Acoustic Insulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

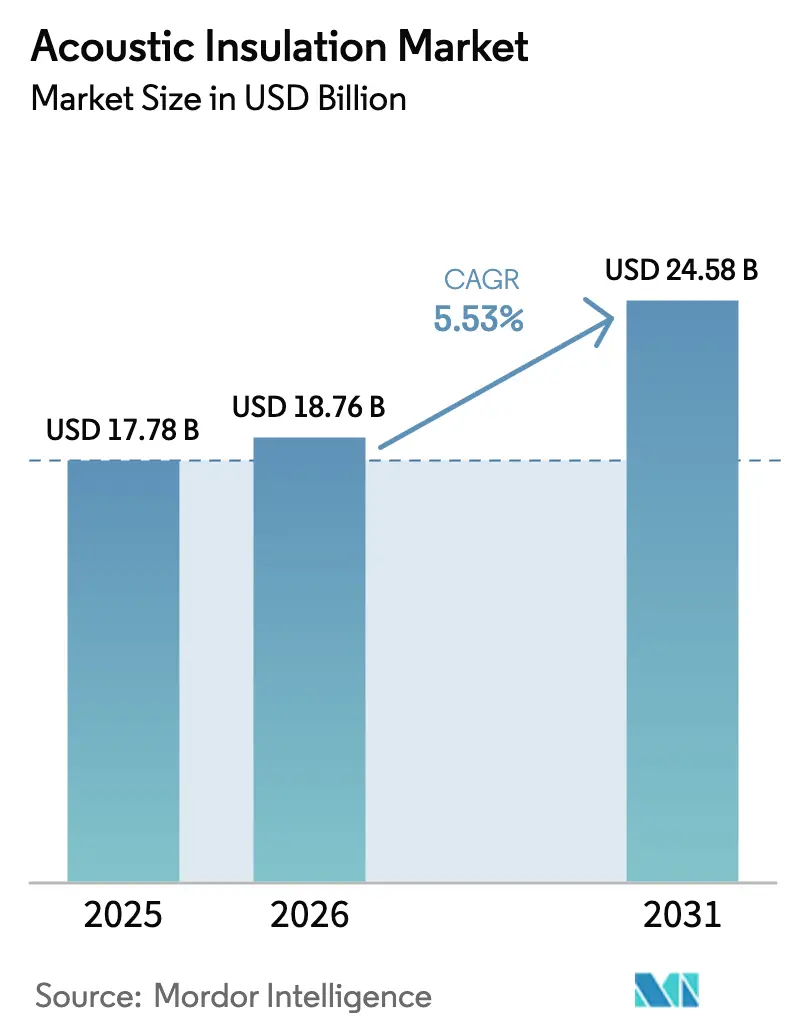

| Market Size (2026) | USD 18.76 Billion |

| Market Size (2031) | USD 24.58 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acoustic Insulation Market Analysis by Mordor Intelligence

The Acoustic Insulation Market was valued at USD 17.78 billion in 2025 and estimated to grow from USD 18.76 billion in 2026 to reach USD 24.58 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). Regulatory authorities in every major region are tightening noise-control rules, propelling early-stage specification of sound-dampening materials in residential, commercial, and industrial projects. Urbanization in Asia-Pacific, the proliferation of open-plan offices in developed economies, and the integrating of acoustic comfort into building energy codes have moved noise mitigation from an afterthought to a core design criterion. Mineral wool retains leadership because it offers robust fire resistance and high sound absorption, and polymeric foams are closing the gap as HVAC engineers demand lightweight, moisture-tolerant solutions. Meanwhile, manufacturers are pursuing carbon-reduced formulations and certified biobased content to align acoustic performance with green-building targets, a combination shaping the competitive playbook in the acoustic insulation market.

Key Report Takeaways

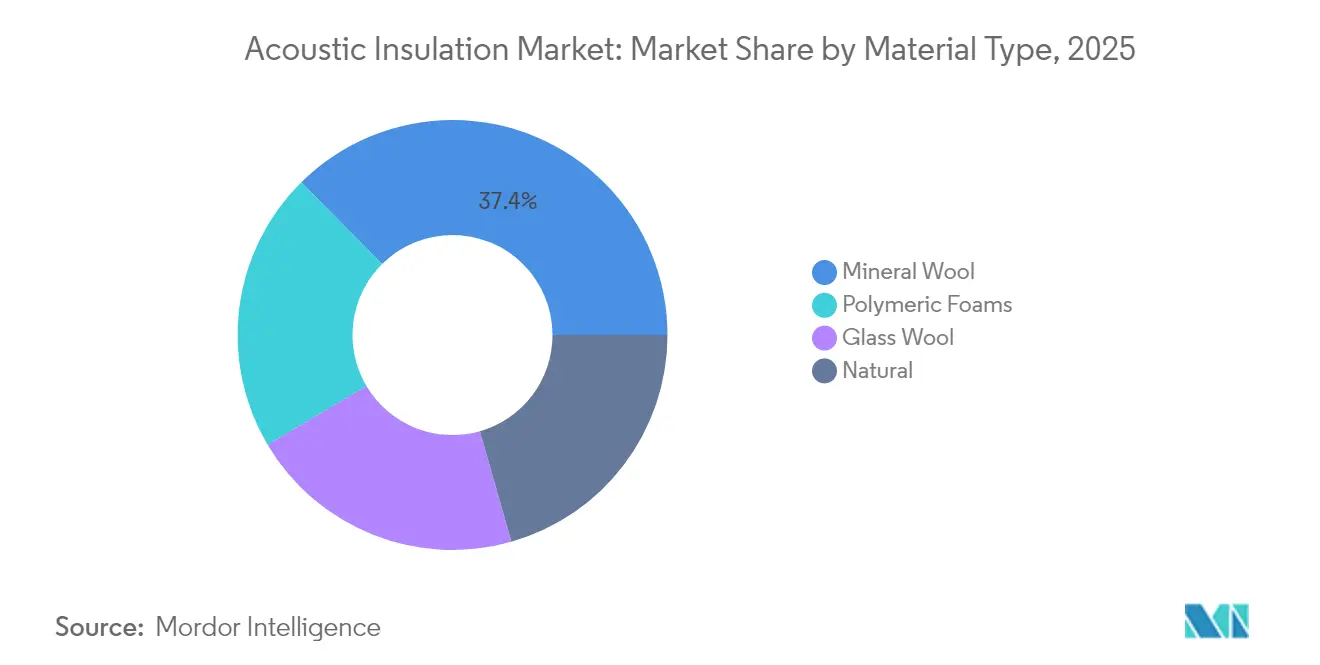

- By material, mineral wool led with 37.42% revenue share in 2025, while polymeric foams are projected to expand at a 5.94% CAGR through 2031.

- By installation zone, wall and partition applications commanded 39.48% of the acoustic insulation market size in 2025, whereas HVAC duct and pipe wrap solutions are growing at 6.12% annually.

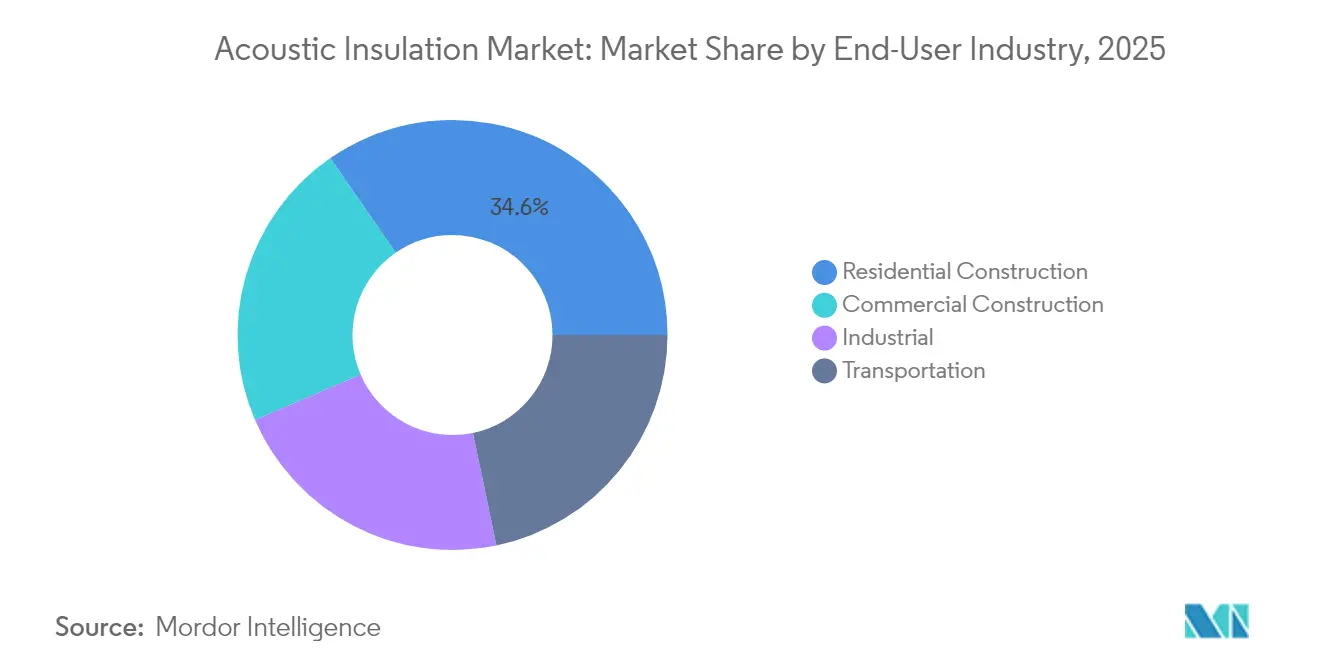

- By end-user, residential construction accounted for 34.62% of the acoustic insulation market size in 2025 and is progressing at a 5.91% CAGR to 2031.

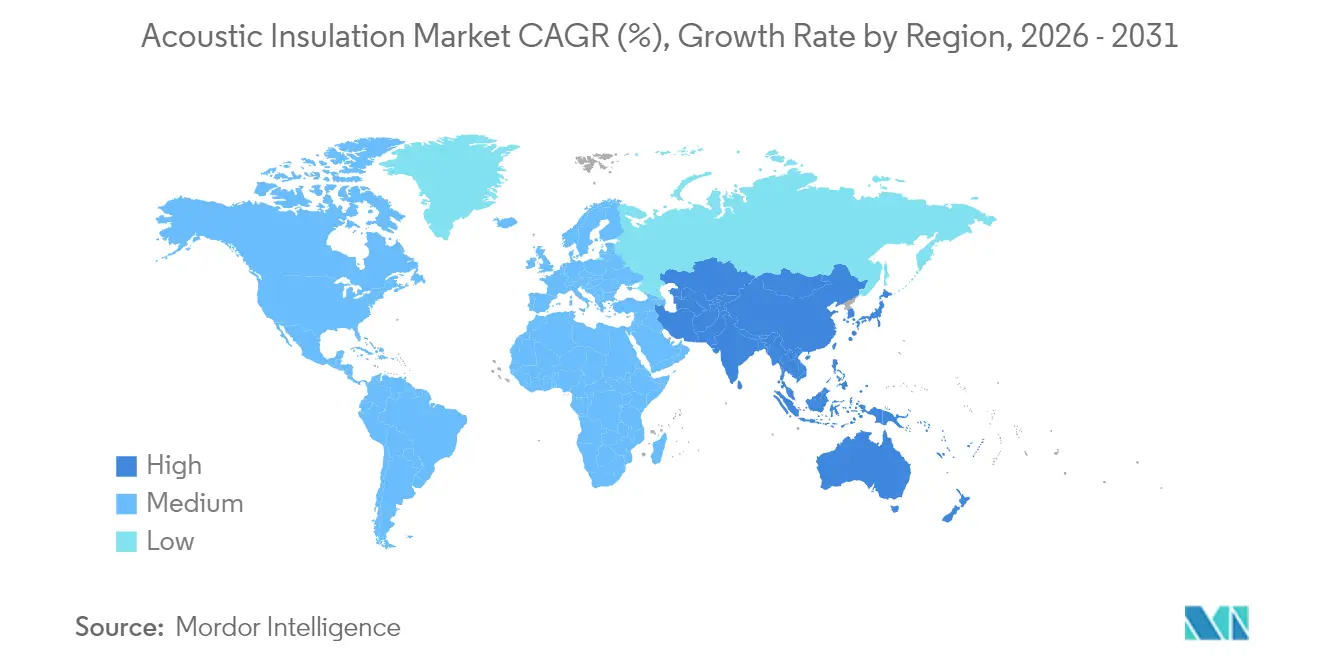

- By region, Asia-Pacific held 36.58% of the acoustic insulation market share in 2025 and is set to record the fastest 7.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acoustic Insulation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Boom-Driven Noise Mitigation Mandates in Asia | +1.80% | Asia-Pacific with spillover to Middle East | Medium term (2-4 years) |

| Government Regulations for Controlling Noise Pollution and Surge in Adoption in Residential Application | +1.50% | Europe and North America followed by Asia | Long term (≥4 years) |

| Rise in Demand from Emerging Economies | +1.00% | Core APAC with spillover to MEA | Medium term (2-4 years) |

| Growth of Open-Plan Offices Spurring Ceiling & Partition Acoustic Panels | +0.80% | High in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Boom-Driven Noise Mitigation Mandates in Asia

Massive investment in rail, airport, and mixed-use real estate across China, India, and Southeast Asia is amplifying demand for low-profile yet high-performance acoustic barriers. China’s updated GB 50118 building code introduces stricter STC thresholds that developers must meet from January 2025, forcing the acoustic insulation market to supply tested systems at scale. India’s phased amendments to its National Building Code replicate this regulatory momentum, locking acoustics into early design and tender stages instead of late-cycle fixes. Multi-tower housing, elevated metro lines, and logistics corridors are now heavily scrutinized for community noise impact, which is pushing architects toward hybrid mineral-wool and polymeric-foam composites that block wide frequency ranges. Manufacturers are localizing production near growth corridors to cut transport noise during logistics and to shorten lead times for large infrastructure lots. Consequently, compliance-driven procurement is accelerating value migration from basic bulk rolls toward certified systems that bundle acoustic, thermal, and fire performance attributes within one product line. This activity is securing a long-run demand floor for the acoustic insulation market while re-shaping sales channels toward specification-led models.

Government Regulations for Controlling Noise Pollution

Policy frameworks are moving beyond simple decibel caps to holistic health-based indicators, forcing specifiers to document absorption coefficients, STC ratings, and life-cycle profiles. The European Union has refreshed the Environmental Noise Directive and Regulation No 540/2014 on vehicle noise, obliging member states to map and treat major road, rail, and airport corridors by 2026. In the United States, ongoing litigation against the EPA to enforce the dormant Noise Control Act has reignited debate on national standards, energizing municipalities that already require acoustic studies for mixed-use permitting[1]Joanne Silberner, “Why Scientists Who Study Noise Pollution Are Calling for More Regulation,” NPR, npr.org . As regulations solidify, procurement teams now demand third-party certificates that prove compliance, opening premium price territory for suppliers with complete documentation packages. Coupling of acoustic standards with energy codes is also growing; several EU states now recognise mineral-wool cavity barriers as both thermal and sound partitions, generating dual-value propositions that fortify pricing power in the acoustic insulation market.

Rise in Demand from Emerging Economies

Rapid urbanisation, rising disposable incomes, and greater awareness of wellness are lifting baseline expectations of acoustic comfort across Southeast Asia and parts of Africa. Developers in tropical climates require solutions that can manage both humidity and noise, prompting a shift toward hybrid glass-and-stone-wool panels coated for moisture resistance. Plant expansions in Indonesia, Vietnam, and Kenya are lowering landed costs and shrinking order-to-delivery cycles, advantages that local distributors leverage to win municipal housing contracts. As domestic production deepens, knowledge-transfer programmes are disseminating best-practice installation, gradually closing the workmanship gap that previously curtailed performance in field conditions. These forces are embedding acoustic insulation into mainstream residential specifications, enlarging the addressable base of the acoustic insulation market.

Growth of Open-Plan Offices Spurring Ceiling & Partition Acoustic Panels

The post-pandemic office refresh emphasises collaboration yet demands quiet zones for hybrid meetings, a duality that drives high NRC ceiling tiles, fabric-wrapped baffles, and moveable partitions. MIT researchers recently demonstrated silk-based textiles that cut sound transmission by 75%, a breakthrough that is already inspiring product roadmaps for modular partitions. Ceiling-grid innovators respond with drop-in tiles boasting NRC values above 0.90, while free-standing dividers integrate recycled PET cores to balance mass and portability. This workplace retrofit cycle is spawning rapid-turn orders, pushing manufacturers to develop color-matched, tool-free panel systems that installers can reposition overnight. As corporate real-estate teams chase WELL and LEED points, documented acoustic performance has become a negotiation lever, further galvanising demand inside the acoustic insulation market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Petrochemical Feedstock Impacting Foamed-Plastic Cost Parity | -0.90% | Global, acute in import-dependent regions | Short term (≤2 years) |

| Installation Skill Gap for Aerogel Blankets in Emerging Markets | -0.50% | Emerging APAC and Latin America | Medium term (2-4 years) |

| Recycling Compliance Pressures on Multilayer Composite Waste Streams | -0.30% | Europe expanding globally | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Feedstock Impacting Foamed-Plastic Cost Parity

Surging prices for isocyanates and blowing agents widen cost differentials between polymeric foams and mineral wool, disrupting established project budgets. Contractors in price-sensitive markets now substitute lower-grade fibre batts when foam quotes spike, trimming short-term demand for polyurethane and extruded polystyrene lines. In response, research teams are reformulating foams with recycled PET, sugarcane bagasse polyols, and bio-CO₂ expansion to insulate against crude-oil price swings. Yet scale-up remains uneven, and volatility is expected to persist through 2026, tempering foam uptake even as performance credentials remain strong.

Installation Skill Gap for Aerogel Blankets in Emerging Markets

Ultra-thin aerogel mats provide exceptional thermal and acoustic attenuation but require specialised cutting tools, edge sealing, and protective gear. Many contractors in fast-growing regions lack these competencies, leading to project delays or last-minute product swaps. Global suppliers are rolling out pre-laminated roll formats and mobile training units; however, adoption lags material innovation, keeping aerogel penetration concentrated in North America and parts of Europe. This execution barrier curtails revenue upside for high-end product lines in the acoustic insulation market until installer certifications become widespread.

Segment Analysis

By Material Type: Mineral Wool Dominates Amid Sustainability Push

Mineral wool generated 37.42% of 2025 revenue, propelled by inherent fire resistance, robust low-frequency absorption, and compatibility with evolving safety codes. ROCKWOOL estimates that stone-wool systems sold in 2024 will save 818 TWh of lifetime energy while enhancing learning conditions for 1.8 million students worldwide. Glass-wool follows closely thanks to lightweight, cost efficiency, and ease of cutting on job sites, especially in pitched-roof housing. Polymeric foams post the quickest 5.94% CAGR as HVAC engineers prioritise moisture control and flexible fit for complex duct geometries, though feedstock volatility moderates uptake. Natural-fiber categories are advancing in low-carbon building schemes, with products like IndiTherm batts delivering a 40 dB reduction at 50 mm thickness and negative embodied carbon scores. Reformulated binders that eliminate formaldehyde and achieve biobased certification are helping mineral wool withstand competitive pressure, ensuring the acoustic insulation market maintains balanced material diversity.

Note: Segment shares of all individual segments available upon report purchase

By Installation Zone: Wall & Partition Leads Acoustic Solutions

Wall and partition assemblies accounted for 39.48% of the acoustic insulation market size in 2025, reflecting stringent inter-unit sound isolation rules in multi-family housing and hotels. The UK’s Approved Document E sets explicit airborne and impact-sound limits, driving high-density mineral-wool slabs and integrated mass-loaded barriers. Ceiling and roof installations are increasingly specified with seamless tile systems that achieve drywall aesthetics while earning LEED acoustic credits. Floor and sub-floor zones, though smaller today, gain traction as owners retrofit older stock to quell footfall noise. HVAC duct and pipe wrap applications show a leading 6.12% CAGR, with Knauf’s Performance+ insulation providing asthma- and allergy-friendly certification in tandem with high NRC ratings. Emerging lightweight composites blend aerogel and glass-wool layers to boost acoustic and thermal resistance without breaching structural load limits, broadening the addressable project mix for the acoustic insulation market.

By End-User Industry: Residential Construction Drives Volume

The residential segment captured 34.62% of revenue in 2025 and is projected to grow at a 5.91% CAGR through 2031. National retrofit programmes, such as the Great British Insulation Scheme under consultation by the Department for Levelling Up, channel public funding toward sound-attenuating cavity fills that simultaneously improve energy ratings. Homeowners cite sleep quality and quiet study areas as leading motivations, prompting do-it-yourself retailers to stock blow-in cellulose like Greenfiber’s SANCTUARY, which can reduce sound power by 60% while trimming heating and cooling costs by 25%. Builders in high-rise condominiums are shifting to dual-purpose mineral-wool boards that meet both acoustic and two-hour fire-rating clauses, ensuring the acoustic insulation market embeds deeper into mainstream residential architecture.

The transportation sector is expanding as automakers, rolling-stock producers, and aircraft OEMs address weight, vibration, and passenger comfort challenges. Research highlights the impact of thickness and fiber orientation on absorption coefficients, driving suppliers to develop multi-layer mats with graded densities. Lear Corporation's FlexAir foam reduces CO₂ emissions by 50% while retaining acoustic damping. The rise of battery-electric vehicles shifts focus to road and wind noise, while shipbuilders adopt mineral-wool fire-blocks to meet SOLAS noise codes. These trends ensure continued technological investment and growth in the acoustic insulation market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated with a 36.58% revenue share in 2025, and the region is forecast to log a 7.38% CAGR through 2031 as China, India, and emerging ASEAN economies advance mega-rail corridors, smart-city zones, and high-rise residential clusters. China’s community backlash against elevated noise has spurred local authorities to enforce stricter facade STC benchmarks, translating into bulk orders for dense stone-wool curtain-wall inserts. India’s urban housing drive, backed by state incentives, similarly elevates acoustic compliance from optional to mandatory, swelling demand for glass-wool rolls and lightweight partition kits.

In 2024, North America significantly contributed to global revenue, driven by proactive office retrofits and heightened enforcement of municipal noise ordinances. Municipal planners increasingly require noise-impact studies for mixed-use permits, and architects respond with hybrid mineral-wool and recycled-PET panels to balance cost and LEED credits. Premium aerogel tapes for curtain-wall spandrels are gaining traction in dense city cores where floor-area ratios pressure facade thickness. Europe remains a key player in regulatory advancements, with the EU's Environmental Noise Directive driving the requirement for updated noise maps and action plans by 2026. Multi-family housing and transport hubs are benefiting significantly, utilizing mineral-wool cavity barriers and high-NRC ceiling clouds that comply with stringent fire classifications. The Middle East and Africa region is experiencing robust growth, particularly in Gulf Cooperation Council states, which are incorporating world-class acoustic standards into their stadiums, metros, and airport terminals. South America contributes notably to sales, with Brazil leading through condominium retrofits favoring glass-wool batts, while Argentina is gradually adopting modular wall panels as awareness increases. This diverse regional landscape highlights the global scope of the acoustic insulation market and provides resilience against market cyclicality

Competitive Landscape

The acoustic insulation market displays moderate fragmentation concentration; the five largest vendors controlled roughly 35% of global revenue in 2024. Saint-Gobain leverages a multi-material portfolio spanning stone-wool, glass-wool, and polymeric foams, enabling cross-selling to builders chasing single-source procurement. ROCKWOOL capitalises on fire and acoustic co-compliance, underscored by its 2023 sustainability report projecting 818 TWh lifetime energy savings from stone-wool sold in that year. Owens Corning and Knauf Insulation double down on product transparency by publishing Environmental Product Declarations that ease specification under LEED v4 and BREEAM schemes.

Innovation pipelines converge on multi-attribute panels that integrate acoustic, thermal, and fire performance. Kingspan’s QuadCore LEC panels reduce embodied carbon by up to 21% while adding sound-attenuation layers, exemplifying this integrated approach. Suppliers are also piloting QR-coded labels that link to digital datasheets, streamlining compliance checks during site inspections and differentiating offerings in bids. These moves collectively keep competitive intensity high while maintaining stable price realisation in the acoustic insulation market.

Acoustic Insulation Industry Leaders

Saint-Gobain

ROCKWOOL A/S

Owens Corning

Knauf Group

Kingspan Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Knauf Insulation has expanded its Performance+ portfolio with new pipe and pipe & tank fiberglass insulation lines. These formaldehyde-free products are the first to achieve both Asthma & Allergy Friendly Certification and Verified Healthier Air designation.

- December 2024: ROCKWOOL has announced a USD 100 million investment in a new production line in Mississippi dedicated to industrial insulation products. This initiative aims to address the increasing demand from the process industry in the Gulf of Mexico region.

Global Acoustic Insulation Market Report Scope

Acoustic insulation is a lightweight bulky material that absorbs sound wave energy and reduces sound echo in homes, offices, and other buildings as it's penetrating the walls and ceilings. In cars and airplanes, it's also used to reduce engine noise going out into the passenger areas. In concert halls and auditoriums, it helps absorb sounds by reducing echo. The acoustic insulation market is segmented based on type, end-user industry, and geography. The market is segmented by type: mineral wool, glass wool, polymeric foams, and natural. The end-user industry segments the market into residential, commercial, transportation, and industrial construction. The report also covers the market size and forecasts for acoustic insulation in 15 countries across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Mineral Wool |

| Glass Wool |

| Polymeric Foams |

| Natural |

| Wall and Partition |

| Floor and Sub-Floor |

| Ceiling and Roof |

| HVAC Duct and Pipe Wrap |

| Residential Construction |

| Commercial Construction |

| Transportation |

| Industrial |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Mineral Wool | |

| Glass Wool | ||

| Polymeric Foams | ||

| Natural | ||

| By Installation Zone | Wall and Partition | |

| Floor and Sub-Floor | ||

| Ceiling and Roof | ||

| HVAC Duct and Pipe Wrap | ||

| By End-User Industry | Residential Construction | |

| Commercial Construction | ||

| Transportation | ||

| Industrial | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the acoustic insulation market?

The acoustic insulation market is valued at USD 18.76 billion in 2026 and is projected to reach USD 24.58 billion by 2031.

Which region contributes the largest share to the acoustic insulation market?

Asia-Pacific led with 36.58% share in 2025 and is also the fastest-growing region, recording a projected 7.38% CAGR.

Why is mineral wool the leading material in acoustic insulation?

Mineral wool combines high sound-absorption with fire resistance, giving it 37.42% revenue share in 2025 and a durable advantage where building codes demand both properties.

How are government regulations influencing demand for acoustic insulation?

Enhanced noise-control mandates in Europe, North America, and Asia require documented acoustic performance, motivating builders to specify certified insulation systems at the design stage.

Who are the major players in the acoustic insulation market?

Key players include Saint-Gobain, ROCKWOOL A/S, Owens Corning, Knauf Insulation, and Kingspan Group.