Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

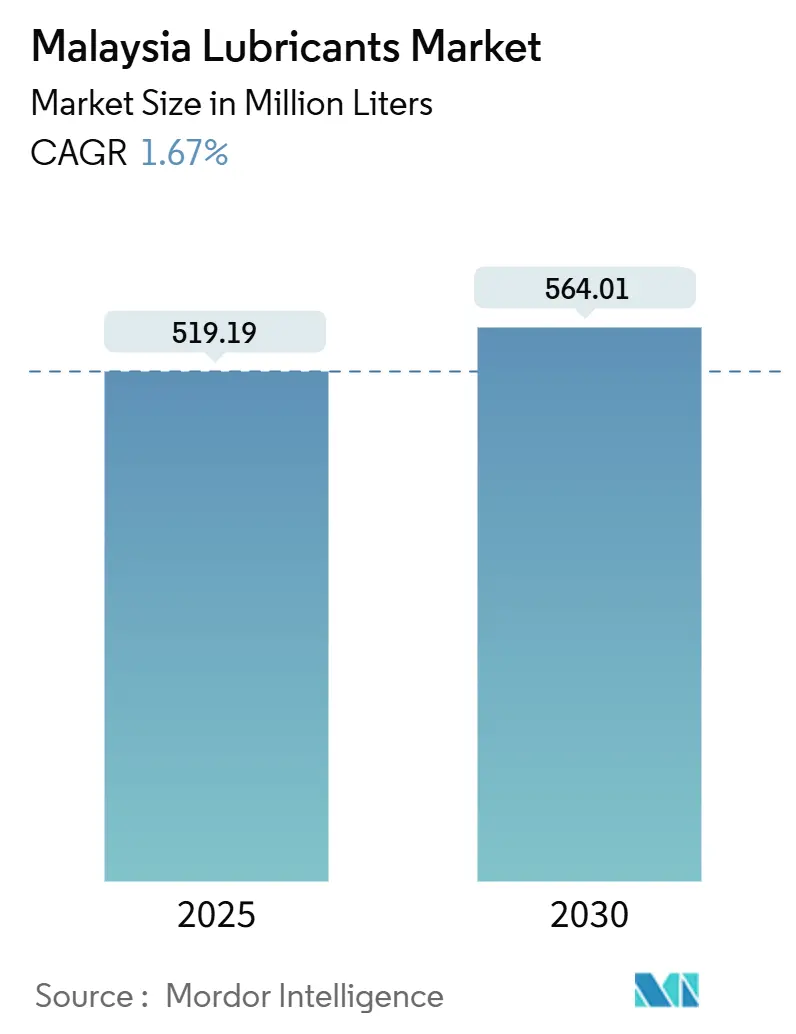

| Market Volume (2025) | 519.19 Million liters |

| Market Volume (2030) | 564.01 Million liters |

| Growth Rate (2025 - 2030) | 1.67% CAGR |

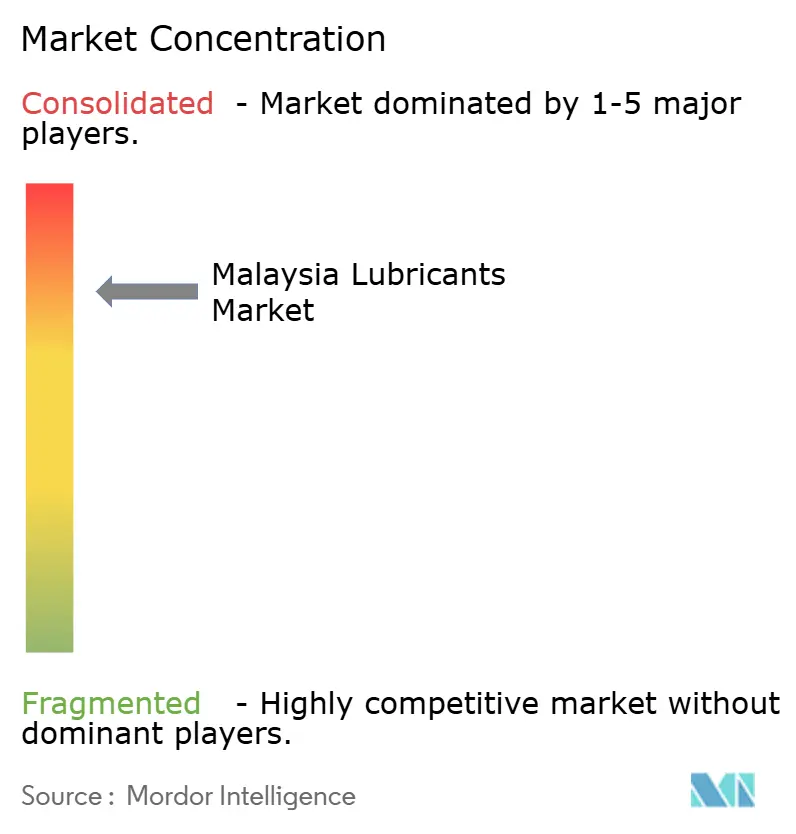

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malaysia Lubricants Market Analysis by Mordor Intelligence

The Malaysia Lubricants Market size is estimated at 519.19 million liters in 2025, and is expected to reach 564.01 million liters by 2030, at a CAGR of 1.67% during the forecast period (2025-2030). Growth remains steady rather than spectacular because the market is already mature, yet it benefits from a wider vehicle parc, new manufacturing capacity, and infrastructure spending that require dependable fluid performance. Passenger cars dominate the national fleet, making Malaysia the only ASEAN country where four-wheelers outnumber two-wheelers, which lifts demand for premium engine oils. Government execution of the 12th Malaysia Plan and the National Industrial Master Plan 2030 (NIMP 2030) adds incremental volume in industrial, construction, and high-tech manufacturing applications. Meanwhile, the electric-vehicle (EV) rollout, longer drain intervals, and rising equipment efficiency limit total volume growth, prompting suppliers to shift toward higher-value synthetic and specialty formulations rather than bulk mineral grades.

Key Report Takeaways

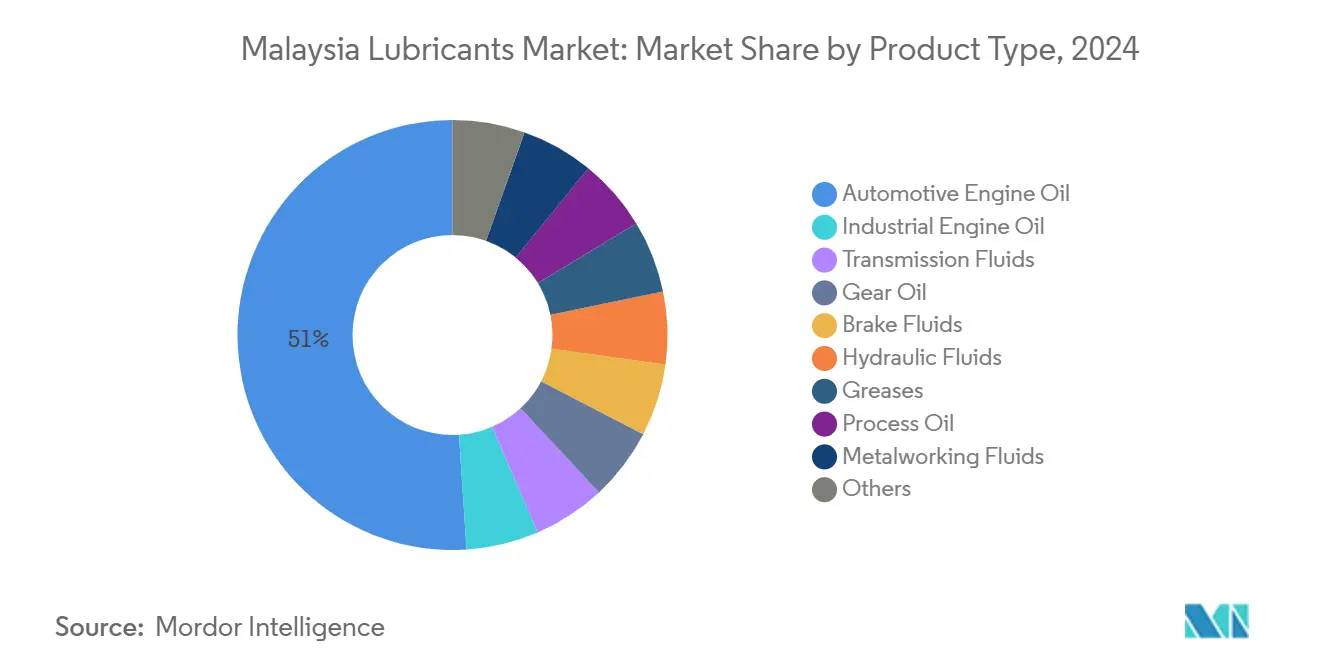

- By product type, automotive engine oil accounted for 51.05% of Malaysia's lubricants market share in 2024. Transmission fluids are projected to experience the fastest product-level expansion, at a 2.55% CAGR, between 2025 and 2030.

- By end-user industry, the automotive segment led with 70.13% revenue share in 2024, while industrial applications are forecast to expand at a 2.92% CAGR through 2030.

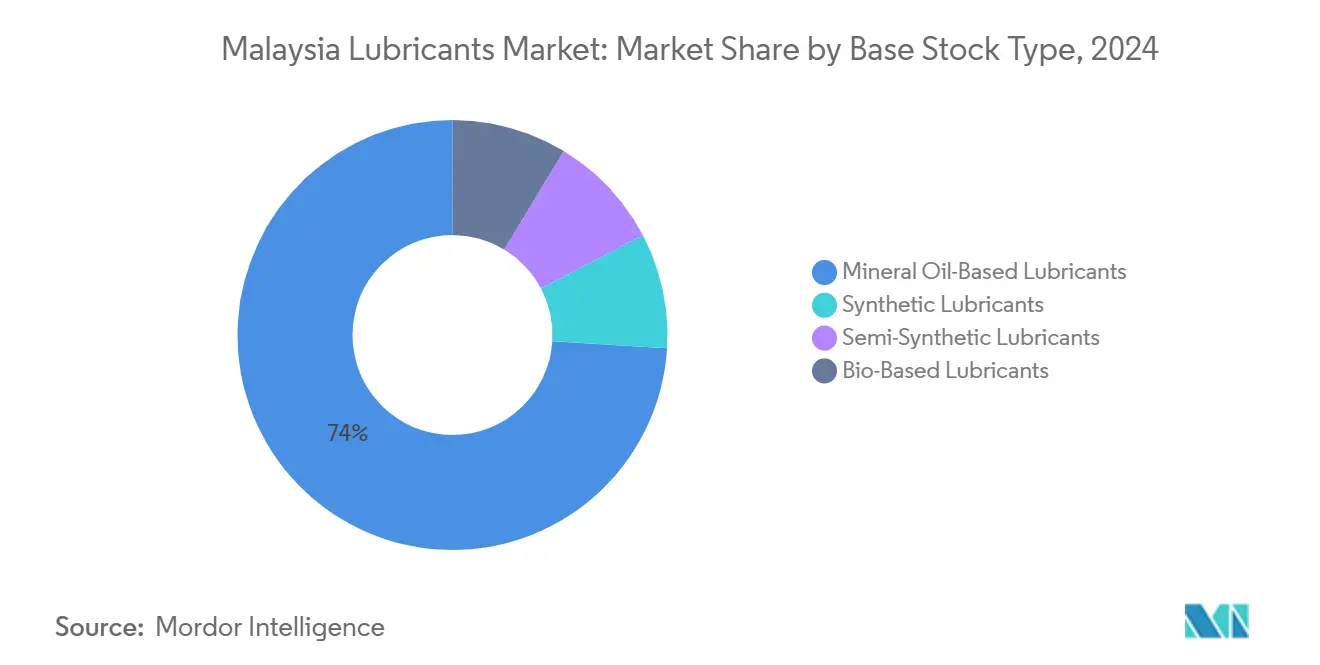

- By base-stock type, mineral-oil grades captured 74.02% of the Malaysian lubricants market size in 2024; however, synthetic formulations are projected to grow at a 2.17% CAGR through 2030.

Malaysia Lubricants Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle parc and new-car sales | +0.8% | National, concentrated in Peninsular Malaysia | Medium term (2-4 years) |

| Industrial and infrastructure expansion | +0.6% | National, with early gains in Johor, Selangor, Penang | Long term (≥ 4 years) |

| Shift toward synthetic/high-performance lubricants | +0.4% | National, premium segments in urban centers | Long term (≥ 4 years) |

| Government mega-projects under 12th Malaysia Plan | +0.3% | National infrastructure corridors | Medium term (2-4 years) |

| E-commerce emergence for lubricant retail (Tier-2 cities) | +0.2% | Tier-2 cities, rural distribution networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and New-Car Sales Drive Sustained Demand

Total vehicle sales reached 816,747 units in 2024, a 2.1% gain that supports lubricant volume growth despite market maturity[1]Malaysian Automotive Association, “Total Industry Volume 2024,” maa.org.my. Passenger cars already outnumber two-wheelers, so demand shifts toward higher-grade automotive engine oils rather than motorcycle lubricants. The implementation of Euro 5 fuel standards prompts workshops and motorists to switch to low-sulfur, full-synthetic formulations that protect catalytic after-treatment systems. Commercial vehicles also contribute because larger sump capacities and stricter fleet maintenance schedules offset slower passenger-car sales growth. Industry associations expect continuous parc expansion through 2030, particularly in the Klang Valley, Penang, and Johor, anchoring base-level consumption.

Industrial and Infrastructure Expansion Under 12th Malaysia Plan

Malaysia aims to create 700,000 high-skill manufacturing jobs by 2030 and double its high-tech export share to 6%[2]ASEAN+3 Macroeconomic Research Office, “NIMP 2030 and Semiconductors,” amro-asia.org. Semiconductor, electronics, and petrochemical projects require reliable hydraulic fluids, metalworking fluids, and process oils that withstand stringent clean-room or high-temperature environments. Manufacturing investments reached RM152 billion in 2023, with foreign investors accounting for nearly 70% of the chemical sector's capital inflows, indicating confidence in continued industrial growth. Infrastructure projects, such as the Johor-Singapore Special Economic Zone, East Coast Rail Link, and Pengerang Integrated Complex, increase lubricant demand for construction machinery, heavy-duty engines, and petrochemical equipment throughout the build-out phase and in routine plant operations.

Synthetic and High-Performance Lubricant Adoption Accelerates

Turbocharging, direct injection, and tightened emissions rules require low-volatility, high-temperature-stable lubricants. Euro 5 compliance forces workshops to recommend low-SAPS and low-sulfur products that resist oxidation while protecting after-treatment systems. PETRONAS introduced the Iona e-fluid series in 2025 to serve EV transmissions, battery thermal management, and specialty greases. Academia has confirmed that nanoparticle-enhanced palm-oil esters can cut friction by 26-34%, presenting local feedstock pathways for sustainable high-performance grades. This shift improves average unit value even as total liters sold rise slowly.

Government Mega-Projects Create Infrastructure Lubricant Demand

The 12th Malaysia Plan allocates multi-billion-ringgit outlays across roads, mass transit, and industrial corridors. Pengerang Integrated Complex received RM7.5 billion and hosts world-scale refining and petrochemical assets that both consume and manufacture base oils. Heavy-equipment fleets engaged on rail lines, industrial zones, and port expansions need hydraulic fluids, gear oils, and greases with high load-carrying capacity and all-weather operability. Sabah and Sarawak mining developments similarly depend on severe-duty engine oils for excavators and haul trucks. The National Energy Transition Roadmap adds niche demand for turbine oils and dielectric fluids used in wind and grid-scale battery installations.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer oil-drain intervals and engine efficiency gains | -0.4% | National, accelerated in urban areas with newer vehicles | Medium term (2-4 years) |

| Accelerating electric-vehicle adoption | -0.3% | National, concentrated in Klang Valley and major cities | Long term (≥ 4 years) |

| Crude-oil price volatility pressuring margins | -0.2% | National, affecting all market participants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Longer Oil-Drain Intervals Constrain Volume Growth

Modern synthetics enable drain intervals of 15,000-20,000 kilometers on a single fill, compared with 5,000-10,000 kilometers for older mineral formulations. This sharply lowers annual liter consumption per vehicle, even though the number of kilometers driven continues to rise. Fleet managers rely on in-service oil analysis to extend drains without compromising warranty coverage. Consequently, volume erosion within entry-level mineral categories offsets gains from the rising car population, and producers bolster revenues by marketing higher-margin full synthetics. Workshops adapt by offering bundled services—such as filter changes, alignment, and cabin-air filtration—to compensate for reduced lubricant frequency.

Electric Vehicle Adoption Reshapes Long-Term Demand Patterns

Despite a low current market share, federal incentives and the expansion of charging networks are accelerating adoption in major cities. EVs remove conventional engine oil demand but create needs for e-gear oils, dielectric coolants, and greases engineered for electromagnetic compatibility. PETRONAS, Grantt, and several independents launched EV-specific fluids in 2024-25 to address this emerging segment. Heavy-duty electrification lags because payload and range constraints still favor diesel; therefore, diesel engine oils remain a stable backbone of the Malaysia lubricants market through the forecast horizon.

Segment Analysis

By Product Type: Automotive Engine Oil Dominance Faces Transmission Fluid Growth

Automotive engine oil accounted for 51.05% of the Malaysia lubricants market share in 2024. A large and growing car population sustains baseline demand, while stricter OEM specifications accelerate the migration from API SN to SP and ILSAC GF-6 categories, which offer higher oxidative stability. Transmission fluids are the fastest-growing product, registering a 2.55% CAGR as automatic, dual-clutch, and continuously variable gearboxes proliferate. Hybrid vehicles further expand this need due to dedicated e-transmission lubrication circuits. The Malaysian lubricants market size, linked to hydraulic fluids, metalworking fluids, and process oils, also rises because semiconductor plants, precision machining centers, and chemical complexes require contamination-free operations and extended fluid life.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Automotive Leadership Challenged by Industrial Growth

Automotive applications retained a 70.13% share in 2024, reflecting the high passenger-car base and routine maintenance culture among Malaysian drivers. Industrial demand grows at the fastest rate of 2.92% CAGR as investors pour capital into electronics assembly, data center infrastructure, and chemicals. The Malaysian lubricants market size for heavy equipment includes hydraulic and gear oils used in construction machinery, as well as on rail, power, and port projects. Marine consumption is steady thanks to bunkering activities in Port Klang and offshore exploration and production operations in Sabah and Sarawak. Aerospace and MRO volumes remain comparatively small but contain stringent quality requirements that elevate unit values.

By Base Stock Type: Mineral Oil Dominance Faces Synthetic Transition

Mineral oil grades represented 74.02% of the total liters in 2024, due to their lower cost per change and wide availability. Synthetic volumes climb at a 2.17% CAGR as OEMs shift warranty specifications and motorists prioritize fuel efficiency. Semi-synthetics cater to cost-sensitive segments that require partial performance gains, bridging the transition. Bio-based lubricants, anchored in palm-oil esters, remain a niche market but demonstrate functional parity in flash point and viscosity index tests, offering a path toward sustainable sourcing when supported by RSPO certification and localized additive packages.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Peninsular Malaysia contributes the bulk of consumption, led by the Klang Valley, where high vehicle density, industrial parks, and port traffic converge. Johor’s lubricant demand accelerates alongside the Pengerang complex and cross-border trade with Singapore. Northern states, such as Penang, benefit from electronics manufacturing clusters, driving up precision metalworking fluid volumes. Sabah and Sarawak have specialized needs for marine, mining, and upstream oil service lubricants, although distribution costs are higher due to the distance. E-commerce adds incremental reach into Tier-2 towns and rural areas, smoothing regional disparities in product availability.

Competitive Landscape

The Malaysia Lubricants Market is consolidated in nature. PETRONAS retains domestic leadership through end-to-end integration that spans crude production, base-oil refining, blending, and retailing across its national service-station footprint. Shell, ExxonMobil, Castrol, and Chevron maintain strong brand equity and broader OEM endorsements, fueling intense rivalry in passenger-car and heavy-duty segments. Shell’s adoption of PurePlus gas-to-liquid technology for API SQ compliance differentiates its top-tier engine oils. Local blenders such as UMW Lubetech, which commissioned a 60 million-liter facility in 2023, compete on price and customized formulations, particularly in industrial oils and greases.

Malaysia Lubricants Industry Leaders

-

Shell plc

-

Petroliam Nasional Berhad (PETRONAS)

-

BP Plc (Castrol)

-

Exxon Mobil Corporation

-

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: BP Plc initiated the sale of its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader divestment strategy targeted for completion by 2027.

- May 2025: PETRONAS Lubricants International signed an exclusive deal with Quaker Houghton to distribute metalworking fluids across Malaysia’s transportation and industrial sectors.

Malaysia Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Malaysia lubricants market in 2025?

Total demand equals 519.19 million liters in 2025, on course for 564.01 million liters by 2030 at a 1.67% CAGR.

Which product sells the most?

Automotive engine oil leads with 51.05% share in 2024, reflecting the country’s large passenger-car base.

What segment is expanding fastest?

Transmission fluids are set for the quickest gain, posting a 2.55% CAGR through 2030 because advanced gearboxes need specialized fluids.

Why are synthetics growing in Malaysia?

Euro 5 fuel standards, turbocharged engines, and longer drain intervals push workshops toward full-synthetic oils that resist oxidation and protect after-treatment systems.

How will EVs change lubricant demand?

EVs reduce the volume of engine oil yet create new needs for e-transmission, cooling, and dielectric fluids, prompting suppliers to launch dedicated e-fluid lines.

Who dominates distribution?

PETRONAS holds the widest retail footprint, but e-commerce platforms increasingly serve Tier-2 cities and rural workshops with next-day lubricant delivery.

Page last updated on: