Executive Summary

The January 2026 EU-India FTA eliminates 90%+ of tariffs across agriculture, food & beverage, and FMCG sectors, creating the EU's deepest agricultural market access in India to date. Wine tariffs drop from 150% to 20-30%; spirits to 40%. Indian fisheries, organics, and specialty foods gain streamlined EU access.

Key Implications: First-mover advantage window appears to be 18-24 months. Regulatory compliance costs may offset tariff savings for smaller players. Dairy and cereals remain protected. Infrastructure gaps persist.

Our Analysis Suggests: Premium differentiation and sustainability positioning will likely separate early winners from commodity players, though execution risk remains elevated through 2027.

The Macro Context

On January 27, 2026, the EU-India free trade agreement was finalized- what European Commission President Ursula von der Leyen called the, "Mother of All Deals." The agreement represents the most comprehensive agricultural market access India has granted to date, covering nearly 2 billion people and approximately 25% of global GDP.

For food, beverage, and FMCG companies, the deal's tariff eliminations create genuine market entry opportunities, though infrastructure gaps and regulatory execution will determine the pace of actual market transformation.

Understanding the Scale of EU India Trade Deal

- Combined population: 2 billion people

- Global GDP coverage: ~25%

- Current bilateral trade (2024-2025): USD 136.5 billion

- Target by 2030: USD 200 billion

- Tariff coverage: 90%+ of goods traded

- Expected EU export growth by 2032: Double

The Agriculture & Agri-Food Opportunity

Breaking Down Tariff Reductions for EU Exporters

Agriculture has historically been the most contentious area in EU-India trade. Indian tariffs on agri-food products averaged 36% and could reach as high as 150%, effectively shutting out European exporters. Current EU agri-food exports to India stand at just EUR 1.3 billion (USD 1.5 billion), a mere 0.6% of the EU's global agri-food trade.

That's about to change.

We're beginning to see structural shifts in market access dynamics, though the pace will depend heavily on logistics infrastructure and regulatory execution.

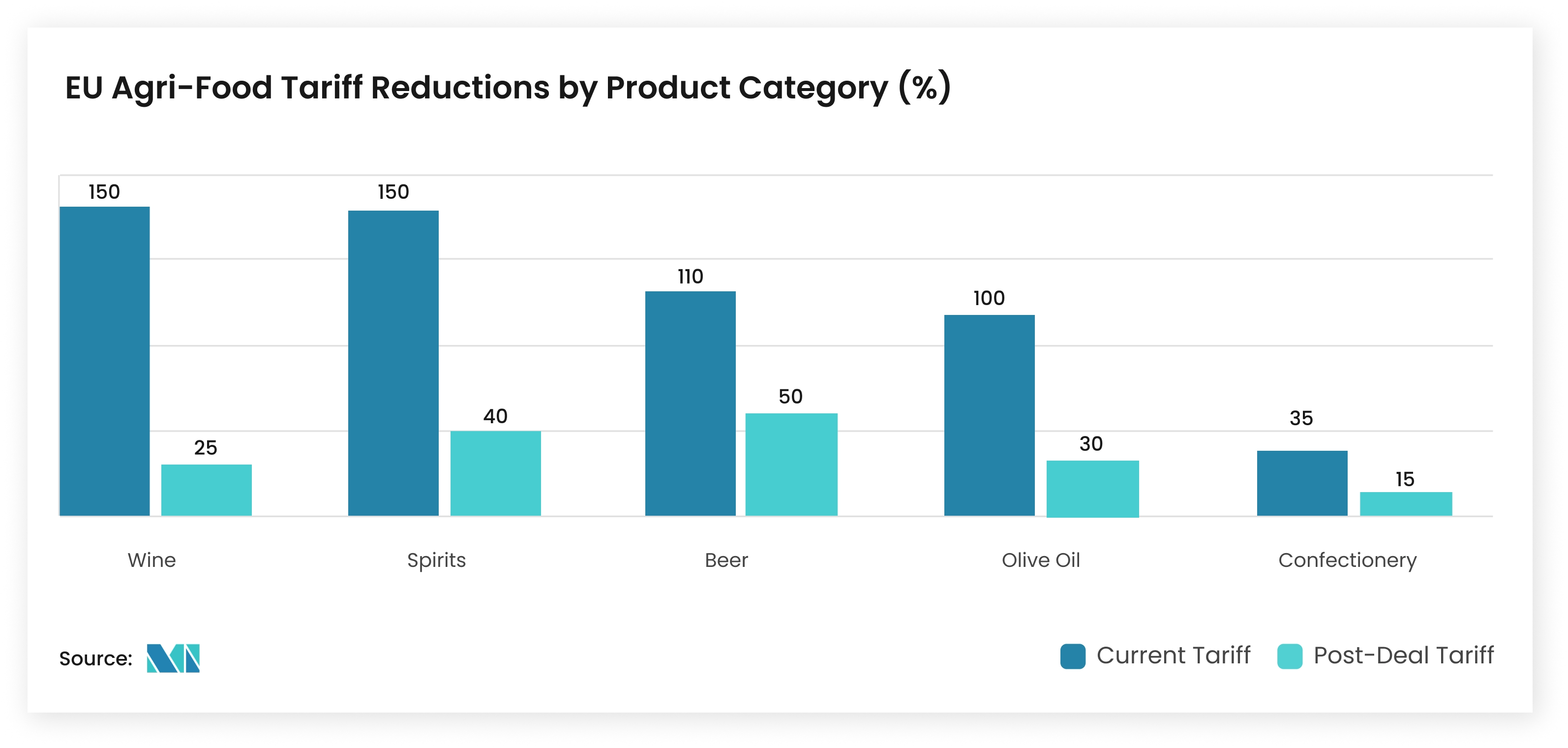

Tariff Reductions for Key EU Agri-Food Categories

| Product Category | Current Tariff | Post-Deal Tariff | Reduction |

| Wine | 150% | 20-30% (premium wines) | Up to 130 percentage points |

| Spirits/Liqueurs | Up to 150% | 40% (flat rate) | Up to 110 percentage points |

| Beer | 110% | 50% | 60 percentage points |

| Olive Oil | Prohibitive | Significantly reduced | TBD on specifics |

| Confectionery | 30-40% | Substantially reduced | TBD on specifics |

| Cheese & Dairy* | Protected | Protected | NO CHANGE |

| Cereals & Grains* | Protected | Protected | NO CHANGE |

Source: Mordor Intelligence

EU Agri-Food Tariff Reductions by Product Category (%)

| Name | Current Tariff | Post-Deal Tariff |

| Wine | 150 | 25 |

| Spirits | 150 | 40 |

| Beer | 110 | 50 |

| Olive Oil | 100 | 30 |

| Confectionery | 35 | 15 |

Source: Mordor Intelligence

What This Means for EU Food Exporters

The free trade agreement grants the EU its highest level of market access to India compared to any other trade partner, including recent agreements with the UK and Australia. This appears to represent a first-mover advantage for European companies in premium agri-food categories, pending successful navigation of regulatory requirements and distribution network establishment.

1. Beverages Sector: Early Indicators of Transformation

The wine and spirits sectors stand to see transformational growth. European producers have long eyed India's growing affluent consumer segment. With tariffs dropping from 150% to 20-40%, price competitiveness fundamentally shifts.

Beyond wine, the tariff reset on spirits and liqueurs alters long-term category economics, with implications for portfolio mix, brand strategy, and route-to-market dynamics across the Alcoholic Beverages Market.

As price barriers ease, European wine producers are better positioned to expand distribution and premium penetration in India, particularly in mid- to high-end categories across the Europe Wine Market.

2. Critical Safeguards: What Remains Protected

The EU successfully protected its most sensitive agricultural sectors, including beef, chicken, rice, sugar, honey, milk powders, bananas, and soft wheat. Quotas limit imports of products like table grapes and cucumbers.

This balance of th ndia trade deal reflects both parties' domestic agricultural priorities while still opening substantial market access, a political necessity that shapes the deal's practical boundaries.

3. Food Safety Standards Maintained

The EU's stringent sanitary and phytosanitary (SPS) standards are fully maintained with no exceptions. Audits and border controls on imported food and animal products will be reinforced, with inspections focusing on pesticide residues and animal welfare compliance.

Implications For Indian Food & Agri-Exporters

Gaining Competitive Advantage in the EU Market

While the EU gains the most headlines for agricultural access, Indian food and agricultural exporters benefit from their own set of tariff reductions and improved market positioning.

Indian Sectors Set to Gain (from the 2026 EU-India free trade agreement):

- Fisheries and Marine Products: Reduced tariffs on processed seafood.

- Organic Chemicals: Food-grade and agricultural inputs.

- Pharmaceutical Ingredients: Used in food production and supplements.

- Value-added Agricultural Products: Organic, sustainably-sourced, and artisanal foods.

These shifts are particularly relevant for exporters targeting premium and sustainability-led demand pockets across the Europe Organic Food and Beverages Market.

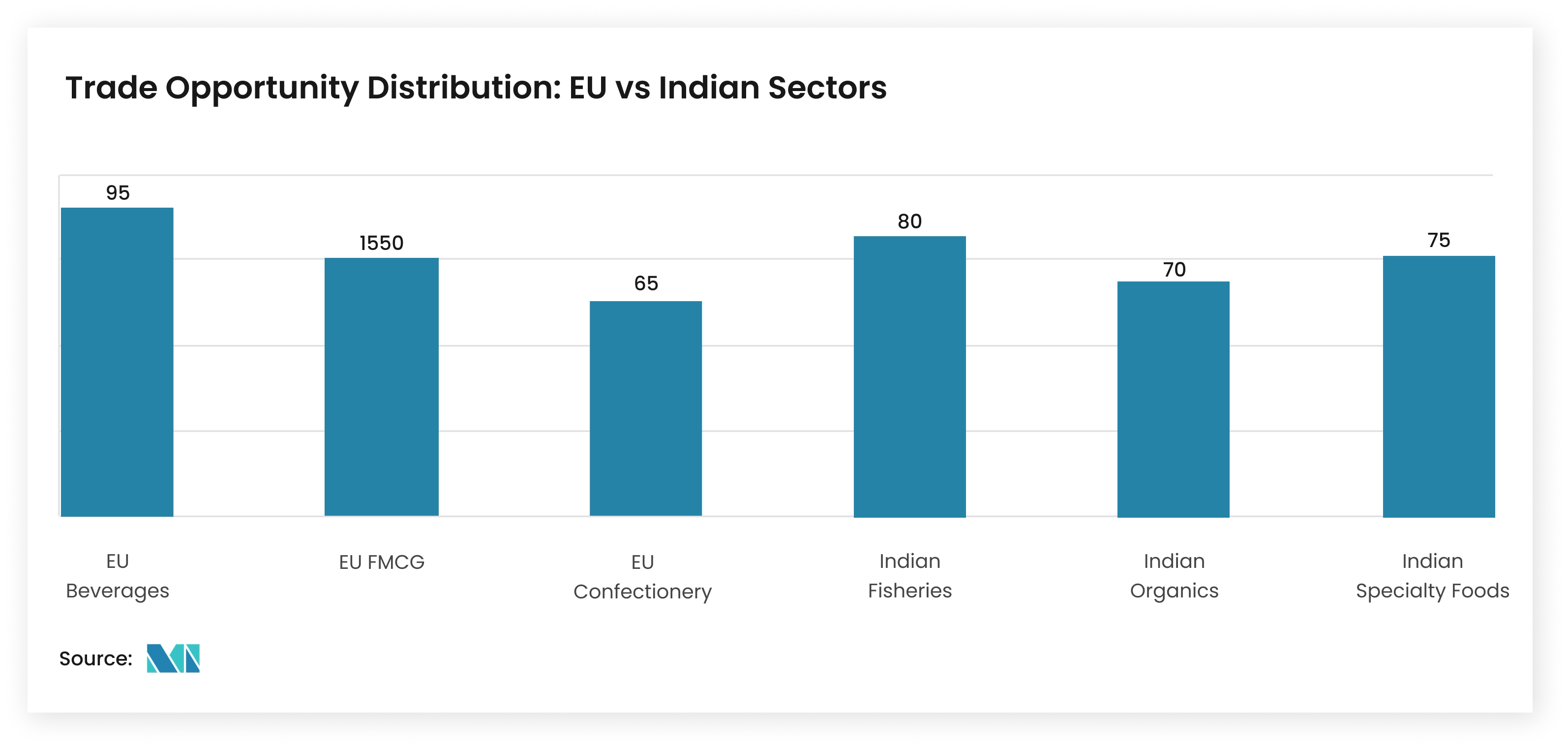

Trade Opportunity Distribution: EU vs. Indian Sectors

| Name | Opportunity Score |

| EU Beverages | 95 |

| EU FMCG | 75 |

| EU Confectionery | 65 |

| Indian Fisheries | 80 |

| Indian Organics | 70 |

| Indian Specialty Foods | 75 |

Source: Mordor Intelligence

FMCG & Consumer Goods Implications

The Broader Consumer Products Landscape

While specific FMCG product tariff details vary, the deal's impact on this sector is multi dimensional.

As import friction declines, ready-to-drink formats stand to benefit from faster market entry and evolving urban consumption patterns, particularly within the Europe Ready-to-Drink Beverages Market.

Timeline - Deal Implementation Roadmap 2026-2032

- Q1 2026: Expected agreement entry into force.

- 2026-2028: Immediate tariff eliminations on 90%+ goods.

- 2028-2032: Phased reductions on sensitive sectors (notably automobiles, with tariffs declining from 110% to 10%).

- 2032: EU aims to double exports to India.

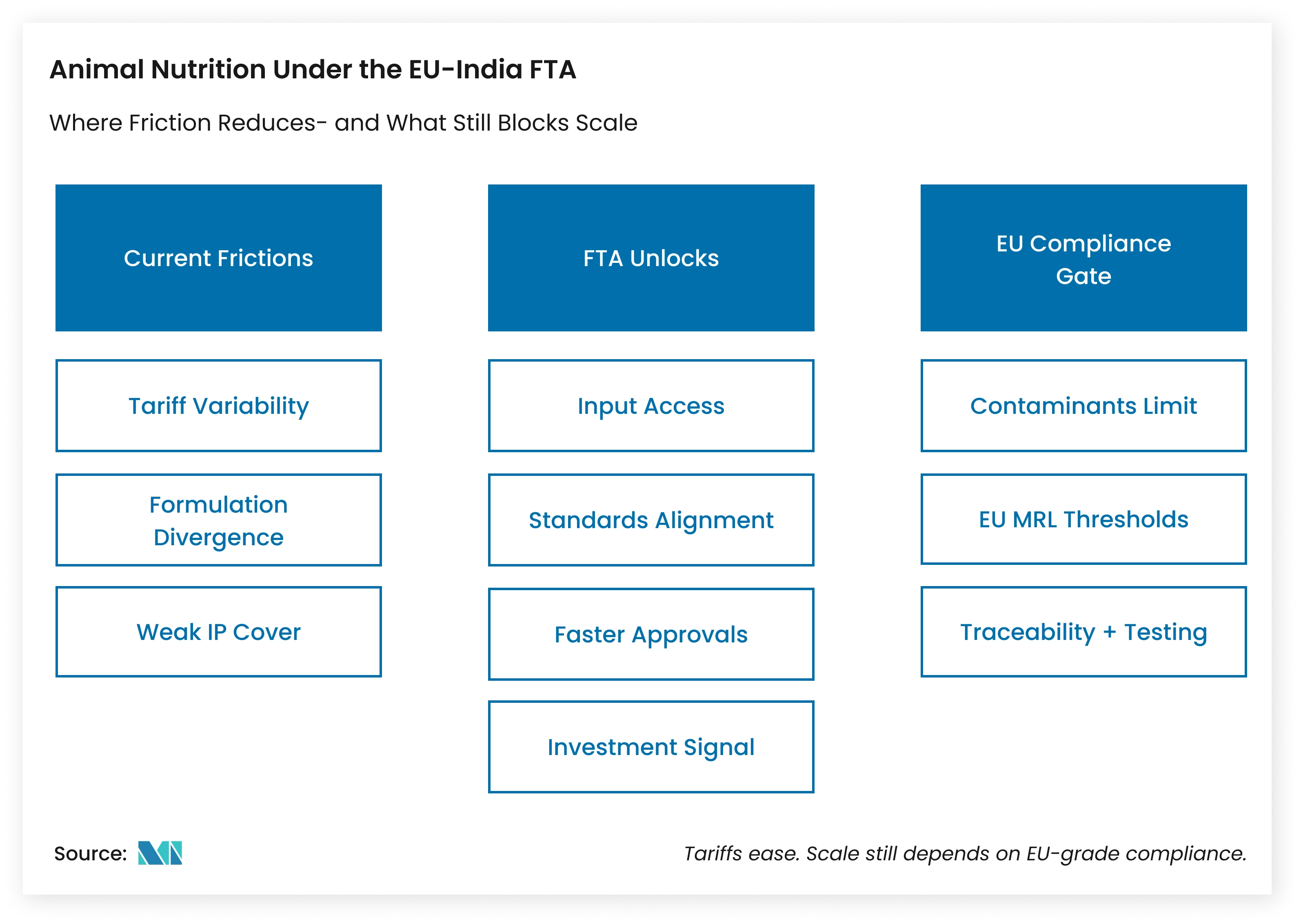

Animal Nutrition Sector Focus

Opportunities in Feed Ingredients and Supplements

The animal nutrition sector occupies a unique position in this agreement.

1. Current State

India is a significant producer of animal feed ingredients, fish meal, and protein supplements, but trade has been constrained by:

- Variable tariffs on animal-derived and plant-based feed ingredients.

- Regulatory divergence on supplement formulations.

- Limited IP protection for specialized feed additives.

2. Post-Deal Opportunities

- Ingredient Access: Reduced tariffs on chemical and organic ingredients used in animal feed formulations benefit both EU and Indian feed manufacturers.

- Standardization Benefits: The IP chapter and standards harmonization reduce compliance costs for feed ingredient exporters.

- Regulatory Alignment: Working groups on food safety and standards will facilitate faster approvals for feed additives and supplements.

- Investment: Enhanced trade certainty encourages production facility investments on both sides.

Structural Advantages & Strategic Considerations

What Makes This Deal Different?

- Rules of Origin: The free trade agreement includes carefully calibrated rules of origin, aligned with recent EU FTAs. These ensure that only products significantly processed within India or the EU can benefit from tariff preferences, protecting both regions from trans-shipment and encouraging genuine value addition. For food and agricultural products, this means companies cannot simply re-export imported goods; they must conduct meaningful processing or manufacturing.

- Self-Certification Advantage: Documentation is based on self-certification by businesses (following the latest WTO standards), making it easier, especially for small and medium-sized companies, to benefit from tariff reductions. This democratizes access and supports emerging food and FMCG brands.

- Sustainability Integration: The EU-India FTA commits both sides to renewable energy promotion, emission reductions in maritime sectors, and circular economy principles. This creates opportunities for sustainable agriculture and eco-friendly FMCG practices to gain preferential treatment.

This Deal vs. India's Other Major FTAs

| Agreement | Agricultural Market Access |

| EU–India FTA (2026) | Highest access granted |

| India–UK FTA (2022) | Moderate access |

| India–Australia FTA (2022) | Moderate access |

| RCEP (2020) | Limited to select sectors |

Source: Mordor Intelligence

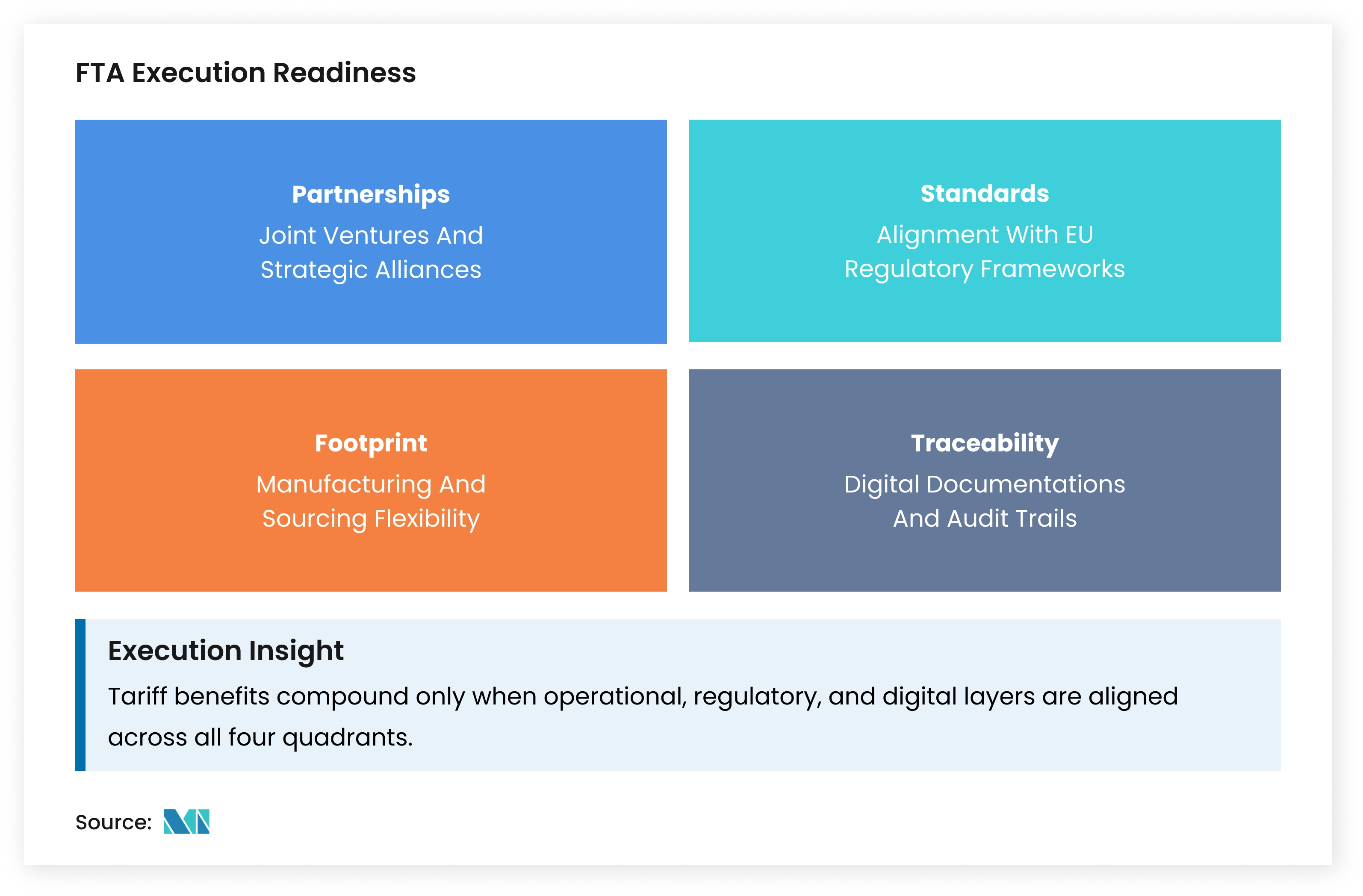

Sector-Specific Actions & Recommendations

- Supply Chain Optimization: Review manufacturing footprint, tariff reductions may make local sourcing more competitive.

- Standard Harmonization: Begin aligning product formulations with partner region's regulatory requirements.

- Strategic Partnerships: Explore joint ventures and partnerships to establish manufacturing or distribution presence.

- Technology Investment: Invest in traceability and documentation systems to ensure rules of origin compliance.

Risks & Challenges To Watch

- Regulatory Hurdles: EU food safety standards, while aligned, remain exceptionally stringent. Compliance costs may offset tariff savings for some Indian producers, particularly smaller operations.

- Logistics & Infrastructure: Current logistics costs between India and the EU remain high. While tariff reductions are immediate, infrastructure improvements and supply chain optimization take time.

- Currency Volatility: Trade between India (Rupees) and EU (Euros) is exposed to exchange rate fluctuations. The rupee's recent weakness adds cost for Indian importers of EU goods.

- Domestic Politics: India and the EU each have domestic stakeholders who opposed aspects of the deal. Implementation and enforcement of the agreement's provisions may face political pressure on both sides.

- Exclusions Create Gaps: Dairy, cereals, and key agricultural products remain off-limits as a part of this EU India trade deal. For some sectors, tariffs remain moderately high despite reductions, limiting immediate transformation. Dairy remains largely excluded from tariff liberalization, meaning competitive dynamics and market access constraints across the Dairy Products Market remain structurally unchanged under the agreement.

Global Context & Outlook

The Real Opportunity

The EU-India FTA is genuine transformational opportunity, not just for large multinationals but for mid-market food and beverage companies, emerging FMCG brands, and specialized animal nutrition producers on both sides.

For European companies, India represents a market of 1.5 billion people with a rapidly expanding middle class. Tariff barriers that once made premium European foods economic non-starters are now manageable. The first-mover advantage is real but time-limited; competitors in other jurisdictions will follow.

For Indian exporters, the EU represents the world's most sophisticated and affluent consumer market. Quality standards are demanding, but the price is market access and premium positioning. The window for brand building is now open.

The commodity game, however, remains unchanged. Basic agricultural products face lower margins regardless of tariff reductions. Success belongs to companies that can differentiate, through quality, sustainability, branding, and innovation.

The timeline is now. The agreement comes into force in 2026. Early movers will establish distribution networks, build regulatory relationships, and capture market share before the landscape stabilizes. Those who wait risk finding mature competition where first-mover advantages once existed.

Want deeper insights on how the EU–India FTA is redefining market access and competitive dynamics in agriculture, food, and FMCG? Explore our latest Food, Beverages and Agriculture reports.