Acellular Dermal Matrices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

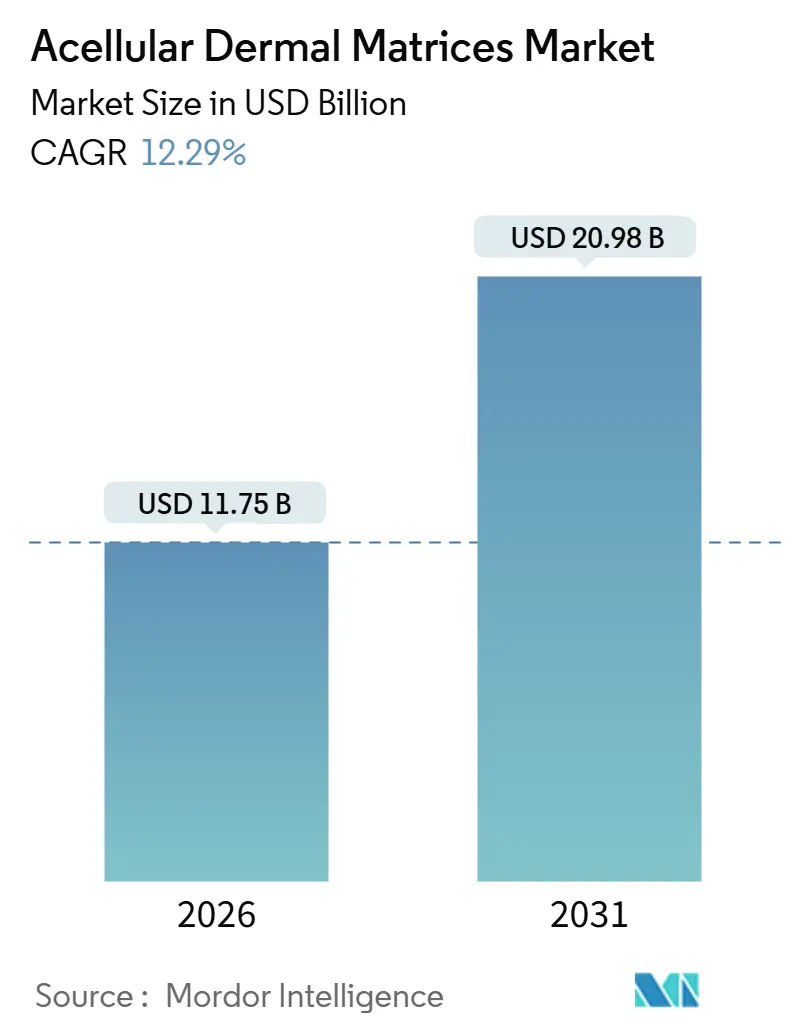

| Market Size (2026) | USD 11.75 Billion |

| Market Size (2031) | USD 20.98 Billion |

| Growth Rate (2026 - 2031) | 12.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acellular Dermal Matrices Market Analysis by Mordor Intelligence

The Acellular Dermal Matrices Market size is estimated at USD 11.75 billion in 2026, and is expected to reach USD 20.98 billion by 2031, at a CAGR of 12.29% during the forecast period (2026-2031).

Bundled-payment models that reward lower readmission rates, advances in decellularization that cut processing losses, and the entry of biosynthetic scaffolds are broadening hospital access to biologic meshes. Product innovations such as pre-hydrated sheets and micronized pastes are shortening operating-room prep times, which improves throughput at ambulatory centers. Supply-chain constraints around cadaveric tissue are steering manufacturers toward xenograft and hybrid synthetic matrices that avoid donor-availability bottlenecks. Meanwhile, regional regulatory harmonization, especially in the Asia-Pacific region, is compressing approval timelines and enabling faster geographic expansion. Competitive intensity remains moderate as leading tissue banks race to automate processing lines and secure long-term donor agreements.

Key Report Takeaways

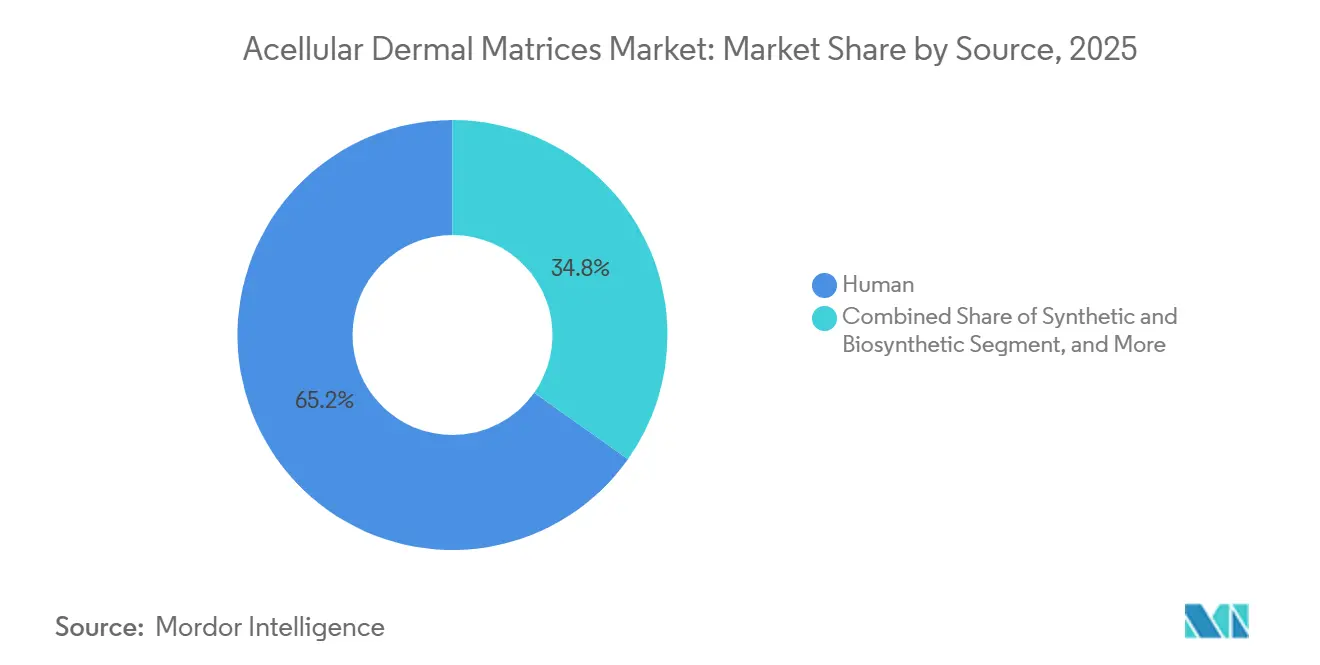

- By source, human-derived products led with 65.21% of the acellular dermal matrices market share in 2025, and synthetic & biosynthetic are advancing at a 13.22% CAGR through 2031.

- By product, freeze-dried sheets held 41.07% share of the acellular dermal matrices market size in 2025, and custom 3-D printed scaffolds are advancing at a 14.52% CAGR through 2031.

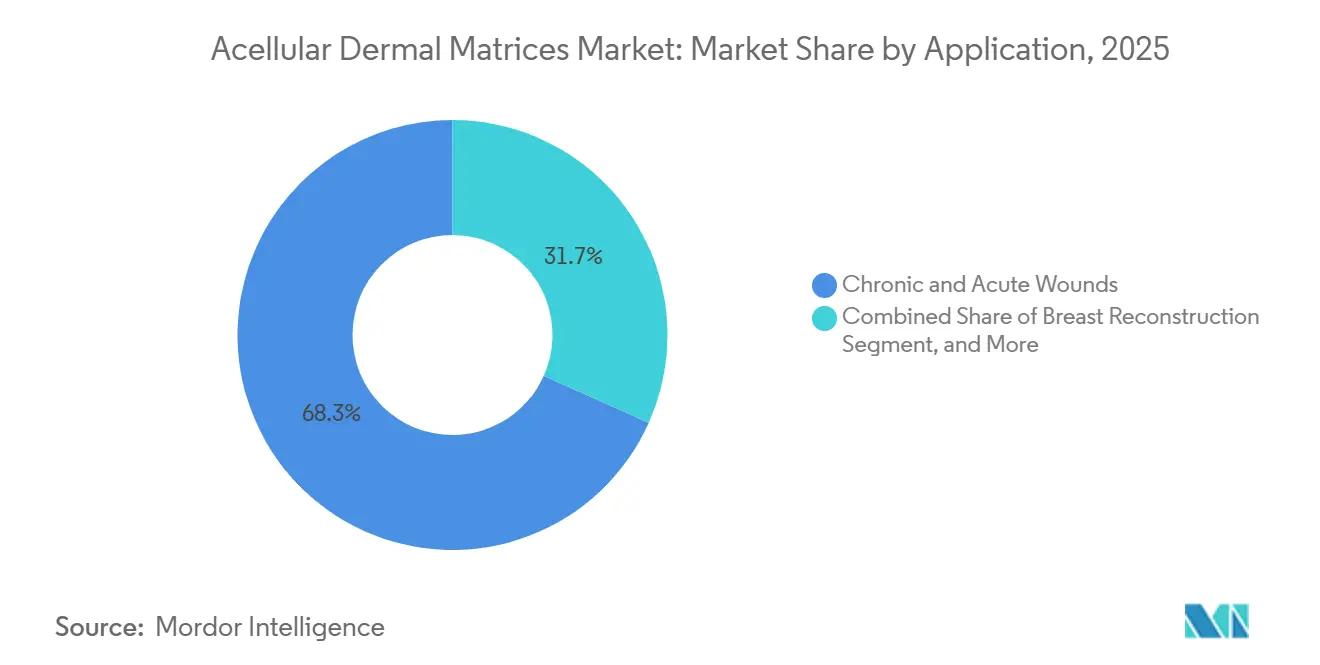

- By application, chronic & acute wounds led the acellular dermal matrices market with 68.32% market share in 2025, and breast reconstruction is advancing at an 18.08% CAGR through 2031.

- By end user, hospitals accounted for 45.93% of 2025 revenue, and ambulatory surgical centers are expanding at a 15.43% CAGR through 2031.

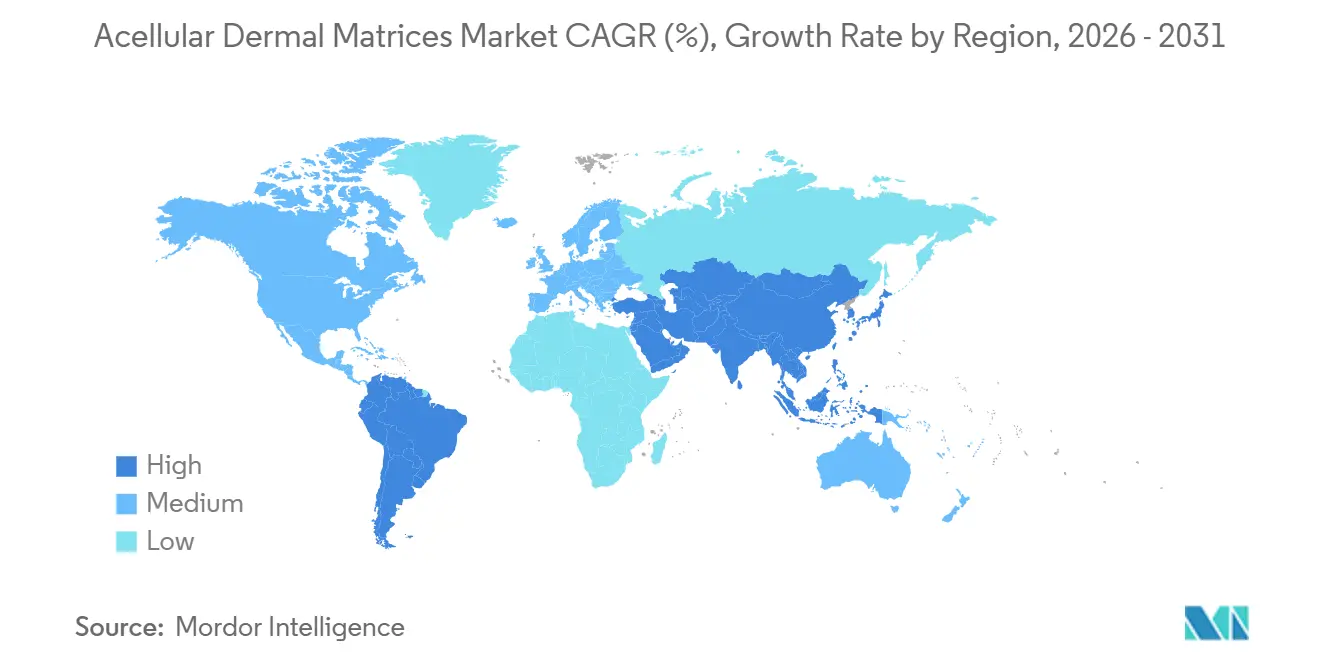

- By geography, North America captured 42.83% of 2025 sales, whereas Asia-Pacific is poised for the fastest 16.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acellular Dermal Matrices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Breast-Reconstruction Procedures | +2.8% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Growing Incidence of Chronic Wounds & Burns | +2.1% | Global, concentrated in aging high-income markets | Long term (≥ 4 years) |

| Advances in Decellularization Technologies | +1.9% | Global, R&D hubs in North America and Europe | Medium term (2-4 years) |

| DRG Bundling in Hernia Repairs | +1.6% | North America, Europe | Short term (≤ 2 years) |

| 3-D Printed Patient-Specific Scaffolds | +1.4% | North America, select European centers, early Asia-Pacific | Long term (≥ 4 years) |

| On-Site Hospital Tissue Banks | +1.1% | North America, expanding into Europe and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Breast-Reconstruction Procedures Post-Mastectomy

Surgeons have shifted toward single-stage implant placement supported by acellular dermal matrices because the technique lowers capsular contracture risk and cuts recovery time.[1]U.S. Food and Drug Administration, “Safety Communication on ADM in Breast Surgery,” fda.gov The 2024 FDA safety communication that compared infection profiles across brands heightened demand for aseptically processed allografts with low biofilm affinity. Hospitals in lower-margin settings remain cautious because most payers fold the matrix cost into mastectomy DRGs, forcing facilities to absorb USD 1,000–5,000 per sheet. Oncoplastic techniques combining tumor removal and immediate reconstruction are expanding in Europe and the Asia-Pacific, widening the clinical canvas for premium matrices. As reimbursement codes mature in emerging markets, the acellular dermal matrices market penetration in breast surgery is expected to accelerate.

Growing Incidence of Chronic Wounds & Burns

More than 40 million people are expected to suffer from diabetic foot ulcers or venous ulcers by 2030, sustaining demand for matrices that accelerate granulation tissue formation.[2]World Health Organization, “Diabetes and Chronic Disease Data,” who.int Products such as DermACELL paste have improved scar elasticity in burn follow-up, though reviews note slower early epithelialization relative to autografts. Variable HCPCS coding and step therapy that mandates cheaper dressings first delay adoption, yet micronized formats that fit irregular wounds are gaining traction in outpatient centers because they cut application time. Continued payer evidence requirements will shape the trajectory of the acellular dermal matrices market in chronic-wound care.

Advances in Decellularization & Sterilization Technologies

Protocols that cut residual DNA below 50 ng per mg minimize immunogenicity while gamma irradiation enables terminal sterilization, extending shelf life and simplifying logistics. Tissue banks can now scale output without proportional donor growth, mitigating a long-standing bottleneck. Similar methods applied to porcine and bovine dermis are producing lower-cost xenografts, though some surgeons remain cautious about graft integration in immunocompromised patients. These process gains bolster supply resilience for the acellular dermal matrices market.

DRG Bundling Boosts Biologic Mesh Use in Hernia Repairs

MS-DRG 338-339 bundles mesh cost into the episode, pushing hospitals to weigh readmission penalties against device price.[3]Centers for Medicare & Medicaid Services, “MS-DRG Definitions,” cms.gov Biologic matrices are favored for CDC class III-IV repairs because lower infection rates reduce 90-day penalties. Yet in elective clean cases, surgeons revert to USD 100 polypropylene because studies show no recurrence advantage, capping broader uptake. Volume contraction and guideline reinforcement will dictate the market momentum for acellular dermal matrices in hernia surgery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Cost & Inconsistent Reimbursement | -2.3% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Complex, Lengthy Biologic Approvals | -1.8% | Global, intensified in Europe and Asia-Pacific | Medium term (2-4 years) |

| Cadaveric Dermis Supply Bottlenecks | -1.5% | North America, Europe | Long term (≥ 4 years) |

| Uptake of Low-Cost Synthetic Meshes | -1.2% | Global, especially cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Product Cost & Inconsistent Reimbursement

ADM sheets priced at USD 1,000–5,000 squeeze budgets when payers bundle costs under DRGs, forcing hospitals to internalize the difference. Local Medicare contractors differ on coverage, and private plans often require prior authorization or proof that cheaper dressings failed. European HTA bodies apply strict cost-effectiveness thresholds, while Japanese and Australian payers insist on local data before granting codes. Until reimbursement coherence improves, price pressure will temper the growth rate of the acellular dermal matrices market.

Complex, Lengthy Biologic-Device Approvals

Minimally manipulated allografts may follow the HCT/P route, yet any scaffold combined with synthetic polymers or growth factors triggers a Biologics License Application that can last 5–7 years. Europe’s ATMP rules impose similar trial burdens, and Asia-Pacific regulators often duplicate Western data, inflating development costs. These delays deter smaller innovators and slow the refresh cycle within the acellular dermal matrices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Human Dermis Dominates Despite Supply Constraints

Human-derived products held 65.21% of the acellular dermal matrices market share in 2025, reflecting surgeons' trust in long-term clinical data. Supply limits, variable donor consent, and price premiums, however, are accelerating a 13.22% CAGR for synthetic and biosynthetic substitutes through 2031. The acellular dermal matrices market size for xenografts is poised to expand as decellularization reduces immunogenicity and regulatory bodies publish clearer guidance. Synthetic-collagen hybrids that tolerate terminal sterilization and room-temperature storage address hospital logistics pain points, giving engineered scaffolds an edge.

Demand for autologous options stays niche because harvesting raises morbidity, yet pediatric surgeons prefer the immunologic safety. Investor attention is shifting to biosynthetic hybrids that can scale without donor dependency, signaling a future pivot in the acellular dermal matrices market.

By Product: Freeze-Dried Sheets Lead, Custom Scaffolds Gain Traction

Freeze-dried sheets accounted for 41.07% of revenue in 2025, favored for a five-year shelf life and easy hydration before placement. Pre-hydrated variants shorten prep time, making them popular in ambulatory centers. The acellular dermal matrices market for custom 3-D-printed scaffolds is growing at 14.52% annually as academic sites trial patient-specific implants for craniofacial and chest-wall defects. Cost and regulatory ambiguity temper adoption, but AI-driven design systems are expected to cut lead times and halve prices by 2028.

Micronized injectable formats simplify treatment of irregular ulcers and fistulas, though inconsistent reimbursement slows volume. If CMS assigns clearer HCPCS codes, outpatient uptake could spike, further diversifying the acellular dermal matrices market.

By Application: Chronic Wounds Dominate, Breast Reconstruction Surges

Chronic and acute wounds accounted for 68.32% of the 2025 volume, driven by global diabetes growth and aging demographics. Breast reconstruction is the fastest-growing segment, with a 18.08% CAGR, driven by over 100,000 annual mastectomies in the United States and surgeons' preference for immediate implant placement with ADM support. Abdominal-wall and hernia repairs remain steady, while synthetic meshes continue to dominate in low-risk cases.

Orthopedic and sports-medicine indications, rotator cuff and tendon repairs are gaining clinical acceptance, as studies show improved biomechanical outcomes. Dental and oral surgery maintains a small yet stable role, anchoring the long tail of the acellular dermal matrices market.

By End-User: Hospitals Lead, ASCs Accelerate

Hospitals generated 45.93% of demand in 2025 because high-acuity breast, burn, and complex hernia cases require multidisciplinary care. Ambulatory surgical centers are growing by 15.43% annually as payers steer low-risk hernia and soft-tissue repair cases to outpatient pathways. Specialty wound-care clinics prefer micronized formats that speed chairside application.

Research institutes, though modest in volume, shape product pipelines through IDE trials in 3-D printing and biosynthetic hybrids, feeding innovation that will influence the acellular dermal matrices market over the next decade.

Geography Analysis

North America accounted for 42.83% of global revenue in 2025, thanks to established CPT codes, dense tissue-bank networks, and high healthcare spending. The United States anchors regional demand with robust plastic-surgery volumes, whereas Canada’s single-payer model restricts coverage to high-risk cases. Mexico’s medical tourism corridors draw international patients, boosting regional demand for acellular dermal matrices.

Europe follows with diverse reimbursement policies. Germany’s statutory insurance covers ADM for contaminated wounds, but Southern European systems favor low-cost synthetics. EMA’s stringent ATMP framework prolongs launches, tilting the competitive field toward established suppliers. The United Kingdom’s NICE approves ADM for select wound and breast applications but questions cost-effectiveness in elective hernia repair, shaping cautious uptake.

Asia-Pacific is the fastest-growing region, with a 16.14% CAGR to 2031, propelled by China’s accelerated review timelines and India’s updated medical-device rules that shorten clearance cycles. South Korea and Thailand capitalize on medical tourism, with demand for premium biologics. Australia maintains high-quality standards aligned with FDA protocols, but public-sector budgets slow adoption. Japan pilots expedited regenerative-medicine pathways, yet cultural preference for autologous tissue tempers market expansion.

The Middle East, Africa, and South America contribute smaller shares. GCC investments in tertiary care are opening limited but profitable channels for ADM, while South Africa’s private-hospital segment is adopting premium products for cash-paying patients. Brazil’s expansive plastic-surgery market supports demand, yet currency volatility challenges pricing stability. Altogether, these regions represent emerging frontiers for the acellular dermal matrices market.

Competitive Landscape

The acellular dermal matrices market is moderately fragmented. The top five players, Integra LifeSciences, LifeNet Health, Organogenesis, MTF Biologics, and AlloSource, held roughly significant share in 2025. Each invests in automation, supercritical CO₂ processing, and gamma irradiation to shorten lead times and boost sterility assurance. Vertical integration through captive donor networks shields supply, while pre-hydrated and micronized formats cater to high-volume ambulatory sites.

Disruptors focus on niche needs. Companies like AlloSource target sports-medicine surgeons with higher suture-retention strength, and injectable paste makers pursue outpatient wound centers. Patent filings from 2024–2025 emphasize enzymatic decellularization and scaffold architectonics that improve cell infiltration. Regulatory strategy is critical: Section 361 pathways get products to market in 18 months, whereas Section 351 BLAs require multiyear trials but confer stronger exclusivity, influencing investment decisions.

Partnerships with hospital tissue banks are emerging as health systems seek to control costs. In-house processing agreements threaten the commercial supply chain while also presenting opportunities for OEM licensing. Biosynthetic hybrid developers courting synthetic mesh distributors could realign channel dynamics. Overall, innovation tempo and reimbursement negotiation skills will decide winners in the acellular dermal matrices market.

Acellular Dermal Matrices Industry Leaders

Smith & Nephew

Integra LifeSciences

MiMedx Group

Organogenesis Holdings

Baxter International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: AlloSource launched AlloMend HD for orthopedic soft-tissue repair, emphasizing enhanced suture retention.

- March 2025: First patient enrolled in MTF Biologics’ IDE trial evaluating FlexHD Pliable in pre-pectoral breast reconstruction.

- March 2025: BD treated the first patient in an IDE study of GalaFLEX LITE scaffold aimed at reducing capsular contracture in breast revision surgery.

- June 2024: MTF Biologics invested USD 25 million to triple injectable ADM output at its New Jersey facility, targeting chronic-wound clinics.

Global Acellular Dermal Matrices Market Report Scope

Acellular Dermal Matrices (ADMs) are biologic grafts or surgical tissue substitutes derived from human (allogenic) or animal (xenogenic, e.g., porcine or bovine) skin/dermis. They undergo a decellularization process that removes all cellular components (to minimize immune rejection and inflammation) while preserving the intact extracellular matrix (ECM), including collagen, elastin, glycosaminoglycans, laminin, fibronectin, and other structural proteins. This results in an acellular scaffold that supports tissue regeneration, cell repopulation, revascularization, and integration into the host tissue without triggering a significant inflammatory response.

The Acellular Dermal Matrices Market Report segments the market by source (Human, Animal, Synthetic & Biosynthetic, Autologous), product type (Freeze-dried Sheets, Pre-hydrated Sheets, Micronized/Injectable, Custom 3-D Printed Scaffolds), application (Breast Reconstruction, Chronic & Acute Wounds, Abdominal Wall & Hernia Repair, Orthopedic & Sports Medicine, Other Applications), end-user (Hospitals, Specialty Clinics & Wound-Care Centers, Ambulatory Surgical Centers, Research & Academic Institutes), and geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). All market forecasts are provided in terms of value (USD).

| Human |

| Animal |

| Synthetic & Biosynthetic |

| Autologous |

| Freeze-dried Sheets |

| Pre-hydrated Sheets |

| Micronized / Injectable |

| Custom 3-D Printed Scaffolds |

| Breast Reconstruction |

| Chronic & Acute Wounds |

| Abdominal Wall & Hernia Repair |

| Orthopedic & Sports Medicine |

| Other Applications (Dental & Oral Surgery, Plastic & Reconstructive Surgery, etc.) |

| Hospitals |

| Specialty Clinics & Wound-Care Centers |

| Ambulatory Surgical Centers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Human | |

| Animal | ||

| Synthetic & Biosynthetic | ||

| Autologous | ||

| By Product | Freeze-dried Sheets | |

| Pre-hydrated Sheets | ||

| Micronized / Injectable | ||

| Custom 3-D Printed Scaffolds | ||

| By Application | Breast Reconstruction | |

| Chronic & Acute Wounds | ||

| Abdominal Wall & Hernia Repair | ||

| Orthopedic & Sports Medicine | ||

| Other Applications (Dental & Oral Surgery, Plastic & Reconstructive Surgery, etc.) | ||

| By End-User | Hospitals | |

| Specialty Clinics & Wound-Care Centers | ||

| Ambulatory Surgical Centers | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the acellular dermal matrices market by 2031?

It is projected to reach USD 11.75 billion, expanding at a 12.29% CAGR.

Which source type currently holds the largest share in the acellular dermal matrices market?

Human-derived matrices led with 65.21% share in 2025.

Which application segment is growing the fastest through 2031?

Breast reconstruction is advancing at an 18.08% CAGR as mastectomy volumes rise.

Why are ambulatory surgical centers important for future ADM growth?

They are posting a 15.43% CAGR because payers shift low-risk hernia and soft-tissue repairs to outpatient pathways.

What key restraint could slow acellular dermal matrices adoption?

High product cost combined with inconsistent reimbursement is cutting 2.3 percentage points from projected CAGR.

Page last updated on: