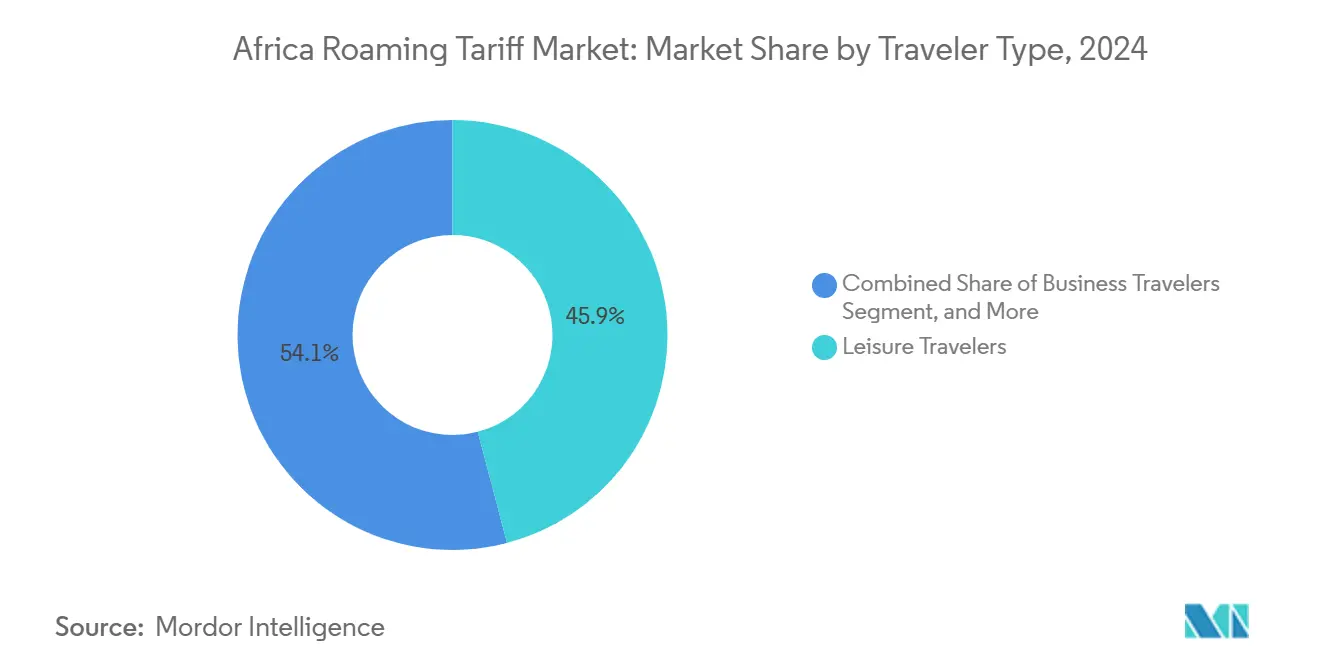

- By traveler type, leisure travelers accounted for 45.93% of the Africa roaming tariff market size in 2024; migrant workers and VFR traffic are projected to advance at a 6.91% CAGR through 2030.

- By network technology, 4G captured 55.89% of the Africa roaming tariff market share in 2024; 5G is projected to expand at a 7.34% CAGR between 2025-2030.

- By geography, Southern Africa held 28.71% of the Africa roaming tariff market share in 2024, whereas East Africa exhibits the fastest-growing pace at a 6.87% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Africa representing one of the more structurally developed among them. The global report on roaming tariff market by Mordor Intelligence reflects how these regional layers combine into a single system.

Africa Roaming Tariff Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of Roam-Like-At-Home (RLAH) Agreements | +1.2% | West Africa, East Africa, Southern Africa | Medium term (2-4 years) |

| Rising Cross-Border E-Commerce Driving Data Roaming | +1.1% | Global, with concentration in Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Surge in Intra-Africa Business Travel After AfCFTA | +0.9% | Global, early gains in Lagos, Nairobi, Cape Town | Medium term (2-4 years) |

| Expansion of 4G and 5G Network Footprints | +0.8% | Urban centers across all regions | Long term (≥ 4 years) |

| Growth of Travel SIM and eSIM Platforms | +0.6% | North Africa, Southern Africa with spillover to West Africa | Medium term (2-4 years) |

| Increasing Migrant Worker Remittances via Mobile Money | +0.5% | West Africa, East Africa corridor countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Roam-Like-At-Home Agreements

Regional blocs are quickly eliminating roaming surcharges, transforming pricing structures across the continent. The October 2024 free-roaming launch between Ghana, Togo, and Benin demonstrated that traffic volumes can triple within 18 months, even as wholesale revenue per minute drops sharply.[1]Ghana Business News, “Ghana, Gambia to Sign Free Roaming Agreement,” ghanabusinessnews.com Regulators such as the Communications Authority of Kenya and the Nigerian Communications Commission are standardizing dispute resolution and technical protocols, allowing operators to offer seamless cross-border plans that encourage higher usage despite lower unit prices.

Rising Cross-Border E-Commerce Driving Data Roaming

Small and medium enterprises conducting cross-border online sales now demand reliable roaming to process payments, synchronize inventory, and deliver real-time customer support. Nigeria alone recorded USD 7.3 billion in cross-border digital transactions during 2024.[2]Central Bank of Nigeria, “Payment System Statistics,” cbn.gov.ng Operators with extensive fiber backbones are capitalizing on this need by providing low-latency wholesale links and premium data packages, thereby monetizing consistent, business-critical traffic rather than sporadic consumer sessions.

Surge in Intra-Africa Business Travel After AfCFTA

The implementation of the continental free-trade area is boosting corporate travel, with roaming traffic on major business corridors increasing by 35% year over year.[3]African Development Bank, “African Continental Free Trade Area: Impact Assessment Report,” afdb.org Business travelers consume up to five times more data per session than leisure travelers and are willing to pay for assured quality of service. Many corporations now negotiate bulk roaming contracts directly with carriers, opening a high-value channel that rewards operators able to customize and guarantee performance.

Expansion of 4G and 5G Network Footprints

Next-generation networks broaden service availability but heighten investment and interoperability demands. Safaricom’s 5G launch in Nairobi in 2024 revealed that 5G roaming commands premiums 40-50% above 4G while requiring adherence to GSMA IR.88 standards. Smaller operators risk marginalization unless they share infrastructure or partner with wholesale aggregators that can spread capital costs across larger traffic bases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Wholesale IOT Price Disparities | -0.8% | Global, particularly acute in Central Africa | Medium term (2-4 years) |

| Regulatory Uncertainties on Surcharges | -0.6% | West Africa, Central Africa | Short term (≤ 2 years) |

| High Prevalence of Multiple-SIM Ownership | -0.5% | Rural areas across all regions | Long term (≥ 4 years) |

| Limited Roaming Awareness Among Rural Subscribers | -0.4% | Rural areas, particularly in Central and West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Wholesale IOT Price Disparities

Inter-operator tariffs vary by up to 15 times across markets, distorting competition and squeezing smaller carriers. Ethiopia’s 25.8% cut to mobile termination rates in May 2024 intensified downward pricing pressure on neighbors. In the absence of continental regulation, bargaining power rests with dominant telcos, which limits tariff harmonization and perpetuates uneven retail prices across borders.

Regulatory Uncertainties on Surcharges

Divergent national policies complicate long-term roaming agreements. In January 2025, Nigeria allowed tariff hikes up to 50%, while adjacent markets maintained different surcharge regimes. Operators must run parallel billing systems to remain compliant, which raises overhead and dampens incentives to launch continent-wide products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Reshapes Revenue Models

Data services held 56.32% of the Africa roaming tariff market share in 2024 and are forecasted to grow at a 6.78% CAGR, signaling a shift away from voice-centric usage. Enterprise roamers average 2.5 GB per trip versus 0.8 GB for leisure travelers. Operators now bundle tiered allowances, real-time usage alerts, and flat-rate passes to capture value while reducing the risk of bill shock. Voice and SMS persist for authentication and financial confirmations but generate modest incremental revenue.

The expansion of the Africa roaming tariff market in data creates an incentive for wholesale data aggregation hubs that dynamically route traffic based on price and latency. eSIM adoption accelerates this trend, simplifying remote provisioning and stimulating uptake among tech-savvy travelers, while simultaneously enabling users to bypass their home network if roaming options lag behind local alternatives.

By Roaming Type: Inbound Growth Signals Destination Appeal

Outbound usage accounted for 62.59% of the Africa roaming tariff market size in 2024. Nonetheless, inbound roaming is the fastest-growing category, with a 7.11% CAGR through 2030, as Africa’s tourism and business events sectors mature. Countries such as Rwanda, Ghana, and Botswana leverage favorable visa regimes and improved infrastructure to attract visitors, whose higher spending tolerance supports premium packages.

Rising inbound traffic pushes local operators to secure bilateral agreements with global carriers, often conceding lower wholesale margins in exchange for volume certainty. Enhanced inbound flows also underscore the importance of consistent quality of service, because international travelers compare African roaming performance with experiences in other regions.

By Traveler Type: Migrant Corridors Drive Sustained Growth

Leisure travelers remain the largest cohort, at 45.93% in 2024, yet migrant worker and VFR traffic are expanding fastest, at a 6.91% CAGR. Remittances moving through mobile money platforms require continuous connectivity, prompting bundled offerings that pair roaming data with reduced-fee money transfers.

Migrants are cost-conscious, so operators are launching prepaid roaming wallets that lock in rates across multiple countries, smoothing expenditure and encouraging habitual use. Corporate travelers continue to generate the highest average revenue per user; however, enterprises are increasingly negotiating pooled data plans that spread allowances across staff, thereby moderating per-user yields.

By Network Technology: 5G Premium Positioning Emerges

4G maintains 55.89% Africa roaming tariff market share in 2024 thanks to broad coverage and mature wholesale billing. 5G, though nascent, is expanding at a 7.34% CAGR as deployments concentrate in Lagos, Nairobi, and Cape Town business districts. Operators differentiate 5G roaming through ultra-low-latency guarantees, which are suited for high-definition videoconferencing and cloud-based analytics.

Implementing network slicing and end-to-end quality assurance raises capital barriers, favoring telcos with regional scale or ties to international groups. Legacy 3G and 2G networks will persist in rural areas as fallback layers for voice and basic data applications until spectrum refarming and device replacement cycles are completed beyond 2030.

Geography Analysis

Southern Africa’s leadership arises from cohesive wholesale arrangements, robust backhaul, and harmonized consumer protection codes. Operators share infrastructure to reduce duplication, enabling competitive pricing and consistent service across borders. Tourism and mining attract sustained inbound traffic with low price elasticity, bolstering average revenue per user.

East Africa’s high growth is attributed to tariff-free roaming within the bloc, encouraging travelers to keep their SIMs active instead of switching to local cards. Kenya’s 5G roll-out creates demonstration effects that motivate neighboring regulators to accelerate spectrum auctions and streamline site permitting, thereby further supporting improvements in roaming quality.

West Africa’s market is shifting as free-roaming pacts proliferate. Nigeria’s inclusion remains pivotal: its regulatory adjustments in 2025 permit operators to recoup 5G investment costs, but asymmetric policies with neighbors can create arbitrage that redistributes traffic. Central Africa’s infrastructure build-out remains in early stages, yet satellite backhaul partnerships promise rapid coverage extensions to remote areas that currently lack reliable roaming.

Competitive Landscape

The Africa roaming tariff market remains moderately fragmented. MTN Group leverages its pan-African presence to negotiate favorable wholesale rates and co-invest in subsea cables. Vodacom capitalizes on Vodafone’s global agreements to offer assured service levels to enterprise clients. Airtel Africa prioritizes affordable bundles tied to its mobile money platforms to capture migrant and VFR segments.

Wholesale aggregators BICS and Syniverse offer single-contract connectivity, which appeals to smaller operators lacking bilateral reach. Travel SIM and eSIM specialists are disrupting traditional roaming by retailing multi-country data packs directly to consumers, pressuring incumbents to refine pricing. Increasing infrastructure sharing, such as tower and fiber co-location, reduces capital intensity and aligns with regulators’ push for cost-efficient expansion.

To differentiate themselves, leading carriers integrate fintech services, offer real-time spend dashboards, and deploy AI-driven analytics that optimize route selection and enhance fraud management. Compliance with varied national data-privacy statutes and consumer-protection laws remains a gating capability that favors established players with robust legal teams.

Africa Roaming Tariff Industry Leaders

MTN Group Limited

Vodacom Group Limited

Airtel Africa Plc

Orange Middle East and Africa SA

Emirates Telecommunications Group Company PJSC (Etisalat Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Vodacom finalizes its cloud-based eSIM provisioning platform, allowing inbound tourists to activate local data plans on arrival in South Africa, Tanzania, Mozambique and the Democratic Republic of the Congo through a single QR code.

- September 2025: ECOWAS ministers adopt a bloc-wide wholesale roaming tariff benchmark that caps inter-operator tariffs at USD 0.015 per megabyte, creating a common reference rate for all 15 member states.

- June 2030: GSMA launches the Africa Roaming Clearing Hub, enabling real-time wholesale settlement and fraud detection for over 40 regional mobile operators, cutting average invoice reconciliation time from 30 days to 3 days.

- March 2025: Safaricom, MTN Group and Airtel Africa introduce a joint “One Africa Data Pass” that provides unified 4G and 5G roaming allowances across 12 countries, eliminating daily surcharges for enterprise subscribers.

Africa Roaming Tariff Market Report Scope

| Voice |

| SMS |

| Data |

| Inbound |

| Outbound |

| Leisure Travelers |

| Business Travelers |

| Migrant Workers and VFR |

| 2G |

| 3G |

| 4G |

| 5G |

| North Africa |

| West Africa |

| Central Africa |

| East Africa |

| Southern Africa |

| By Service Type | Voice |

| SMS | |

| Data | |

| By Roaming Type | Inbound |

| Outbound | |

| By Traveler Type | Leisure Travelers |

| Business Travelers | |

| Migrant Workers and VFR | |

| By Network Technology | 2G |

| 3G | |

| 4G | |

| 5G | |

| By Geography | North Africa |

| West Africa | |

| Central Africa | |

| East Africa | |

| Southern Africa |

Key Questions Answered in the Report

What value are Africa roaming tariffs projected to reach by 2030?

They are forecast to climb to USD 3.81 billion.

How quickly are Africa roaming tariffs expected to expand from 2025 to 2030?

A 6.17% compound annual growth rate is projected for the period.

Which service currently brings in the most roaming revenue across Africa?

Data services lead with 56.32% share, driven by smartphone and cloud-application usage.

Which African region is growing the fastest for roaming tariffs?

East Africa posts the highest pace at a 6.87% CAGR on the back of the One Network Area initiative.

What technology tier is advancing the quickest in African roaming?

5G roaming shows the fastest rise, tracking a 7.34% CAGR as operators monetize premium, low-latency connectivity.

Which companies hold leading positions in African roaming tariffs?

MTN Group, Vodacom and Airtel Africa dominate, supported by wholesale aggregators BICS and Syniverse.

Page last updated on: