Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

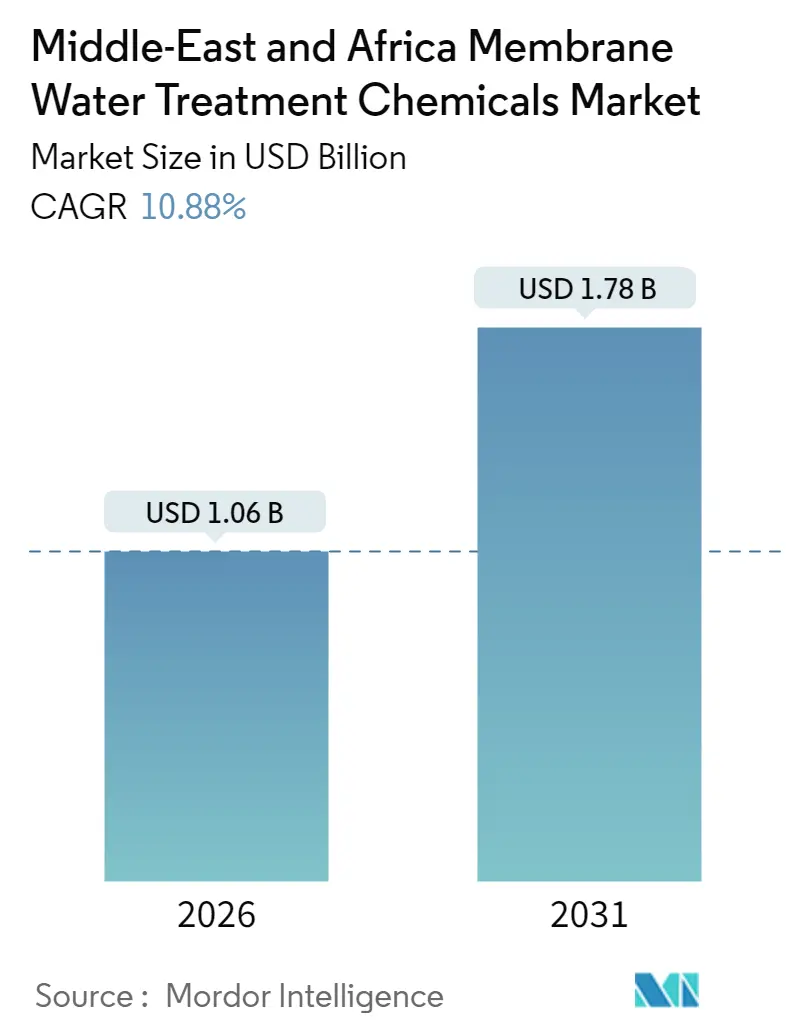

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 10.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Membrane Water Treatment Chemicals Market Analysis by Mordor Intelligence

The Middle East and Africa membrane water treatment chemicals market size in 2026 is estimated at USD 1.06 billion, growing from 2025 value of USD 0.96 billion with 2031 projections showing USD 1.78 billion, growing at 10.88% CAGR over 2026-2031. The membrane water treatment chemicals market is advancing because desalination construction has become integral to national water security plans, green hydrogen complexes require ultrapure feedwater, and utilities are under mandates to retrofit networks for potable reuse. Persistent feed-water salinity, tightening discharge regulations, and double-digit energy inflation have increased demand for coagulants, antiscalants, and smart dosing platforms that stabilize flux and curb chemical wastage. Suppliers are responding with biodegradable polycarboxylates, non-oxidizing biocides, and AI-enabled control technologies that, together, lower lifetime operating costs despite higher unit prices. Competitive intensity remains moderate because five to seven multinationals bundle proprietary chemistries with long-term service agreements, but localized specialists still win retrofit work in mid-sized municipal plants.

Key Report Takeaways

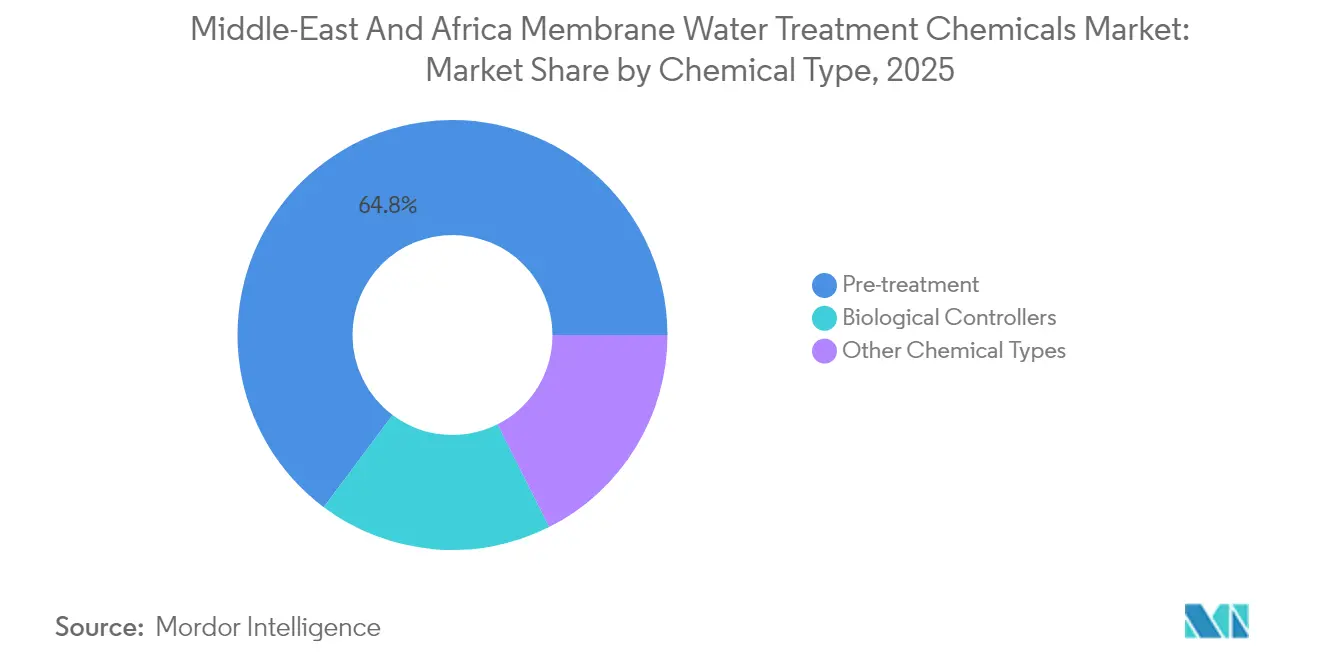

- By chemical type, pre-treatment products accounted for a 64.78% share of the membrane water treatment chemicals market in 2025 and are forecast to expand at an 11.05% CAGR through 2031.

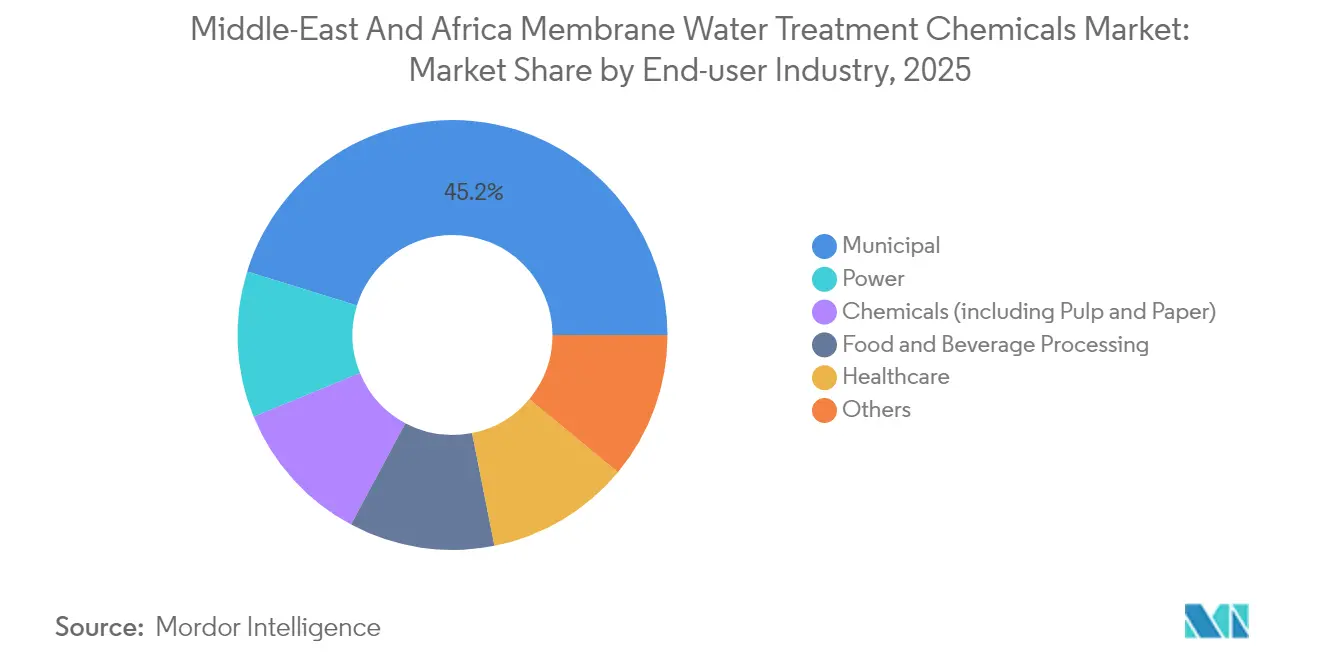

- By end-user industry, municipal applications accounted for 45.22% of the membrane water treatment chemicals market size in 2025 and are projected to advance at a 11.18% CAGR to 2031.

- By geography, Saudi Arabia captured 19.18% of the Middle East and Africa membrane water treatment chemicals market size in 2025 and is set to expand at a 10.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle-East And Africa Membrane Water Treatment Chemicals Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing freshwater-scarcity-driven desalination build-out | +3.2% | GCC core, Egypt, North Africa | Medium term (2-4 years) |

| Regulatory push for potable reuse and industrial zero-liquid-discharge | +2.1% | Saudi Arabia, UAE, South Africa | Long term (≥ 4 years) |

| Rapid municipal and industrial infrastructure expansion | +2.5% | Egypt, Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Consolidation of GCC hydrogen and ammonia projects needing ultrapure water | +1.8% | Saudi Arabia, UAE | Medium term (2-4 years) |

| AI-enabled chemical-dosing optimisation improving ROI | +1.0% | GCC, South Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Freshwater-Scarcity-Driven Desalination Build-Out

Chronic water stress has prompted governments to invest in large reverse-osmosis plants, making desalination the single largest growth engine for the membrane water treatment chemicals market. Saudi Arabia alone plans to add 8.4 million m³/day of new capacity by 2030, resulting in an annual demand of 12,000 tonnes for antiscalants and biocides. The Taweelah expansion in the United Arab Emirates adds 909,000 m³/day and relies on coagulant–flocculant sequences to cut turbidity below 0.5 NTU before membranes. Qatar’s North Field LNG trains utilize polyaluminum chloride and cationic polymers to strip colloidal silica, which otherwise halves the membrane life[1]QatarEnergy, “North Field expansion water strategy,” QatarEnergy, qatareenergy.qa . Contract structures have shifted toward 10- to 20-year chemical supply agreements that bundle dosing equipment and performance guarantees, locking in visibility for suppliers that can co-invest in inventory and field service. These developments embed the membrane water treatment chemicals market phrase deeply in operator procurement strategies.

Regulatory Push for Potable Reuse and Industrial Zero-Liquid-Discharge

New discharge rules now require utilities and industries to meet stringent quality targets that only membrane trains can achieve, thereby increasing chemical demand. Saudi Arabia requires effluent meant for irrigation to contain <1,500 mg/L TDS and <10 mg/L BOD, thresholds met through ultrafiltration or reverse osmosis preceded by robust biological control. The UAE’s Federal Law 24 caps brine salinity at 70,000 mg/L and bans specific halogenated biocides in coastal zones, driving a switch to isothiazolinones that cost up to 30% more but degrade within 48 h. South Africa is piloting zero-liquid-discharge mandates in mining; membrane stages in these systems double antiscalant use because supersaturation spikes increase scaling propensity, as reported by. Project lenders now require ISO 14001-certified formulations, favoring suppliers with transparent safety data and documented biodegradability.

Rapid Municipal and Industrial Infrastructure Expansion

Fast-growing cities and industrial zones have created a backlog of treatment-plant upgrades that rely on membranes and, by extension, chemicals. Egypt’s New Administrative Capital awarded a 250,000 m³/day membrane bioreactor that demands continuous biocide dosing to suppress hollow-fiber biofilm. Petrochemical complexes in Jubail and Yanbu recycle cooling-tower blowdown through nanofiltration, consuming scale inhibitors at rates directly tied to concentration cycles. Procurement cycles are becoming shorter, so EPC contractors are insisting on pre-qualified chemical vendors that can guarantee just-in-time deliveries, thereby reinforcing volumes within the membrane water treatment chemicals market.

Consolidation of GCC Hydrogen and Ammonia Projects Needing Ultrapure Water

Mega-projects such as NEOM’s green-hydrogen complex require feedwater with conductivity below 1 µS/cm, necessitating three-stage trains of ultrafiltration, reverse osmosis, and electrodeionization that together consume specialized antiscalants and resin regenerants. The Ras Al-Khair hydrogen hub and the Khalifa Industrial Zone ammonia plant utilize contracts that stipulate a maximum annual decline in membrane flux of 5%, prompting operators to pay premiums of 40-50% for high-performance chemicals. Suppliers are formulating phosphonate-free antiscalants to prevent proton-exchange membrane contamination, and they station technical experts on-site to recalibrate dosing as seawater salinity levels fluctuate. These requirements give the membrane water treatment chemicals market an additional growth vector and raise entry barriers for suppliers without ultrapure-water credentials.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs of membrane plants | -1.5% | Egypt, South Africa, and smaller GCC municipalities | Short term (≤ 2 years) |

| Tightening discharge rules for hazardous actives | -0.9% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Supply-chain shocks in specialty polymer/phosphonate inputs | -0.7% | Region-wide, acute in Egypt & South Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs of Membrane Plants

Upfront investment for reverse-osmosis or ultrafiltration facilities often deters utilities in price-sensitive regions, especially once chemical consumption is factored into life-cycle budgets. Municipalities in Egypt’s Nile Delta and South Africa’s Eastern Cape have postponed tenders because projected tariffs exceed affordable thresholds even with concessional finance. Petrochemical users transitioning to zero-liquid-discharge systems see water-treatment costs increase from USD 0.40/m³ for once-through cooling to USD 2.80/m³ for closed-loop membrane systems, compressing margins in commodity markets. Accelerated fouling increases the frequency of membrane replacement, doubling annualized capital-recovery charges when chemical dosing is sub-optimal.

Tightening Discharge Rules for Hazardous Actives

Environmental agencies are implementing stricter limits on phosphonate antiscalants and halogenated biocides, citing risks to marine ecosystems. Saudi Arabia plans to ban certain organobromine biocides by 2027, forcing operators to switch to hydrogen peroxide or peracetic acid, which cost 30-40% more and require stainless-steel piping. The UAE caps phosphorus at 1 mg/L in coastal discharges, so plants switch to polycarboxylate inhibitors that are less efficient and require higher doses. Qatar’s quarterly toxicity-testing mandate adds a USD 50,000-100,000 annual compliance cost. These changes compress margins for legacy chemistries and slow decisions in the membrane water treatment chemicals market.

Segment Analysis

By Chemical Type: Pre-Treatment Dominance Anchored in Fouling Prevention

Pre-treatment products held 64.78% of 2025 revenue and are on track to grow 11.05% annually to 2031, sustaining clear leadership within the membrane water treatment chemicals market size for this category. Coagulants and flocculants agglomerate suspended solids to push turbidity below 1 NTU and maintain flux above 20 L/m²·h, while phosphonate antiscalants inhibit carbonate, sulfate, and silica precipitation even in Gulf seawater, where scaling potential is quadruple that of Atlantic sources. Biocides prevent biofilm formation, which would otherwise reduce permeability by 30% within weeks. Growth is amplified by the adoption of ultrafiltration ahead of reverse osmosis, adding a second layer of chemical demand.

Anticipated regulatory shifts toward biodegradable formulations may lift average selling prices 20-30%, but operators consider the premium justified because warranty terms void coverage if approved chemistries are not used. AI-based dosing platforms are increasingly bundling these pre-treatment chemicals within long-term service contracts, locking in volumes and thereby elevating switching costs. Biological controllers form a smaller yet rapidly expanding niche as membrane bioreactors scale up in municipal wastewater. Maintenance-oriented cleaners such as citric-acid and EDTA solutions restore flux during periodic clean-in-place procedures, ensuring that the membrane water treatment chemicals market remains structurally tied to robust pre-treatment regimes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Municipal Leadership Driven by Reuse Mandates

Municipal utilities commanded 45.22% of demand in 2025 and will rise at an 11.18% CAGR, retaining the largest slice of the membrane water treatment chemicals market share through 2031. Saudi Arabia’s National Water Company operates 5.6 million m³/day of desalination and has tendered 12 new plants under Vision 2030, each with multi-year chemical supply requirements benchmarked to their respective throughputs. South Africa’s metro reuse projects combine ultrafiltration, reverse osmosis, and UV, consuming chemicals at every barrier to hit Department of Water and Sanitation limits.

Power generation follows, driven by boiler feed demineralization and the recycling of cooling tower blowdown. Food and beverage processors need water below 500 mg/L TDS and 100 CFU/mL microbes, achievable only through membrane trains fed by high-purity chemicals. Healthcare sites, notably dialysis centers, require pharmaceutical-grade water, making them small but high-margin customers. Chemical and petrochemical complexes are installing zero-liquid-discharge double membrane-stage systems to reduce consumption because brine concentration accelerates scaling. Mining, textiles, and electronics add fragmented yet rising volumes as tariffs rise and compliance pressure intensifies, bolstering the long-term prospects for the membrane water treatment chemicals market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Saudi Arabia accounted for a 19.18% share of the Middle East and Africa membrane water treatment chemicals market revenue in 2025 and is expected to increase by 10.95% annually to 2031, underpinned by 8.4 million m³/day of planned desalination and a surge in green hydrogen and petrochemical capacity. Saudi Arabia's Vision 2030 mandates zero-liquid-discharge in Jubail and Yanbu, elevating demand for high-performance scale inhibitors and cleaners. Long-term service contracts, such as Veolia’s 25-year Jubail deal, tighten supplier lock-in.

The United Arab Emirates and Qatar are experiencing a growing demand for membrane water treatment chemicals due to the increasing number of water treatment projects. Abu Dhabi’s Taweelah unit added 909,000 m³/day in 2024, while QatarEnergy’s LNG trains require ultrafiltration ahead of high-pressure boilers. Dubai aims to achieve 100% wastewater recycling by 2030, upgrading eight plants with membrane bioreactors that utilize biocides and cleaners at a rate 1.5 times that of activated sludge systems. Qatar’s Ashghal has 12 wastewater expansion projects in tender, each incorporating citric acid and sodium hydroxide clean-in-place protocols every 90 days. Willingness to pay for reliability is high; AI-enabled dosing shows 15-20% chemical savings and 10-15% life extensions.

Egypt and South Africa form the second tier. Egypt targets 8.85 million m³/day desalination by 2050, with phase-one plants set to double current import volumes for pre-treatment chemicals, but tariff reforms remain politically sensitive. South Africa’s ports authority installed desalination at Durban and Saldanha Bay to secure industrial supply and specifies maximum annual flux decline of 5%, thereby demanding precise dosing. The market growth in Rest of Middle East and Africa—including Jordan, Oman, Kenya, and Nigeria is fueled by donor-funded water projects and industrial investments. Jordan’s wastewater-reuse program recycles 90% of effluent for agriculture, relying on ultrafiltration and reverse osmosis that consume antiscalants and biocides proportional to 1,200 mg/L average salinity.

Competitive Landscape

The Middle East and Africa membrane water treatment chemicals market is moderately consolidated, with major players such as Ecolab and Kemira having chemical-dosing contracts. They leverage proprietary formulations, dosing equipment, and cloud analytics to secure long-term agreements and co-invest in field service labs, giving them scale and data that smaller rivals cannot match. White-space opportunities abound in green-label chemistries that meet tighter discharge rules, ultrapure formulations for hydrogen and semiconductors, and software that integrates chemical dosing into broader plant automation. Regional specialists compete on price and local support, winning aftermarket work where multinationals’ order thresholds exclude mid-sized utilities. As digital platforms and backward integration demand higher capital outlays, the field is likely to consolidate further, with smaller firms becoming toll blenders for larger groups, reinforcing existing share patterns within the membrane water treatment chemicals market.

Middle-East And Africa Membrane Water Treatment Chemicals Industry Leaders

Ecolab

Kurita Water Industries Ltd

Solenis

Kemira

Dow

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Dow committed USD 150 million to expand FilmTec membrane and antiscalant manufacturing in Jubail, adding 20 million m² of membrane and 15,000 t of chemical capacity by 2027.

- March 2025: Italmatch Chemicals secured ISO 14001 certification for phosphonate-free antiscalants that meet UAE discharge limits, focusing on Abu Dhabi and Dubai users.

Middle-East And Africa Membrane Water Treatment Chemicals Market Report Scope

Membrane water treatment chemicals serve as barriers in water treatment, allowing water to flow through while preventing undesired contaminants from doing so. The market is segmented by chemical type, end-user industry, and geography. By chemical types the market is segmented into pre-treatment, biological controllers, and other chemical types. By end-user industry, the market is segmented into food and beverage processing, healthcare, municipal, chemicals (including pulp and paper) power, and other end-user industries. By geography, the report provides market estimates and forecasts for Saudi Arabia, United Arab Emirates, Qatar, South Africa, Egypt, and the Rest of the Middle East and Africa. The report offers the market size and forecasts in revenue (USD) for all the above segments.

By Chemical Type

| Pre-treatment |

| Biological Controllers |

| Other Chemical Types |

By End-user Industry

| Food and Beverage Processing |

| Healthcare |

| Municipal |

| Chemicals (including Pulp and Paper) |

| Power |

| Others |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| South Africa |

| Egypt |

| Rest of Middle East and Africa |

| By Chemical Type | Pre-treatment |

| Biological Controllers | |

| Other Chemical Types | |

| By End-user Industry | Food and Beverage Processing |

| Healthcare | |

| Municipal | |

| Chemicals (including Pulp and Paper) | |

| Power | |

| Others | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is demand for membrane chemicals growing in the Gulf?

Regional consumption is increasing at a 10.88% CAGR, driven by desalination build-outs and potable reuse mandates.

Which chemical segment leads in spending?

Pre-treatment products account for 64.78% of 2025 revenue, due to their essential role in fouling prevention.

Why are utilities adopting AI-enabled dosing?

Platforms such as 3D TRASAR lower chemical and energy costs by 15-20% while extending membrane life by roughly a year.

What regulatory shifts influence product choices?

Saudi and UAE regulations restrict phosphonates and halogenated actives, prompting operators to shift toward biodegradable polycarboxylates and non-oxidizing biocides.

Which country offers the largest growth opportunity?

Saudi Arabia, with 8.4 million m³/day of new desalination capacity, is expected to add 18,000-20,000 t/year of chemical demand by 2030.

How concentrated is supplier power?

The Middle East and Africa membrane water treatment chemicals market is moderately consolidated.

What is the current market size for Middle East and Africa Membrane Water Treatment Chemicals Market?

The Middle East and Africa membrane water treatment chemicals market size is estimated at USD 1.06 billion in 2026 and is expected to reach USD 1.78 billion by 2031, at a CAGR of 10.88% during the forecast period (2026-2031).